Healthcare Financial Reporting

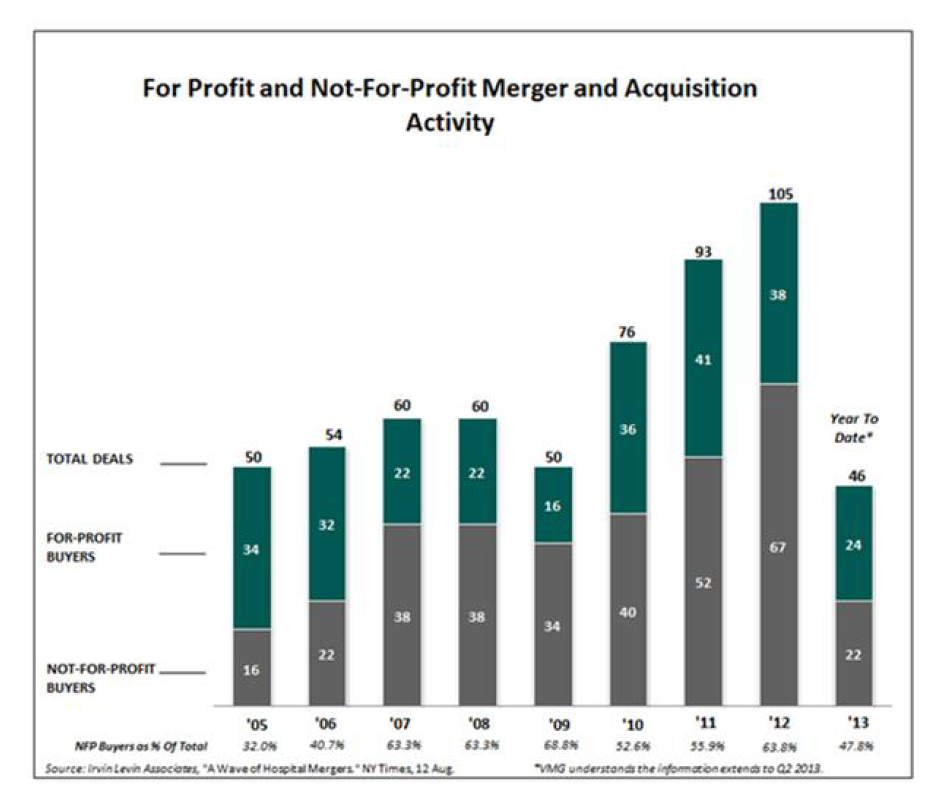

Over the past several years, M&A activity in the hospital sector has increased to a level not seen since the 1990s. The consolidations are being driven by many forces, not least of which is the Affordable Care Act (“ACA”), and much of this consolidation is occurring with not-for-profit health systems. As the chart below indicates, not-for-profit buyers have been more active than for-profit buyers since 2007.

This current wave of consolidations has created financial reporting implications for the not-for-profit buyers, making it critical for not-for-profit operators to have a thorough understanding of Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) 958, not-for-profit entities and ASC 805, business combinations (“ASC 958-805”) and the associated valuation issues.

Overview of ASC 958-805

In January of 2010, FASB issued Accounting Standards Update No. 2010-07, which recodified FASB Statement 164 to ASC 958-805. According to FASB, the purpose of this statement is to: “Improve the relevance, representational faithfulness, and comparability of the information that a not-for-profit entity provides in its financial reports about a combination with one or more other not-for-profit activities.”

The key provisions outlined in this standard are as follows:

- Provides guidance on determining whether a combination is a merger or an acquisition

- Requires the carryover method be utilized in accounting for a merger

- Requires the acquisition method be utilized in accounting for an acquisition and provides guidance to determine which of the combining entities is the acquirer

- Amends ASC 350, Goodwill and Other Intangible Assets, to make it fully applicable to not-for-profit entities

According to ASC 958-805, the accounting requirements differ depending on whether a combination of a not-for-profit entity is considered to be a merger or an acquisition. A merger occurs when the governing bodies of the combining entities cede control and, in turn, create a new governing body that will control the newly combined entity. The carryover method is utilized to account for a merger. This method involves the combination of the book values of the assets and liabilities of the merging organizations as of the merger date.

In the case of an acquisition, the acquisition method is used. The criteria used to determine if the transaction is an acquisition are as follows:

- Acquirer obtains control of one or more acquiree activities or businesses

- Acquirer often dominates the negotiations and terms of the transaction

- Acquirer has a disproportionate board representation

- Acquirer retains more key officers

- Acquirer’s bylaws, operating policies and practices are substantially unchanged

- Acquirer is financially stronger

- Acquiree is in financial distress

- Acquirer is substantially larger in terms of revenue, assets or net assets

Not-for-Profit Affiliations and the Accounting Implications

The consolidation of not-for-profit hospitals often occurs through an affiliation (also referred to as a member substitution). An affiliation refers to a transaction among not-for-profit hospitals where one organization becomes the corporate member of the other hospital or health system’s parent organization. In an affiliation, the acquiree typically gives up control.

Not-for-profit affiliations are treated as an acquisition for financial reporting purposes under the guidance of ASC 958-805. ASC 958-805 utilizes the premise of “fair value.” Fair value is defined by ASC 820, Fair Value Measurements and Disclosures, as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants. Fair value is a market-based measurement, rather than an entity specific measurement, and is measured using assumptions that market participants would use in pricing the hospital, including assumptions about risk.

An affiliation does not have an agreed upon fair value purchase price (in most cases the acquirer simply assumes the acquiree’s balance sheet); therefore, the first step of the analysis is to determine the fair value of the business enterprise of the acquiree (i.e., what would the hypothetical purchase price been had the hospital been sold). This hypothetical purchase price is then allocated to the identifiable tangible and intangible assets of the acquiree.

Typically, book value is utilized as a proxy for fair value for working capital and investment assets. A third-party valuation firm is retained to assist management with the determination of the fair value of the business enterprise, the personal property (exam tables, patient beds and medical equipment), the real property (land and buildings) and the intangible assets (certificate of need, trade names and non-compete agreements).

Conclusion

As the challenges in the hospital sector continue, not-for-profit hospitals will take proactive measures to align themselves with other like-minded systems so they can continue their mission and provide patient care in their communities. This will result in continued acquisition activity, which, in turn, will increase the need for not-for-profit healthcare systems to comply with ASC 958-805.