Written by Ash Midyett, CFA; William Teague, CFA, CVA

After a multi-year drought, the healthcare services industry has helped lead the way in re-opening the initial public offerings (IPO) market, contributing half of the top 10 largest IPOs of the year. In July alone, Ardent Healthcare (ARDT) and Concentra (CON) filed back-to-back IPOs, raising $192 million and $529 million respectively. Ardent Healthcare marks the first traditional health system to IPO in decades, and in this article, we will discuss the company’s performance and offering compared to that of its public peers.

Historical Financial Performance

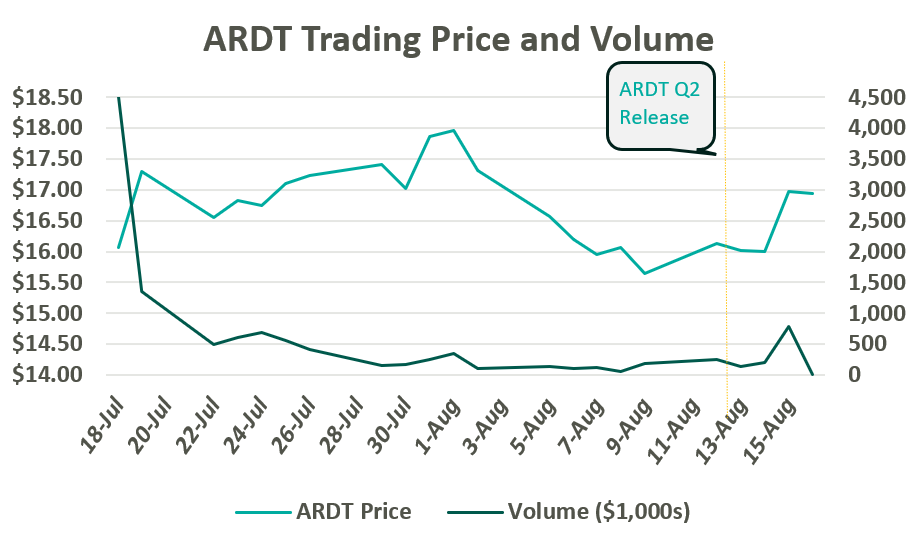

On July 19, Ardent Healthcare listed 12 million common shares on the New York Stock Exchange at $16 per share. After accounting for options granted to underwriters, the proceeds generated $209 million, which is expected to be allocated towards debt repayment and future acquisitions. The IPO marks a notable downshift from their initial price target of $20-$22 per share. Since trading, ARDT moved up toward a peak close of $17.97 before returning to $16.00 per share following a global market sell-off in the first week of August. Following Ardent Healthcare’s Q2 Earnings release on August 14, their shares jumped 6% to $16.97.

Since the company’s founding in 2001, Ardent Healthcare has grown into the fourth largest, for-profit hospital operator and healthcare services provider in the United States. The company currently operates 30 acute care hospitals and over 200 sites of care. Its market footprint spans eight mid-sized, urban markets across six states: Texas, Oklahoma, New Mexico, New Jersey, Idaho, and Kansas.1,2

Strategy

Ardent Healthcare is listed as a “Controlled” company, meaning control and shareholder rights are concentrated with the company’s private equity sponsor, EGI-AM Investments, L.L.C. EGI-AM Investments acquired Ardent Healthcare in July 2015 and has since supported an aggressive business development strategy characterized by scale and leverage. From 2015 to 2018, Ardent Healthcare nearly tripled its operating revenue through the acquisition of 16 hospitals and 95 other sites of care while generating margins between 6% and 10%. While Ardent Healthcare aggressively expanded its footprint, the company simultaneously divested most of its real estate to an affiliated REIT, Ventas, Inc.

Ardent Healthcare’s inorganic growth is primarily attributable to three large joint ventures, which exemplify the company’s established business development strategy. In March 2017, Ardent Healthcare acquired five hospitals from LHP Hospital Group, Inc. and, in turn, established a joint venture with the University of Kansas Health System. The acquisition was quickly followed by the acquisition of St. Francis Health Center in Topeka, KS in May 2017. Within a year, Ardent Healthcare made its largest acquisition to date and acquired a majority stake in 10 hospitals and 39 clinics from East Texas Medical Center Regional Healthcare System, a subsidiary of the University of Texas Health System during March 2018.

Valuation Observations

All three acquisitions adhere to Ardent Heathcare’s purported strategy of founding joint ventures with established, not-for-profit and academic health systems located within growing, mid-sized markets.

During its expansion period, the Company sold off most of its real estate to Ventas, Inc. and other affiliated REITs while paying out significant distributions to shareholders. In July 2015, Ardent sold the real estate for 10 acute-care hospitals to Ventas for $1.75 billion, shortly followed by a special distribution of $500 million to shareholders. Between 2018 and 2020, Ardent Healthcare sold off the real estate for 14 skilled nursing facilities and the three more acute-care hospitals for a total of $1 billion. Meanwhile, Ardent Healthcare paid out an additional $950 million in special dividends.

Real estate lease backs are nothing new to the healthcare services industry, but Ardent Healthcare marks the first publicly traded healthcare services company to pursue this strategy at scale. The cash infusion from the sale represents an opportunity to optimize capital structure via debt repayment, reward shareholders, and equip the company with dry powder to pursue future acquisitions. Meanwhile, real estate can trade independently with the oversight of a specialized management team. However, the lease backs also add operational leverage, adding a fixed rental expense to the income statement, similar to fixed interest on a loan.

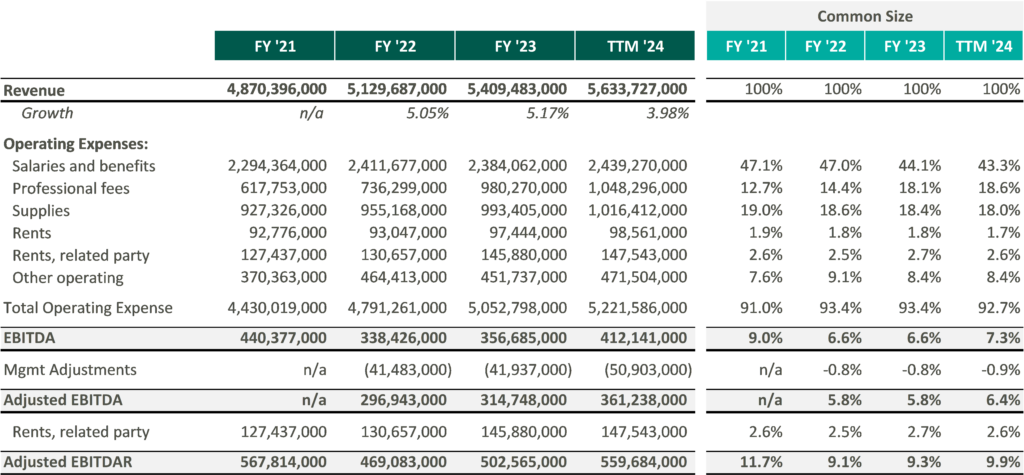

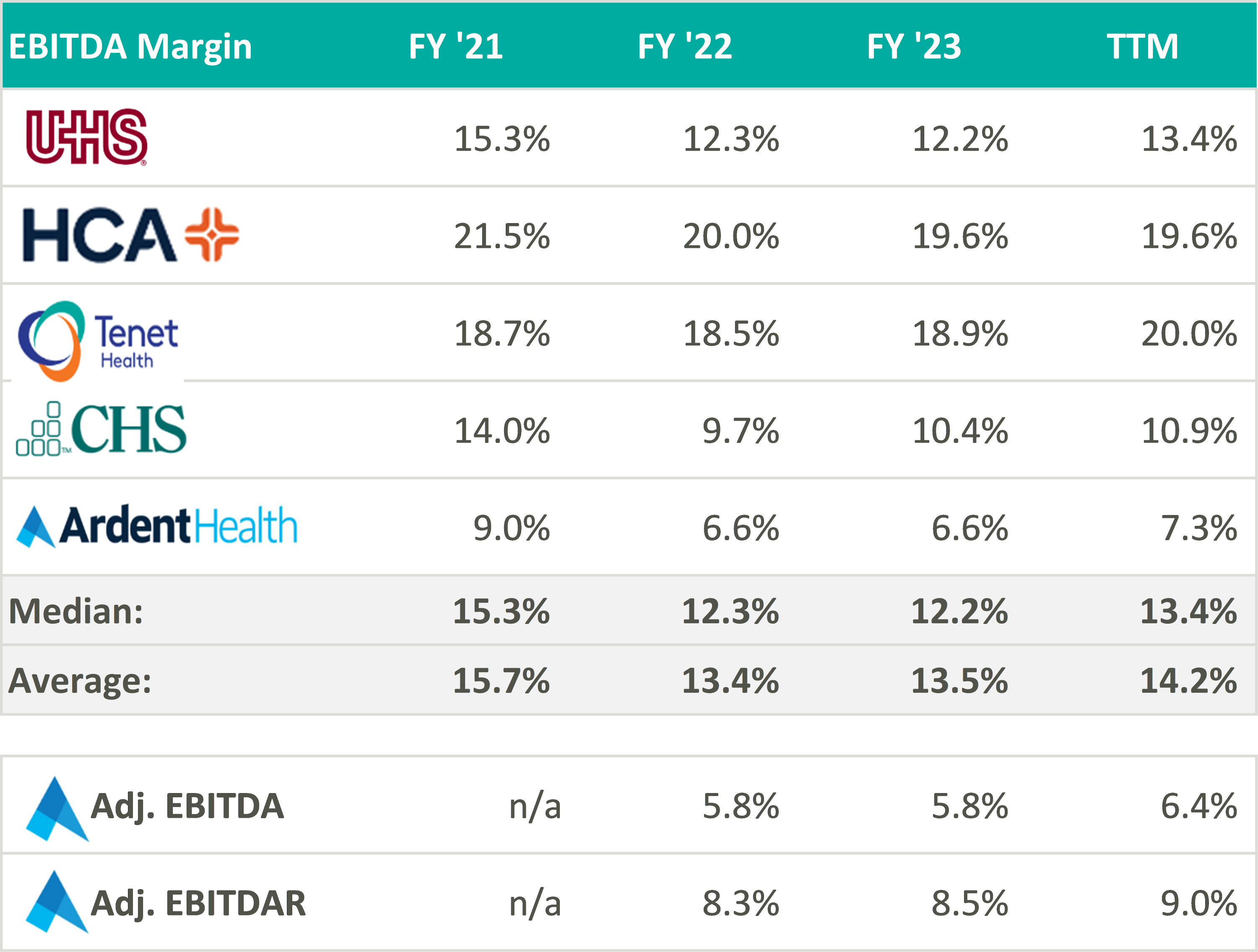

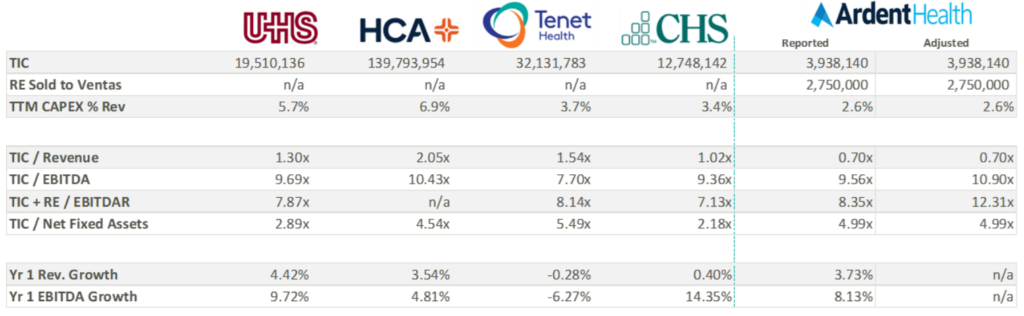

In recent marketing materials, Ardent Healthcare has advocated for analysts and investors to consider their valuation in relation to its EBITDAR multiple rather than EBITDA because of its unique expense structure. However, after accounting for rental expenses, Ardent Healthcare’s margins fall below those of its peers thereby increasing free cash flow volatility.3

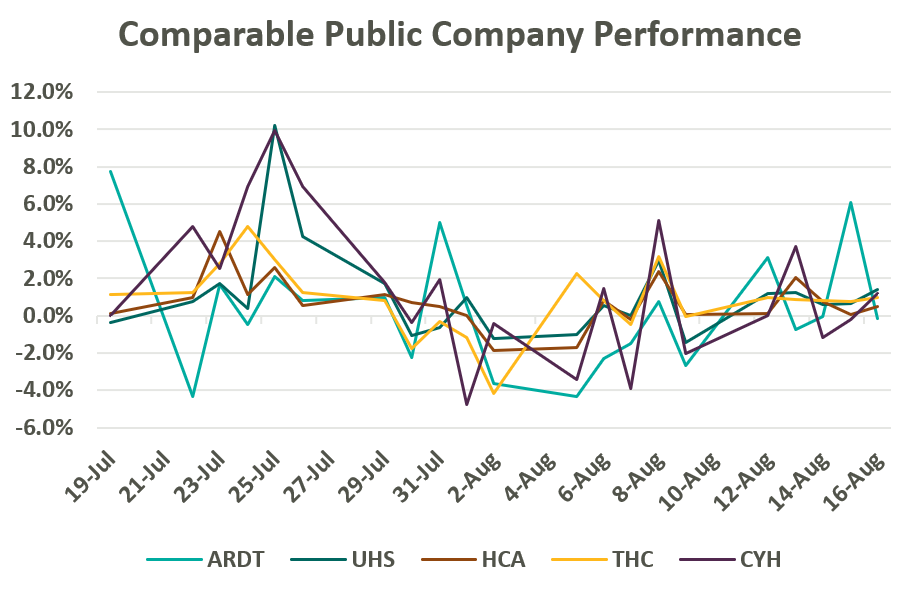

Despite lower margins and a higher-risk balance sheet, Ardent Healthcare’s implied trading multiple remains in line with its peers (or above after management adjustments to EBITDA): United Health Services (UHS), HCA Healthcare Inc. (HCA), Tenet Healthcare Corporation (THC), and Community Health Systems (CYH). As of August 19, Ardent Healthcare’s market capital roughly implies a 9.5x reported EBITDA multiple compared to the peer group median of 9.3x reported EBITDA.4

Over the three most recent fiscal years, Ardent Healthcare has reported capital expenditures well below those of its peers. All things equal, a lower capital expenditure increases cash flow to equity and thereby increases valuation—not to mention bolstering distributable free cash flow for shareholders. While some of the discrepancy in capital expenditure may be attributable to Ardent Healthcare’s asset light balance sheet, Ardent Healthcare’s lease agreement with Ventas stipulates a triple net lease obligation. It is possible that the company may be beholden to higher capital investment in the coming years, decreasing cash flow and shareholder value.

Perhaps more important to value is the company’s growth expectations, which currently appear elevated compared to peers. As seen in the table above, analysts are anticipating an 8% increase in EBITDA over the coming year compared to the peer group median of 5.5%. Three-year growth expectations considerably outpace peers as the company gains scale and increases revenue.

Conclusion

Ardent Healthcare’s growth strategy, outlined in its recent S-1 filing, will be key to growing market share, scale, and margin to best compete and grow into its current valuation. Specifically, Ardent Healthcare’s inorganic growth strategy remains focused on expanding its portfolio of joint ventures and has identified an addressable market of nearly 350 mid-sized, urban communities. Ardent Healthcare also intends to embolden its ACO participation and value-based care programs while accelerating their ambulatory and physician alignment initiatives (with eight new ambulatory surgery centers added in Q2 alone). Coming off a strong quarter, Ardent Healthcare certainly has ample opportunity to expand its stated 3% market share and continue providing high-quality care to its patients. VMG Health looks forward to following the company’s performance in the coming quarters.