Since the start of the current administration, public markets have been flooded with a wave of policy changes and macroeconomic signals—from newly imposed tariffs to legislative reforms under the One Big Beautiful Bill (OBBB) to shifting interest rate dynamics. The surge in policy and economic changes has created a noisy environment for operators and investors alike, particularly in the healthcare sector. VMG Health analyzed public healthcare companies’ performances in Q2 2025 by comparing key financial metrics before and after earnings releases to assess their impact on future outlook and market behavior. As changes in equity prices for publicly traded companies can be observed daily, the markets can be an early indicator to inform valuation within the healthcare sector.

Methodology

VMG Health tracked 16 companies across three subsectors: acute care hospitals, post-acute care, and other healthcare operators. For each company, we reviewed reported Q2 performance, equity analyst expectations, and management’s outlook on full–year guidance. Additionally, we reviewed the change in enterprise value, consensus EBITDA, and implied forward multiples, as defined below, from July 21, 2025 (start of Q2 2025 earnings season) to August 29, 2025. We then quantified the impact to enterprise value for each of the identified companies in Exhibit A, resulting from fluctuations in EBITDA as compared to the implied forward multiple over the observed period.

Key Definitions

- EBITDA: Equity analyst consensus EBITDA estimates of a company’s expected operating earnings for fiscal year 2025 (FY+1) as reported by S&P Capital IQ on the observation date*

- Enterprise Value: The market value of equity plus interest‐bearing debt (excluding right-of-use liabilities) and minority interest less cash and cash equivalents

- Implied Forward Multiple: [Enterprise Value] ÷ [FY+1 Consensus EBITDA Estimates]

*Note: VMG Health relied on S&P Capital IQ for the FY+1 consensus EBITDA estimates as of July 21, 2025 and August 29, 2025. VMG Health understands all 16 companies report on a calendar year end. Therefore, FY+1 EBITDA represents FY 2025 and FY+2 EBITDA represents FY 2026. The consensus EBITDA as of 8/29 is primarily based on analyst estimates following companies’ Q2 2025 earnings calls.

Key Observations: Earnings

- Fifteen out of 16 companies beat analyst expectations, delivering higher EPS against consensus during the quarter.

- Ten out of 16 companies revised full-year EBITDA guidance, while six out of 16 companies either reaffirmed full-year EBITDA guidance or remained silent.

- Eight out of 10 companies revised full-year EBITDA guidance upward.

- Two out of 10 companies revised full-year EBITDA guidance downward.

- Sixteen out of 16 companies had higher Consensus EBITDA estimates for fiscal year 2026 (FY+2).

Key Observations: Sectors

Acute Care

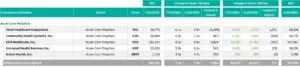

Among the publicly traded acute care hospital operators, Tenet Healthcare Corporation, HCA Healthcare, Inc. and Universal Health Services, Inc., revised full-year EBITDA guidance upward in their Q2 earnings release. Between July 1, 2025 and August 29, 2025, VMG Health observed a direct correlation between revised EBITDA guidance and analyst consensus EBITDA estimates for FY 2025, with increased consensus EBITDA estimates for these three hospital operators. Community Health Systems, Inc., on the other hand, revised full-year EBITDA guidance downward, with a correlated decrease in consensus 2025 EBITDA estimates between July 1, 2025 and August 29, 2025.

Collectively, enterprise value for the acute care hospital sector increased by approximately 4.1%, or $7.7B, driven by both an increase in consensus EBITDA estimates and expansion in implied trading multiples. It is worth noting that all hospital operators outperformed consensus EPS expectations in Q2 2025, despite the regulatory headwinds resulting from tariffs, OBBB, and interest rate fluctuations.

Post-Acute Care

Within the post-acute care operators, Encompass Health Corporation and Enhabit, Inc. revised full-year EBITDA guidance upward, and Select Medical Holdings Corporation reaffirmed full-year EBITDA guidance. Analyst estimates for FY 2025 EBITDA increased considerably for Encompass Health Corporation between July 21, 2025 and August 29, 2025, while 2025 EBITDA estimates fluctuated slightly for Select Medical Holdings Corporation and Enhabit, Inc. during the same period. All three companies within the post-acute care sector outperformed consensus EPS expectations in Q2 2025. Enterprise value for the post-acute care sector increased by approximately 5.5%, or $7.7B, driven primarily by expansion in implied trading multiples.

Other Healthcare Subsectors

Of the other publicly traded healthcare operators observed, Concentra Group Holdings Parent, Inc. is the company that did not meet consensus EPS expectations in Q2 2025. U.S. Physical Therapy, Inc.; Concentra Group Holdings Parent, Inc.; and RadNet, Inc. revised full-year EBITDA guidance upward in the Q2 earnings release. Acadia Healthcare Company, Inc. revised full-year EBITDA guidance downward, and all other companies either reaffirmed full-year EBITDA guidance or remained silent. VMG Health observed increases and decreases in FY 2025 EBITDA estimates for the other healthcare operators. Overall, enterprise value increased by approximately 6.3%, or $5.7B, driven primarily by expansion in implied trading multiples.

Key Observations: Pricing

- Thirteen out of 16 companies had higher implied multiples from July 21, 2025 to August 29, 2025.

- Of the approximate $14.3B increase in enterprise value across all of the public companies analyzed, 68.1% of the increase is attributable to higher implied forward multiples.

Conclusion

The equity markets continue to react to macroeconomic factors. Most of the public companies analyzed currently have higher consensus EBITDA estimates for FY 2025, and the market appears to have expanded its appetite for valuations, as evidenced by the rise in the implied forward multiples. From the data above, it appears that public companies do not believe the regulatory uncertainty will have a near-term impact on financial performance.

Given the unpredictability of the future, few operators have quantified the long-term financial impact due to regulatory change. More importantly, the public companies’ valuations have not declined to date. Whether this increase in enterprise value is short-term in nature and the public markets will adjust valuations down in the long-term remains to be seen. As always, VMG Health will continue to monitor the public markets.

![]()

Contributors:

Kaitlin Heil & Maggie Perry