Hospital-based medicine is currently navigating a complex landscape marked by significant challenges, such as declining payer reimbursement, an aging population, staffing shortages, rising operating costs, regulatory changes, and shifts in site-of-service care delivery. These combined pressures are squeezing hospital margins and straining operational capacity, compelling hospitals to adopt strategic partnerships, expand ambulatory services, and embrace new technologies to sustain financial health and maintain access to quality care in a competitive environment. Among the various hospital departments, radiology faces unique impacts from these headwinds, including changes in imaging utilization, reimbursement pressures, and workforce challenges. Exploring how these factors specifically affect radiology can shed light on the strategic adaptations necessary to ensure their vital role in patient care continues uninterrupted.

Economic Pressures Are Reshaping the Landscape

Independent radiology groups are feeling the squeeze. Declining reimbursement rates are eroding margins, even as physician productivity rises. Many organizations are discovering a disconnect between benchmarked and actual collections per wRVU, making it harder to negotiate sustainable contracts.

Median Reimbursement Increase Required Over Prior Medicare Physician Fee Schedules

- Source: American College of Radiology Medicare Physician Fee Schedule impact tables for 70,000 and non-70,000 code series

- CPT codes as listed in the ACR’s CPT code impact tables were classified in accordance with the modality crosswalk published by the National Radiology Data Registry

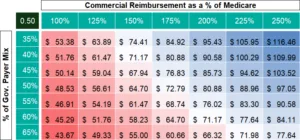

Lower work to total RVU ratios experienced in radiology (~0.70 work to total wRVU ratio), coupled with elevated governmental populations, requires organizations to negotiate very competitive commercial contracts. To remain viable, commercial agreements must now exceed 200–225% of Medicare rates to achieve sustainability without support payments.

A Shrinking Workforce Meets Rising Demand

Approximately 30% of the active 29,000 radiologists in the U.S. are above the age of 65, and an aging population adds to the demand for imaging services. Meanwhile, the number of residency positions has remained flat for decades. Industry forecasts project cumulative imaging volume growth of approximately 10%–15% over the next decade, with higher growth in advanced modalities like CT, PET, and ultrasound.

Remote Work & Teleradiology: The New Normal

Radiology is leading the charge in remote care delivery. Most U.S. hospitals now use teleradiology, expanding well beyond overnight “nighthawk” coverage to serve as a routine daytime solution to address subspecialty access gaps, geographic disparities, and staffing shortages. Secure home setups, AI integration, and centralized workflow tools are enabling radiologists to work flexibly while maintaining high standards of care. This shift is helping address workforce shortages and changing the value proposition of exclusivity.

Interventional Radiology Faces Competitive Pressures

Cardiology, vascular surgery, and oncology are increasingly performing procedures once dominated by interventional radiologists. Reimbursement often undervalues the complexity of interventional radiology work, and fewer residents are choosing the specialty due to long hours and high liability.

Given the competition and subsequent narrowing scope of practice many interventional radiologists need to supplement collections from interventional procedures through some combination of the following:

- Diagnostic radiology: In many instances, diagnostic volumes represent upwards of 80% of an interventional radiologist’s patient volume.

- Hospital support payment: Given collections alone generally don’t offset the cost of coverage; many health systems provide interventional radiologists with revenue guarantees or supplemental stipends to support competitive practice economics.

- Coverage arrangements: In lieu of a collections guarantee or stipend, health systems will directly contract with interventional radiologists to pay for call coverage.

Independent Imaging Groups: Financial Strain Intensifies

VMG Health Market Observations

As radiology continues to evolve amid shifting economic pressures and care delivery models, hospital systems must take a proactive stance in adapting their operational strategies. The limitations of the current survey data—particularly regarding work standards, such as onsite versus remote and day shifts versus night shifts—highlight the need for more nuanced analysis when evaluating service costs. Early organizational preparation is essential to mitigating financial risks and safeguarding community access to care. Moreover, the traditional value of exclusivity has waned as remote work rises, weakening individual physicians’ ties to specific markets. To ensure service stability and affordability, institutions must reevaluate standards around onsite presence, turnaround times, and high-volume reads, ultimately aiming to redefine value in a way that benefits all stakeholders.

![]()

Navigating radiology workforce challenges and reimbursement pressure can be difficult without the right partner. Contact VMG Health for help evaluating coverage models, contract structures, and operational strategies that support long-term sustainability.