Behavioral health providers are at an inflection point. Demand for services has surged in the wake of the COVID-19 pandemic, yet the sector continues to be hampered by chronic underinvestment, rising wage expectations, and uncertain Medicaid funding. Hospitals, community mental health centers, and residential treatment facilities are confronting a challenging paradox: The nation needs more behavioral health services than ever, but the financial and staffing models to support them are under severe strain. A thoughtful, data-informed behavioral health strategy is more critical than ever.

Bed Need & Infrastructure Gaps

Across the country, there is a persistent shortage of inpatient psychiatric beds, even in regions with stable or modest population growth. Recent market-level analyses demonstrate a growing mismatch between community behavioral health needs and inpatient bed supply. In a sample of metro areas studied by VMG Health, behavioral bed capacity falls short of estimated need by as much as 90–325 beds, or 15–40%, depending on methodology. The figure below illustrates estimated dedicated inpatient behavioral health bed shortages in select metro areas, based on a blended methodology.*

Bed Need

* Bed need estimates reflect a blended approach using (1) a fixed ratio of 40 beds per 100,000 CBSA residents and (2) incidence-based modeling that applies age-specific rates, average lengths of stay, and an 80% target occupancy rate.

The demand for inpatient behavioral health services is rising steadily, driven by high and increasing prevalence of mental illness (more than 25% of adults in many states report experiencing “any mental illness”). Pediatric and geriatric patients represent a disproportionate share of the unmet need, placing added pressure on a fragmented system. Many communities lack hospital-based psychiatric departments altogether, and despite widening gaps in access, there are no significant public expansion plans underway. The result is a growing shortfall in psychiatric beds, particularly in areas already operating well below the commonly cited benchmark of 40 beds per 100,000 residents. Without matching capital investment, patients continue to face long waits in emergency departments or skip care entirely.

Compensation Trends & Workforce Shortages

Behavioral health providers face acute labor shortages across nearly all roles, with 24/7 coverage models proving especially difficult to sustain. Compensation rates have risen steadily, driven by burnout, competition from other sectors, and rising demand, but many roles remain hard to fill. Occupancy remains high (73–85%), further compounding staffing strain and operational risk.

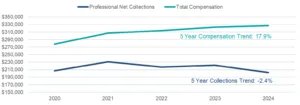

Compensation Trends

Notable Trends:

- Compensation for behavioral health clinicians has increased 15–20% over the past five years, driven by competitive markets, low provider supply and stagnant, fragmented funding.

- Behavioral facilities report particularly acute shortages in child/adolescent and geriatric psychiatric roles, where staffing models are complex and reimbursement is often lower.

- Turnover is high (30–60%) among clinicians and support staff, especially for overnight and weekend shifts.

- Without thoughtful workforce planning, wage investment, and operational redesign, organizations risk further capacity constraints, despite physical infrastructure growth.

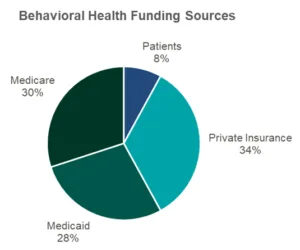

Medicaid Funding Uncertainty

Medicaid remains the dominant payer for behavioral health services in the U.S., particularly for inpatient psychiatric care. In most markets, Medicaid and other public sources (e.g., Medicare, supplemental state funding) represent the majority of behavioral health revenue. This overreliance creates significant vulnerability to policy changes.

Providers are particularly exposed to:

- Potential changes to enhanced federal Medicaid funding or Section 1115 waivers

- State-by-state variability in behavioral health reimbursement

- Growing reliance on supplemental or non-base payments that may not be sustainable long-term

Given that many behavioral health facilities are already operating at or above 80% occupancy, any disruption in public reimbursement could quickly strain operations, lead to service line closures, or force consolidation with larger systems.

Implications include:

- Margin pressure in publicly funded facilities

- Deferred expansion of new services or beds

- Increased M&A activity or provider exits in vulnerable markets

Strategic Takeaways

Proactive Workforce & Funding Strategies Are Critical for System Resilience

Organizations are actively adapting to these compensation and staffing challenges, particularly for hard-to-fill and 24/7 roles, by implementing differentiated pay models, flexible staffing approaches, and investing in talent pipelines. Simultaneously, many are working to stabilize revenue through Medicaid advocacy, diversified payer strategies, and predictive financial planning.

Infrastructure & Partnership Strategies Are Emerging as Catalysts for Sustainable Growth

Recognizing that infrastructure investment and modernization are essential to meet rising demand, leading systems are prioritizing behavioral health bed expansion and tech-enabled care models. New strategic relationships, including joint ventures and cross-sector partnerships, are also gaining traction as a method to share risk, expand access, and increase long-term viability without sacrificing clinical autonomy.

Conclusion

The behavioral health system is under growing strain, and without structural action, these pressures may accelerate into systemic breakdowns. Nationally, several urban and mid-size markets already project behavioral bed growth needs of 30–55% by 2035, with no corresponding surge in capital investment. At the same time, Medicaid funding (already essential to the sector’s survival) remains uncertain in many states. Meanwhile, staffing remains a key vulnerability, as demand for professionals far outpaces supply, and persistent burnout and turnover continue to slow recovery.

However, behavioral health providers are not without options. Forward-looking organizations are already taking strategic steps to adapt:

- Restructuring compensation models to better align incentives with market dynamics and care delivery realities

- Rethinking workforce strategies with a focus on retention, flexibility, and sustainable coverage models for inpatient and residential care

- Pursuing capital partnerships that enable growth while sharing risk

- Exploring new care delivery models that create additional access and make the best use of resources

With the right data, strategic alignment, and operational planning, organizations can position themselves to weather today’s challenges while laying the foundation for long-term resilience and growth.

VMG Health is actively working with several behavioral health providers to navigate this landscape, providing data-driven insights, compensation and workforce planning, partnership structuring, and financial modeling. Whether evaluating bed expansion, redesigning provider compensation, or planning for funding uncertainty, we help organizations build sustainable strategies rooted in operational and financial reality.

![]()

Contributor:

Reed Larson

References

Beidas, R. S., Stewart, R. E., Adams, D. R., Fernandez, T., Lustbader, S., Powell, B. J., … & Mandell, D. S. (2020). A repeated cross-sectional study of clinicians’ use of psychotherapy techniques during implementation of evidence-based practices in Philadelphia. Psychiatric Services, 71(1), 66–73. https://doi.org/10.1176/appi.ps.201900169

Counts, N. (2022, September 7). Behavioral health care in the United States: How it works and where it falls short [Explainer]. Commonwealth Fund. https://doi.org/10.26099/txpy-va34

Johnson-Kwochka, A., Wu, W., Luther, L., Fischer, M. W., Salyers, M. P., & Rollins, A. L. (2020). The relationship between clinician turnover and client outcomes in community behavioral health settings. Psychiatric Services, 71(1), 28–34. https://doi.org/10.1176/appi.ps.201900169

Kanner-Mascolo, M. (2025, May 5). Collaborating through a crisis: More than 50% of Central Mass. ER beds are taken up by mental health patients waiting for treatment. Worcester Business Journal. https://www.wbjournal.com/article/collaborating-through-a-crisis-more-than-50-of-central-mass-er-beds-are-taken-up-by-mental

Lutterman, T., Shaw, R., Fisher, W. H., & Manderscheid, R. (2017). Trend in psychiatric inpatient capacity, United States and each state, 1970 to 2014. National Association of State Mental Health Program Directors. https://www.nasmhpd.org/sites/default/files/TACPaper.2.Psychiatric-Inpatient-Capacity_508C.pdf

National Wraparound Implementation Center & National Wraparound Initiative. (2024). Addressing the behavioral health workforce crisis: Understanding the drivers of turnover and strategies for retention. University of Connecticut School of Social Work. https://innovations-socialwork.media.uconn.edu/wp-content/uploads/sites/3657/2024/02/Workforce-NWIC-NWI-Feb2024.pdf

Sisti, D. A., Segal, A. G., & Emanuel, E. J. (2022). The psychiatric bed crisis in the United States: Understanding the problem and moving toward solutions. American Journal of Psychiatry, 179(8), 586–588. https://doi.org/10.1176/appi.ajp.22179004

Treatment Advocacy Center. (2024). Prevention over punishment: Finding the right balance of civil and forensic state psychiatric hospital beds. Office of Research and Public Affairs. https://www.treatmentadvocacycenter.org/wp-content/uploads/2024/01/Prevention-Over-Punishment-Full-Report.pdf

Treatment Advocacy Center. (2024). Research summary 1.24: Psychiatric bed shortages and unmet needs in the U.S. Office of Research and Public Affairs. https://www.treatmentadvocacycenter.org/wp-content/uploads/2024/03/TAC_ORPA_ResearchSummary1.24.pdf