On March 3, Surgery Partners (NASDAQ: SGRY) reported a record-breaking $3.1 billion in annual revenue and $508.2 million in adjusted EBITDA while an open bid at $25.75 per share from Bain Capital to take the company private looms. While analysts might have anticipated clarity from the latest earnings release, negotiations remain open.

Bain’s initial investment in Surgery Partners at $19.00 per share back in 2017 is but one of many private equity investments over the past decade shaping the current market for ambulatory care, and recent acquisitions like TPG’s investment in Compass Surgical Partners in January of 2024, along with public interest from TPG, UNH, and Bain into Surgery Partners, continue reinforcing the strength of the physician hospital joint venture model.

Historical Context

On August 31, 2017, Bain acquired a 54.19% stake in Surgery Partners for $502.7 million alongside 100% equity in fellow ASC portfolio company, National Surgical Healthcare (NSH), for $760 million. NSH was then absorbed by Surgery Partners, resulting in a combined footprint across 32 states, comprised of 125 ambulatory surgery centers (ASCs) and surgical hospitals, roughly 60 physician practice locations, and ancillary assets such as urgent care centers and diagnostic laboratories.

Bain’s initial investment, management focused on portfolio oversight while developing a unified platform for strategic growth. As the company divested non-core assets like non-profitable surgical hospitals, optometry centers, and other ancillaries, it simultaneously positioned itself for a wave of musculoskeletal (MSK) procedures expected to migrate to outpatient settings, remaining one of the company’s primary organic growth drivers.

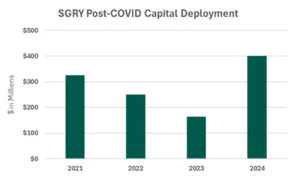

COVID-19 stalled initial attempts to go to market but by the winter of 2021, Surgery Partners announced it had raised $260 million in dry powder with the intent to deploy as much as $400 million in fiscal year 2021 at a sub 8x multiple on EBITDA. For context, the company had deployed $300 million over the prior three years in total. During 2024, Surgery Partners deployed $400 million.

As Surgery Partners executed its strategy of amassing scale to capitalize on the MSK transition, its playbook evolved to include de novo initiatives and partnerships with health systems like Parkview Health, Intermountain Health, Methodist Health System, and Ohio Health. Moreover, the company is positioning itself for an anticipated wave of cardiovascular surgeries to migrate to the outpatient setting.

From 2017 to Q3 2024, Surgery Partner’s adjusted revenue and EBIDTA grew 13.1% and 17.5%, respectively, on a compound annual basis while consistently growing into improved profitability. Despite consistent execution on behalf of management, the company’s common stock performance has been modest, returning roughly 142.4% in cumulative total return amidst significant market volatility compared to the S&P 500’s 156.1% and S&P 500 Health Care Providers & Services Index of 129.6%.

Surgery Partners Valuation Considerations

At its essence, valuation is the confluence of three factors: cash flow, growth, and risk. As valuation practitioners, we appreciate the simplicity of expressing valuation as a multiple of earnings, thereby allowing for a comparison of growth and risk across companies of differing earnings.

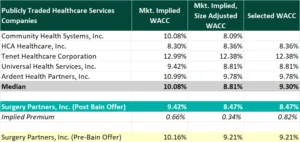

As a multiple of EBITDA, Bain’s offer implies 12.7x total invested capital. While there are few pure-play ASC comparables on the public market, the implied multiple is notably higher than those typically observed within the healthcare services industry.

Perhaps the most obvious reason for Surgery Partners’ premium to the broader healthcare services public market is its remarkable track record of growth. As volumes shift from inpatient to outpatient, the company is poised to benefit from industry-wide tailwinds further amplified by a relatively high debt load and aggressive, inorganic growth strategy. Analysts project SGRY’s EBITDA growth at 10.8%, 11.6%, and 11.2% over the next three years—significantly outpacing the 4.7%, 5.3%, and 5.7% expected growth rates of its peers.

As for risk, the market may be placing a modest premium on Surgery Partners as a pure-play ASC portfolio. Using the same analyst growth rate expectations as the current market implied total invested capital, Surgery Partners’ implied weighted average cost of capital (WACC) is approximately 82bps lower than that of its peers on a size-adjusted basis. All else equal, a cheaper cost of capital speaks to both the strength of the company’s market position and its pure-play ASC model.

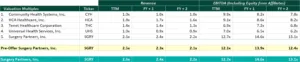

For simplicity, VMG’s analysis excludes cash flow and equity from minority interests as these items were not reported in the analyst forecasts relied upon. Additionally, VMG has assumed a blended federal and state income tax rate of 24.8% and a 10% of incremental revenue working capital requirement for all companies. VMG has chosen to exclude Community Health Systems in our consideration of the group median due to its significant debt load of roughly 29x equity.

Surgery Partners’ premium valuation aligns with similar ambulatory surgery center platform deals over the past decade, with a 11.76x median, suggesting the market consistently places a premium on pure-play ASC roll-up strategies.

Private Equity Investment Strategy

Roll-up strategies employed by private equity-backed portfolio companies like Surgery Partners require three central ingredients for success:

- Systemic tailwinds to support organic growth

- Multiple arbitrage

- Leverage

The ASC market is uniquely positioned to continue attracting PE involvement. With 11,521 ASCs nationwide—of which, approximately 6,300 are Medicare-certified—the market is diverse, with a near-even split between single-specialty and multi-specialty centers. The total addressable market is estimated to range from $130 billion. In such a fragmented ecosystem, portfolio companies like Surgery Partners can acquire individual ASCs at a lower multiple—often around 7–8x—while attracting outside capital at higher valuations due to their size, growth potential, diversified market, and professional management.

Moreover, the industry tailwinds favoring outpatient migration support this strategy. ASCs generate high levels of cash flow and operate in an inelastic, non-cyclical industry, making them attractive investments even during economic uncertainty. They offer an economical and beneficial alternative for patients and are increasingly favored by insurance companies and healthcare referrals. Macroeconomic headwinds, like rising healthcare costs, make cost-efficient models like ASCs even more appealing.

Technological advancements are expanding the scope of services, allowing higher-acuity cases to be treated in outpatient settings. Regulatory rollbacks, such as changes to Certificate of Need (CON) laws and new Ambulatory Payment Classification (APC) codes further position ASCs for continued growth.

ASC Investment Outlook: Sustained Growth & Strategic Opportunity

Additionally, healthcare providers favor convenience and operational efficiency. As national discourse shifts toward more affordable healthcare options, ASCs are seen as an increasingly viable solution.

These favorable industry dynamics drive sustained investor interest, exemplified by Bain Capital’s involvement with Surgery Partners. Because the ASC industry fits so well into the traditional, roll-up formula for success, we will likely see more robust M&A volumes further supporting elevated valuations for the foreseeable future.

As these trends continue, VMG Health expects further deal volume among private equity–backed consolidators and health systems entering the market. In turn, valuations are likely to remain buoyed by continued activity.

References

Reuters. (2025, January 28). Bain Capital proposes to acquire remaining shares in Surgery Partners. Reuters. https://www.reuters.com/business/healthcare-pharmaceuticals/bain-capital-proposes-acquire-remaining-shares-surgery-partners-2025-01-28/#:~:text=Jan%2028%20(Reuters)%20%2D%20Bain,a%20filing%20showed%20on%20Tuesday

Seeking Alpha. (2024, February 9). Surgery Partners jumps after report of interest from UnitedHealth, TPG. Seeking Alpha. https://seekingalpha.com/news/4143439-surgery-partners-jumps-after-report-of-interest-from-unitedhealth-tpg

Surgery Partners. (2024, May 15). Surgery Partners completes acquisition of National Surgical. https://ir.surgerypartners.com/news-releases/news-release-details/surgery-partners-completes-acquisition-national-surgical

H.I.G. Capital. (2024, April 30). H.I.G. Capital announces the sale of its equity stake in Surgery Partners. https://hig.com/news/h-i-g-capital-announces-the-sale-of-its-equity-stake-in-surgery-partners/#:~:text=completed%20an%20initial%20public%20offering,ancillary%20services%20in%2032%20states

ASC Data. (2024, May). ASC Data industry overview. https://ascdata.com/wp-content/uploads/2024/05/ASC-Data-Industry-Overview-May-2024.pdf

Ambulatory Surgery Center Association. (2024). ASCs per state. https://www.ascassociation.org/asca/medicare/asc-map/ascs-per-state

Surgery Partners. (2024). Investor presentation. https://ir.surgerypartners.com/static-files/66cc55dc-8933-4b10-a8b7-50deef2bd930