Many health systems across the U.S. are under increasing strain, challenged by aging populations, rising costs, persistent workforce shortages, and legislative uncertainty. These pressures are calling into question the long-term sustainability of traditional healthcare models. Nationwide, health system leaders are seeking opportunities within their care continuum that offer strategic value but haven’t reached their full potential. One such opportunity is a strategic focus on inpatient rehabilitation facilities (IRFs).

IRFs offer compelling margins to top operators, averaging 24% for freestanding hospitals according to 2023 fee-for-service Medicare Margin data, per MedPac 2025’s report. However, average margins for departmental IRFs within acute care hospitals are close to breakeven (1% in 2023, per MedPac 2025’s report). Below, we will highlight emerging trends in the inpatient rehabilitation industry. Many of these trends are driving consolidation and increased utilization of partnership models. We will also discuss the tradeoffs of various alignment models and considerations for selecting a partner.

Increasing Utilization

In 2023, the number of IRF beds increased by 3%, however growth in IRFs was concentrated in freestandings IRFs compared to departmental/hospital-based IRFs The number of freestanding IRFs increased from 345 in 2022 to 371 in 2023, seeing 7.4% growth. Departmental IRFs declined slightly across the same period from 836 to 835 as patients indicate their preference for private rooms and updated facilities when choosing between post-acute options. The majority of IRFs are still fragmented in hospital-based departments of acute care hospitals.

According to MedPAC, Medicare IRF admissions grew 7.3% in aggregate from 2022 to 2023. While there are positive volume trends for the industry, certain headwinds may compress margins, including reimbursement trends promulgated by the Centers for Medicare & Medicaid Services (CMS). While the industry achieved moderate growth in Medicare reimbursement between 2019 and 2025, that growth has generally lagged cost inflations, particularly inflationary pressure on wages and employee benefits. When an IRF can’t achieve economies of scale through volume growth, the likelihood of expense inflation outpacing reimbursement growth represents a greater risk of margin compression. Operators in this situation have begun searching for potential partners who can help with increasing bed capacity where demand is present.

Strong Margins

Fee-for-service (FFS) Medicare margins for freestanding IRFs rose from 23.3% in 2022 to 24.2% in 2023, maintaining a significant disparity between the hospital-based margin of 1%. In aggregate, MedPAC reports that the higher an IRF’s bed count, the higher the Medicare margin will typically be. Overall, the cost of an IRF stay was generally higher in hospital-based facilities at $21,000 compared to $15,000 per freestanding stay. This discrepancy can be caused by variables such as a lack of economies of scale, patients billed for costs that are indirectly related to IRF services, and patient mix. Per MedPAC, hospital-based IRFs admit more patients with less profitable diagnoses, such as stroke, whereas freestanding IRFs admit patients with more profitable diagnoses.

Variation Across States

An important delineation to make when tracking IRF industry-level performance is differentiating statistics between IRFs located in states with and without certificate of need (CON) laws and restrictions. CON laws are state-level regulatory mechanisms used for approving major capital expenditures and projects for certain types of health care facilities. In a state with CON laws, a regulatory agency typically approves or denies the creation of new health care facilities or the expansion of an existing facility’s services in a specified area. Currently, 35 states and Washington, D.C., operate CON programs.

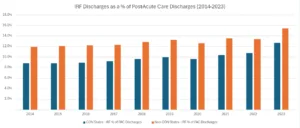

National

At the national level, total IRF discharges as a percentage of total acute care discharges increased from 5.5% to 6% between 2022 and 2023. As a percentage of total post-acute care discharges (IRF, SNF, LTCH, and hospice considered, home health excluded), IRF discharges comprised 13.3%, compared to 11.4% in the prior year.

CON States vs. Non-CON States

As previously mentioned, it is important to note the discrepancy in discharge rates when comparing CON states to non-CON states. The charts below show IRF discharge statistics between CON and non-CON States.

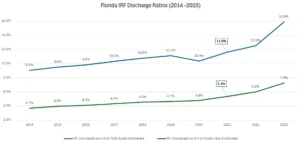

IRF discharges in States with CON laws as of 2023 totaled 5.6% of total acute–care discharges. This is a stark contrast when compared to states without CON restrictions at 7.5%. Please note that this chart does not consider Florida a non-CON state, although restrictions related to IRFs were repealed by the state in 2019.

In 2023, States without CON laws showed higher favor for IRFs as a post-acute option when compared to States with CON laws, at rates of 15.5% and 12.7%, respectively.

CON Reform

Several states have revised or repealed their CON laws, affecting the regulatory landscape for healthcare facilities, including IRFs:

- South Carolina: In May 2023, the state repealed its CON program for most healthcare facilities, including rehabilitation facilities, effective in 2027. This move aims to reduce regulatory burdens and foster competition, potentially increasing access to rehabilitation services.

- Florida: Florida’s 2019 legislation repealed CON requirements for general hospitals and complex rehabilitation facilities, leaving only nursing homes and hospices subject to CON regulations. This deregulation is expected to encourage the establishment of new IRFs and expand existing ones.

- Tennessee: Recent changes exempt certain healthcare facilities from CON requirements, including freestanding emergency departments and ambulatory surgery centers. However, these changes do not directly affect IRFs, which may continue to face regulatory constraints.

These reforms are anticipated to increase competition and access to rehabilitation services, potentially leading to improved patient outcomes. Additionally, other national legislative changes have impacted IRF operation. For example, effective October 1, 2024, CMS updated the ICD-10-CM codes used to determine placement in tiers for IRF discharges. These updates include additions and removals of diagnoses, which impact both tier assignments and presumptive compliance with the 60% rule. Facilities must ensure accurate coding to maintain compliance and appropriate reimbursement. Additionally, a joint resolution (H.J.Res.216) was introduced in Congress to disapprove the final rule submitted by CMS for the Inpatient Rehabilitation Facility Prospective Payment System for federal fiscal year 2025. If enacted, this could delay or alter the implementation of the updated coding and payment policies, adding uncertainty to the regulatory and reimbursement environment for IRFs.

With the changes in these laws and other marketplace regulations, the freestanding IRF market has seen continued growth, while departmental units have either closed or transitioned to freestanding units. One way that hospitals have been transitioning their current departmental IRFs to freestanding entities is through partnering with an inpatient rehabilitation facility operator. Such partnerships offer a wide range of benefits to their hospital partners. Below is a summary of the key advantages of the partnerships:

- Expertise: IRF operators bring specialized knowledge and years of expertise in efficiently and effectively running IRFs. This includes best practices, compliance with CMS, accreditation, and contract negotiation with payers. Additionally, this allows the hospital to gain access to performance data and benchmarking tools to enable better tracking of productivity, quality metrics, and patient outcomes.

- Improved Patient Outcomes: By implementing a proven process based on rehabilitation best practices, the partners can help improve patient outcomes, reduce readmissions, and shorten length of stay—all while allowing the hospital to continue positioning itself as a provider of inpatient rehabilitation services.

- Enhance Financial Performance: Partners are often able to optimize case mix, streamline administrative processes, and improve resource utilization—leading to stronger financial performance for the IRF unit. Additionally, relocating the IRF to a separate facility can help the hospital improve in-house profitability by repurposing the vacated space for higher-acuity, higher-margin services.

- Other Benefits: Partnerships also expedite the launch of the freestanding IRF by leveraging the hospital’s existing patient base. Additionally, partners gain access to the hospital’s CON-designated IRF beds, which may otherwise be unavailable in the market.

“…We can approach that acute-care hospital with what we believe is a win-win proposition… We can build a freestanding inpatient rehabilitation hospital proximate to your existing hospital. If you will sign a non-compete for IRF services and convert your CON unit into something else that’s more profitable for you… we can give you and in-kind equity contribution into that new freestanding hospital… You will have the opportunity to still represent to your key constituencies and the community that you’re still in the IRF service, but you will now have enhanced profitability within your four walls, plus a profit contribution from our hospital.”

– Mark Tarr, President, CEO & Director, Encompass Health

Exploring Innovative Partnership Models

Operators looking to expand their inpatient IRF presence have several partnership models to consider. The most common structures include joint ventures, joint operating agreements (JOAs), and management agreements—each offering different levels of risk, control, and financial involvement.

In a joint venture, the operator and a health system form a new legal entity to jointly develop and manage an IRF, sharing assets such as capital, licenses, and brand reputation. JOAs involve a contractual partnership to operate and grow an existing IRF, with both parties sharing financial risk through agreed-upon terms. Alternatively, a management agreement allows the operator to oversee the IRF’s operations in exchange for a fixed fee, without assuming financial risk.

Financial Returns by Structure

When evaluating partnership arrangements for IRF expansion, organizations must consider a range of financial strategies to determine the best fit for their goals. VMG Health has supported many IRF operators through this process by modeling and comparing the financial implications of various structures.

In one example, VMG Health worked with a health system in a CON state to evaluate multiple expansion options. Scenarios included building a freestanding facility independently, with different capital structures, or entering a joint venture using a mix of debt, cash, and equity from the existing IRF business. VMG Health developed a detailed financial return pro forma, factoring in key variables such as bed count, construction costs, reimbursement changes, staffing, and physician fees. The health system ultimately pursued a joint venture model, leveraging their current IRF equity, and the new facility is now under construction.

While strategic partnerships in inpatient rehabilitation may offer significant opportunities for health systems, the path to alignment is often complicated by a range of operational, financial, and regulatory hurdles. For example, if the health system previously operated their inpatient rehabilitation unit on a campus of their acute care hospital, it may have historically covered significant overhead costs on behalf of the hospital. If the unit were sold to a joint venture, all or some of these overhead costs would have to be re-absorbed by other departments.

Alternatively, if the inpatient rehabilitation business moves off-site, the hospital may replace the former unit with other profitable inpatient services, re-covering the overhead. The health system should consider other challenges to partnership, such as giving up some control over a program historically managed in house, competitive forces and market dynamics, and partner alignment factors. Selecting the right partner up front can mitigate risks of future alignment issues.

Consider these criteria during the partner evaluation process:

- Proven history of strong clinical outcomes (such as community discharge percentages, low re-admission rates, etc.)

- Mission, values, and cultural alignment

- Access and depth of resources: capital, expertise, leadership, technology, negotiating experience

- Forecasted financial returns under proposed structure, in conjunction with capital restraints and other strategic priorities

- Proposed decision-making authority and degree of control retained by health system

Aligning with experienced IRF partners can be an important tool for building resilience in health systems. Beyond optimizing an IRF’s current patient outcomes and financial returns, strategic partners’ dedicated expertise gives their affiliates an advantage in navigating future hurdles, all while keeping high-quality care close to home and within the system.

Contributors:

Sydney Richards, CVA

Lance Whitty

References

Research and Planning Consultants, LP. (n.d.). Changes made to CON laws in 2019. Retrieved May 15, 2025, from https://www.rpcconsulting.com/changes-made-to-con-laws-in-2019/

Research and Planning Consultants, LP. (n.d.). Changes to Tennessee’s Certificate of Need Program. Retrieved May 15, 2025, from https://www.rpcconsulting.com/changes-to-tennessees-con-program/

Shumaker, Loop & Kendrick, LLP. (2023, May 4). Client alert: South Carolina Certificate of Need program repealed (except for nursing homes). Retrieved May 15, 2025, from https://www.shumaker.com/insight/client-alert-south-carolina-certificate-of-need-program-repealed-except-for-nursing-homes-/