The Affordable Care Act (ACA) was designed to expand access to, and improve the value of, healthcare in the United States. The ACA drove a significant shift from fee-for-service (FFS) reimbursement toward value-based care (VBC). What began as a gradual evolution eventually triggered a major surge of interest and investment in VBC models, such as Accountable Care Organizations (ACOs) and risk-bearing provider groups. In parallel, favorable payment and policy changes also incentivized growth in Medicare Advantage (MA), further driving demand for, and valuations of, risk-bearing networks and platforms. While the height of the “gold rush” years may have ended, VBC is here to stay, but with moderated valuations and recalibrated markets.

The Affordable Care Act: The Early Years

In the years immediately following ACA implementation, VBC was experimental. The Center for Medicare and Medicaid Innovation (CMMI) introduced Accountable Care Organizations (ACOs) and the Shared Savings Program. Many organizations, like health systems and larger provider groups, began developing VBC strategies and establishing ACOs and clinically integrated networks (CINs). However, VBC was largely seen as a secondary revenue stream or a future imperative.

At this time, VBC was not yet a material factor in valuations. Little to no premium was attributed to an entity’s ability to manage population health or to support success under a VBC reimbursement model.

The Expansion of Value-Based Care

Beginning around 2015, several major policy and payment changes significantly expanded VBC incentives. They triggered a massive influx of private equity (PE) and venture capital investment, expanded interest from health systems and payers, and a proliferation of new entrants looking to capitalize on the financial upside of effectively managing population health at scale and supporting broader strategic goals.

By the height of this “gold rush” era in the early 2020s, the market had entered a hyper-growth phase, and valuations exploded. The financial return from the VBC model was believed to be driven almost exclusively by a managed population’s size and revenue potential. Rapid member acquisition was favored over operational efficiency and prior historical success. During this time, “lives” and revenue multiples drove valuations of risk-bearing networks and large provider groups that were viewed as capable of managing risk—regardless of whether they’d demonstrated capability.

Investors believed returns would come from the ability to support further material growth in lives, risk-contracting streams, and revenue-enhancement initiatives. They were willing to overlook historical performance, operational efficiency, and profitability. Valuations climbed to astronomical levels, further propelled by a competitive market.

The challenges of converting VBC growth into profitability and investor returns quickly became evident, and the market began to shift.

Rethinking Operational & Financial Assumptions

After more than a decade of expansion, organizations are reevaluating several operational and financial assumptions, including:

Private, PE-backed, and publicly traded VBC aggregators have struggled to demonstrate value creation or a path to sustainable profitability. These struggles, plus payment and regulatory changes within a market that no longer values membership growth without the ability to drive earnings, have driven down earnings and valuation multiples and prompted some key players to change their VBC strategy:

- In January 2026, Optum shifted from aggressive membership growth toward margin recovery, operational discipline, and network optimization, including exiting underperforming arrangements and narrowing portions of its affiliate network.

- VillageMD and Walgreens Boots Alliance have scaled back earlier expansion efforts through restructuring initiatives, market consolidation, and the closure or divestiture of underperforming locations.

- Agilon Health has faced ongoing financial and investor pressure, prompting restructuring efforts to improve operational performance and restore long-term stability.

- The tide has turned, but not all VBC companies are struggling or dramatically shifting focus. Examining those with steadier performance highlights the current VBC best practices—prioritizing integration and efficiency, valuing and incentivizing strong provider performance, and pursuing thoughtful growth:

- Humana and its CenterWell platform have pursued a more measured value-based care strategy, focusing on integrating practices into a common operating model while selectively acquiring established, high-performing assets such as MaxHealth.

- Privia Health continues to demonstrate steady performance growth through a selective, asset-light model that emphasizes disciplined expansion, operational efficiency, and risk-managed value-based care participation.

The Next Chapter in Value-Based Care

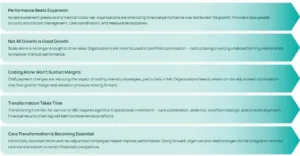

The evolution of VBC is far from over. We will see more changes in strategy and incentives that support long-term sustainability and steady performance:

Success in VBC is necessary for survival in a risk-adjusted world. It will depend less on scale and more on execution, selective participation, and cost savings under tighter financial conditions.

![]()

In a maturing VBC market, understanding the drivers behind performance and valuation has never been more important. Partner with VMG Health to assess strategy, performance, and opportunities in a changing landscape.