Radiology providers are facing a complex and evolving operational landscape shaped by unfavorable changes to the Medicare Physician Fee Schedule (MPFS), workforce shortages, and capacity limitations. Despite these headwinds, tailwinds—including technological advancements and new operational models—have emerged in recent years. Understanding the implications of these shifts is critical for diagnostic imaging groups, health systems, and investors alike.

Headwinds

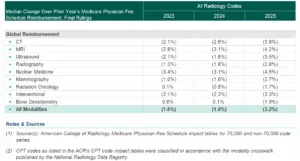

MPFS 2025 Final Rule Marks 25 Years of Reimbursement Declines

Based on the data from the American College of Radiology (ACR), the MPFS final rulings through 2025 reflect steady decreases in both professional and technical reimbursement across various diagnostic imaging modalities seen in the chart below. The MPFS 2025 payment schedule includes an overall 2.8% cut to the conversion factor, which will likely decrease margins for radiology providers.

Radiologist Shortages Felt Nationwide

Demand for radiologists has steadily outpaced the growth of new radiologists in the market, as discussed in a recent Radiology Business article, which quotes Andrew Colbert, Senior Managing Director at Ziegler, during the 2025 Radiology Business Management Association meeting in Nashville, Tennessee:

“…the biggest issue is the scarcity of radiologists right now….The number of studies is increasing, call it, 5.0% per year, while the supply of radiologists is, at most, up 2.0%.”

While this scarcity of radiologists will continue to affect the market in the short term, it points to an overarching issue within the industry. Colbert went on to state that the U.S. is expected to have a shortage of 42,000 radiologists and other physician specialists by 2033. Additionally, Colbert brought attention to a 2021 survey of 350 participants from 34 states performed by the Advanced Health Education Center (AHEC), in which 81% of respondents answered “Yes” to the question, “Is your facility experience a staffing shortage?”

The Number of Freestanding Diagnostic Imaging Facilities Remains Stagnant Since Peaking in 2012

Capacity limitations are another headwind shaping the industry; workforce shortages alongside increased demand for imaging services have led to significant backlogging and centers reaching maximum capacity. The largest operator of freestanding outpatient diagnostic imaging facilities in the U.S., RadNet, Inc., has noted the stagnant number of outpatient facilities for years in its investor presentations.

In the latest version, dated December of 2024, the company reported the number “…peaked in 2012 and has been relatively stable since, despite growing demand.” In a possible move to address capacity limits, RadNet has recently accelerated the pace of internally developing new outpatient centers at an unprecedented rate. In 2024, RadNet developed 44 new centers—compared to just 1 in 2021, 14 in 2022, and 11 in 2023.

Tailwinds

Tailwinds

For most freestanding diagnostic imaging centers, which can be characterized as mom-and-pop operations, building de novo facilities is a less practical option compared to large, geographically diverse operators. Radiology practices instead look to realign resources, adopt new technologies, and explore collaborative models to maintain service levels.

Broader Interest in Joint Venture Arrangements

Market participants have increasingly looked toward joint venturing with hospitals, health systems, and other operators as an avenue to enhance their volumes and provide financial stability. Notably, 38.4% of RadNet’s facilities are structured as joint ventures, and management often stresses the strategic importance of these collaborations in their business model during earnings calls.

Capital Infusions from Private Equity on the Rise

Private equity firms have been rapidly expanding within radiology, penetrating every modality and increasing the amount of capital available to firms. Melissa A. Davis, MD, MBA, Vice Chair of Medical Informatics and Associate Professor at Yale University’s Department of Radiology and Biomedical Imaging, stated that this new capital has allowed for the hiring of more staff and upgrades in technology. These investments are key drivers of the newfound interest in artificial intelligence (AI).

AI Provides Welcome Relief to the Industry

Technological advancements, particularly in AI, are reshaping radiology operations. AI tools enhance diagnostic accuracy and streamline workflows, enabling radiologists to manage larger caseloads more efficiently. To illustrate, companies like Rad AI have developed generative AI solutions, such as Rad AI Reporting and Rad AI Impressions, which have been widely adopted by thousands of U.S. radiologists. These tools streamline reporting processes and improve workflow.

In Radiology Business, Andrew Colbert stated that a survey from their advisory board found that 53% of hospitals and 33% of radiology practices are using at least one imaging AI product.

To highlight this commitment to new technology and AI integration, RadNet’s Digital Health segment, which develops and deploys clinical applications to enhance interpretation of medical images and improve patient outcomes, has seen its first quarter revenue increase by 31.1% year over year. Most recently, RadNet has acquired iCad, an AI cancer detection software, with hopes of accelerating AI-powered early detection and diagnosis of breast cancer.

Higher-Acuity Diagnostic Imaging Services on the Rise

In response to the need for higher-acuity imaging services, facilities are investing in more comprehensive scanning technologies. As an example, RadNet has seen double-digit growth in PET/CT volume for the last six quarters, outpacing all other imaging modalities since Q1 2022. During RadNet’s Q1 2025 earnings call, CEO Dr. Howard Berger described this growth as, “primarily the result of continued growth of prostate and brain imaging procedures. The cumulative strength of these trends has provided us the confidence to increase 2025 guidance ranges.”

Conclusion

Reimbursement changes are a continuous and expected aspect of healthcare delivery; however, radiology faces additional challenges with workforce shortages and capacity limitations. The headwinds currently challenging industry participants may stretch into the long term: These dynamics could act as a catalyst for certain tailwinds, including strategic realignment and technological advancements.

Groups that approach this period with flexibility, focus, and foresight will be best positioned to continue delivering value in a dynamic market. Valuations will remain a necessity as companies look to acquire new centers, carve out modalities from within, and explore new operational structures. Overall, the radiology industry is poised for significant changes.

![]()

References

Christensen, E. W., & others. (2023). Budget neutrality and Medicare Physician Fee Schedule reimbursement trends for radiologists, 2005 to 2021. Journal of the American College of Radiology, 20(10), 947–953. https://www.jacr.org/article/S1546-1440(23)00521-5/abstract

Carfagno, R. (2025, March 5). Five radiology trends to watch in 2025. XiFin. https://www.xifin.com/resource/blog-post/five-radiology-trends-to-watch-in-2025/

Fornell, D. (2023, December 14). The impact of Medicare payment cuts on radiology and patient care access. Radiology Business. https://radiologybusiness.com/topics/healthcare-management/healthcare-policy/impact-medicare-payment-cuts-radiology-and-patient-care-access

Driggers, B., Wilson, C., & Anderson, T. (2025, January 31). Radiology compensation models: How they’re evolving to meet modern needs. Regents Health Resources. https://www.regentshealth.com/newsroom/radiology-compensation-models-how-theyre-evolving-to-meet-modern-needs

Stempniak, M. (2025, April 11). Radiology M&A expert shares 6 trends to watch in 2025. Radiology Business. https://radiologybusiness.com/topics/healthcare-management/mergers-and-acquisitions/radiology-ma-expert-shares-6-trends-watch-2025

Fornell, D. (n.d.). PET-CT seeing increasing adoption, and now more affordable systems have facilities taking a closer look. Cardiovascular Business. https://cardiovascularbusiness.com/sponsored/1164/positron/topics/cardiac-imaging/nuclear-cardiology/pet-ct-seeing-increasing-adoption-and-now-more-affordable-systems-have-facilities-taking-closer-look

Fornell, D. (2025, January 29). Concerns about private equity’s growing influence in radiology. Radiology Business. https://radiologybusiness.com/topics/healthcare-management/medical-practice-management/concerns-about-private-equitys-growing-influence-radiology

RadNet, Inc. (2024, December). Investor presentation. https://www.radnet.com/about-radnet/investor-relations

RadNet, Inc. (n.d.). SEC filings. https://www.radnet.com/about-radnet/investor-relations