On December 11, Lumexa Imaging Holdings, Inc. (NASDAQ:LMRI) listed 25 million common shares on the Nasdaq Global Select Market at $18.50 per share. Before accounting for options granted to underwriters, the proceeds generated $462.5M, which is expected to be allocated towards debt repayment, working capital, and future acquisitions. Since trading, LMRI stock fell to $17.08 per share before returning to $18.11 per share by the end of the year.

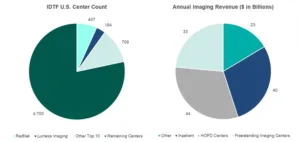

Lumexa and its affiliates operate the second largest outpatient imaging center footprint in the United States, spanning 184 centers across 13 states, and includes eight joint venture partnerships with major health systems. Lumexa was founded in 2018 as a joint venture between the physician practice, Charlotte Radiology, and private equity sponsor Welsch, Carson, Anderson & Stowe (WCAS). Initially operating as US Radiology Specialists, Lumexa rebranded in July 2025.

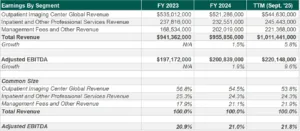

During the 12 months ended September 30, 2025, Lumexa reported $1B in consolidated revenue, comprised of professional and technical billing along with management and development fees. During this period, Lumexa reported $220.1M in adjusted EBITDA, representing a 21.8% margin.

Corporate Growth Strategy

Lumexa’s IPO is a testament to the success of the company’s growth strategy delivered over the past eight years, largely defined by three core tenants:

- Inorganic acquisitions

- Systemic tailwinds to support organic growth

- Leverage

Inorganic Growth Strategy

The Independent Diagnostic Testing Facility (IDTF) market is positioned for sustainable future consolidation. With roughly 6,000 IDTFs nationwide—75% of which are owned by single-facility operators or small chains—the market is diverse and highly fragmented. Lumexa estimates the total addressable market for imaging services to be roughly $140B. In such a fragmented ecosystem, consolidators like Lumexa are positioned to acquire individual IDTFs at a lower multiple, while attracting outside capital at higher valuations with their size, growth potential, diversified market, and professional management.

Since 2018, Lumexa has pursued both de novo and acquisition growth in scaling its platform from 20 facilities to over 180. During this time, Lumexa has favored de novo buildouts for their cost advantages and design control. With an average development time of 12–24 months, Lumexa boasts a maximum payback period of three years—significantly less than average acquisition payback periods. In select situations, Lumexa has also demonstrated a successful track record of 20 acquisitions with an average acquisition multiple of 8–9x EBITDA for platforms and less than 5x EBITDA for centers with fewer than five locations.

Since 2018, Lumexa has pursued both de novo and acquisition growth in scaling its platform from 20 facilities to over 180. During this time, Lumexa has favored de novo buildouts for their cost advantages and design control. With an average development time of 12–24 months, Lumexa boasts a maximum payback period of three years—significantly less than average acquisition payback periods. In select situations, Lumexa has also demonstrated a successful track record of 20 acquisitions with an average acquisition multiple of 8–9x EBITDA for platforms and less than 5x EBITDA for centers with fewer than five locations.

Systemic Tailwinds

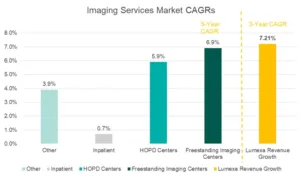

Systemic tailwinds make Lumexa’s organic growth strategy sustainable while validating the company’s value proposition. According to UnitedHealth Group, “imaging services provided in imaging centers or physician’s offices are approximately 60% less expensive than those performed in an HOPD.” For this reason, IDTFs are the preferred setting for care by payers, patients, and practitioners. Consequently, IDTF revenue growth has outpaced that of the aggregate imaging industry over the past five years, while LMRI’s revenue growth has outpaced IDTF growth by 31 basis points.

As IDTFs continue to take market share, more health systems are looking to partner with national platforms with expertise in the build out and management of freestanding centers. As many states continue to relax Certificate of Need (CON) laws, such as North Carolina’s 2026 elimination of MRI CONs, national consolidators such as LMRI offer expertise, access to capital, and speed to market when it counts. In turn, health systems provide IDTFs with expanded referral opportunities and leverage with payers for higher reimbursement, making health system partnerships an attractive opportunity for future growth.

Since its inception, Lumexa has partnered with over eight health systems involving 85 centers, establishing LMRI as a preferred partner for development and management of IDTFs. According to LMRI’s S1, LMRI has identified approximately 100 potential health system partners across its top 20 target MSAs, with fewer than 20% having an existing imaging joint venture partner.

Joint Venture Partners

Finally, imaging is positioned to benefit from advancements in artificial intelligence (AI). LMRI cites the adoption of third-party AI solutions, as opposed to internally developed systems, as a key driver for improved scan times, clinical efficiency, and faster scheduling and communication. However, unlike RadNet, it does not appear that LMRI is focused on developing proprietary AI systems that would be marketed to outside parties as a SaaS-type revenue model.

Leverage

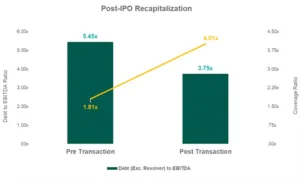

Lumexa’s strategic use of debt contributed to the company’s ability to scale quickly and may also be a significant reason for the company’s pursuit of public capital. As of year-end 2025, LMRI’s coverage ratio was 1.84x, based on Q3 2025 YTD normalized EBITDA and interest expense, leaving little cushion for potential adverse shocks to cash flow or sustained inorganic expansion.

Post–IPO, LMRI intends to refinance its existing loan facility and revolver, currently $1.2B at roughly 4.5% plus secured overnight financing rate (SOFR), to an $825M term loan with a $250M revolver at the lesser of 3% plus SOFR or 2% plus prime. Post–recapitalization, LMRI expects to increase its coverage ratio to 4x while reducing its debt to EBITDA ratio from 5.45x to 3.75x. In doing so, LMRI positions itself for sustainable growth, insulated from potential macroeconomic headwinds.

Valuation Insights

At its essence, valuation is the confluence of three factors: cash flow, growth, and risk. As valuation practitioners, we appreciate the simplicity of expressing valuation as a multiple of earnings, allowing for a comparison of growth and risk across companies of differing earnings.

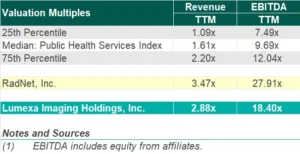

As a multiple of EBITDA, LMRI traded at 18.4x at the end of the year, significantly lower than the only publicly traded, pure-play operator, RadNet, Inc., which traded at 28x.

Relative to other publicly traded healthcare services providers, both LMRI and RadNet trade at a premium, which may be primarily attributable to two factors. First, successful pure-play consolidators like LMRI and RadNet may offer superior growth opportunities than more mature operators with diversified lines of business. Second, the market has high expectations for AI to unlock value in the imaging segment—the “AI Premium.”

While there are numerous differences between LMRI’s and RadNet’s business models, we believe the AI Premium is a significant contributor to the observed 10x differential between these two companies. Unlike LMRI, which positions itself as a beneficiary of third-party adoption, RadNet’s subsidiary DeepHealth is actively developing AI solutions to be marketed externally.

While few in number, platform-level transactions within the imaging industry also provide insight into LMRI’s current valuation. Nine platform-level imaging transactions occurred since LMRI’s 2018 founding, and none of which occurred post-AI. The median clearing multiple was 10x with Madison Dearborn Partner’s acquisition of Solis Mammography in 2018, hitting a peak at 14.2x. LMRI’s and RadNet’s current valuations speak to significant growth expectations developed over the past several years.

Market Approach

Conclusion

Lumexa’s IPO represents the culmination of a thoughtfully executed growth strategy that has leveraged industry fragmentation, favorable site-of-care dynamics, and disciplined capital deployment to build one of the largest outpatient imaging platforms in the country. The company enters the public markets with meaningful scale, strong margins, and a favorable position as a preferred partner to health systems seeking lower-cost imaging solutions outside the hospital setting.

Moreover, the LMRI’s IPO signals investor confidence in the outpatient imaging industry, as operators continue to gain market share and grow earnings. LMRI’s post-IPO performance may provide assurance to other major private equity–backed imaging businesses (such as RAYUS/Wellspring Capital, Solis Mammography/Madison Dearborn Partners, MedQuest/TPG, SimonMed Imaging/American Securities) that the public markets present a viable opportunity for a favorable exit. In addition, the successful IPO could also provide confidence to other private equity–backed healthcare service businesses in other verticals (PPM, ASC, etc.) that public markets are a viable avenue for a future liquidity event.

Ultimately, Lumexa’s ability to justify its valuation will hinge on disciplined capital allocation post-IPO; successful refinancing and deleveraging; and continued execution across de novo development, acquisitions, and health system partnerships. We look forward to continuing to monitor Lumexa’s future performance for years to come.

![]()

VMG Health helps clients make sense of valuation in a rapidly evolving healthcare market. Connect with the experts to apply real-world insights to your strategic, transaction, or capital planning decisions.

![]()

References

Lumexa Imaging Holdings, Inc. (2025, December 2). Amended registration statement on Form S-1/A. U.S. Securities and Exchange Commission. https://www.sec.gov/Archives/edgar/data/2071288/000119312525304460/d217676ds1a.htm

RadNet, Inc.(2025, November 11). Investor Day: Advancing imaging through innovation & technology. RadNet. https://www.radnet.com/investor-day

ScopeResearch Database

Whyde, M., Schulte, S. H., & Aboud-Hall, B. (2025, June 24). Diagnostic imaging: Headwinds & tailwinds shaping the industry. VMG Health. https://vmghealth.com/insights/blog/diagnostic-imaging-headwinds-tailwinds-shaping-the-industry/

![]()

Contributor:

Dylan Lane