Published by

Becker's Hospital Review

Valuations of a business or enterprise and

real estate share numerous methodologies, terms and standards, which often result in confusion amongst the distinct disciplines. Both types of valuation largely depend upon an Income Approach. Both utilize financials that are usually prepared and audited by a third-party and in accord with Generally Accepted Accounting Principles (“GAAP”). Both valuations depend upon an appraiser’s ability to determine either a stabilized income stream or to prepare a reasonable forecast based upon historical performances, current market conditions and projected future market conditions.

Business valuations utilize EBITDA (earnings before interest, taxes, depreciation and amortization) as a key format metric to determine value. An appraiser’s ability to either determine a stabilized level of EBITDA or a reasonable forecast of EBITDA then allows for the application of a market-derived multiple or a discounted cash flow analysis in order to determine a supportable determination of value.

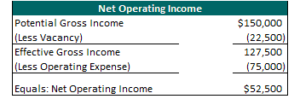

Within the context of a real estate analysis, Net Operating Income is the key formula metric of value that parallels EBITDA for business valuation. Please note that the Net Operating Income is exclusive to the operation of the real estate component only. An example of a Net Operating Income calculation is depicted in the following table.

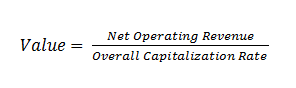

Once the appraiser's estimate of net operating income is made, two options to convert this into an indication of value are available. If the net operating income is considered to be at a stabilized value, then the application of an overall capitalization rate is often utilized. An overall capitalization rate is an arithmetic factor that expresses the relationship between net operating income and value through division. The calculation is expressed as:

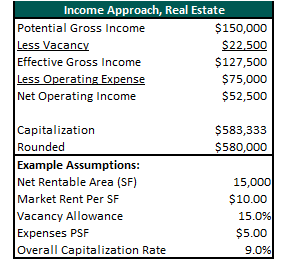

There are several methods of extracting an Overall Capitalization Rate. The most prominent cap rates are abstractions directly from the marketplace itself. By dividing a comparable property’s net operating income by the sale price, an Overall Capitalization Rate can be derived. These rates then can be compared to the subject property in terms of the quantity, quality, and durability of the income streams. Other popular methods of Overall Capitalization Rate derivation include market surveys (from appraiser or published surveys), the band-of-investment technique, and debt coverage rate analysis. The following table depicts an example of the methodology employed in the Income Approach of real estate.

If a Net Operating Income stream is not stabilized, then a discounted cash flow analysis is often preferred in the analysis of real estate.

In summary, both business valuations and real estate valuations often rely upon an Income Approach to generate value. Both sciences base value upon the determination of either stabilized income stream or a reasonable forecast of income. However, each of the disciplines utilize a separate and distinct methodology and base financial metric in the final derivation of value.

Click to continue to the full article.