Contributors: Madison Whyde, Alex Malin & Chris Madden

As discussed in Part One, volume levels have been significantly impacted by elective procedure suspensions, reduced operating hours, and other restrictive measures such as shelter-in-place and social distancing guidelines, which has placed additional emphasis on expense management and overall profitability. In Part Two of this three-part series, we explore how the combination of government stimulus programs and expense mitigation strategies have impacted profitability of these public healthcare companies.

Government Relief

Providers benefited from prompt and material actions by the federal government. Key sources of relief include the Coronavirus Aid, Relief and Economic Security Act (the “CARES Act”) and the Paycheck Protection Program and Health Care Enhancement Act (the “PPPHCE Act”); collectively, these legislative measures allocated $175.0 billion in funding to eligible providers through the Public Health and Social Services Emergency Fund (the “PHSSEF”). In addition, the CARES Act provides for the expansion of the Medicare Accelerated and Advance Payment Program (“MAAPP”). Although a few companies declined and/or returned relief dollars (such as Encompass Health), notable recipients of these funds were the larger hospital operators, including Community Health Systems, Inc. (“CHS”), HCA Healthcare, Inc. (“HCA”), Tenet Healthcare Corporation (“THC”), and Universal Health Services, Inc. (“UHS”).

During the three months ended June 30, 2020, CHS received approximately $564.0 million in payments through the PHSSEF, of which $448.0 million qualified to be recognized within the consolidated statements of income. HCA received nearly $1.4 billion from the CARES Act, of which they recognized $822.0 million in the consolidated income statements. Tenet received cash payments of approximately $712.0 million and recognized approximately $511.0 million in their consolidated statements of operations due to grants from the CARES Act and state grant programs. UHS received approximately $320.0 million of funds from various governmental stimulus programs (most notably the PHSSEF). Included in their consolidated statements of income is approximately $218.0 million of net revenues recorded in connection with these stimulus programs. We have summarized how these relief dollars compared to Q2 net income in the chart below.

In addition, Medicare accelerated payments (advances that must be repaid) of approximately $1.2 billion were received by CYH during the three months ended June 30, 2020, HCA received approximately $4.4 billion, Tenet received approximately $1.5 billion, and UHS received approximately $375.0 million of Medicare accelerated payments, which collectively totals to nearly $7.5 billion.

The monies received through both the CARES Act and MAAPP served as a key source of relief for healthcare providers’ profitability and cash flow in Q2.

Expense Mitigation Strategies

Despite the relief dollars, healthcare operators discussed how they are still actively addressing issues affecting their expense structures. More specifically, supply chain disruptions, shortages, delays, and price increases in medical supplies, additional PPE requirements, increased general and professional liability exposure, and broader economic shocks to unemployment rates and consumer spending that have increased the number of uninsured and underinsured patients throughout the quarter. As a result, second quarter earnings calls concentrated around newly implemented expense mitigation strategies. For example, looking exclusively at labor-related costs, some of these strategies included adjustments to employee salaries, wages, and benefits such as salary decreases, furloughs, reduced hours, and freezes on merit increases and 401(k) contributions. The following earnings call excerpts provide additional detail on what executive and operational management is doing to preserve profitability from an expense structure standpoint:

Imaging

“We analyzed all aspects of our business and focused on ways to most effectively reduce our cash spend. We created a multi-prong plan to impact major expenses and cash flow categories. Specifically, we focused on reducing salaries and professional fees and lowering our facilities’ rental payments. We investigated every local market in which we operate to identify centers we could temporarily close and where we felt with a high degree of confidence, we could direct patient volume into facilities that would remain open. We also evaluated our large categories of cash spend and identified vendors that would work with us to lower our costs or defer payments.”

Howard G. Berger, Chairman, President, CEO & Treasurer, RadNet Q2 2020 Earnings Call Transcript

Behavioral Health

“These initiatives included aligning corporate and facility level staffing costs with patient volumes, implementing a hiring freeze for nonclinical staff, canceling and now limiting all nonessential business travel, reducing discretionary expenditures, temporarily reducing marketing spending, negotiating with certain vendors for discounts and/or revised payment terms and closely managing our working capital as our facilities continue to bill and collect for services rendered.”

David M. Duckworth, Chief Financial Officer Acadia Healthcare Company, Inc. Q2 2020 Earnings Call Transcript

Post-Acute Care

“…In early May, we made a shift in our reimbursement structure for therapists, lowering each therapists’ base pay by 20% and in turn, lowering their productivity expectations for the pay period by the same 20% factor. And that proved to be a really successful strategy for us, both in the near term and I think, ultimately, in the long term… that structure allowed us to really lower our cost per visit, but it also gave us the opportunity to maintain 100% of our therapy staff. We didn’t have to furlough anyone with that approach. We were able to keep them benefit-eligible and keep them available to us and allowed them to use flex capacity to get back to their full compensation. And so, it’s really proven to be a good strategy, and we have announced that we intend to maintain that with our physical therapy team for the foreseeable future that we don’t intend to go back to the 100.0% pay. And that was probably the biggest single structure change we’ve made.”

April Kaye Bullock Anthony, CEO of Home Health & Hospice, Encompass Health Corporation Q2 2020 Earnings Call Transcript

“Our operating expenses in both segments were elevated by our response to the pandemic. Labor productivity was adversely impacted by revised clinical protocols and operating procedures required for infectious disease management. Along with all other health care providers, we incurred higher costs related to increased utilization and pricing of PPE and cleaning supplies. In addition, we elected to reward our frontline employees with extra PTO, resulting in a $43 million incremental expense in the second quarter.”

Mark Tarr, President & CEO & Douglas E. Coltharp, Executive VP & CFO, Encompass Health Corporation Q2 2020 Earnings Call Transcript

Hospitals

“Our strategic margin improvement program has delivered expense savings across our corporate office infrastructure, shared service centers, supply procurement, vendor fees and other non-patient care areas. These savings, while significant, were more than offset by our net revenue loss due to COVID-19 in the second quarter, but we do expect these savings to provide long-term benefit through ongoing expense reductions and greater efficiencies as our business returns to more normal levels.”

Tim L. Hingten, Executive Chairman & CEO, Community Health Systems Q2 2020 Earnings Call Transcript

“We also implemented a series of necessary targeted cost actions in Q2 so we could redirect additional resources to our response… The real-time data-driven dashboards we created during the pandemic have been instrumental in informing our response. Our teams are constantly inputting data into each system to closely monitor staffing, additionally, also monitoring PPE supplies, medication, equipment, and bed capacity. The ability to capture real-time inventory levels of crucial things means we can dial back or accelerate as needed, keeping us balanced throughout the system and ahead in meeting the demands of our clinicians and facilities. These systems are supporting our needs and enabling us to transfer nursing support and supplies to other facilities when deemed necessary.”

Ronald A. Rittenmeyer, Executive Chairman & CEO, Tenet Healthcare Corporation Q2 2020 Earnings Call Transcript

“I think generally speaking, we can hold much of the cost controls that we put in place. As we said, most of those were around adjusting some of our discretionary spending as well as some of the variable costs… We do know this recent COVID surge, we’re having to make sure we have the appropriate labor to serve that surge that may result in some increased use of either contract or premium labor… We’re very pleased with the results, and we’re just going to have to see how the volume returns and what are the variable costs that we’re going to need to support that. But we feel, for the most part, we can hold much of the expense adjustments that we made during the quarter.”

William B. Rutherford, Executive VP & CFO, HCA Healthcare, Inc. Q2 2020 Earnings Call Transcript

Clinical Laboratories

“During the first quarter, we commented that given the decline in our business as a result of the pandemic as well as the uncertainty in our outlook, we took actions such as furloughs, reduced hours and withheld merit increases and 401(k) contributions. Now with increased demand and an improved outlook, we have brought back employees from furloughs, we are proceeding with merit adjustments, and we will retroactively reinstate 401(k) contributions, recognizing the significant contributions of our employees.”

Glenn A. Eisenberg, CFO & Executive VP, Laboratory Corporation of America Holdings Q2 2020 Earnings Call Transcript

“LabCorp Diagnostics adjusted operating income for the quarter was $309 million or 18.2% of revenue compared to $345 million or 19.6% last year. The decrease in adjusted operating income and margin was primarily due to the decline in our base business as a result of the pandemic as well as higher personnel costs due to merit increases, partially offset by COVID-19 testing and LaunchPad savings.”

Glenn A. Eisenberg, CFO & Executive VP, Laboratory Corporation of America Holdings Q2 2020 Earnings Call Transcript

Dialysis

“Adjusted operating income margin was strong for the quarter at 16.0%. On a year-over-year basis, our margin expanded due to strong cost management across the P&L and an improvement in RPT.”

Joel Ackerman, CFO & Treasurer, DaVita Inc. Q2 2020 Earnings Call Transcript

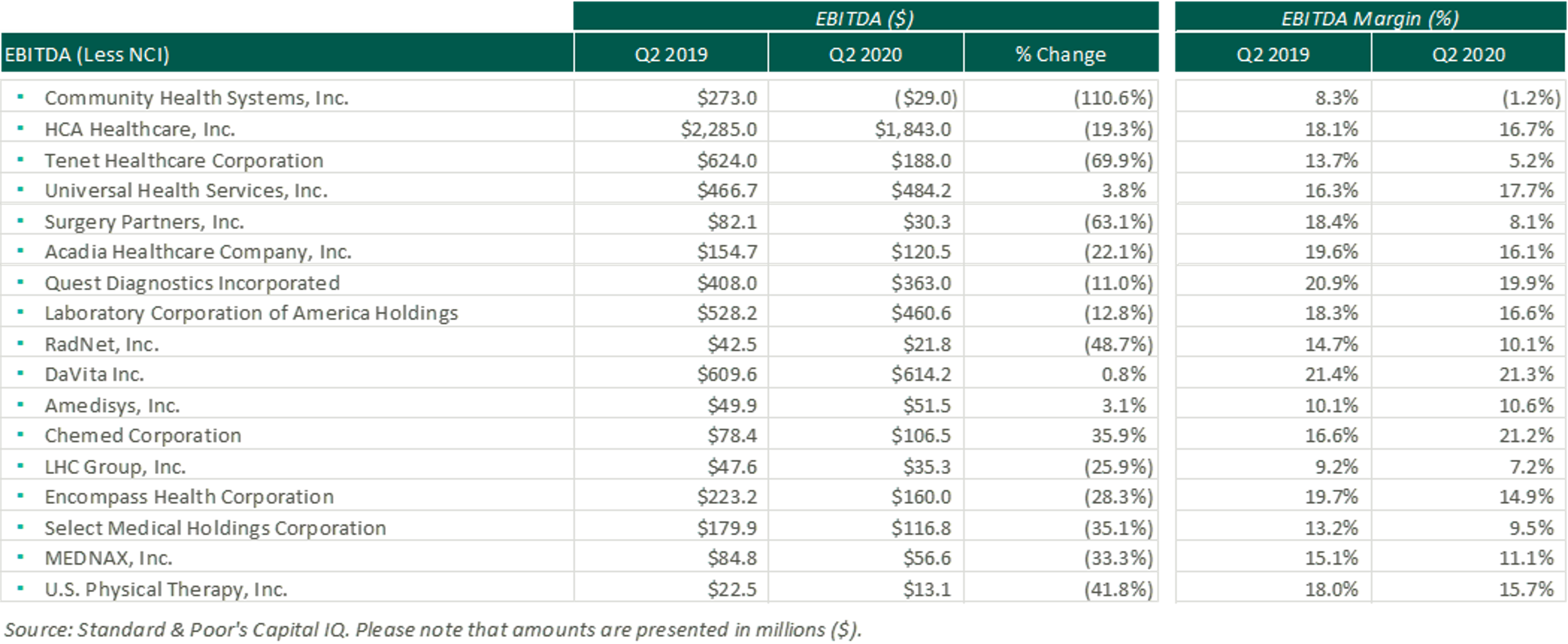

Profitability

Although several companies reported a decline in EBITDA on a dollar basis, the combination of government relief dollars and expense mitigation strategies allowed several companies to report EBITDA margins generally in-line with historical levels.

Conclusions

While our healthcare system continues to contend with COVID-19, many companies declined to provide future guidance on financial performance during earnings calls, citing uncertainties that remain surrounding the duration of COVID-19, government regulations and relief measures, and the recovery of the broader U.S. economy. However, cautious optimism permeates management sentiment. As noted in several of the quotes presented, the impact of COVID-19 may have unforeseen benefits. Most companies reacted quickly to preserve margin, which may ultimately benefit future performance and profitability. With the efficiencies gained through this unprecedented quarter, healthcare companies may be positioning themselves for a more pleasant Q3 than originally thought possible.