Lithotripsy: Demographics and Technology to Drive Demand

Rachel Linch

November 28, 2022

Written by Jack Hawkins and Ryan Mendez

The following article was published by Becker’s Hospital Review.

On November 1, 2022, the Centers for Medicare & Medicaid Services (CMS) released the CY 2023 Hospital Outpatient Prospective Payment System (OPPS) and Ambulatory Surgery Center (ASC) payment system policy changes and payment rates final rule.

Based on the final ruling, CMS will continue to update the ASC payment system using the hospital market basket update rather than the Consumer Price Index for All Urban Consumers (CPI-U) for CYs 2019 through 2023.

As 2023 is slated to be the last year of the trial, CMS indicates in this final rule that the agency intends to “update the public on [its] assessment of service migration and other factors in the CY 2024 OPPS/ASC proposed rule.” The final rule resulted in overall expected growth in payments equal to 3.8% in CY 2023. This increase is determined based on a projected inflation rate of 4.1% less the multifactor productivity (MFP) reduction of 0.3% mandated by the ACA.

“While the AHA is pleased that CMS will provide hospitals and health systems with an improved update to outpatient payments next year compared to the agency’s proposal in July, the increase is still insufficient given the extraordinary cost pressures hospitals face from labor, supplies, equipment, drugs, and other expenses. As we urged, CMS will use more recent data in its calculations on the payment update, resulting in more accurate data that better reflects the historic inflation and tremendous financial pressures hospitals and health systems have confronted recently. However, hospitals are still dealing with a wide range of challenges in providing care which is why the AHA is urging Congress for additional support by the end of the year.”

Stacey Hughes, Executive Vice President, AHA

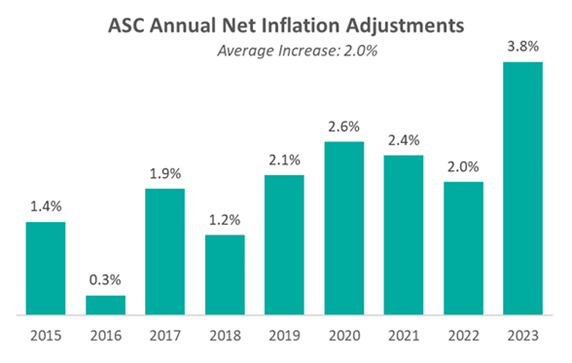

Presented in the chart below is a summary of the historical net inflation adjustments for CY 2015 through CY 2023. The annual inflation adjustments are presented net of additional adjustments, such as the MFP reduction, outlined in the final rule for the respective CY. The CY 2023 inflation adjustment is nearly double the increase we have observed in each of the last eight years and is largely driven by labor and supply cost pressures.

CMS is shaking things up for ASCs with the finalization of a new policy related to complexity adjustments for CY 2023. The policy will provide complexity adjustments for combinations of specific procedures and add-on procedure codes deemed eligible for the complexity adjustment under the hospital outpatient prospective payment system (OPPS). By themselves, add-on codes do not receive supplementary reimbursement when they are bundled with primary codes. However, the addition of add-on codes to a primary procedure code will often change the assigned complexity of a procedure and make it more costly in the process. As a result of the policy finalized by CMS, Medicare will provide complexity adjustments that affect the payment rate for certain primary procedures to make up for the additional cost of performing specific add-on services.

CMS received 64 recommendations for potential procedures to be added to the ASC CPL for CY 2023. Based on the review of clinical characteristics conducted by CMS, four out of the 64 procedures were added to the CPL for CY 2023. The four procedures are outlined in the table below. These codes correspond to procedures that have few to no inpatient admissions and are widely performed in outpatient settings.

“CMS’s decision to add only four new procedures to the ASC-CPL for 2023 after ASCA proposed 47 procedures that ASCs are performing safely and successfully for privately insured patients is a serious mistake and denies beneficiary access to high-value care. Forcing otherwise healthy Medicare beneficiaries to receive care in higher-cost settings for these procedures needlessly increases costs to the Medicare program and undercuts Medicare’s mission of serving as a responsible steward of public funds.”

-Bill Prentice, Chief Executive Officer, ASCA

CMS has projected total ASC payments in 2023 to increase from approximately $230 million in 2022, to approximately $5.3 billion. The source of the increase in payments is a combination of enrollment, case-mix, and utilization changes. In conclusion, we have continued to see the trend of rising labor and supply costs play out throughout 2022 and continue into the finalization of the CY 2023 payment system. CMS continues to show stability on the annual inflation adjustment utilizing the hospital market basket to update rates. With that said, ASCA Chief Executive Officer Bill Prentice and AHA Executive Vice President Stacey Hughes have pointed out how the costs of providing care continue to rise rapidly. CMS finalized the addition of four procedures to the ASC CPL for CY 2023. However, the addition of only four codes from the 47 proposed procedures resulted in further pushback and a continued desire for additional procedures to be added to the CPL that are being performed safely and successfully by ASCs.

Written by Taryn Nasr, ASA and Madeline Noble

The following article was published by Becker’s Hospital Review.

The demand for lithotripsy procedures is expected to increase in the coming years. This expected increase is supported by a review of the Global Lithotripsy Devices Market. It is forecasted to grow at a 5.5% CAGR and is expected to be valued at $2.03 billion by 2027. [1] While several factors have contributed to this rising demand, the primary drivers are the increasing incidence of kidney stones among the geriatric population and the advancements in lithotripsy technology. Healthcare systems and facilities must meet increasing patient demands for lithotripsy services.

The most common lithotripsy procedure is referred to as extracorporeal shock wave lithotripsy (ESWL). ESWL is a noninvasive procedure that uses high-intensity acoustic pulses, or shockwaves, generated by a lithotripter machine to break up kidney stones that are too large to pass through the urinary system. Another common lithotripsy procedure is ureteroscopy with laser lithotripsy which utilizes a ureteroscope and laser fibers to break up the kidney stones. ESWL is typically used for stones inside the kidneys while ureteroscopy is typically used for stones inside the ureter.

Lithotripsy procedures can be performed on an outpatient basis in a variety of formats such as fixed-site, transportable, and mobile. While there are many providers of lithotripsy services throughout North America, the two most recognized names in the mobile lithotripsy space are NextMed and United Medical Systems (UMS). In addition to these nationwide providers, there are smaller, physician-owned providers that service healthcare facilities on a geographic/regional basis.

One approach for facilities to meet the increasing demand for lithotripsy services is to enter into arrangements with lithotripsy providers through professional service agreements. Oftentimes, healthcare facilities find it to be financially prudent to purchase lithotripsy services on an as-needed basis rather than purchase equipment, employ dedicated staff, and fund other expenses associated with the service. In those instances, the hospital or ambulatory surgery center (ASC) will contract with a lithotripsy provider to assume responsibility for all costs related to the operation of the lithotripsy service. In return, the hospital or ASC will pay a predetermined fee to the provider for the services rendered.

The contracted fees are structured to compensate the lithotripsy providers for equipment, personnel, and other costs related to the lithotripsy service. The agreements are usually structured on a mutual, nonexclusive basis with key responsibilities delegated between the facility and the provider. Typically, the provider is responsible for transporting and maintaining the lithotripsy equipment, training and licensing the technician to assist with the procedure, and providing the supplies required to support the procedures.

The most common fee structure consists of a price per lithotripsy procedure. In addition, many agreements consider a maximum annual payment for lithotripsy services to determine the commercial reasonableness of the services agreement. In other words, it must be financially prudent for the facility to purchase lithotripsy services on an as-needed basis rather than purchasing the equipment,

employing the staff, and funding the other operating costs associated with the provision of the services. Other fees that may be included in a lithotripsy services agreement include cancellation fees, minimum on-site charge fees, and after-hours/holiday fees. Regardless of the fee structure of the agreement, the arrangement between the facility and the provider must be understood and followed by both parties for regulatory compliance.

For lithotripsy and similar equipment-based arrangements to maintain compliance, the compensation stated in a service agreement between a facility and a provider must be set at fair market value (FMV). To determine the FMV of service agreements, the environment surrounding healthcare must be considered. The bodies of law often considered include the federal Anti-Kickback Statute and the Physician Self-Referral Law (Stark Law). These statutes provide guidance in determining whether service agreements between facilities and providers, such as lithotripsy service agreements, are compliant and based on FMV.

The Stark Law prohibits physicians from ordering designated health services (DHS) for Medicare patients from entities with which the physician has a financial relationship. However, lithotripsy services are not considered DHS for purpose of the Stark Law. Therefore, lithotripsy services agreements are not governed by regulations regarding per-click leasing arrangements. It is important to note the lithotripsy services agreement must be structured to provide full-service lithotripsy services, and not just a lease of the lithotripsy equipment.

When completing an FMV analysis of lithotripsy services agreements, one must consider the rising cost of equipment and technology advances, staffing pressure causing rising labor costs, requests for quality assurance programs, and market-specific trends such as volume trends and service areas. As the demand for lithotripsy services continues to rise, it will become increasingly important for healthcare facilities to execute proper due diligence and ensure regulatory compliance. To avoid violations of the federal Anti-Kickback Statute and the Stark law, parties must document why an agreement for lithotripsy services is at fair market value.

Noteworthy for investors of ambulatory surgery centers (“ASCs”), the Office of Inspector General (“OIG”) released a favorable (low risk) Advisory Opinion (No. 21-02)1 on April 29th, 2021. The Advisory Opinion reviewed a proposed arrangement (“Arrangement”) in which a health system (“Health System”), manager (“Manager”) and five orthopedic surgeons and three neurosurgeons employed by the Health System (“Physician Investors”) would like to invest in a new ASC (“New ASC”). The offer or payment of investment returns from an ASC to an investor constitutes remuneration under the Federal anti-kickback statute. As a result, the Advisory Opinion analyzed if the Arrangement, if assumed, would constitute justification for the imposition of sanctions under the Federal anti-kickback statute.

According to the Advisory Opinion, “the Proposed Arrangement, if undertaken, would generate prohibited remuneration under the Federal anti-kickback statute if the requisite intent were present, the OIG would not impose administrative sanctions on Requestors in connection with the proposed Arrangement under sections 1128A(a)(7) or 1128(b)(7) of the Act, as those sections relate to the commission of acts described in the Federal anti-kickback statute.”

Under the Proposed Arrangement, both the Health System and its affiliated physicians, including Physician Investors, would be in a position to generate or influence referrals to various beneficiaries of Federal health care programs to the New ASC. In order to limit the ability of the aforementioned physicians to make or influence referrals, the Health System would disallow any action that required and/or encouraged any physician or medical staff members refer patients to the New ASC or to the Physician Investors. In addition, the Health System would refrain from tracking any referrals made to the new ASC by its affiliated physicians. Further, the compensation received by the affiliated physicians from the Health System would be consistent with Fair Market Value and would not be related in any way, to the volume or value of referrals that the Health System’s affiliated physicians make to the New ASC or its Physician Investors. Lastly, the Manager also attested that it would not make or influence referrals in any way to the Physician Investors or to the New ASC.

According to the Advisory Opinion, the Health System certified the following:

The Advisory Opinion acknowledged several ways that the Arrangement mitigated risk and keys questions that should be asked in similar situations which are listed below:

Although the Advisory Opinion is favorable, the OIG took the unique stance of relying heavily on the Health Systems’ certifications as previously discussed. In addition to the certifications, the OIG offered a multitude of factors that should be carefully considered for similar arrangements. The safeguards outlined in the opinion demonstrate regulatory guidance remains an important part of investing in health care. All interested parties should consider their referral relationships, as well as guidance provided by this opinion and applicable laws before finalizing a similar arrangement.

Endnotes

1 OIG Advisory Opinion 21-02 available at:

https://oig.hhs.gov/fraud/docs/advisoryopinions/2021/AdvOpn21-02.pdf

Authors