Q3 2022 Snapshot: A Look Inside the Earnings Calls of Public Healthcare Operators

December 15, 2022

By: Madi Whyde, Savanna Ganyard, CFA, Jordan Tussy, and Madison Higgins

VMG Health reviewed the earnings calls of publicly traded healthcare operators that reported earnings for the third quarter that ended on September 30, 2022. By focusing on the major players in select subsectors defined below, we analyzed the frequency of certain keywords including inflation, COVID-19, interest rates, premium labor, and others. We used these keywords to identify which topics commanded the room this earnings season. Highlights from the calls are summarized in this article.

Companies Reviewed:

Acute Care Hospitals: Community Health Systems, Inc. (CYH), HCA Healthcare, Inc. (HCA), Tenet Healthcare Corporation (THC), Universal Health Services, Inc. (UHS)

Ambulatory Surgery Centers: Surgery Partners, Inc. (SRGY)

Diagnostic Imaging: RadNet, Inc. (RDNT)

Dialysis: DaVita Inc. (DVA)

Diversified Managed Care: Humana Inc. (HUM), UnitedHealth Group Incorporated (UNH)

Laboratory: Quest Diagnostics Incorporated (DGX)

Physician Services and Other: U.S. Physical Therapy, Inc. (USPH)

Post-Acute: Acadia Healthcare Company, Inc. (ACHC), Amedisys, Inc. (AMED), Chemed Corporation (CHE), Enhabit, Inc. (EHAB), Encompass Health Corporation (EHC), Select Medical Holdings Corporation (SEM)

Risk-Bearing Organizations: Agilon Health, Inc. (AGL), CareMax, Inc. (CMAX), Privia Health Group, Inc. (PRVA), The Oncology Institute, Inc. (TOI)

Key Takeaway: Volume

Volume:Although volume trends are unique to each industry sector nearly all operators remained focused on the impacts of COVID.

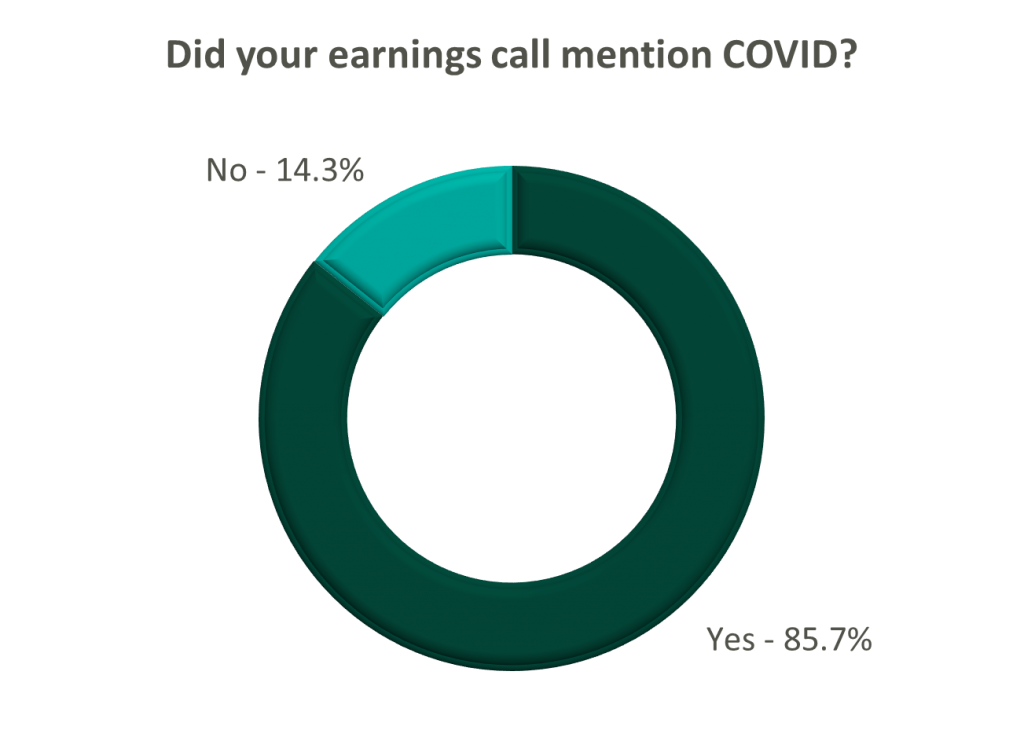

Poll:Did the earnings call mention COVID-19?

Acute Care Hospitals

On a same-facility basis, admission volumes declined as much as 5.0% from the comparable prior year quarter (Q3 2021) for acute care hospital operators. Despite the weakening of COVID-19, the decline in volumes was attributed to higher-than-average cancellation rates (THC), the migration of certain procedures to outpatient status (CYH and HCA), and capacity constraints (HCA). Inpatient volumes generally remained at or below pre-pandemic levels.

Ambulatory Surgery Centers

Ambulatory surgery center (ASC) operators reaped the benefits of the migration to the outpatient setting and reported positive volume trends when compared to Q3 2021. Surgical volumes were reported as consistent with 2019 pre-pandemic levels (THC), and one operator claimed the business did not experience any material direct impact related to COVID-19 during Q3 2022 (SGRY).

Post-Acute

The post-acute sector reported mixed results in volume trends. One operator reported a year-over-year decline of 14.0% in hospice admissions, citing capacity constraints and reduced referrals from acute care hospitals (EHAB). However, another operator indicated that increases in admissions in the second half of the third quarter showed growth that they “haven’t experienced since the start of the pandemic” (CHE).

All Other

Volume trends among other industry players including dialysis providers, risk-bearing organizations, and physician services were also affected by COVID-19 in Q3 2022. Headwinds in dialysis volumes are expected to persist for the foreseeable future (DVA), and inpatient volumes for risk-bearing organizations remain below pre-pandemic levels (AGL). Notably, AGL also reported a rebound in physician office visits and outpatient volumes were in line with pre-pandemic levels.

Key Takeaway: Reimbursement

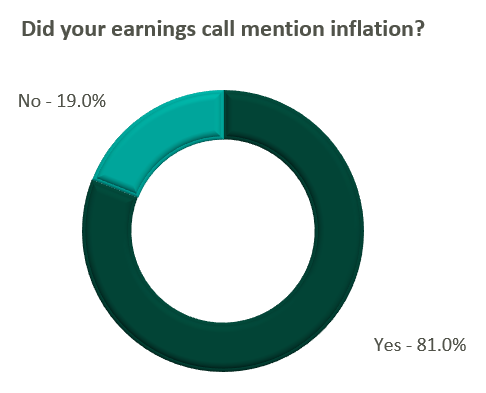

Reimbursement:Declining COVID-19 volumes mean less incremental government revenue for certain industry players who also now contend with an uncertain inflationary environment.

Poll: Did the earnings call mention inflation?

Acute Care Hospitals

Declining COVID-19 volumes resulted in lower acuity patients and reduced incremental government reimbursement. This softened the reimbursement per admission for the acute care hospital segment. Further exacerbated by inflation, these dynamics were evident in reported EBITDA margins which declined as much as 17.0% (CYH) over Q3 2021. In response, some acute care hospital operators are turning to commercial payor negotiations. Rate increases for the next year are anticipated to range from a minimum of 3.0% (THC) to upwards of 6.0% (CYH).

Post-Acute

The post-acute sector did not release specific figures regarding contract rate hikes. However, the sector is optimistically looking for high single-digit rate increases (SEM) to provide relief in the current inflationary environment.

Key Takeaway: Labor

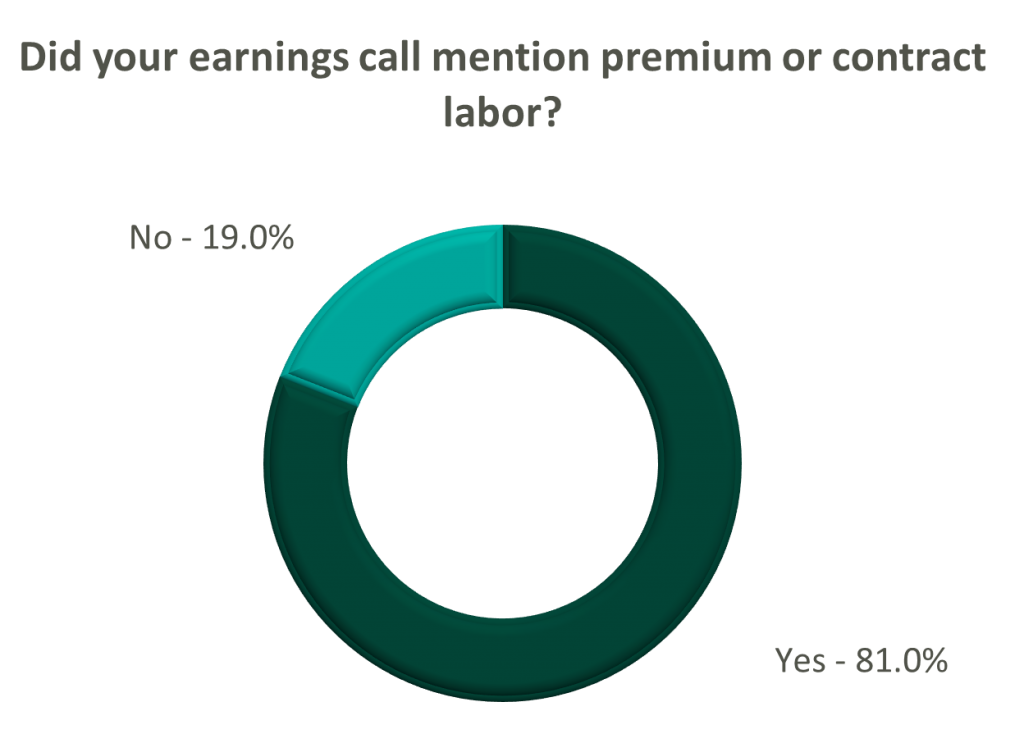

Labor:Unsurprisingly, management teams across the sector were faced with questions about labor trends and management techniques during their earnings calls. Contract labor remained pivotal for the operations of some, but premium labor appears to have softened during the quarter.

Poll: Did the earnings call mention premium or contract labor?

Acute Care Hospitals

The reliance on contract labor continued its downward trend in Q3 helping moderate expenses. HCA even indicated overall labor costs were stable due to targeted market adjustments. However, contract labor and premium pay remain at uncomfortably high levels for most acute care hospital operators. UHS revealed during their call it will be unlikely to reach pre-pandemic levels in the near future.

Post-Acute

Staffing challenges persisted among the post-acute operators and directly impacted volume by as much as 60.0% (AMED). Increased indirect labor costs including orientation, training, and sign-on bonuses were the leading drivers of decreased EBITDA (AMED). Wage inflation, particularly for nursing positions, is expected to rise as much as 5.0% next year (SEM). However, several management teams are optimistic wages will stabilize to historical levels (SEM, EHC) in the near future.

All Other

Other industry players, including dialysis and physical therapy providers, also faced challenges with contract labor during the quarter. USPH reported labor costs were approximately 200 basis points higher than Q3 2021 levels, and DVA indicated such costs showed no improvement.

Key Takeaway: Go Forward Expectations and Guidance

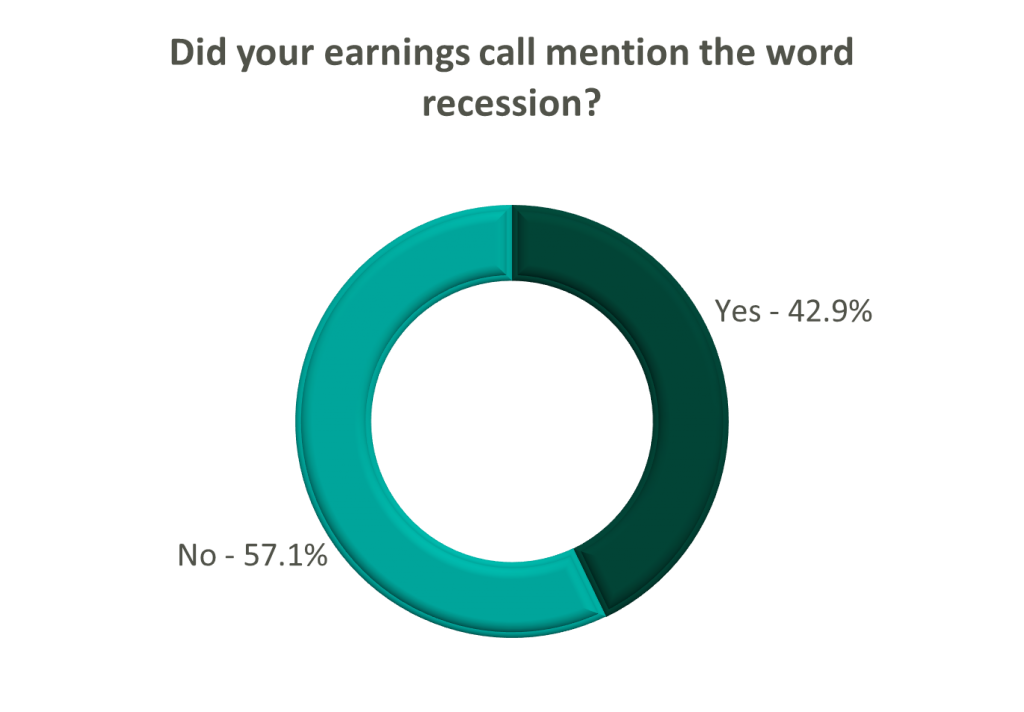

Go Forward Expectations and Guidance:Considering the quarter’s performance, the companies we reviewed were divided relatively evenly in terms of revised FY 2022 revenue guidance, (i.e., raised, lowered, unchanged). In general, the quarter brought about a more pessimistic view of FY 2022 EBITDA, and the majority of public companies lowered their guidance for the year. Further, most stakeholders were left with no guidance for FY 2023.

Poll: Did the earnings call mention a recession?

Acute Care Hospitals

FY 2022 revenue and EBITDA guidance among the acute care hospital operators was generally left unchanged except for THC which lowered EBITDA guidance. However, all companies that were reviewed declined to provide FY 2023 guidance during the call, and primarily cited economic uncertainty (HCA).

Post-Acute

The post-acute sector appeared nearly unanimous in the outlook for the rest of 2022, and most operators lowered their revenue and EBITDA guidance. Unsurprisingly, no one offered FY 2023 guidance during the earnings calls.

Risk-Bearing Organizations

Interestingly, risk-bearing organizations mostly raised their revenue guidance for FY 2022 (AGL, CMAX, PRVA). However, EBITDA guidance was less predictable and was lowered (AGL, TOI), raised (PRVA), and unchanged (CMAX).

All Other

Most other healthcare operators followed similar patterns in terms of providing guidance for FY 2023. Of the companies we reviewed, only DVA revealed an outlook for the next year. The company anticipates revenue to be flat (driven by unfavorable volume trends) and margins to continue to feel the impact of labor market pressures.

By: Jordan Tussy, Hunter Hamilton and William Teague, CFA

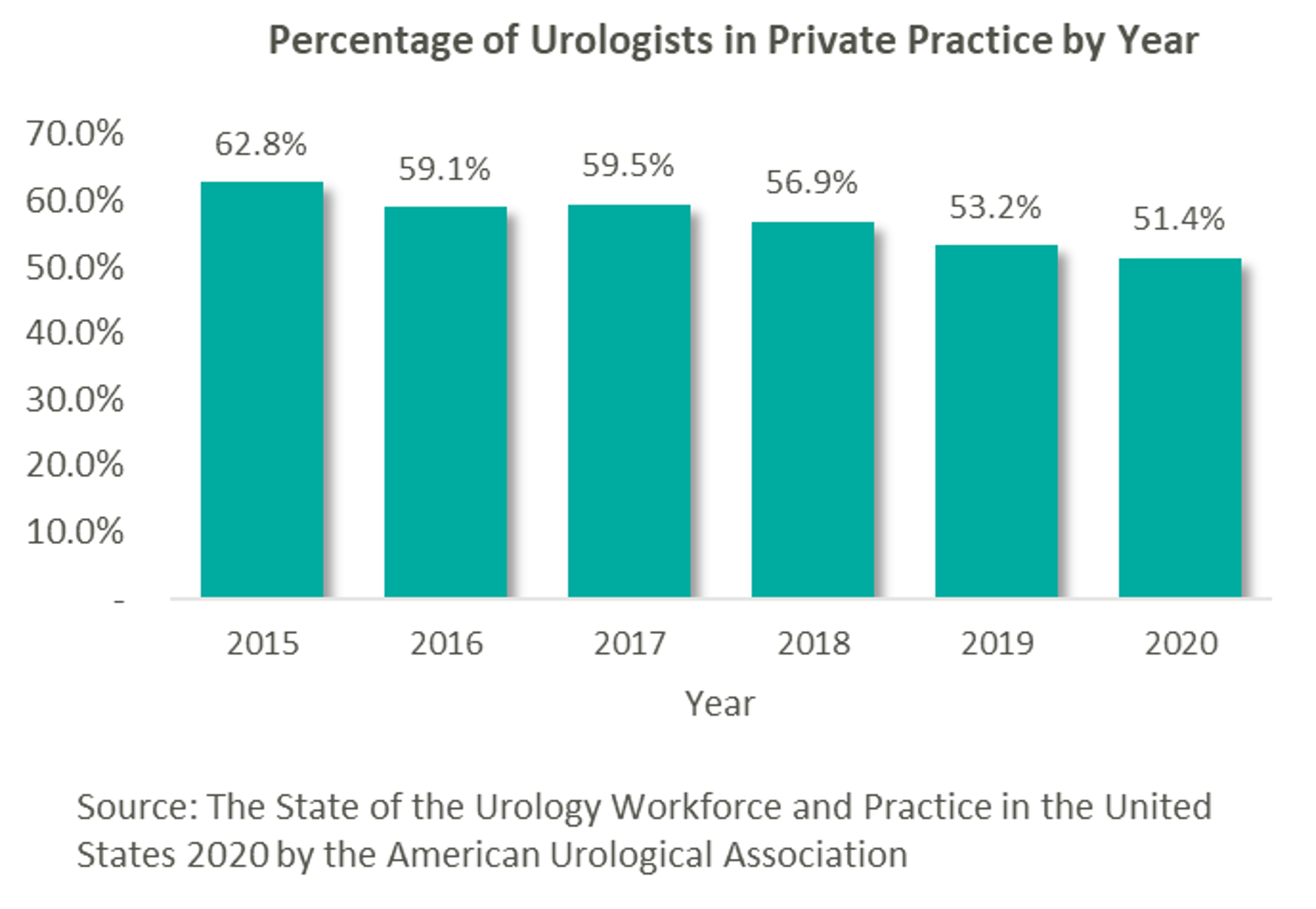

As many physician specialties begin to mature (e.g., gastroenterology, dermatology and ophthalmology), funds have started to flow into the urology space from private equity (“PE”) firms still eyeing platform acquisitions. “Competition for quality assets in this segment is still pretty light. There are a number of independent urology groups of scale with good management teams and back-office infrastructure,” stated Jeanne Proia of Cross Keys Capital in an interview with Mergermarket. [1] Growth prospects for urology practices are also particularly strong due to increases in life expectancy that have led to increases in demand for urologic services. Additionally, an expected shortage of urologists estimated to exceed 3,600 by 2025 will only further amplify the situation. [2] Urology’s several sources of ancillary revenue such as lab & pathology services, lithotripsy, radiation oncology, and ambulatory surgery make the specialty particularly attractive to platforms seeking to execute a roll-up strategy. With over 13,000 urology providers, 51.4% of whom work in private practice, this fragmented market offers PE firms the opportunity to facilitate consolidation. [3]

This prospect, paired with the strong demand for urologic services, has led to significant investment interest in the space, which can trace its roots back to August 2016 with Audax Private Equity’s partnership with Chesapeake Urology and the resulting formation of United Urology Group (“UUG”).

United Urology Group

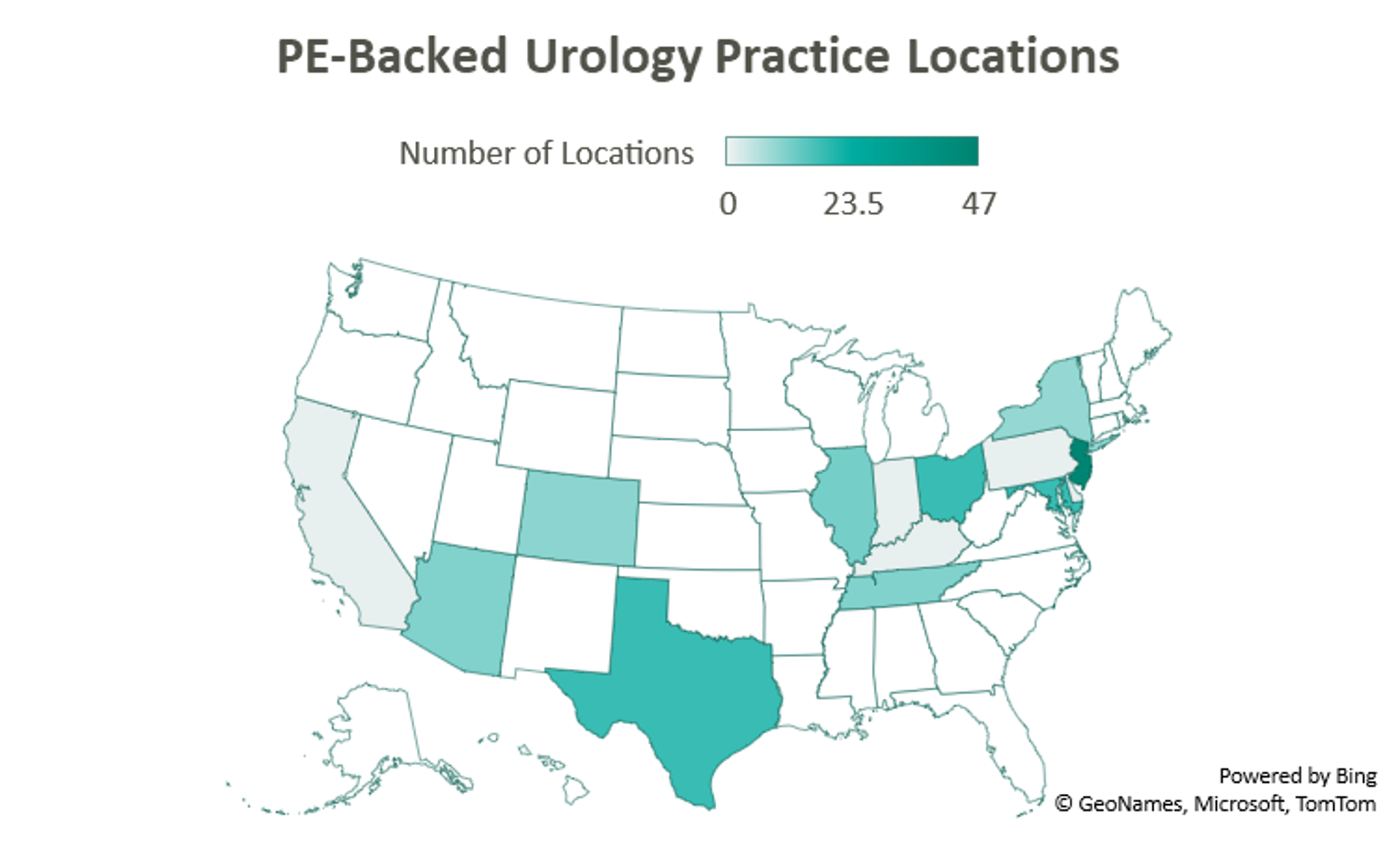

Since acquiring Maryland’s Chesapeake Urology, Audax Private Equity’s UUG has further expanded its footprint both locally in Maryland, as well as nationally. Most recently, UUG has entered Arizona markets through its partnership with Arizona Urology Specialists in late 2019 and additional affiliations with Arizona Institute of Urology and Urological Associates of Southern Arizona in January of this year. Through this most recent partnership, UUG now operates out of 25 offices in Delaware and Maryland, 11 facilities in Tennessee, 10 offices in Colorado, and 23 locations in Arizona. With these locations and over 220 physicians, UUG remains committed to providing accessible care. [4]

Urology Management Associates

Prospect Hill Growth Partners (formerly known as J.W. Childs Associates) partnered with New Jersey Urology (“NJU”), a practice comprised of 96 providers in 46 New Jersey locations, to form Urology Management Associates (“UMA”) in September 2018. [5] NJU, having previously merged with Delaware Valley Urology in April 2018, represented the largest group of urologists in the United States at the time. Since then, UMA has expanded through a partnership with Premier Urology Group in September 2019 and Urology Care Alliance in December 2019. This latest affiliation expanded the platform’s presence in New Jersey and established its stake in Pennsylvania. UMA currently has over 150 providers and operates out of 64 locations, including 6 cancer treatment centers. [6]

U.S. Urology Partners

A 2018 strategic investment by NMS Capital in Central Ohio Urology Group launched US Urology Partners as an employment alternative for practices wanting to maintain their independence. As of August 2019, the hope of the organization’s CEO Mark Cherney was to grow US Urology Partners’ roughly $50M in revenue 10x in the next 3-5 years. Cherney also indicated that urology may be the next physician specialty to see significant consolidation, stating that “while the other physician specialties such as dermatology, dental and ophthalmology have seen heavy M&A activity in recent years, urology has remained relatively untapped for sponsor investment.” [7] Cherney cites shrinking rates of reimbursement, growing administrative costs, a complex regulatory environment, and a lack of independence as deterrents to hospital employment, while a national platform partnership on the other hand can provide “greater management support and financial strength.” [8] The group most recently partnered with Associated Medical Professionals of New York, a nearly 30-physician practice operating out of 9 locations throughout the Central New York region. Ancillary services offered by the practice include radiation oncology, pathology, imaging, lithotripsy services, as well as clinical research. [9]

Solaris Health

Another big presence in the space is Lee Equity Partners, who in June 2020 acquired and merged Integrated Medical Professionals and The Urology Group to form Solaris Health. The goal of Solaris “is to build a national platform that attracts leading independent urological partners who are committed to providing quality and value in healthcare.” [10] The platform has since expanded from its origins in New York, Ohio, Kentucky, and Indiana into Pennsylvania through a partnership with MidLantic Urology and, most recently, into Illinois through an affiliation with Chicago’s Associated Urological Specialists in March of this year. With more than 262 providers, Solaris now operates out of more than 11 sites in six states. [11]

Urology America

With its formal acquisition of Texas-based Urology Austin in October 2020, Gauge Capital established Urology America, a fully integrated urology network providing comprehensive urologic care. The largest urology practice in the metro Austin area, Urology Austin brought 18 locations and over 50 providers to the platform. Also included in the transaction were Urology Austin’s clinical research department, patient navigation programs, pelvic floor physical therapy, the Austin Center for Radiation Oncology, as well as a nationally accredited in-house pharmacy and pathology laboratory. Urology America is currently seeking to partner with urology practices nationally recognized as innovators and leaders in the field. [12]

Urology Partners of America

New to the space is Triton Pacific Capital Partners. This May, the Los Angeles private equity firm partnered with Genesis Healthcare Partners (“GHP”), a Southern California urology group with 48 providers and 15 locations, to establish Urology Partners of America (“UPA”). At the time of the transaction, GHP represented the largest independent urology group on the West Coast. With a current focus on further expansion across the Western States, the platform has a long-term goal, according to UPA CEO, Marshal Salomon, of building “the business to 200+ physicians within the next few years.” [13]

Future of the Field

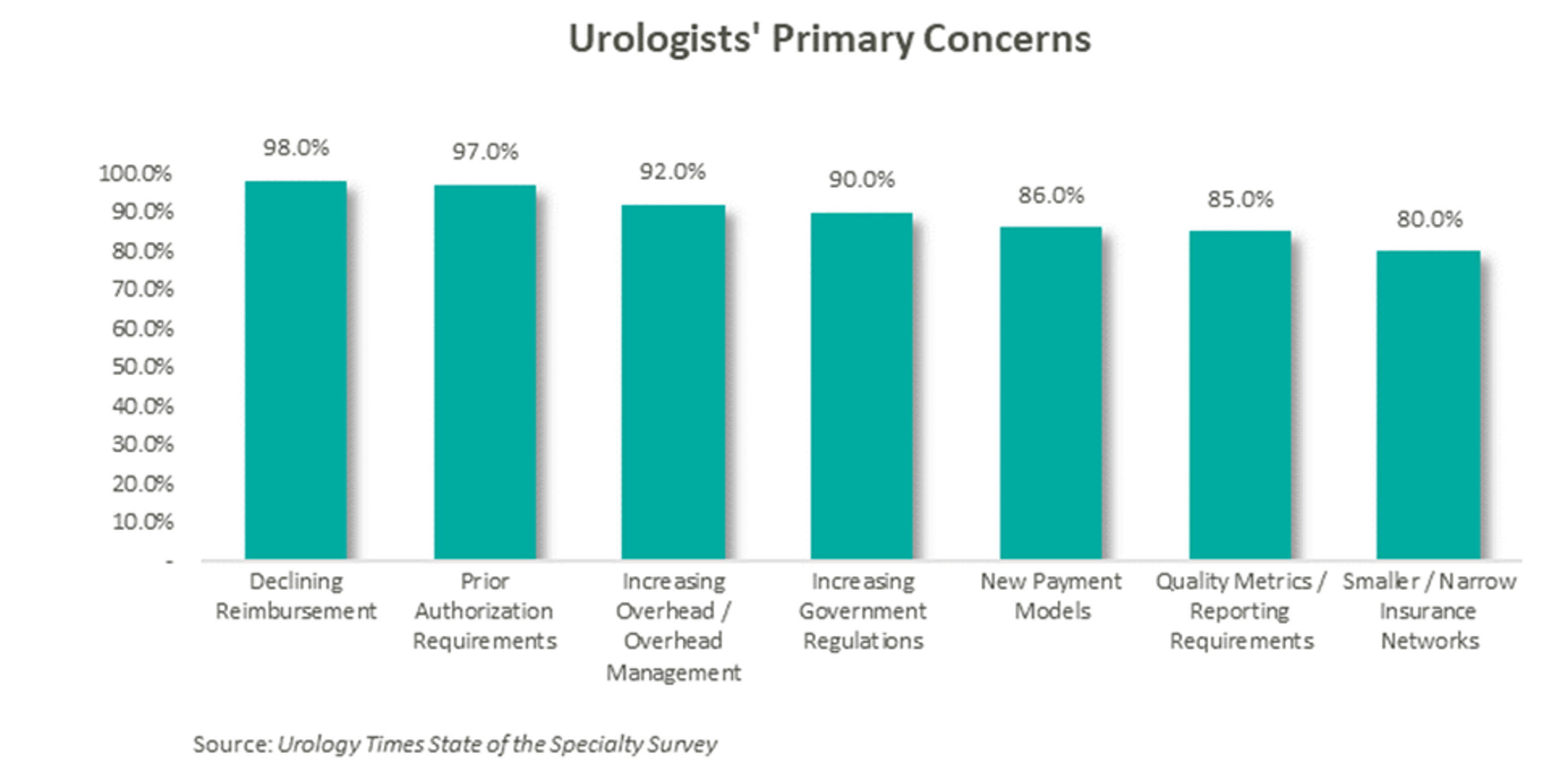

According to data compiled by Urology Times, over 90% of urologists surveyed are concerned about declining reimbursement trends, growing regulation, and increasing overhead costs. [14] Furthermore, a study published in the July 2021 Issue of The Journal of Urology revealed that the average rate of reimbursement per urologic procedure decreased by an average of 0.4% per year from 2000 to 2020 before adjusting for inflation. [15]

As a result of these pressures, independent physicians are seeking alternative employment structures to private practice. PE firms are an attractive option due to their ability to alleviate some of the administrative burden, strengthen payor negotiations though scale, provide access to additional capital and allow the providers to focus on their clinical services. With this model, physicians receive upfront compensation from the acquisition and may retain an equity position in the new entity. They often agree to a reduction in their historical compensation as a trade-off for the promise of future equity returns and current liquidity. The success of the model depends on the ability of the PE firm to provide both operational and financial value to the practice and deliver on earnings repair. Otherwise, shareholder physicians may not continue to perform at historical levels, and non-shareholder physicians may begin to reconsider private practice.

Since the formation of United Urology Group, there has been a trend of PE-backed urology practice consolidation over the past 5 years. Given that most urology visits are with patients over the age of 65 and that nearly 20% of the population is expected to be 65 or older by 2030, demand for urologic services is only expected to increase. [16] With increasing demand, fragmentation, and a complex regulatory environment, continued consolidation should be expected in the urology space. The ability to deliver on earnings recapture through the successful implementation of economies of scale will ultimately determine the outcome of these platforms, as the value of the model hinges on the loyalty of the urologists.