Insights into Healthcare Provider Compensation Trends for 2024

Christa Shephard

March 4, 2024

Written by Christa Shephard, Maureen Regan

Physician assistants (PAs) and advanced practice registered nurses (APRNs), like nurse practitioners (NPs), midwives, CRNAs, and clinical nurse specialists, have been around for decades. The first class of PAs graduated from Duke University in1967, and in 1965, the first training program for NPs began at the University of Colorado. Since then, for many reasons, both professions have become integral to the quality delivery of healthcare. Through advanced practice nonphysician provider (APP) integration, patients experience increased access to the healthcare services they need, and they are more satisfied with the care they receive. Physicians experience greater job satisfaction, as APP integration helps to alleviate the burden on overburdened work schedules. Through these benefits, APP integration leads to better patient retention, physician satisfaction, and stronger financial health for practices and health systems overall.

The Centers for Medicare & Medicaid Services (CMS) certainly plays a role in the practice and reimbursement environment of PAs and APRNs; however, most of the legislative and regulatory environment for practice is determined at the state level. Due to the evolution of each profession and the historical and ongoing shortage of physicians, it’s important for health systems and practices to stay abreast of primary source legislative and regulatory guidance changes regarding scope, documentation, and billing compliance. These factors are also important to ensure an employer is capturing maximum reimbursement for clinical work done by both professions while minimizing their risk of an audit and resulting penalties. Systems and practices must uphold an ongoing, longitudinal review of Medical Staff Bylaws, delineation of privileges, policies, and processes.

CMS recognizes qualified billing providers to render services independently and establishes billing and coding rules for APPs to ensure accurate reimbursement and quality care delivery within the Medicare program. These rules outline the scope of practice and reimbursement guidelines for nurse practitioners, physician assistants, certified nurse-midwives, clinical nurse specialists, and certified registered nurse anesthetists. APPs must adhere to specific documentation requirements, including maintaining accurate patient records and submitting claims using appropriate evaluation and management (E/M) codes. Additionally, CMS provides guidance on incident-to billing, which allows certain services provided by APPs to be billed under a supervising physician’s National Provider Identifier (NPI). Understanding and following CMS billing and coding rules are essential for APPs to navigate the complexities of reimbursement and ensure compliance with Medicare regulations.

Because CMS recognizes APPs as qualified billing providers but not as physicians, APPs fall into a separate reimbursement category. When APPs are billing under their own NPI numbers, the reimbursement level is less than what it would be if the physician were to bill for the same services. Physicians may bill for a service that was rendered by an APP with incident-to services and with split/shared E/M services.

VMG Health Managing Director and coding and compliance expert Pam D’Apuzzo says, “There are two rules, which are where everybody gets themselves into trouble… Those two rules have specific guidelines, both from a documentation and a billing standpoint. The patient type, the service type—everything needs to be adhered to.”

To bill for incident-to and split/shared E/M services, practices must meet specific criteria outlined by Medicare. For incident-to services, the criteria include:

For split/shared E/M services, the criteria include:

These criteria ensure that incident-to and split/shared services are billed appropriately and in compliance with Medicare guidelines. Practices must continually educate and train so that they can successfully adhere to these criteria to avoid billing errors and potential audits. Additionally, practices must continuously monitor to ensure all documentation, billing, and coding processes are followed correctly.

There are tools and services that allow for easier monitoring. “We utilize a tool called Compliance Risk Analyzer, which provides us with statistical insight on coding practices,” D’Apuzzo says. “So, we can data mine ourselves and see what’s happening just based on our views. And this is what the payors, specifically, and the government does as well: They can see the [relative value unites] RVUs are for a physician or off the chart, or that a physician has submitted claims for two distinct services at two different locations on the same day.”

This is more common than you might think.

“What’s normally happening in those interactions is that [a doctor with two locations] realizes he can’t keep up with all of that patient flow in two places, so they hire a PA and put them at location number two,” D’Apuzzo says. “But now all that billing goes under the doctor, so it flags for Medicare.”

With VMG Health’s Compliance Risk Analyzer (CRA), practices can see the same data mining and areas of risk, as the program would flag the RVUs as a potential audit risk. This gives practices the opportunity to self-audit and refine their processes to ensure they are billing and coding appropriately.

VMG Health offers multiple comprehensive services that help health systems and practices implement and follow new procedures like APP utilization without issue, from honoring existing care models to ensuring provider compensation is fair, compliant, and reasonable.

Cordell Mack, VMG Health Managing Director, says, “We’ve spent a lot of time trying to make sure we get that right, both in terms of the underlying, practice-level agreements as well as the ways in which the compensation model works for both the physician and the APP.”

In many practices, physicians struggle to handle their case load, which means their busy schedules can prevent them from seeing existing patients when they need services and from taking on new patients. Bringing APPs into the fold allows physicians to offload some of their patient care so that they can see new patients while APPs see more established patients.

BSM Consulting (a division of VMG Health) Senior Consultant and subject matter expert Elizabeth Monroe provides an excellent example: “Let’s say we have an orthopedic surgeon who really wants to spend most of their time in surgery. We would want to have that physician in surgery because that’s what their skill set and licensure permits. With a nurse practitioner or physician assistant providing follow-up, post-operative care, that oftentimes is a much better model. It allows the MD to do the surgical cases only they can do, but it also eases patient access to care.”

This expansion of a physician’s schedule creates an opportunity to provide more patient services, which easily translates to improved patient satisfaction when, without this expansion, they would likely be unable to see their provider when they felt they needed to be seen. While APP-rendered services are reimbursed at 85% instead of 100%, our experts say that missing 15% shouldn’t dissuade practices and health systems from leveraging the APP integration.

“It’s a very short-sighted approach to just think about, ‘But we could be making 100% instead of 85% if we bill under the doctor,’ because ultimately, we are never able to do that 100% of the time, and it’s a higher risk than it is reward,” says D’Apuzzo.

Additionally, physicians with packed schedules and no APP support may inadvertently rush through appointments to see each patient scheduled for that day. Patients who feel rushed may leave an appointment feeling unheard and like their problem is unresolved. Alternatively, when a patient calls and asks for services but can’t be seen for multiple weeks or months, they may never make an appointment and instead turn to another provider for help.

All of this culminates in poor patient retention, which equals a loss of revenue for the practice. Dissatisfied patients will seek better treatment and better outcomes elsewhere. However, when practices and health systems embrace APP support, patients are more likely to be able to schedule appointments when they feel they need to be seen, feel heard in an appointment with an APP who has the time to sit and listen, and even spend less time in the doctor’s office overall, as patient wait times significantly decrease with APP appointments.

“Practices are better able to meet patient demand, and they’re able to really allow physician assistants, nurses… to add a tremendous value for the patients, offering them outstanding care,” Monroe says.

With both patient demand and physician scarcity placing the U.S. health system in crisis, many practices and health systems know they need to integrate APPs into their workflows, but they don’t know how. VMG Health offers strategic advisory services that can guide this implementation to ensure practices are educated, compliant, and working within the care model they prefer.

“Our team would want to spend time really trying to identify the underlying care model that practices are trying to, you know, work inside of,” says Mack.

One approach is to assess patient needs and practice capabilities to determine the most effective roles for APPs, such as providing primary care, specialty care, or supporting services like telemedicine. Implementing standardized protocols and workflows can ensure efficient APP utilization while maintaining quality and safety standards.

Finally, ongoing training, supervision, and quality monitoring are essential to support APPs and ensure their integration into the practice or health system effectively meets patient needs.

“It starts with getting your appropriate documentation in place… [with] supervisory responsibilities and collaborating physician agreements,” says Mack. “It migrates to, ‘What’s the operational agreement among the APP and the doctor?’ and how cases are presented, or how the physician is consulted. So, it’s getting an underlying clinical service agreement among those professionals.”

Optimal APP utilization shows up in the numbers. When practices increase patient access to care without overburdening physicians through APP utilization, they can accommodate more patients, leading to increased revenue generation. Moreover, because APPs often bill at a lower rate than physicians, utilizing them efficiently can improve cost-effectiveness, thereby enhancing the overall financial performance of the practice.

“It should realize an ROI, and that ROI should be something more in terms of duties and tasks that other teammates can’t do,” says Mack. “Meaning, it would be unfortunate if an advanced practice professional is working at such a capacity whereby duties some of the day-to-day responsibilities should probably be done by teammates working at a higher level of their own individual license.”

Changing existing workflows can be difficult, but the rewards heavily outweigh the risks. Physicians must support APP integration to successfully navigate the transition. Physicians are typically the leaders and decision-makers within medical practices, and their support is essential for implementing any significant changes in workflow or care delivery models. Without physician buy-in, resistance to change may arise, hindering the smooth integration of APPs into the practice.

Physicians play a vital role in collaborating with APPs and delegating tasks effectively. By endorsing and supporting the integration of APPs, physicians can foster a culture of teamwork and mutual respect within the practice. This collaborative approach promotes a cohesive care team where APPs work alongside physicians to provide high-quality patient care.

It’s important for physicians to trust that their APPs are qualified and capable of providing excellent patient care. Allowing an APP to care for an established patient does not sever the relationship between the physician and the patient; it can actually enhance the patient’s experience and trust in the practice.

“We want patients who have had a long-standing relationship with an MD to be able to see that doctor, and then we want to help the doctor know and understand how to appropriately transfer care over to an APP within their system or within their practice,” says Monroe. “So, that provider can be still linked to the doctor, and the doctor can still be linked to the patient.”

Furthermore, physician buy-in is essential for maintaining continuity of care and ensuring patients feel confident in receiving treatment from both physicians and APPs. When physicians actively endorse the role of APPs and communicate the benefits of team-based care to their patients, it builds trust and acceptance of APP-provided services.

Physician engagement is critical for the long-term success and sustainability of APP integration initiatives. When physicians recognize the value that APPs bring to the practice, including increased efficiency, expanded access to care, and improved patient outcomes, they are more likely to champion these initiatives and advocate for their continued support and development.

The integration of APPs into physician practices and health systems presents a strategic opportunity to optimize patient care delivery and operational efficiency. By expanding access to healthcare services and alleviating the workload of overburdened physicians, APP integration improves patient and employee satisfaction, and enhances patient retention. However, successful integration requires careful attention to regulatory compliance, billing, and coding practices. VMG Health offers comprehensive billing, coding, and strategy advisory services to support practices in navigating the complexities of APP integration, ensuring compliance with Medicare regulations, and maximizing reimbursement while minimizing audit risk.

Optimal APP utilization yields tangible benefits, including increased patient access to care, improved patient satisfaction, and enhanced financial performance. By leveraging APPs’ unique skill sets, practices can accommodate more patients, reduce wait times, and deliver high-quality care cost-effectively. Physician engagement is essential for the successful implementation of APP integration initiatives, as physicians play a pivotal role in endorsing and supporting APPs within the care team. Through collaborative leadership and effective communication, physicians can foster a culture of teamwork and mutual respect, driving the long-term success and sustainability of APP integration efforts.

In summary, strategic APP integration presents a transformative opportunity for physician practices and health systems to meet evolving patient needs, enhance operational efficiency, and achieve sustainable growth. By partnering with VMG Health for expert guidance and support, practices can navigate the complexities of APP integration with confidence, realizing the full potential of this innovative care delivery model.

American Academy of Physician Assistants. (n.d.). History of AAPA. Retrieved from https://www.aapa.org/about/history/

American Medical Association. (2022). AMA president sounds alarm on national physician shortage. Retrieved from https://www.ama-assn.org/press-center/press-releases/ama-president-sounds-alarm-national-physician-shortage

Centers for Medicare & Medicaid Services. (2023). Advanced practice nonphysician practitioners. Medicare Physician Fee Schedule. https://www.cms.gov/medicare/payment/fee-schedules/physician-fee-schedule/advanced-practice-nonphysician-practitioners

Centers for Medicare & Medicaid Services. (2023). Advanced Practice Registered Nurses (APRNs) and Physician Assistants (PAs) in the Medicare Program. Retrieved from https://www.cms.gov/medicare/payment/fee-schedules/physician-fee-schedule/advanced-practice-nonphysician-practitioners

Centers for Medicare & Medicaid Services. (2023). Incident-to billing. Medicare. https://www.cms.gov/medicare/payment/fee-schedules/physician-fee-schedule/advanced-practice-nonphysician-practitioners

Mujica-Mota, M. A., Nguyen, L. H., & Stanley, K. (2017). The use of advance care planning in terminal cancer: A systematic review. Palliative & Supportive Care, 15(4), 495-513. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC5594520/

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

I spoke with King and Spalding attorney Kim Roeder on different, hot-button issues that arise when structuring and valuing different value-based arrangements. It started off as a presentation of different case studies and focused on what Roeder has encountered from a legal perspective and what I have encountered from a valuation perspective. We often receive questions when it comes to structure or even value drivers, and we wanted to present solutions to what we saw or clients struggling with so that they could develop a better understanding of them.

The focus on the metrics themselves and how carefully they need to be considered seemed to be the most surprising. Recent regulations have been really focused on metrics, and that’s what we get the most questions about. I think our audience was also surprised to learn that Kim had experienced those questions as well, and metrics aren’t just a consideration on the valuation perspective. Both legal and valuation perspectives must carefully consider metrics.

Our presentation was a very pragmatic way of illustrating six key issues that often come up during valuation. It’s a great resource for healthcare leaders to reference as they go through and check the boxes to ensure they have thought through all of the considerations that we often see as eleventh-hour issues.

I co-wrote a section of the 2023 Physician Alignment: Tips and Trends Report that discusses quality incentives for providers. It captures key factors to consider, from a valuation perspective, when looking to enter value-based arrangements and where to start.

Value-based arrangements require a very orchestrated balance between legal and compliance, operational champions, and valuation teams. Operational teams should be able to focus on what changes and improvements they want to implement, valuation teams must have an understanding of those goals, and legal and compliance must be involved to ensure the approach is appropriate and compliant. Without cohesion between these three groups, we see those eleventh-hour issues pop up.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.

Written by Cordell Mack, MPT, MBA

Hospitals and health systems have been developing strategies for vertical integration with physician groups for decades. Through the premise of integrated care delivery, “defined as a coherent set of methods and models on the funding, administrative, organizational, service delivery and clinical levels,” U.S. policymakers, healthcare operators and payors expect to improve the quality, service and efficiency of healthcare services. Results of value generated through integrated delivery models are mixed, and the operating model is often confounded with varying market dynamics (payor concentration, culture, physician supply/demand, leadership, etc.) by community.

Regardless of integrated care delivery success, health system employment continues to increase and today accounts for greater than 50% of all practicing physicians. Interestingly and unknown to many, other strategics (private equity, Optum, CVS, etc.) account for approximately another 25%, leaving approximately a quarter of physicians organized in a private practice.

Source: Physicians Advocacy Institute: Physician Practice Trends Specialty Report

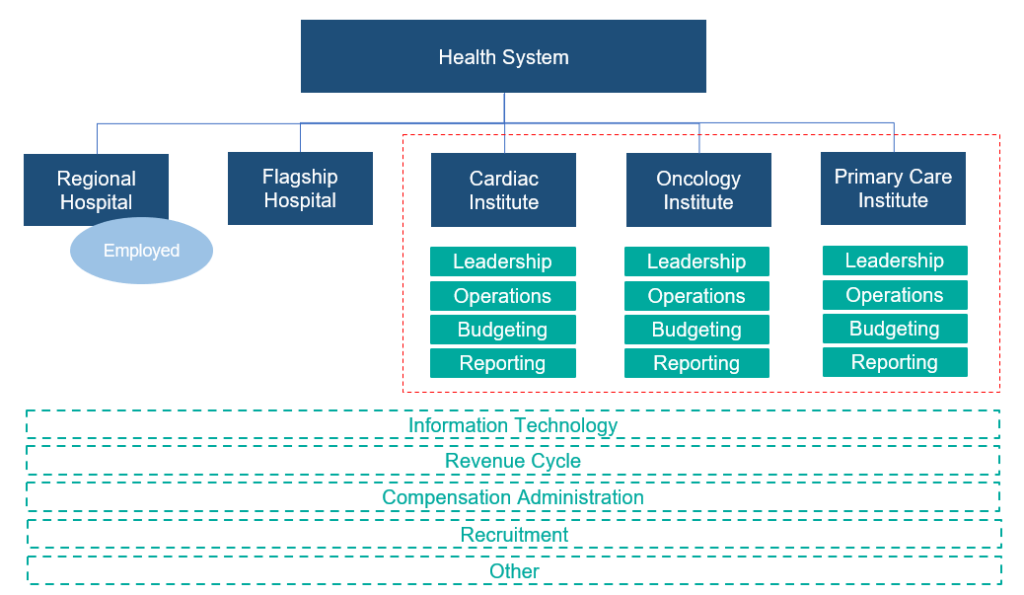

Across many integrated delivery systems, physicians are organized under a formal medical group structure, often with supporting leadership, governance, and practice management systems. This structure essentially groups the collective interests of primary care, surgical subspecialists, medical subspecialists, and hospital-based physicians together. Unlike independent, multispecialty practices who have an underpinning of sharing economics, most multispecialty groups in integrated delivery systems lack material financial alignment across subspecialties.

To this end, there are several challenges with a multispecialty group structure in health systems, including an aggregation of physician losses whereby various revenue streams (e.g., in-office ancillaries) have been integrated with hospital operations, sensitivity to practice losses based on confounding facts as to the true operating performance, silo board and/or decision making, and frustration by large clinical service lines due to widely held convention that everything needs to be the same for all physicians across the physician enterprise. Figure 2 outlines the most prevalent medical group structure and its multispecialty orientation.

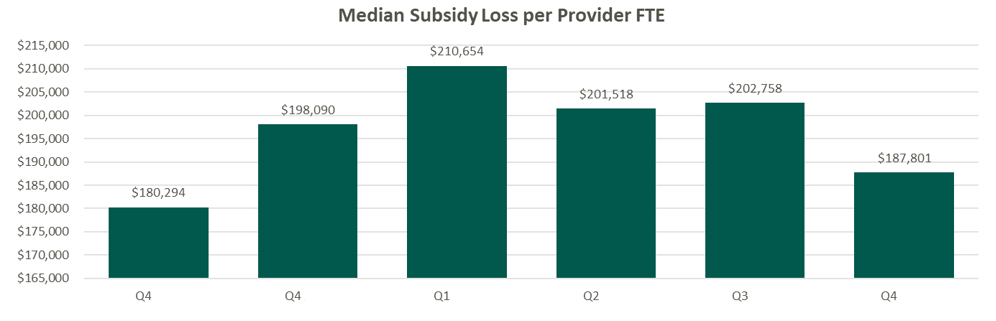

Financial system reporting remains inconsistent across organizations; however, there are data repositories that suggest continued median subsidies for employed providers. As figure 3 outlines, regardless of timing and/or subspecialty orientation, there remains a significant net investment per provider.

Source: Kaufman Hall Flash Reports

Based on VMG Health’s experience, significant financial reporting subsidies lead to suboptimized decision making, as significant pressure is placed on medical group leadership to reduce practice losses and improve overall practice performance. This has led to a variety of strategic missteps for organizations operating in competitive markets.

As an alternative, VMG Health has been working with clients to reorganize physician enterprise offerings inside of integrated delivery systems, including the development of financial reporting, management, and governance systems that better align care delivery across service lines. These more contemporary structures, while variable system to system, are all designed to:

The landscape of physician organizational structures within hospitals and health systems remains in transition. While traditional, multispecialty group practice models remain prevalent, challenges such as physician losses and inconsistent financial reporting have spurred the need for more contemporary structures. Through strategic reorganization and improved governance, health systems can enhance physician loyalty, accountability, growth, and operational efficiency, ultimately optimizing care delivery and aligned (or improved) financial performance.

Heeringa, J., et. al. (2020). Horizontal and Vertical Integration of Health Care Providers: A Framework for Understanding Various Provider Organizational Structures. National Library of Medicine. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC6978994/

Written by Carla Zarazua, Preston Edison, and James Tekippe, CFA

Radiopharmaceutical drugs (RPs) are “radioactive substances used for diagnostic or therapeutic purposes.” To effectively diagnose and treat diseases, physicians need to have access to radiopharmaceutical agents that will assist with detecting and treating medical conditions. The current pricing methodology for RPs under the Centers for Medicare and Medicaid Services (CMS) has created a financial burden on hospitals and health systems. In addition, it has created a barrier to patient access when considering the utilization of diagnostic RPs in hospital outpatient departments. This article will outline the challenges created by the current CMS payment structure and outline steps hospitals and health systems can take to remain compliant with fair market value (FMV) and commercial reasonableness (CR) while CMS reconsiders its position.

In the 2008 Hospital Outpatient Prospective Payment System (HOPPS) final rule, CMS opted to categorize all diagnostic RPs as supplies rather than drugs. Under this current pricing structure, the reimbursement for diagnostic RPs is bundled into the technical procedure rate, known as a “policy-packaged drug.” CMS categorizes procedures with similar costs and clinical work effort into an ambulatory payment classification (APC) group. All procedures in an APC group are reimbursed at the same rate based on the average cost of all the procedures within that APC, inclusive of the primary service, ancillary service, and drug. As such, there is a set price for procedures in an APC group regardless of the policy-packaged drug in use. Unfortunately, this pricing methodology can create a misalignment in the expense incurred to acquire an RP and the reimbursement received from CMS, especially for high-cost drugs.

A report issued by the U.S. Government Accountability Office indicated that CMS will encourage hospitals to use the most effective resource that minimizes costs while still being able to meet the patient care needs. In addition, the structure does not incentivize medically unnecessary services and encourages hospitals to negotiate drug purchase pricing with manufacturers.

There is a temporary exception to the pricing for RPs for new and high-costs drugs, which can qualify for a pass-through period of two to three years. Under the pass-through methodology, the RP will be paid separately from the technical procedure rate at the average sales price + 6% incurred by a provider for the RP. Although this provides some relief to the misalignment of costs and reimbursement for RPs, the pass-through period is finite for an RP, and once outside of the pass-through period, an RP will be bundled or “packaged” within the APC procedure rate. Although CMS’ intent is understandable, under the current pricing model, hospitals may face a challenging financial burden, and providers may be confronted with difficult decisions that may impact patient care.

In the post-COVID era, hospitals have increased focus on increasing margins and reducing costs, and the current payment structure for RPs is putting increased pressure on the hospitals’ and health systems’ bottom line. Various stakeholders have voiced concerns about the economic burden resulting from CMS’ payment structure for RPs. For example, the American Medical Association indicated that, for financial reasons, hospitals may need to limit or end the use of radiopharmaceuticals, especially the high-cost or newer ones, given the misalignment in reimbursement. In addition, the American Hospital Association has put out a statement that the 2024 HOPPS final rule is an “inadequate update to hospital payments.” Hospitals and health systems unfortunately face heavy financial risk if a provider chooses to select a policy-packaged, high-cost drug that is more than the APC payment rate for a procedure. For this reason, hospitals may want to limit the use of the high-cost drugs by its providers, which may cause patients to receive sub-optimal care.

Given this dynamic, providers may choose not to utilize more expensive or advanced RPs, although it may be better off for a patient in the long term. As indicated by the Medical Imaging & Technology Alliance (MITAS), utilizing an advanced RP would be more beneficial in the patient’s overall treatment management, as these RPs have earlier, more accurate detection and can actually reduce the use of other unnecessary treatments because physicians will be in a better position to understand and treat the disease. Even more challenging, some advanced RPs truly have no alternative or substitute, so concerns about costs may result in the use of a less effective RP, which could result in misdiagnoses and ill-tailored treatment plans. Lastly, the lack of reimbursement inhibits innovation and development of new drugs because drug manufacturers would not be incentivized to continue the research and development if the drugs have a low clinical use.

As demonstrated above, there are several issues with the current pricing structure for RPs, but CMS has asked for comments on potential remedies. In the 2024 CMS proposed rule, CMS outlined the following five alternative payment models for RPs:

While various stakeholders appreciate CMS requesting and seeking recommendations on changes to the structure, many stakeholders such as MITAS and the American College of Radiology (ACR) recommend that “CMS establish separate payment for diagnostic radiopharmaceuticals, including a per day cost threshold based on average sales price (ASP) + 6% methodology.” Stakeholders believe this method will allow for adequate reimbursement and treatment access options for patients.

Unfortunately, CMS did not make a decision on how to move forward with the reimbursement structure for radiopharmaceuticals in the 2024 HOPPS final rule. Given the potential, pending changes in reimbursement, and the fact that CMS reimburses some RPs at a lower amount than it costs to acquire them, it is important for hospital outpatient departments to document and outline a plan with their care teams on how best to use RPs within their organization to remain compliant when it comes to FMV and CR. As such, VMG Health has outlined some important factors to consider for each compliance component in the interim.

Fair Market Value:

Although, the price paid for the drug may be within market range upon determining FMV, CMS may not reimburse at this rate for certain RPs. As such, given that CMS is the most widely cited market comparable and a market maker in terms of how these drugs are reimbursed, hospitals may find that they are losing on these types of arrangements. For this reason, it is important to document the legitimate business purpose of the use of the RP:

Commercial Reasonableness:

While CMS hasn’t reached a solution on the changes to reimbursement for RPs, it is important for hospitals and health systems to consider the financial and patient care implications of what RPs providers use. Developing compliance protocols around how best to determine the utilization of these RPs can minimize the risk placed on patients and hospitals.

GAO. (2021). Medicare Part B Payments and Use for Selected New, High-Cost Drugs. United States Government Accountability Office. https://www.gao.gov/assets/720/712727.pdf

SNMMI. (2008). Radiopharmaceutical Reimbursement Under Meidcare: Recommendations for Reform. Socity of Nuclear Medicine and Molecular Imaging. https://s3.amazonaws.com/rdcms-snmmi/files/production/public/docs/Radiopharmaceutical_Reimbursement_Policy_Ltrhd_5-22-08.pdf

Klitzke, A. (2023). Passage of the Facilitating Innovative Nuclear Diagnostics (FIND) Act. American Medical Association Organized Medical Staff Section. https://www.ama-assn.org/system/files/i23-omss-resolution-7.pdf

American Hospital Association. (2023). In OPPS rule, CMS increases payment rates by 3.1%, modifies price transparency rules. AHA. https://www.aha.org/news/headline/2023-11-02-opps-rule-cms-increases-payment-rates-31-modifies-price-transparency-rules

Hope, P. (2023). Comments on CMS–1786–P: CY 2023 Medicare Program: Hospital Outpatient Prospective

Payment and Ambulatory Surgical Center Payment Systems; etc. MITA. https://www.medicalimaging.org/docs/librariesprovider3/mitadocuments/2023.09.11-mita-comments-on-cy-2024-hopps-proposed-rule.pdf?sfvrsn=7c8627e_3/

Stempniak, M. (2023). CMS seeks feedback on issuing separate payment for diagnostic radiopharmaceuticals. Radiology Business. https://radiologybusiness.com/topics/healthcare-management/healthcare-policy/cms-seeks-feedback-issuing-separate-payment-diagnostic-radiopharmaceuticals

American College of Radiology. (2023). ACR Submits Radiology-Specific Comments About the 2024 HOPPS Proposed Rule. ACR. https://www.acr.org/Advocacy-and-Economics/Advocacy-News/Advocacy-News-Issues/In-the-Sept-16-2023-Issue/ACR-Submits-Radiology-Specific-Comments-About-the-2024-HOPPS-Proposed-Rule

While the valuation of a public company is dependent on macroeconomic, industry, and company-specific factors, VMG Health has attempted to isolate key drivers of the recent market pullback of public healthcare operators. Specifically, VMG Health has isolated two variables:

VMG Health reviewed the change in enterprise value, EBITDA, and the implied forward multiple, as defined below, of 17 publicly traded healthcare operators from December 31, 2021, to June 10, 2022. We then quantified the impact on enterprise value for each of the identified companies in Exhibit A resulting from fluctuations in EBITDA as compared to the implied forward multiple over the observed period.

Based on a review of 17 publicly traded healthcare operators, aggregate total enterprise value declined by approximately $46.1 billion, or 15.0%, from December 31, 2021, to June 10, 2022. While 10 of the 17 companies now have lower consensus EBITDA estimates, this appears to account for only 10.9% of the enterprise value decline. The overwhelming reduction in the total enterprise value is due to multiple contraction with 13 of the 17 companies currently trading at a lower implied multiple.

Furthermore, 14 of the 17 public operators experienced a decline in enterprise value over the last six months, whereas Acadia Healthcare Company, Inc., LHC Group, Inc., and U.S. Physical Therapy, Inc. were the only three companies that saw an enterprise value increase over the same period [2]. Unsurprisingly, these companies also did not experience multiple contraction.

The two publicly traded diagnostic laboratory businesses, Laboratory Corporation of America Holdings and Quest Diagnostics Incorporated, experienced the most significant enterprise value decline because of multiple contraction. On average, the implied forward EBITDA multiples decreased by approximately 4.0 turns of EBITDA, from around a 13.0x to approximately a 9.0x.

Select Medical Holdings Corporation (“Select”) saw the most significant enterprise value decline due to a decrease in consensus EBITDA estimates. Select’s EBITDA has declined by almost $150.0 million over the last 6 months, which has resulted in a 15.6%, or $1.2 billion, reduction in enterprise value. Overall, the trading multiples for public operators within the post-acute care sector have remained relatively flat, but consensus EBITDA estimates have declined by approximately 6.7% with an approximately $2.6 billion impact on enterprise value.

Among the publicly traded acute-care hospital operators, HCA Healthcare, Inc. experienced the most significant dollar reduction in enterprise value, decreasing $19.6 billion, or 17.0%, from $115.3 billion to $95.8 billion. Of this change, approximately 62.6% was due to multiple contraction and 37.4% was due to consensus EBITDA decline. Collectively, enterprise value for the acute care hospital sector decreased by approximately 14.2%, or $24.0 billion, driven primarily by a contraction in trading multiples of nearly 1.0 turn of EBITDA.

Of the other publicly traded healthcare operators observed, Surgery Partners Inc. experienced the most significant impact on enterprise value, on a percentage basis, due to the contraction in implied multiple. The company’s multiple declined by almost 5.0 turns of EBITDA from December 31, 2021, to June 10, 2022, resulting in a $1.9 billion, or 21.8%, reduction in enterprise value. Overall, declines in consensus EBITDA estimates did not have as significant of an impact on enterprise value as implied multiple contraction for the other companies with two of the five operators experiencing growth in their consensus EBITDA estimates over the observed period.

The equity markets continue to react to macroeconomic factors, such as interest rate fluctuations, as well as industry-specific information, including rising labor costs. While many of the public companies currently have lower consensus EBITDA estimates for FY 2022, the market seems to have also pulled back on valuations, as evidenced by the decline in the implied forward multiples. It is yet to be determined if this reduction is short-term in nature, and VMG Health will continue to monitor the public markets.

[1] VMG Health relied on S&P Capital IQ for the FY 2022 consensus EBITDA estimates as of December 31, 2021, and June 17, 2022. The consensus EBITDA as of December 31 is primarily based on analyst estimates following companies’ Q3 2021 earnings calls through December 2021. Similarly, the consensus EBITDA as of June 17 is largely comprised of analyst estimates following the Q1 2022 earnings calls through June 2022.

[2] While VMG Health’s analysis focuses on the effect of two variables on enterprise value, we understand there are additional factors impacting public company valuations. For example, following the March 29, 2022 announcement of UnitedHealth’s plan to acquire LHC Group, LHC’s price and forward multiple increased and have remained elevated based on the market expectations of this transaction.

As we enter 2022, we look back to reflect on the major trends that shaped the healthcare sector over the past year. COVID-19 continued to be a major player throughout 2021, forcing healthcare systems to adapt to new variants, rising labor pressures, financial activity, and new regulations. Despite these challenges, the sector remains optimistic and ready to adapt.

Here are five key takeaways we believe defined the healthcare sector over the past year:

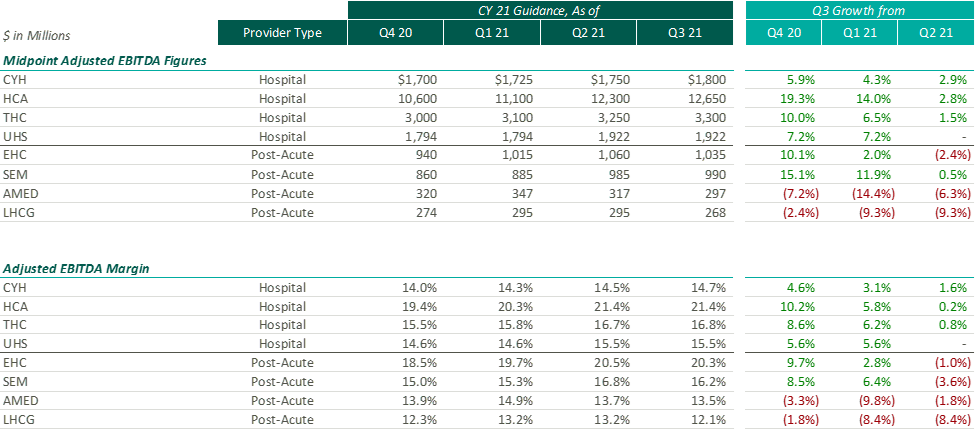

After the Q2 earnings season, VMG Health released an article analyzing post-COVID healthcare operator guidance. Generally, we found that healthcare operators were optimistic about the recovery of their revenue and adjusted EBITDA metrics over pre-pandemic levels, with most operators increasing their FY 2021 guidance with each subsequent reporting period.

While optimism for recovery to pre-pandemic levels remains, it appears that the post-acute operators have tempered some of their recent growth expectations. Based on disclosures of the public operators, the recent resurgence of COVID-19 through the Omicron variant has caused additional strain on the post-acute sector. During the J.P. Morgan Healthcare Conference, Universal Health Services (“UHS”) CFO, Steve Filton noted that the company was struggling to find providers who can accept COVID patients once they are ready to be discharged from the hospital.

Post-acute providers appear to have been hit especially hard by the recent labor shortages in the healthcare industry (discussed further below). As compared to the hospital operators, the financial performance of these post-acute providers has been affected disproportionally by the labor shortages. While hospital operators have been receiving additional reimbursement for COVID patients, helping to offset a portion of the increased staffing costs, the post-acute care providers have not received a similar subsidy.

Due to these recent pressures, Select Medical Holdings Corporation (“SEM”) released an expected earnings announcement in advance of the actual results, in which it noted “the unpredictable effects of the COVID-19 pandemic, including the duration and extent of disruption on Select Medical’s operations and increases to our labor costs, creates uncertainties about Select Medical’s future operating results and financial condition.”

While we have seen increasing optimism by healthcare providers over the past few quarters, the recent disclosures from the post-acute sector illustrate that the effects of COVID continue to ripple through the healthcare sector. With the fourth quarter results being released over the coming weeks (HCA and Encompass recently released), it will be interesting to hear if other sectors report similar headwinds.

Healthcare labor expenses continued to exceed historical levels with a 12.6% year-over-year increase based on a recent analysis of over 900 hospitals. Labor expenses grew at a faster rate than the number of clinical hours worked, which supports the notion that rising labor costs were not due to increased staffing levels but rather due to labor shortages driving higher pay to improve employee retention. Part of the labor shortage can be credited to the surge of Delta and Omicron variants in the second half of 2021 that resulted in high volumes of quarantined staff and a reliance on costly contract labor and travel nurses. At the Bank of America December 2021 Home Care Conference, LHC Group announced a decrease in quarantined staff throughout Q4 from a high of 4% down to 1% in December. This indicates that the labor market issues will see some improvement as health systems’ dependence on pandemic-related contract labor declines as COVID-19 surges dissipate going into 2022.

A more concerning challenge faced by all sectors was the shrinking workforce, coined the “Great Resignation.” The Bureau of Labor Statistics reported healthcare and social assistance workers had the second highest quit rate in November 2021 at 6.4% due to increasingly high levels of professional burnout. The waning labor force has prompted companies to offer additional incentives such as shift and retention bonuses. For example, HCA reported during Q3 a 10-12% annual increase in FTEs being in the premium pay categories. Many large public players have voiced an anticipation of continued high levels of premium pay, competitive bases, and higher annual wage inflation to attract and maintain adequate staffing levels in 2022.

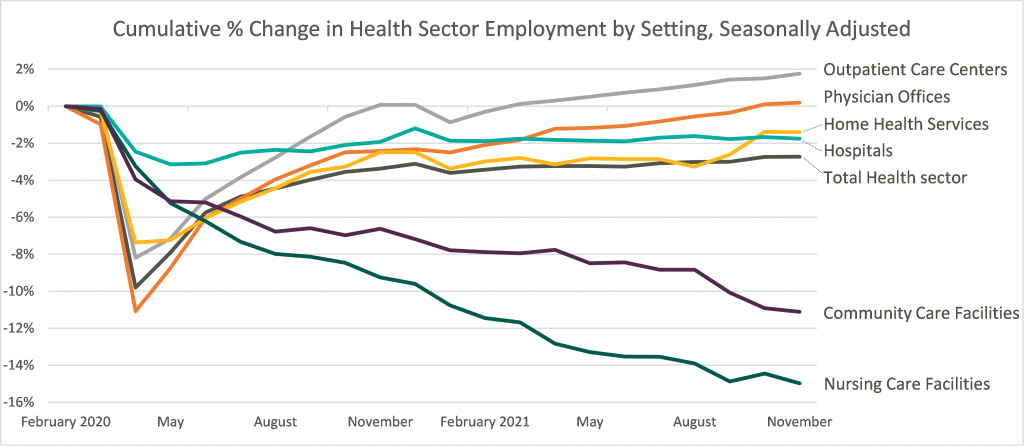

Leaders in the industry have announced initiatives to decrease labor pressure primarily by focusing on recruiting and retention to bounce back to pre-pandemic levels of employment. With a heightened focus on attracting and maintaining adequate levels of hired staff as opposed to contract labor, it appears the overall industry expectation for 2022 is that labor costs will likely decrease compared to 2021 although not to pre-pandemic levels. The chart below shows the percentage change in employment across the healthcare sector from the Bureau of Labor Statistics Job Openings & Labor Turnover Survey from February 2020 to November 2021. This highlights the steady recovery toward pre-pandemic staffing levels for outpatient care and physician offices, the continued employment challenges in home health and hospital settings, and the notable struggle for community and nursing care facilities to return to a state of normalcy.

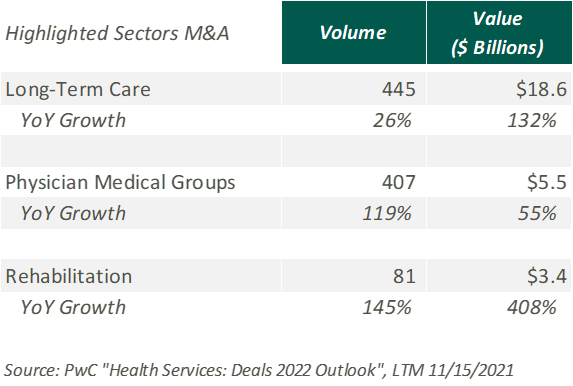

Deal activity within the healthcare sector was strong in 2021 with industry-specific multiples that reached or in many cases exceeded 2019 levels. Experiencing a noticeable rebound from 2020, volume and value of deals grew by substantial margins on a year-over-year basis. Deal volume in the health services industry rose by 56% while value rose 227% in the TTM 11/15/21 period. Long-term care led all sectors with the highest volume of deals, as seen historically, and continues to remain a hot spot in the transaction space. Similarly, physician medical groups and the rehabilitation sector experienced the largest growth transaction volumes year-over-year.

Physician medical groups have received vast interest in physician employment from private equity firms, new-age value-based care organizations, services arms of managed care giants (Optum, Neue Health), and health systems. This, coupled with independent physician group operating challenges from COVID-19 related volume impact and looming Centers for Medicare and Medicaid Services (CMS) cuts, is creating a robust transaction environment that is expected to continue during 2022. For the rehabilitation sector, strong demographic tailwind, along with the lifted CON moratorium in Florida and continued joint venture interest between health systems and strong rehabilitation operators (Select, Kindred, Encompass), has resulted in material deal volume in the space.

Hospitals and health systems were the only sector to see a decline in volume of deals, down 26% from the previous year. Despite the decline, the total transaction size of deals only dropped slightly year over year, indicating larger deal-size on a per-transaction basis. The acceleration of megadeals taking place, the shifted focus on scale, and the diversification of their business models all drove average total size per deal higher than seen before in 2021.

Effective January 1, 2021, the Centers for Medicare and Medicaid Services (CMS) implemented a price transparency rule requiring hospitals in the United States to provide accessible pricing information to patients about the cost of the care they may receive. Hospitals must display negotiated rates for all items and services, in a machine-readable format, so that patients can compare prices before arriving at the hospital.

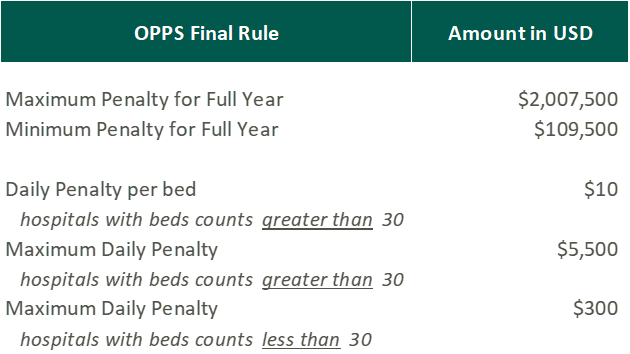

Though, in July 2021, a study was published by PatientsRightsAdvocate.org detailing that a vast majority of hospitals were not compliant with the new rule. At the release of the study, the penalty for non-compliant hospitals was $300 per hospital, per day. While many patients advocate for CMS to stiffen penalties for non-compliant hospitals, healthcare professionals argue against the rule, stating CMS did not provide enough clarity on what the rule should entail.

A vice president of a large U.S. health system discussed the ambiguities around the rule with Fierce Healthcare. “One interpretation is you simply publish your rate schedule – whatever your rate exhibits are in your contracts, publish that and that’s compliant. Another one is to summarize these [CMS] packages [and] what your negotiated charges are.” For many health systems, the resources required to implement their rates in a machine-readable format far outweigh the penalty of remaining non-compliant. The VP stated that he believes many hospitals already provide their rates in a clear, understandable way, but the rule’s lack of clarity and the requirement for a machine-readable format make compliance difficult and costly.

In November 2021, CMS released the 2022 Outpatient Prospective Payment System (OPPS)/Ambulatory Surgery Center (ASC) Payment System final rule (OPPS Final Rule). Within this rule, CMS increased penalties for hospitals that are not compliant with the price transparency rules and removed barriers for patients accessing online pricing information.

While the Final Rule may be beneficial for patients, Stacey Hughes, Executive Vice President for the American Hospital Association (AHA), states that they “are very concerned about the significant increase in penalties for non-compliance with the hospital price transparency rule, particularly in light of the many demands place on hospitals over the past 18 months, including both responding to COVID-19, as well as preparing to implement additional, overlapping price transparency policies.”

The new penalties, visible in the chart above, went into effect on January 1, 2022.

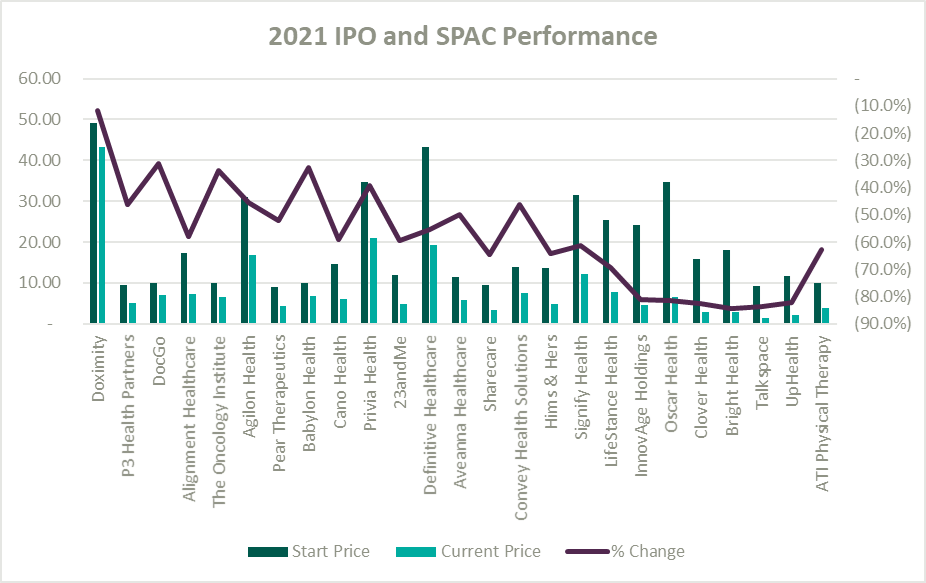

A record number of health and health services companies went public during 2021 by way of SPAC or IPO. Rebecca Springer, a private equity analyst with PitchBook noted, “The multiples in public markets are very, very strong right now, so you can get, all else equal, a better return on your investment if you go public with your company rather than selling it to a strategic investor.”

Unfortunately, while the stock market might be performing well, the recently public healthcare operators have not faired as well since their initial offerings. The Healthy Muse Health Tech Index (“HTI”) generally underperformed the overall performance of the stock market, with the majority of the players finishing in red; the HTI declined 35% as opposed to the 27% gain for the S&P 500 during 2021. The public markets seemed like a perfect place for an exit strategy given the multiples observed in the public markets. All recent entrants finished the year below the original IPO price and while the reasons for the price declines varied it is clear the public markets are less forgiving with valuations if an organization does not achieve expectations.

Overall, the healthcare sector experienced highs and lows during 2021 as it continued to navigate a post-COVID world. As pandemic pressures continue into 2022, healthcare institutions will have to keep a close eye on staffing costs and abide by new regulations. Despite these challenges, the appetite for M&A transactions and market participation in the sector remains strong. We look forward to a new year of challenges, wins, and continued changes in this interesting industry.

https://www.cms.gov/medicare/covid-19/new-covid-19-treatments-add-payment-nctap

https://www.pwc.com/us/en/industries/health-industries/library/health-services-deals-insights.html

https://www.policymed.com/2021/12/cms-announces-increased-fines-for-transparency-violations.html

Related Content