How to Optimize the Value of Advanced Practice Providers: Workflow, Coding, & Compliance

Christa Shephard

May 8, 2024

Written by Ashleigh Surgeon and Caroline Dean, CVA

In recent years, the anesthesiology market has seen many changes in compensation trends and practice models. With continued provider shortages and a growing demand for anesthesia services, providers in this specialty are becoming increasingly valuable. Specifically, certified registered nurse anesthetists (CRNAs) have become some of the most sought-after advanced practice providers in the industry, leading to significant increases in compensation for these providers. In addition, hospitals and health systems are shifting to expanded CRNA utilization as opposed to physicians due to the ongoing push for cost-effective treatment options. Understanding the factors impacting CRNA compensation trends is crucial to anticipating and addressing potential challenges in the pursuit of CRNA arrangements.

According to Becker’s ASC Review, the anesthesiology market is facing a projected shortage of 12,500 providers by 2033. As basic economic principle rules, a decrease in supply of any healthcare provider drives demand upward, forcing costs of anesthesia services and provider compensation upward as well. In 2023, median compensation for CRNAs in the United States was reported at $221,300, an increase in total cash compensation of 11.3% from 2022.

Source: Sullivan, Cotter and Associates, Inc. 2019-2023 Physician Compensation and Productivity Survey and 2019-2023 Advanced Practice Provider Compensation and Productivity Survey

This is a significant rise as compared to general physician assistants and nurse practitioners, who saw only a 5% increase on average from 2022 to 2023. This level of compensation is mostly accredited to the additional education and training required for the certification, as well as the increased risk and level of independence associated with their standard practice.

To receive certification from the National Board of Certification and Recertification for Nurse Anesthetists (NBCRNA), a candidate must first complete registered nurse training and the appropriate clinical experience. Then CRNAs complete a Nurse Anesthesia program, which grants the candidate a master’s degree. Program length varies from two to four years and includes a clinical experience requirement in addition to coursework. In total, the process of becoming a certified nurse anesthetist takes at least seven years to complete, surpassing a standard registered nurse by an average of three years in education and experience. As with any advanced degree, CRNAs often receive increased compensation due to a higher level of education and training than a standard practicing registered nurse.

Because of their advanced training, CRNAs have an increased level of independence in a clinical setting. Though anesthesiologists may manage high-acuity surgeries, CRNAs in many states and facilities may be responsible for primary patient care, including informing the patient, completing examinations, developing pain management plans, prescribing medications, administering and monitoring medications, and responding to adverse reactions or emergencies. A CRNA’s involvement in responsibility for patient care puts the provider in higher-risk scenarios when compared to other registered nurse professions. In 23 states, CRNAs may operate independently without the supervision of a medical doctorate. CRNAs are also typically the sole anesthesia provider in many plastic surgery centers, eye surgery centers, dental surgery centers, and gastrointestinal surgery centers. Additionally, in the U.S., many facilities in rural areas with limited healthcare providers use CRNAs for routine surgical services in the specialties of general surgery, obstetrics, and pain management. According to the American Association of Nurse Anesthesiology, CRNAs comprise over 80% of anesthesia providers in rural areas.

Though CRNAs’ level of autonomy may vary depending on location, state government regulations and a facility’s scope of services, the importance of CRNAs is often constant across markets. With their ability to operate nearly identically to an anesthesiologist in most general cases, CRNAs also incur the same level of risk as physicians and the increased costs associated with such risk. Increased utilization, higher malpractice insurance expenses, and reimbursement difficulties play a large role in these higher costs for CRNAs, which create a competitive environment amongst healthcare systems when considering compensation in recruitment efforts.

Historically, anesthesiology services have been provided by a mix of physicians and CRNAs together. However, with continued physician shortages and health systems and facilities seeking more profitable provider options, CRNA-heavy care team models have risen to the forefront. In a care team model, one physician typically supervises between one and four CRNAs, allowing the facilities to rely on CRNAs as opposed to more expensive physician coverage. As CRNA utilization grows, so grows CRNA compensation as facilities are forced to offer more lucrative recruitment packages, inclusive of commencement bonuses and higher-dollar salaries to retain top CRNA talent and stay competitive. In addition, as many U.S. lawmakers are pushing to expand the scope of CRNA independent practice, it is likely CRNA utilization will continue to increase.

Additionally, according to the Centers of Medicare and Medicaid Services (CMS), average CRNA malpractice insurance in 2024 is $5,968—nearly 50% higher than the average for all other midlevel providers. This is most likely attributed to the large number of CRNAs practicing independently, and therefore solely liable for any case complications. The most common malpractice claims involving CRNAs include subpar performance during procedures, poor patient monitoring and improper positioning. All three of these claims are extremely serious and can result in recovery complications, severe injury, and even death. As a result, CRNAs face higher medical malpractice premiums than providers not solely responsible for a patient’s care. Health systems and facilities must consider this expense when employing CRNAs’ services, whether they reimburse, subsidize, or include the expense in compensation.

Lastly, anesthesia has seen a downward trend in reimbursement based on the CMS Medicare Physician Fee Schedules as Anesthesia Base Units (ASAs) reimbursement have decreased from $22.27 per unit in 2019 to $20.44 in 2024. In the states where CRNAs can practice independently, CMS will reimburse services provided by CRNAs at these rates. This reduction in reimbursement can impact a provider’s ability to collect sufficient revenue based on professional services alone, often requiring additional compensation or subsidization from a facility to sustain operational costs. This issue is commonly present for providers in a community highly comprised of governmental payors. Public payor rates, such as Medicare and Medicaid, reimburse medical services at a significantly lower rate than private insurance, less than 28% of median commercial rates in 2022. As such, facilities serving a population with a significant amount of governmental insured patients must offer providers a compensation plan not only to offset the practice’s operational costs, but also as an alluring salary serving as incentive to relocate to the market. With a CRNA shortage looming, these underserved areas must stay competitive in compensation offers to recruit and retain the essential services CRNAs provide to the community. This level of competition contributes largely to the upward drive of average CRNA compensation, as majority of the CRNAs are operating in the U.S. in lower-income markets.

In summary, the CRNA compensation market will continue to evolve in the coming years, and health systems and facilities must understand and address these changes to capitalize on the benefits associated with CRNA utilization. VMG Health is frequently engaged to provide fair market value and consultative services to ensure CRNA compensation packages are both competitive and compliant with government regulations. Utilizing in-depth analyses of revenue, market data, costs and recruitment expenditures, and expert experience in similar arrangements, VMG Health can assist in navigating the increasingly important CRNA market.

Becker’s ASC Review. (June 28, 2022). Weathering the storm in Anesthesiology: making the business case and demonstrating the value of Anesthesiology. https://www.beckersasc.com/asc-news/weathering-the-storm-in-anesthesiology-making-the-business-case-and-demonstrating-the-value-of-anesthesiology.html

Sullivan Cotter. 2019-2023 Physician Compensation and Productivity Survey and 2019-2023 Advanced Practice Provider Compensation and Productivity Survey

O’Brien, E. Health eCareers. (January 23, 2023). How Long is CRNA School? https://www.healthecareers.com/career-resources/nurse-credentialing-and-education/how-long-is-crna-school

Munday, R. Nurse Journal. (November 16, 2023). CRNA Supervision Requirements by State. https://nursejournal.org/nurse-anesthetist/crna-supervision-requirements/

AMN Healthcare. (June 23, 2023). CRNAs Practice Updates and Trends. https://www.amnhealthcare.com/blog/physician/locums/crnas-practice-updates-and-trends/

Centers for Medicare & Medicaid Services. 2019-2024 Anesthesia Conversion Factors. https://www.cms.gov/medicare/payment/fee-schedules/physician/anesthesiologists-center

Baxter Pro. (May 6, 2022). The 3 Most Common CRNA Malpractice Claims. https://baxterpro.com/the-3-most-common-crna-malpractice-claims/#:~:text=Do%20CRNAs%20Get%20Sued%20More,the%20benefits%20of%20the%20job

American Society of Anesthesiologists. (December 2022). Anesthesia Payment Basics Series: #3 Payment, Conversion Factors, Modifiers. https://www.asahq.org/quality-and-practice-management/managing-your-practice/timely-topics-in-payment-and-practice-management/anesthesia-payment-basics-series-3-payment-conversion-factors-modifiers#:~:text=In%202022%2C%20the%20Medicare%20anesthesia,conversion%20factor%20survey%20was%20%2478.00.&text=Overall%2C%20Medicare%20was%20paying%20less,commercial%20rates%20in%20that%20year

Liao. C, et. all. Semantic Scholar (2015). Geographical Imbalance of Anesthesia Providers and its Impact on the Uninsured and Vulnerable Populations. https://www.semanticscholar.org/paper/Geographical-Imbalance-of-Anesthesia-Providers-and-Liao-Quraishi/77112f1f7ca09a86142b4f5e7c065ae9a073dec2

Written by Grayson Terrell, CPA

The following article was published by Becker’s Hospital Review.

In today’s complex healthcare environment, mergers and acquisitions (M&A) are proving to be more challenging than ever, with heightened governmental regulations impacting both the operation of an entity and the purchase and sale of an entity.

To successfully navigate a transaction in the healthcare sector, it is paramount that buyers and sellers make informed decisions through all of the tools made available to them. For sellers, this can come in the form of understanding how their business operates, understanding inefficiencies and growth opportunities, and even understanding what their business is worth. For buyers, informed decision making relies heavily upon understanding the markets in which they are investing, including governmental regulations in some states that may impact their ability to invest and operate; understanding the key operating metrics of similar companies in similar industries; and ensuring that they are paying an appropriate amount for the business. This is especially important because, in healthcare transactions, the capital used to purchase is often provided by investors who are counting on timely positive returns.

Financial due diligence (FDD) is pivotal to the success of any healthcare transaction, as it requires detailed investigation and analysis of a company’s financial information and is used to validate a company’s true run-rate operating potential. With most healthcare M&A transactions, purchase price is based on a multiple of a company’s salable earnings before interest, taxes, depreciation, and amortization (EBITDA). As such, the buyer and seller must perform the appropriate financial due diligence procedures prior to executing a transaction. Below are five vital aspects of the financial due diligence process.

The Quality of Earnings (QofE) process consists of making adjustments to the entity’s reported financial statements to normalize EBITDA. The bulk of these adjustments involve adjusting or removing impacts of non-recurring and one-time items from earnings to arrive at an adjusted EBITDA figure that represents a more accurate view of the entity’s true cashflows. This process also gives the FDD team the opportunity to pose pointed questions related to the entity’s operations, finances, and accounting functions, highlighting key information that could negatively or positively impact adjusted earnings. Specific to healthcare transactions, some of the relevant areas of interest with respect to potential EBITDA adjustments are:

The Quality of Revenue (QofR) analysis may be the most important part of the FDD process when it comes to healthcare-related transactions, given the unique characteristics and nuances of healthcare revenue. During this process in many middle-market healthcare deals, the conversion of revenue from cash basis to accrual basis is a fundamental exercise with respect to the QofE analysis. The cash waterfall approach is the gold standard and therefore the most common method for accomplishing the cash-to-accrual conversion. With this method, detailed billing data is obtained from the entity’s revenue cycle management (RCM) system, which includes charges by date of service and payments by date of service and by date of payment. In this analysis, payments are adjusted back to their specific date of service (accrual basis), and outstanding collections on charges billed during the period under analysis are estimated based on historical collection patterns cut by payor, CPT code, or various other means.

Pro forma adjustments are forward-looking projections on certain aspects of the business, which are layered back in across the historical financial statements. These assumptions can help buyers understand potential areas of future direction and growth opportunities for the company; however, these adjustments should be thoroughly scrutinized during buy-side FDD procedures to ensure the adjusted EBITDA and purchase price are not over- or understated. These estimations tend to lean more in favor of the seller and are often a primary area of focus by the opposing buy-side FDD team. As such, a seller should understand all aspects of the business, especially as they relate to these forward-looking projections, and should be able to support the key inputs utilized to derive these pro forma adjustments. If properly supported, these adjustments often increase the sale price of the business enough to cover the cost of FDD procedures incurred by the seller, if not many times over. Some examples of commonly observed pro forma adjustments in healthcare related QofE reports include:

Another common analysis in FDD procedures is a Net Working Capital analysis, which is used to determine the working capital (current assets less current liabilities, excluding cash and debt) required to operate a business in the post-transaction environment. This subsection of FDD typically involves substantial negotiation between buyers and sellers when approaching the close of a deal, as both parties will view various inputs differently, often striving to set a working capital peg that is more favorable for themselves. As a miscalculation of this peg can cost a seller on a dollar-for-dollar basis if the agreed-upon level of net working capital is not met, it is imperative that management and their advisors are involved and knowledgeable on this calculation.

Most of the time, healthcare transactions occur on a cash-free, debt-free basis. Standard with any cash-basis business, many debt and debt-like items have the potential to be inaccurately reflected within a company’s balance sheet. As such, a Debt and Debt-Like Items analysis can assist buyers and sellers in understanding a company’s debts and liabilities as of the date of sale. These items can include potential tax-related exposures, outstanding litigation and legal settlements, deferred compensation, notes payable, and others.

In closing, FDD is a necessary step in ensuring that sellers have the keys to sell their businesses at the best possible price, and buyers can protect the money of their companies, firms, or investors by making a sound investment in the target company. This proactive approach creates trust between all parties and leads to more lucrative transactions for all.

Written by Grayson Terrell, CPA; Joe Scott, CPA; Lukas Recio, CPA; Wayne Prior, CPA; and the Baker Tilly team

The M&A healthcare industry presents a unique set of challenges, and it is important to have the proper M&A professionals involved to assist with identifying potential deal issues. In addition to financial due diligence experts, M&A tax professionals should assist with understanding and identifying the transactional tax consequences, as the identified tax issues may impact the overall deal structure or may be used to negotiate in the purchase agreement. During the M&A due diligence lifecycle, financial and tax due diligence teams must collaborate closely. This collaboration often uncovers synergies between their processes, enhancing completeness and efficiency. As their work is often completed first, the financial due diligence team may act as the first line of defense and can assist with identifying potential exposures earlier in the process. M&A tax advisors can assist with vetting and quantifying these exposures, which can assist with limiting the identified risks during the purchase negotiations. Tax considerations often influence the structure of a sale, determining whether it’s taxable or tax-free, whether assets or equity are bought, and whether taxable gains can be delayed through methods like earn-outs, installment sales, and debt.

The starting point for tax diligence is understanding the tax entity type of the target included in the transaction. Different tax issues may arise depending on how the entity is treated for tax purposes. The common tax entity types are:

S corporation:

Partnership:

C corporation:

Improper independent contractor classification (applicable to all tax entity types). While some employers misclassify their employees as independent contractors in error, others do it intentionally to avoid paying state and federal payroll taxes by passing that responsibility onto the employee. Employers found to have misclassified their employees are subject to payroll tax and penalties that could succeed to the buyer. During due diligence, it’s important to determine whether independent contractors should be considered full-time employees. A common healthcare tax due diligence issue is the misclassification of certified registered nurse anesthetists (CRNAs), doctors, and other healthcare professionals as independent contractors. It is important to request IRS Form 1099 and understand the services performed by the independent contractors. Depending on the time dedicated to the business, level of pay, direction from the employer, and several other factors, there may be contractors who could be misclassified, resulting in potential payroll tax exposures. The IRS provides a 20-factor test to help make that determination with considerations related to direction and control.

Unclaimed property (applicable to all entity types). Each state has an unclaimed property statute governing when and what types of property must be remitted to it. Examples of unclaimed property include uncashed or unclaimed refund checks, patient overpayments, insurance overpayments, payroll checks, or vendor checks. If unclaimed after a certain period (dormancy period), those checks must be turned over to the state. This is a common issue amongst healthcare providers, as there may be instances where a patient’s insurance covers more than what was originally estimated for an appointment or procedure, resulting in a patient overpayment. In a situation where a healthcare provider sees non-recurring patients, the patients are less likely to use a credit balance toward a future appointment. It is important to review the target’s accounts payable and accounts receivable aging schedules to determine whether there are any balances that give rise to an unclaimed property risk. Financial due diligence teams will likely have access to the target’s financials and can assist with pulling the documentation necessary to evaluate these potential risks. To avoid possible unclaimed property liability, buyers should determine whether the target is properly addressing its escheatable property.

Improper treatment of owner personal expenses (applicable to S and C corporations). Is the S corporation owner using a corporate account for any personal expenses? If so, these payments may be considered compensation and subject to payroll tax. If the employer’s share of payroll tax is unpaid, the buyer could be held liable for the amount owed after the acquisition, including interest and penalties. In parallel, if a C corporation shareholder is conducting similar activities, the IRS or state revenue service may classify these expenses as dividends, which are non-deductible for income tax purposes.

Unreasonable owner compensation (applicable to S and C corporations). Since an S corporation shareholder’s distributive share of income is not subject to self-employment or payroll tax, owners are often motivated to minimize their salary in favor of non-wage distributions. However, if the IRS determines an owner’s salary to be too low based on multiple factors—including profits, business activities, and the shareholder’s involvement in the business—non-wage distributions could be reclassified to wages subject to employment taxes. The buyer may be responsible for this tax if it isn’t resolved before the acquisition. Conversely, if a C corporation shareholder’s salary is too high relative to the available facts, the IRS or state revenue service may deem the compensation to be excessive and reclassify a portion to dividends.

Related-party transactions (applicable to all entity types). A related-party transaction takes place between two parties that hold a pre-existing connection prior to a transaction. There are many types of transactions that can be conducted between related parties, such as sales, asset transfers, leases, lending arrangements, guarantees, and allocations of common costs. These transactions can become problematic when an S corporation utilizes them as a vehicle to get extra cash out of the business. If a shareholder owns both Company A and Company B, and Company A pays the shareholder a below-market salary while also renting a building from Company B (an LLC taxed as flow-through) at inflated rates, it may be considered disguised compensation to avoid payroll taxes. It is important to request copies of the lease agreements and understand the fair market value of the square footage and rent of the property to determine a potential disguised compensation risk as it relates to related-party transactions. Problematic related-party transactions should be addressed during due diligence.

Cash vs. accrual accounting method (applicable to all entity types). The IRS prefers the accrual method, but if a company is on the cash basis of accounting for tax purposes, the buyer should determine whether they meet the requirements to continue using that method. The change in accounting method from cash to accrual may result in additional income that could be recognized in the post-closing period. By identifying the issue and quantifying the potential exposure, the buyer and seller can negotiate who will bear the tax on the additional income.

Pass-through entity tax (PTET) (applicable to S corporations and partnerships). In certain states, eligible S corporations can make PTET elections, whereby the entity is responsible for paying the shareholder’s share of tax at the entity level. States began enacting responses to state and local tax deduction limitation because of the 2017 Tax Cuts and Jobs Act (TCJA), which limited the allowable deduction for state and local taxes on an individual’s tax return to $10,000. The primary benefit is reduction of federal income taxes; however, use caution when evaluating whether benefit exists on state returns. PTET elections may shift the successor liability for state income taxes from the shareholder to the entity. Most of the elections are irrevocable. During due diligence, determine whether the company has made these elections for the states that have enacted these rules. Given the ever-changing PTET rules, companies should maintain a process to review company’s PTET elections.

20 Percent Deduction Under Section 199A (applicable to S corporations and partnerships). Section 199A was enacted as part of the TCJA and provides a deduction for qualified business income (QBI) from a qualified trade or business operated directly or through a pass-through entity. For healthcare providers, the application of Section 199A can be complex due to the nature of healthcare services being classified as a non-qualifying Specified Service Trade or Business (SSTB). However, certain healthcare-related businesses may qualify, such as a dermatology practice’s sales of skincare products or certain laboratories whose tests benefit the healthcare industry but aren’t independently viewed as health services. Additionally, while a doctor, nurse, or dentist is in the field of health, someone who merely endeavors to improve overall well-being, such as a personal trainer or the owner of a health club, is not in the field of health.

Built-in gains tax (applicable to S corporations). When a corporation has converted its status from C corporation to S corporation, or has acquired assets from a C corporation in a tax-free transaction and has a recognition event within five years, it may be subject to a corporate-level, “built-in gains” tax in addition to the tax imposed on its shareholders from the transaction. The buyer can leverage its knowledge of a potential, built-in-gains tax liability, as identified in the due diligence process, to negotiate with the seller such that the buyer would not inherit said liability.

Non-resident withholding (applicable to S corporations and partnerships). State and local governments are permitted to tax the income of their residents and the income of nonresidents if that income is derived from sources within their state or locality. It’s important to ensure that the S corporation or partnership complies with state and local income tax withholding regulations.

When it comes to healthcare acquisitions, it is important to consider the above items from a tax perspective. Financial and tax due diligence teams should work together to help buyers and sellers avoid tax liabilities, identify unrealized tax savings, and structure the transaction in a tax-efficient manner. Baker Tilly’s M&A tax team can assist in identifying the related risks and opportunities associated with healthcare acquisitions, all in an effort to maximize value. If you have any questions or would like additional information, please contact:

Michael O’Connor, Partner Emeritus: Michael.OConnor@bakertilly.com

Michael DeRose, Senior Manager: Michael.DeRose@bakertilly.com

Peter Dewan, Manager: Pete.Dewan@bakertilly.com

Kendra Nowak, Senior Associate: Kendra.Nowak@bakertilly.com

Written by Christa Shephard, Maureen Regan

Physician assistants (PAs) and advanced practice registered nurses (APRNs), like nurse practitioners (NPs), midwives, CRNAs, and clinical nurse specialists, have been around for decades. The first class of PAs graduated from Duke University in1967, and in 1965, the first training program for NPs began at the University of Colorado. Since then, for many reasons, both professions have become integral to the quality delivery of healthcare. Through advanced practice nonphysician provider (APP) integration, patients experience increased access to the healthcare services they need, and they are more satisfied with the care they receive. Physicians experience greater job satisfaction, as APP integration helps to alleviate the burden on overburdened work schedules. Through these benefits, APP integration leads to better patient retention, physician satisfaction, and stronger financial health for practices and health systems overall.

The Centers for Medicare & Medicaid Services (CMS) certainly plays a role in the practice and reimbursement environment of PAs and APRNs; however, most of the legislative and regulatory environment for practice is determined at the state level. Due to the evolution of each profession and the historical and ongoing shortage of physicians, it’s important for health systems and practices to stay abreast of primary source legislative and regulatory guidance changes regarding scope, documentation, and billing compliance. These factors are also important to ensure an employer is capturing maximum reimbursement for clinical work done by both professions while minimizing their risk of an audit and resulting penalties. Systems and practices must uphold an ongoing, longitudinal review of Medical Staff Bylaws, delineation of privileges, policies, and processes.

CMS recognizes qualified billing providers to render services independently and establishes billing and coding rules for APPs to ensure accurate reimbursement and quality care delivery within the Medicare program. These rules outline the scope of practice and reimbursement guidelines for nurse practitioners, physician assistants, certified nurse-midwives, clinical nurse specialists, and certified registered nurse anesthetists. APPs must adhere to specific documentation requirements, including maintaining accurate patient records and submitting claims using appropriate evaluation and management (E/M) codes. Additionally, CMS provides guidance on incident-to billing, which allows certain services provided by APPs to be billed under a supervising physician’s National Provider Identifier (NPI). Understanding and following CMS billing and coding rules are essential for APPs to navigate the complexities of reimbursement and ensure compliance with Medicare regulations.

Because CMS recognizes APPs as qualified billing providers but not as physicians, APPs fall into a separate reimbursement category. When APPs are billing under their own NPI numbers, the reimbursement level is less than what it would be if the physician were to bill for the same services. Physicians may bill for a service that was rendered by an APP with incident-to services and with split/shared E/M services.

VMG Health Managing Director and coding and compliance expert Pam D’Apuzzo says, “There are two rules, which are where everybody gets themselves into trouble… Those two rules have specific guidelines, both from a documentation and a billing standpoint. The patient type, the service type—everything needs to be adhered to.”

To bill for incident-to and split/shared E/M services, practices must meet specific criteria outlined by Medicare. For incident-to services, the criteria include:

For split/shared E/M services, the criteria include:

These criteria ensure that incident-to and split/shared services are billed appropriately and in compliance with Medicare guidelines. Practices must continually educate and train so that they can successfully adhere to these criteria to avoid billing errors and potential audits. Additionally, practices must continuously monitor to ensure all documentation, billing, and coding processes are followed correctly.

There are tools and services that allow for easier monitoring. “We utilize a tool called Compliance Risk Analyzer, which provides us with statistical insight on coding practices,” D’Apuzzo says. “So, we can data mine ourselves and see what’s happening just based on our views. And this is what the payors, specifically, and the government does as well: They can see the [relative value unites] RVUs are for a physician or off the chart, or that a physician has submitted claims for two distinct services at two different locations on the same day.”

This is more common than you might think.

“What’s normally happening in those interactions is that [a doctor with two locations] realizes he can’t keep up with all of that patient flow in two places, so they hire a PA and put them at location number two,” D’Apuzzo says. “But now all that billing goes under the doctor, so it flags for Medicare.”

With VMG Health’s Compliance Risk Analyzer (CRA), practices can see the same data mining and areas of risk, as the program would flag the RVUs as a potential audit risk. This gives practices the opportunity to self-audit and refine their processes to ensure they are billing and coding appropriately.

VMG Health offers multiple comprehensive services that help health systems and practices implement and follow new procedures like APP utilization without issue, from honoring existing care models to ensuring provider compensation is fair, compliant, and reasonable.

Cordell Mack, VMG Health Managing Director, says, “We’ve spent a lot of time trying to make sure we get that right, both in terms of the underlying, practice-level agreements as well as the ways in which the compensation model works for both the physician and the APP.”

In many practices, physicians struggle to handle their case load, which means their busy schedules can prevent them from seeing existing patients when they need services and from taking on new patients. Bringing APPs into the fold allows physicians to offload some of their patient care so that they can see new patients while APPs see more established patients.

BSM Consulting (a division of VMG Health) Senior Consultant and subject matter expert Elizabeth Monroe provides an excellent example: “Let’s say we have an orthopedic surgeon who really wants to spend most of their time in surgery. We would want to have that physician in surgery because that’s what their skill set and licensure permits. With a nurse practitioner or physician assistant providing follow-up, post-operative care, that oftentimes is a much better model. It allows the MD to do the surgical cases only they can do, but it also eases patient access to care.”

This expansion of a physician’s schedule creates an opportunity to provide more patient services, which easily translates to improved patient satisfaction when, without this expansion, they would likely be unable to see their provider when they felt they needed to be seen. While APP-rendered services are reimbursed at 85% instead of 100%, our experts say that missing 15% shouldn’t dissuade practices and health systems from leveraging the APP integration.

“It’s a very short-sighted approach to just think about, ‘But we could be making 100% instead of 85% if we bill under the doctor,’ because ultimately, we are never able to do that 100% of the time, and it’s a higher risk than it is reward,” says D’Apuzzo.

Additionally, physicians with packed schedules and no APP support may inadvertently rush through appointments to see each patient scheduled for that day. Patients who feel rushed may leave an appointment feeling unheard and like their problem is unresolved. Alternatively, when a patient calls and asks for services but can’t be seen for multiple weeks or months, they may never make an appointment and instead turn to another provider for help.

All of this culminates in poor patient retention, which equals a loss of revenue for the practice. Dissatisfied patients will seek better treatment and better outcomes elsewhere. However, when practices and health systems embrace APP support, patients are more likely to be able to schedule appointments when they feel they need to be seen, feel heard in an appointment with an APP who has the time to sit and listen, and even spend less time in the doctor’s office overall, as patient wait times significantly decrease with APP appointments.

“Practices are better able to meet patient demand, and they’re able to really allow physician assistants, nurses… to add a tremendous value for the patients, offering them outstanding care,” Monroe says.

With both patient demand and physician scarcity placing the U.S. health system in crisis, many practices and health systems know they need to integrate APPs into their workflows, but they don’t know how. VMG Health offers strategic advisory services that can guide this implementation to ensure practices are educated, compliant, and working within the care model they prefer.

“Our team would want to spend time really trying to identify the underlying care model that practices are trying to, you know, work inside of,” says Mack.

One approach is to assess patient needs and practice capabilities to determine the most effective roles for APPs, such as providing primary care, specialty care, or supporting services like telemedicine. Implementing standardized protocols and workflows can ensure efficient APP utilization while maintaining quality and safety standards.

Finally, ongoing training, supervision, and quality monitoring are essential to support APPs and ensure their integration into the practice or health system effectively meets patient needs.

“It starts with getting your appropriate documentation in place… [with] supervisory responsibilities and collaborating physician agreements,” says Mack. “It migrates to, ‘What’s the operational agreement among the APP and the doctor?’ and how cases are presented, or how the physician is consulted. So, it’s getting an underlying clinical service agreement among those professionals.”

Optimal APP utilization shows up in the numbers. When practices increase patient access to care without overburdening physicians through APP utilization, they can accommodate more patients, leading to increased revenue generation. Moreover, because APPs often bill at a lower rate than physicians, utilizing them efficiently can improve cost-effectiveness, thereby enhancing the overall financial performance of the practice.

“It should realize an ROI, and that ROI should be something more in terms of duties and tasks that other teammates can’t do,” says Mack. “Meaning, it would be unfortunate if an advanced practice professional is working at such a capacity whereby duties some of the day-to-day responsibilities should probably be done by teammates working at a higher level of their own individual license.”

Changing existing workflows can be difficult, but the rewards heavily outweigh the risks. Physicians must support APP integration to successfully navigate the transition. Physicians are typically the leaders and decision-makers within medical practices, and their support is essential for implementing any significant changes in workflow or care delivery models. Without physician buy-in, resistance to change may arise, hindering the smooth integration of APPs into the practice.

Physicians play a vital role in collaborating with APPs and delegating tasks effectively. By endorsing and supporting the integration of APPs, physicians can foster a culture of teamwork and mutual respect within the practice. This collaborative approach promotes a cohesive care team where APPs work alongside physicians to provide high-quality patient care.

It’s important for physicians to trust that their APPs are qualified and capable of providing excellent patient care. Allowing an APP to care for an established patient does not sever the relationship between the physician and the patient; it can actually enhance the patient’s experience and trust in the practice.

“We want patients who have had a long-standing relationship with an MD to be able to see that doctor, and then we want to help the doctor know and understand how to appropriately transfer care over to an APP within their system or within their practice,” says Monroe. “So, that provider can be still linked to the doctor, and the doctor can still be linked to the patient.”

Furthermore, physician buy-in is essential for maintaining continuity of care and ensuring patients feel confident in receiving treatment from both physicians and APPs. When physicians actively endorse the role of APPs and communicate the benefits of team-based care to their patients, it builds trust and acceptance of APP-provided services.

Physician engagement is critical for the long-term success and sustainability of APP integration initiatives. When physicians recognize the value that APPs bring to the practice, including increased efficiency, expanded access to care, and improved patient outcomes, they are more likely to champion these initiatives and advocate for their continued support and development.

The integration of APPs into physician practices and health systems presents a strategic opportunity to optimize patient care delivery and operational efficiency. By expanding access to healthcare services and alleviating the workload of overburdened physicians, APP integration improves patient and employee satisfaction, and enhances patient retention. However, successful integration requires careful attention to regulatory compliance, billing, and coding practices. VMG Health offers comprehensive billing, coding, and strategy advisory services to support practices in navigating the complexities of APP integration, ensuring compliance with Medicare regulations, and maximizing reimbursement while minimizing audit risk.

Optimal APP utilization yields tangible benefits, including increased patient access to care, improved patient satisfaction, and enhanced financial performance. By leveraging APPs’ unique skill sets, practices can accommodate more patients, reduce wait times, and deliver high-quality care cost-effectively. Physician engagement is essential for the successful implementation of APP integration initiatives, as physicians play a pivotal role in endorsing and supporting APPs within the care team. Through collaborative leadership and effective communication, physicians can foster a culture of teamwork and mutual respect, driving the long-term success and sustainability of APP integration efforts.

In summary, strategic APP integration presents a transformative opportunity for physician practices and health systems to meet evolving patient needs, enhance operational efficiency, and achieve sustainable growth. By partnering with VMG Health for expert guidance and support, practices can navigate the complexities of APP integration with confidence, realizing the full potential of this innovative care delivery model.

American Academy of Physician Assistants. (n.d.). History of AAPA. Retrieved from https://www.aapa.org/about/history/

American Medical Association. (2022). AMA president sounds alarm on national physician shortage. Retrieved from https://www.ama-assn.org/press-center/press-releases/ama-president-sounds-alarm-national-physician-shortage

Centers for Medicare & Medicaid Services. (2023). Advanced practice nonphysician practitioners. Medicare Physician Fee Schedule. https://www.cms.gov/medicare/payment/fee-schedules/physician-fee-schedule/advanced-practice-nonphysician-practitioners

Centers for Medicare & Medicaid Services. (2023). Advanced Practice Registered Nurses (APRNs) and Physician Assistants (PAs) in the Medicare Program. Retrieved from https://www.cms.gov/medicare/payment/fee-schedules/physician-fee-schedule/advanced-practice-nonphysician-practitioners

Centers for Medicare & Medicaid Services. (2023). Incident-to billing. Medicare. https://www.cms.gov/medicare/payment/fee-schedules/physician-fee-schedule/advanced-practice-nonphysician-practitioners

Mujica-Mota, M. A., Nguyen, L. H., & Stanley, K. (2017). The use of advance care planning in terminal cancer: A systematic review. Palliative & Supportive Care, 15(4), 495-513. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC5594520/

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

I spoke with King and Spalding attorney Kim Roeder on different, hot-button issues that arise when structuring and valuing different value-based arrangements. It started off as a presentation of different case studies and focused on what Roeder has encountered from a legal perspective and what I have encountered from a valuation perspective. We often receive questions when it comes to structure or even value drivers, and we wanted to present solutions to what we saw or clients struggling with so that they could develop a better understanding of them.

The focus on the metrics themselves and how carefully they need to be considered seemed to be the most surprising. Recent regulations have been really focused on metrics, and that’s what we get the most questions about. I think our audience was also surprised to learn that Kim had experienced those questions as well, and metrics aren’t just a consideration on the valuation perspective. Both legal and valuation perspectives must carefully consider metrics.

Our presentation was a very pragmatic way of illustrating six key issues that often come up during valuation. It’s a great resource for healthcare leaders to reference as they go through and check the boxes to ensure they have thought through all of the considerations that we often see as eleventh-hour issues.

I co-wrote a section of the 2023 Physician Alignment: Tips and Trends Report that discusses quality incentives for providers. It captures key factors to consider, from a valuation perspective, when looking to enter value-based arrangements and where to start.

Value-based arrangements require a very orchestrated balance between legal and compliance, operational champions, and valuation teams. Operational teams should be able to focus on what changes and improvements they want to implement, valuation teams must have an understanding of those goals, and legal and compliance must be involved to ensure the approach is appropriate and compliant. Without cohesion between these three groups, we see those eleventh-hour issues pop up.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.

Written by Cordell Mack, MPT, MBA

Hospitals and health systems have been developing strategies for vertical integration with physician groups for decades. Through the premise of integrated care delivery, “defined as a coherent set of methods and models on the funding, administrative, organizational, service delivery and clinical levels,” U.S. policymakers, healthcare operators and payors expect to improve the quality, service and efficiency of healthcare services. Results of value generated through integrated delivery models are mixed, and the operating model is often confounded with varying market dynamics (payor concentration, culture, physician supply/demand, leadership, etc.) by community.

Regardless of integrated care delivery success, health system employment continues to increase and today accounts for greater than 50% of all practicing physicians. Interestingly and unknown to many, other strategics (private equity, Optum, CVS, etc.) account for approximately another 25%, leaving approximately a quarter of physicians organized in a private practice.

Source: Physicians Advocacy Institute: Physician Practice Trends Specialty Report

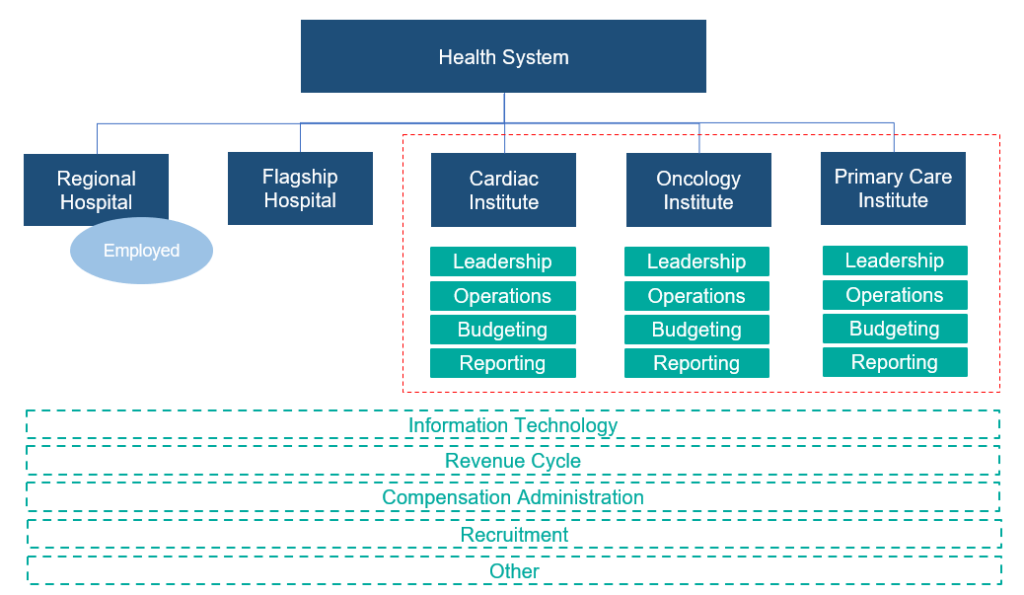

Across many integrated delivery systems, physicians are organized under a formal medical group structure, often with supporting leadership, governance, and practice management systems. This structure essentially groups the collective interests of primary care, surgical subspecialists, medical subspecialists, and hospital-based physicians together. Unlike independent, multispecialty practices who have an underpinning of sharing economics, most multispecialty groups in integrated delivery systems lack material financial alignment across subspecialties.

To this end, there are several challenges with a multispecialty group structure in health systems, including an aggregation of physician losses whereby various revenue streams (e.g., in-office ancillaries) have been integrated with hospital operations, sensitivity to practice losses based on confounding facts as to the true operating performance, silo board and/or decision making, and frustration by large clinical service lines due to widely held convention that everything needs to be the same for all physicians across the physician enterprise. Figure 2 outlines the most prevalent medical group structure and its multispecialty orientation.

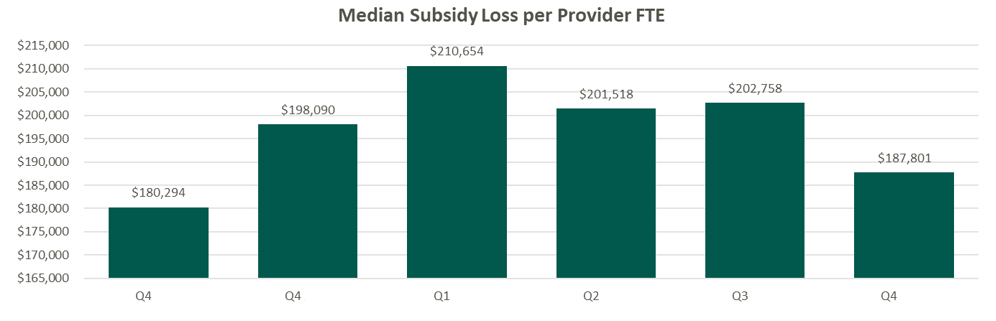

Financial system reporting remains inconsistent across organizations; however, there are data repositories that suggest continued median subsidies for employed providers. As figure 3 outlines, regardless of timing and/or subspecialty orientation, there remains a significant net investment per provider.

Source: Kaufman Hall Flash Reports

Based on VMG Health’s experience, significant financial reporting subsidies lead to suboptimized decision making, as significant pressure is placed on medical group leadership to reduce practice losses and improve overall practice performance. This has led to a variety of strategic missteps for organizations operating in competitive markets.

As an alternative, VMG Health has been working with clients to reorganize physician enterprise offerings inside of integrated delivery systems, including the development of financial reporting, management, and governance systems that better align care delivery across service lines. These more contemporary structures, while variable system to system, are all designed to:

The landscape of physician organizational structures within hospitals and health systems remains in transition. While traditional, multispecialty group practice models remain prevalent, challenges such as physician losses and inconsistent financial reporting have spurred the need for more contemporary structures. Through strategic reorganization and improved governance, health systems can enhance physician loyalty, accountability, growth, and operational efficiency, ultimately optimizing care delivery and aligned (or improved) financial performance.

Heeringa, J., et. al. (2020). Horizontal and Vertical Integration of Health Care Providers: A Framework for Understanding Various Provider Organizational Structures. National Library of Medicine. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC6978994/

Written by Clinton Flume, CVA, Cordell J. Mack, Tim Spadaro, CFA, CPA/ABV, Christopher Tracanna, Colin McDermott, CFA, CPA/ABV

The following article was published by VMG Health’s Physician Practice Affinity Group

Cardiovascular disease ranks as the leading cause of death in the United States, so it should come as no surprise that healthcare executives are placing an increasing emphasis on the stability and growth of cardiovascular services. In addition to the aging U.S. population, management is being forced to take strategic action due to industry factors such as shifting physician employment trends, patient procedures transitioning to lower-cost outpatient care settings, and payor models changing from fee-for-service to value-based care. To ensure continuity of alignment for cardiology providers and stakeholders, executives need to consider the strategic impact of cardiovascular medical group affiliations in their decisions. These decisions include investment in comprehensive cardiac care services, external affiliation models (joint ventures or joint operating agreements), and alignment models with private equity.

According to the Physician Advocacy Institute, as of January 2022 approximately 67.3% of cardiologists were employed by hospitals or health systems, 17.9% were employed by other corporate entities, and the remaining 14.8% were in independent practices. The combined hospital/health system and corporate entity employment (85.2%) was 12.2% higher than the number of cardiologists (73.0%) employed by these entities in January 2019 [1]. Due to the high concentration of employment for cardiology, this specialty has been insulated from the traditional roll-up activity seen in the orthopedic, gastroenterology, and ophthalmology spaces. This suggests the industry is primed for a reversal of employment back to private practice as providers look for ways to diversify from legacy employment models and engage in outside investment opportunities, such as private practices and surgical centers.

Health systems, payors, providers, and, most importantly, patients are increasingly seeking high-quality and lower-cost options for routine cardiovascular care. Outpatient cardiology services began to see a transition to the outpatient setting in 2016 when the Centers for Medicare and Medicaid Services (CMS) approved pacemaker implants for the ambulatory surgery center (ASC) covered procedure list (CPL) [2]. In the 2019 Final Rule, CMS added 17 cardiac catheterization procedures to the ASC CPL, and in the 2020 Final Rule, CMS allowed physicians to begin performing six additional minimally invasive procedures (percutaneous coronary interventions) in ASCs. Additionally, several states have followed CMS’ lead by removing barriers to accessing cardiovascular care in ASCs [3]. The continued approval of procedures to the CPL and expanded access to care are major catalysts for the shift in cardiology services to the outpatient setting and the desire of providers to engage in external clinical investment opportunities.

Cardiologists have long sought refuge from rising costs and downward reimbursement pressure by aligning with larger entities that have more leverage and pricing power. This often materialized through traditional health system employment with many hospital providers looking to operate traditional in-office ancillaries in an adjunct hospital outpatient department. The arbitrage in reimbursement (HOPD versus freestanding) was an offset to the ever-increasing physician compensation inflation. However, challenges continue to mount.

The Medicare Physician Fee Schedule (MPFS) conversion factor has fallen year-over-year since CY 2020. On November 1, 2022, CMS released the 2023 MPFS which continued to lower the conversion factor and resulted in cardiology reimbursement falling an estimated 1.0% [4]. During the same period, many health systems are reporting larger net professional losses per cardiologist as costs continue to rise faster than revenue.

These factors, coupled with bundled pricing initiatives and trends focused on value-based care initiatives, are compelling cardiologists to consider all alternative employment scenarios in response to slowing compensation growth. Whether cardiologists continue to be employed by health systems and corporate entities or they venture into private settings to explore outside investment opportunities, there is no doubt cardiology will continue to face financial pressure from rising operating costs in tandem with reimbursement cuts.

Cardiology employment trends, increasing access to outpatient cardiology services, and changes in payor models are all leading indicators that impact the strategic alignment of cardiology medical groups. The following are key external and internal drivers that serve as signals of the fragmentation of the cardiology market. Healthcare executives should be proactive in their evaluation of these market factors which can dictate how cardiology coverage is delivered and can impact current and future affiliations.

Physician Alignment

Degree to which cardiology services are provided by independent cardiologists, employed providers, or a group professional services agreement.

High Impact – To determine the top-line revenue impact between two parties’ contracts.

Entrepreneurial Leadership

The presence of forward-thinking medical leadership.

High Impact – Visionary leadership required to change the market status quo, and generally visionary leaders see today’s disruption (rate pressure, ambulatory migration, etc.) as opportunity.

Economic Sustainability

Degree to which current employed or contracted cardiology economics remains financially viable.

High Impact – Health system alignment can result in inflated market compensation and greater economic burdens for healthcare organizations. The higher the degree of financial unsustainability, the higher the likelihood of stakeholders (health systems, payors, and providers) are open to alternative structures.

Physician Contracts

Degree to which physicians are subject to a noncompete or other similar provisions.

Medium Impact – This may delay fragmentation, but ultimately a large cadre of cardiologists seeking an alternative care model will likely prevail.

Payor Fragmentation

Depth of managed care and commercial contract consolidation.

Medium Impact – The more consolidated the managed care community is in a market, the stronger the likelihood of evolving lower total-cost care models.

Upon evaluation of the internal and external environment, health systems have strategic options that range from staying the course with minimal change through employment to proactively migrating the cardiology care delivery model in partnership with a private equity-backed platform. Below are strategic opportunities for organizations to consider when developing long-term cardiovascular medical group affiliations.

As healthcare executives evaluate the overall strategic positioning of cardiovascular services, industry factors such as physician employment trends, a shift to lower-cost outpatient care, and changing payor models will continue to change the cardiovascular landscape. Mindful executives with a strong pulse on external and internal factors, such as physician alignment and service line stability, will have an advantage in tactical decision-making. Position opportunities, such as investment in comprehensive cardiac institutes, joint ventures with MSOs, and partnerships with private equity firms, are all potential models for long-term strategic success.

By: Madi Whyde, Savanna Ganyard, CFA, Jordan Tussy, and Madison Higgins

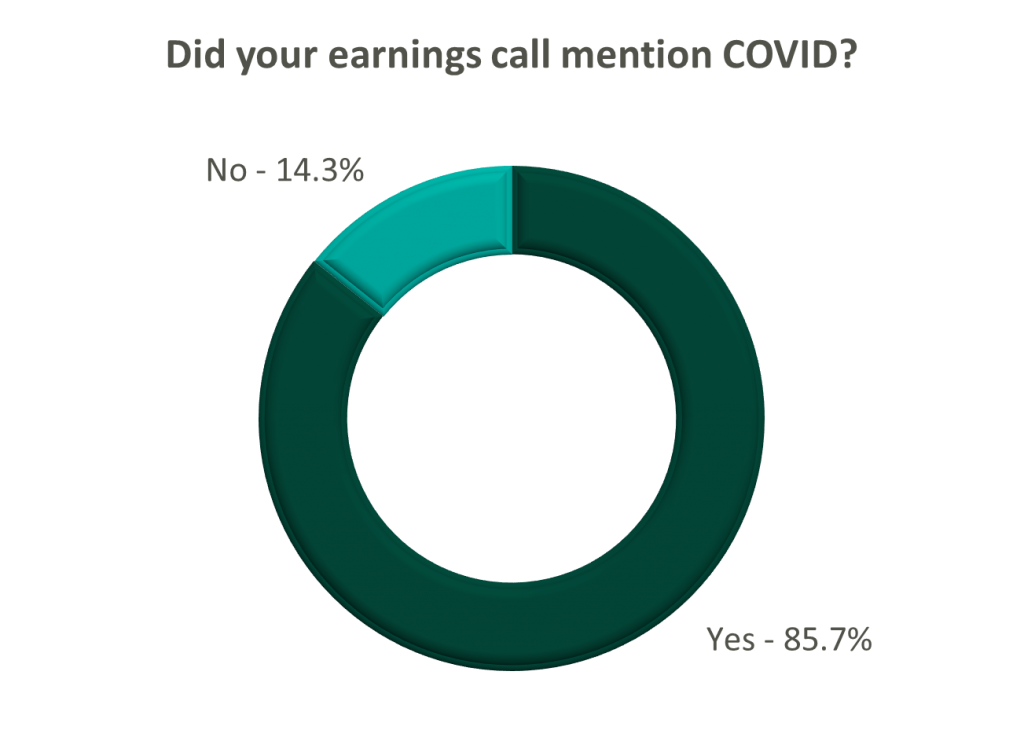

VMG Health reviewed the earnings calls of publicly traded healthcare operators that reported earnings for the third quarter that ended on September 30, 2022. By focusing on the major players in select subsectors defined below, we analyzed the frequency of certain keywords including inflation, COVID-19, interest rates, premium labor, and others. We used these keywords to identify which topics commanded the room this earnings season. Highlights from the calls are summarized in this article.

Volume: Although volume trends are unique to each industry sector nearly all operators remained focused on the impacts of COVID.

Poll: Did the earnings call mention COVID-19?

On a same-facility basis, admission volumes declined as much as 5.0% from the comparable prior year quarter (Q3 2021) for acute care hospital operators. Despite the weakening of COVID-19, the decline in volumes was attributed to higher-than-average cancellation rates (THC), the migration of certain procedures to outpatient status (CYH and HCA), and capacity constraints (HCA). Inpatient volumes generally remained at or below pre-pandemic levels.

Ambulatory surgery center (ASC) operators reaped the benefits of the migration to the outpatient setting and reported positive volume trends when compared to Q3 2021. Surgical volumes were reported as consistent with 2019 pre-pandemic levels (THC), and one operator claimed the business did not experience any material direct impact related to COVID-19 during Q3 2022 (SGRY).

The post-acute sector reported mixed results in volume trends. One operator reported a year-over-year decline of 14.0% in hospice admissions, citing capacity constraints and reduced referrals from acute care hospitals (EHAB). However, another operator indicated that increases in admissions in the second half of the third quarter showed growth that they “haven’t experienced since the start of the pandemic” (CHE).

Volume trends among other industry players including dialysis providers, risk-bearing organizations, and physician services were also affected by COVID-19 in Q3 2022. Headwinds in dialysis volumes are expected to persist for the foreseeable future (DVA), and inpatient volumes for risk-bearing organizations remain below pre-pandemic levels (AGL). Notably, AGL also reported a rebound in physician office visits and outpatient volumes were in line with pre-pandemic levels.

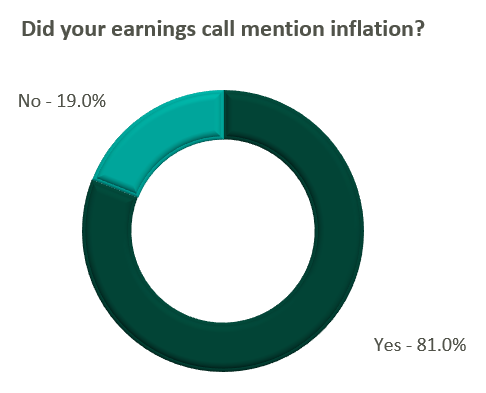

Reimbursement: Declining COVID-19 volumes mean less incremental government revenue for certain industry players who also now contend with an uncertain inflationary environment.

Poll: Did the earnings call mention inflation?

Declining COVID-19 volumes resulted in lower acuity patients and reduced incremental government reimbursement. This softened the reimbursement per admission for the acute care hospital segment. Further exacerbated by inflation, these dynamics were evident in reported EBITDA margins which declined as much as 17.0% (CYH) over Q3 2021. In response, some acute care hospital operators are turning to commercial payor negotiations. Rate increases for the next year are anticipated to range from a minimum of 3.0% (THC) to upwards of 6.0% (CYH).

The post-acute sector did not release specific figures regarding contract rate hikes. However, the sector is optimistically looking for high single-digit rate increases (SEM) to provide relief in the current inflationary environment.

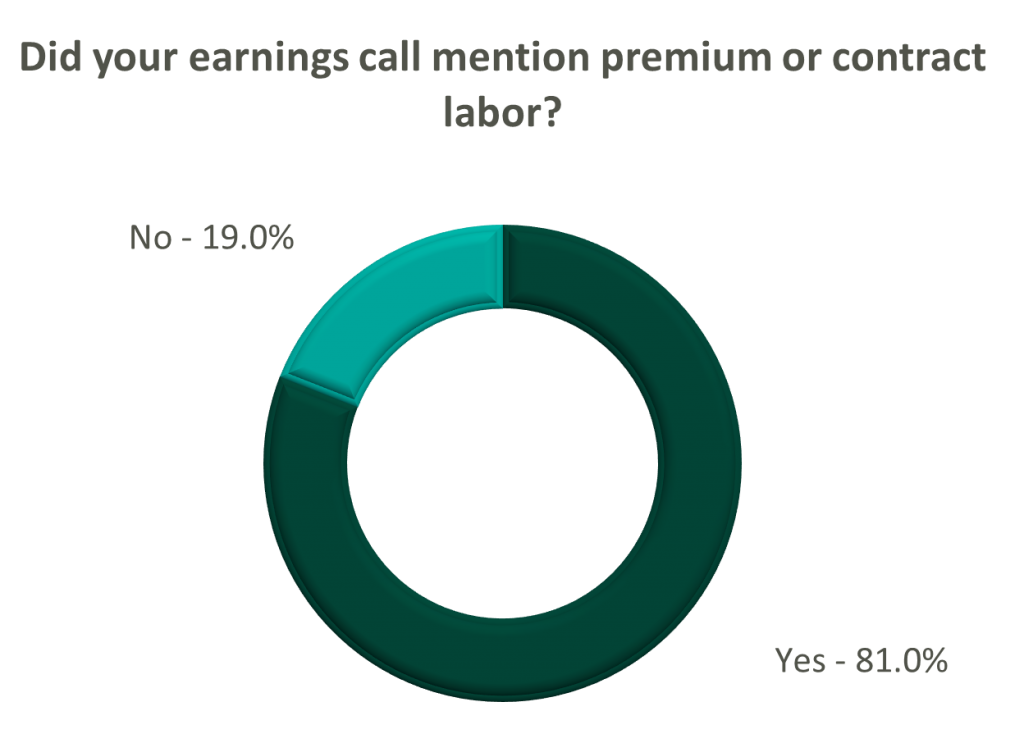

Labor: Unsurprisingly, management teams across the sector were faced with questions about labor trends and management techniques during their earnings calls. Contract labor remained pivotal for the operations of some, but premium labor appears to have softened during the quarter.

Poll: Did the earnings call mention premium or contract labor?

The reliance on contract labor continued its downward trend in Q3 helping moderate expenses. HCA even indicated overall labor costs were stable due to targeted market adjustments. However, contract labor and premium pay remain at uncomfortably high levels for most acute care hospital operators. UHS revealed during their call it will be unlikely to reach pre-pandemic levels in the near future.

Staffing challenges persisted among the post-acute operators and directly impacted volume by as much as 60.0% (AMED). Increased indirect labor costs including orientation, training, and sign-on bonuses were the leading drivers of decreased EBITDA (AMED). Wage inflation, particularly for nursing positions, is expected to rise as much as 5.0% next year (SEM). However, several management teams are optimistic wages will stabilize to historical levels (SEM, EHC) in the near future.

Other industry players, including dialysis and physical therapy providers, also faced challenges with contract labor during the quarter. USPH reported labor costs were approximately 200 basis points higher than Q3 2021 levels, and DVA indicated such costs showed no improvement.

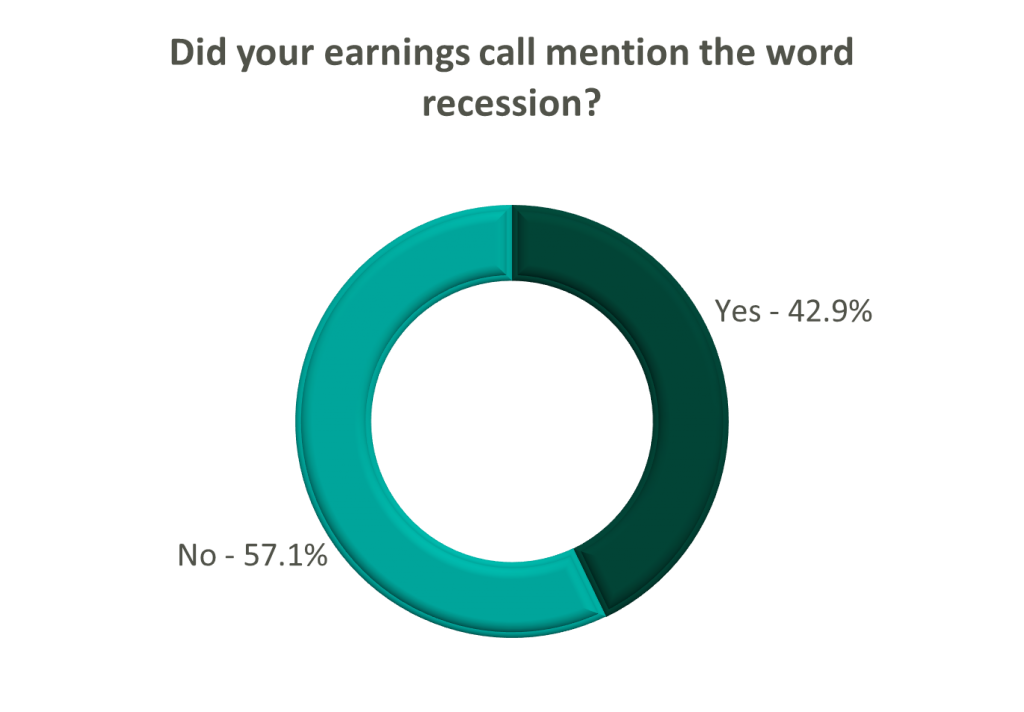

Go Forward Expectations and Guidance: Considering the quarter’s performance, the companies we reviewed were divided relatively evenly in terms of revised FY 2022 revenue guidance, (i.e., raised, lowered, unchanged). In general, the quarter brought about a more pessimistic view of FY 2022 EBITDA, and the majority of public companies lowered their guidance for the year. Further, most stakeholders were left with no guidance for FY 2023.

Poll: Did the earnings call mention a recession?

FY 2022 revenue and EBITDA guidance among the acute care hospital operators was generally left unchanged except for THC which lowered EBITDA guidance. However, all companies that were reviewed declined to provide FY 2023 guidance during the call, and primarily cited economic uncertainty (HCA).

The post-acute sector appeared nearly unanimous in the outlook for the rest of 2022, and most operators lowered their revenue and EBITDA guidance. Unsurprisingly, no one offered FY 2023 guidance during the earnings calls.

Interestingly, risk-bearing organizations mostly raised their revenue guidance for FY 2022 (AGL, CMAX, PRVA). However, EBITDA guidance was less predictable and was lowered (AGL, TOI), raised (PRVA), and unchanged (CMAX).

Most other healthcare operators followed similar patterns in terms of providing guidance for FY 2023. Of the companies we reviewed, only DVA revealed an outlook for the next year. The company anticipates revenue to be flat (driven by unfavorable volume trends) and margins to continue to feel the impact of labor market pressures.

By: Anthony Domanico, CVA and Nicole Montanaro

The following article was published by the American Association of Provider Compensation Professionals

While the healthcare industry has been moving from volume to value for the last two decades, the movement toward true value-based care has really taken off within the last few years. This is because the way health systems are paid has been largely based on fee-for-service payments with a relatively small share of a health system’s revenue being driven through “value.”

The 2022 MGMA Practice Operations Survey found that health systems see approximately $31,000 in value-based revenue per FTE physician [1]. While that figure is just a small portion of what organizations bring in for the typical physician, the expectation among leaders in the healthcare provider and the payor industries is this trend of shifting revenue away from fee-for service and towards value-based care is going to grow significantly over the next several years. As the way organizations are reimbursed moves towards quality and other non-productivity-based metrics, how those organizations pay their physicians needs to evolve in similar ways. Many organizations we work with at VMG Health are engaging our firm in the following ways:

The remainder of this article will focus on common ways organizations are implementing value into their physician compensation plans. It will also include guidance to organizations on how to select meaningful value-based metrics to provide the most value to the organization.

For those organizations just starting on this journey from volume to value, the most important decision is how to start including quality in plans that have previously paid physicians solely based on the volume of their work. Organizations often start by adding a modest amount of compensation tied to value, and typically it is an amount that guarantees a physician’s base salary or rate per wRVU does not need to decrease to make room for the quality incentive while staying within budgetary expectations.

For example, a productivity model at $55 per wRVU with an expected 2.5% budget increase in 2023 might leave the conversion factor at $55 and add a 2.5% quality incentive as a bonus. Over time, that percentage tied to quality can increase as physicians become more familiar with and trusting of value-based metric reports as they are with wRVU reports. However, this process generally starts small and typically tops out somewhere in the 10-20% range for organizations on the value-based side of the volume-to-value continuum.

Once the magnitude of compensation is determined, there are a few main ways organizations typically structure value-based incentives in their physician compensation plans. These structures are typically based on how the organization’s leadership team answers the following question:

Question: “Should quality be the same for everyone, or should there be some variability for factors like productivity, tenure, base salary differences, or other factors?”

These organizations typically pay all physicians the same flat dollar amount, regardless of physician subspecialty area. As an example, every physician, whether a neurosurgeon or a family practitioner, would have the same $20,000 quality opportunity.

These organizations typically use a percent of market (usually median) approach that pays everyone within the same specialty the same total dollars for quality. As an example, every family medicine doctor would receive up to $13,500 (~5% of median), and every neurosurgeon would receive $37,500 (~5% of median).

These organizations typically use a percentage of-base salary approach where the base salary is set according to organizational policies. This might provide a differentiated level of base compensation for factors like tenure, experience, productivity level, or other factors, and each physician can receive 5% of their individualized base salary as a quality bonus. As an example, Family Medicine Physician A with a $230,000 base salary is eligible for an incentive of up to $11,500, and Family Medicine Physician B with a $250,000 base salary can earn up to $12,500.

These organizations typically use either a quality rate per wRVU or a percentage of total production-based comp approach. Under a pure productivity-based plan, if the compensation plan targets a compensation per wRVU rate of $50 then$47.50 per wRVU might be earmarked for wRVU productivity, and an additional $2.50 per wRVU is set aside, and paid based on quality performance. This type of incentive provides different (and sometimes significantly different) quality incentive opportunities for physicians with different levels of productivity.

Regardless of which of these quality compensation structures is selected, when considering supporting quality bonus payments to physicians a key factor is having a substantive set of quality metrics.

VMG Health collected industry research and identified multiple healthcare articles, publications, and other sources related to quality bonuses paid to physicians. The takeaways about value driver considerations related to the metrics are summarized below. While this list is not exhaustive, it does provide the most common and important factors that support quality bonus payments to physicians.

Generally, factors such as paying for the achievement of “superior” performance standards and selecting patient clinical quality metrics demonstrably impacted by the subject physician(s) help to justify higher-quality bonus payments.

Further, the following chart outlines some best practices to consider for identifying and selecting meaningful metrics, as well as factors to consider before including value-based incentives in a compensation model.

It is important to note the considerations described herein are most pertinent when a party wishes to fund its own value-based compensation program. Alternatively, and subject to certain facts and circumstances, if the funding for a value-based compensation program were to be tied to incremental quality or savings payments from a governmental or commercial payor, other factors may be relevant to consider. Some examples of factors are the incremental revenue/actual savings generated, and the risk and responsibility of the parties.

Organizations that are already far along on the value-based care continuum with a robust quality department/program are starting to expand beyond the quality incentive programs outlined above. These groups are starting to include patient access or acuity-adjusted panel size factors to further focus their compensation plans on population health management. Patient access can include incentives for things like open panels, time to third-next-available appointments, or other factors that get layered on top of productivity and quality compensation.

Acuity-adjusted panel size is an alternative productivity metric to wRVUs that attempts to measure how large a panel of patients a particular physician is charged with caring for. Raw panels (actual number of patients) are adjusted for some level of patient acuity factor – an age and sex adjustment factor, hierarchical condition categories (HCCs), or a multitude of other factors to ensure panel comparability. Unfortunately, there is no perfect acuity-adjustment factor, which makes comparing panel sizes to the external market a unique challenge.

Finally, some organizations are using incentives embedded in payor contracts – quality incentives, shared savings, and other payments – as additional incentives in the provider compensation formula. Typically, organizations take some percentage of dollars received from payors to cover costs incurred by the system and to provide some level of additional remuneration to physicians.

As these value-based programs continue to evolve, organizations have many levers to provide competitive levels of compensation to their physicians. These options help move physicians’ focus from being solely on production to providing high-quality care to patients and reducing unnecessary procedures.

With this complexity, however, organizations must be more diligent than ever to ensure their provider compensation programs continue to align with federal fraud and abuse laws. These regulations are also changing and providing additional levels of protection to organizations that ask physicians to take on meaningful downside risk in their compensation plans. Therefore, careful consideration should be taken in establishing a compensation strategy to ensure the compensation levels remain both competitive and compliant.

Written by Clinton Flume, CVA, Tim Spadaro, CFA, CPA/ABV, Olivia Chambers, and Blake Toppins

The following article was published by Becker’s Hospital Review.

The physician medical group sector remains a hot transaction space that outperforms expectations each quarter. This sector’s strong prospects are driven by interest from private equity groups, health systems, and value-based care organizations. However, before buyers operate in this robust sector, they must consider the unique transaction intricacies of such deals, including physician alignment, compensation structure, and due diligence considerations.

For more in-depth insight on this sector, refer to VMG Health’s 2022 Healthcare M&A Report which describes the nature of this sector and summarizes the robust transaction environment experienced in 2021. This report also projected the ongoing elevated deal activity in 2022 which has been confirmed by the 170 deals in Q3 2022 alone (representing a 63.0% increase over Q3 2021).1

Below are three key considerations when executing a physician medical group deal.

Effective medical group alignment strategies are imperative to a healthcare organization’s growth, and the two most common strategies are direct employment and equity investment. The latter can be accomplished through joint ventures or investment in a management service organization (MSO). MSOs are an increasingly popular alignment strategy in states that adopt the corporate practice of medicine (CPOM) doctrine. For more information on MSOs and how they work, read “Physician Practice Strategy: The Private Equity Play.”

According to the Physician Advocacy Institute, 74% of physicians are employed by hospitals or corporate healthcare entities (a 19% increase since 2019).2 The main drivers of this trend include physicians’ financial security, physicians’ professional and work-life balance, the payor environment’s evolution from fee-for-service to value-based care, and the administrative complexities of running a business. In many instances, a direct employment model enables physicians to receive market compensation consistent with their productivity and to focus more closely on clinical initiatives which alleviates their day-to-day administrative responsibilities. From a buyer’s perspective, direct employment models mitigate the risks associated with provider contractual arrangements and enable more definitive long-term planning.

Joint venture structures with physicians may also constitute an attractive proposition for alignment. A joint venture opportunity may take the form of an equity investment in a medical practice (state specific based on CPOM) or in a physician-aligned business, such as an ambulatory surgery center or retail healthcare business. Joint venture affiliations can strengthen physician alignment through synergies such as reimbursement lifts, growth capital, and economies of scale. Along with governance rights, each of these elements plays a key role in defining post-transaction equity alignment structures.

Due to the regulated healthcare industry and strict guidance around physician transactions needing to be consistent with Fair Market Value, it is important that both the business being valued and the compensation offered is documented to be Fair Market Value. Further, there are a myriad of structural nuances that should be considered from a legal, operational, and clinical perspective. As a result, leaning on experts focused on the physician practice sector is highly recommended.

Compensation can be the single most important negotiation item in a medical group transaction. As private equity, insurance companies, and for-profit management organizations enter the sector, compensation models demand careful attention to ensure a good alignment of physician productivity, physician pay, and medical group returns.

External alignment allows providers to benefit from direct investment when shifting to an employment model. Although complex, it has increasingly become the norm for compensation models to factor a physician’s external interests into an agreement.

Compensation arrangements continue to require ongoing innovation to stay competitive and relevant. As transaction activity intensifies and healthcare shifts from a volume-based system of care to a value-based system of care, compensation arrangements must be designed to evolve with the dynamic intricacies of the industry. Understanding the latest compensation models, and how to design those models and a transition plan, has proven to be a critical factor for success with physician practice strategy. For recent insight on design, further information can be found here.

The competitive environment for medical group assets has intensified as capital continues to flow into the sector. As part of the deal process, performing both pre- and post-acquisition due diligence is now the standard for high-value deals. Due diligence focuses on the following areas: