Fair Market Value Considerations for Your Recruiting and Leased Staff Agreements

Rachel Linch

October 18, 2023

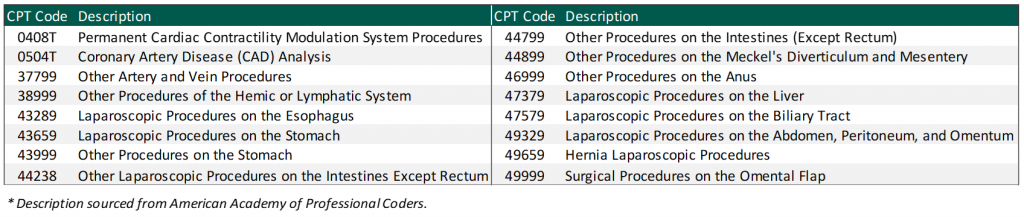

Physician compensation continues to have new areas to tackle, from payments for quality to excess call to shared savings. In addition, VMG Health has recently seen an increase in unlisted procedures and inquiries from organizations on how to appropriately compensate physicians for their services. It is important to note that while unlisted procedures may still be reimbursable by a payor(s), they do not yet have a corresponding work relative value unit (WRVU) assigned by CMS and the American Medical Association (AMA).

This raises the question from health systems: what is an appropriate methodology to account for unlisted services when determining physician compensation if the physician is paid based on a WRVU productivity model and/or a base salary with a WRVU-based bonus model?

Due to the complexity of the CMS Medicare Physician Fee Schedule (MPFS) and the magnitude of codes listed, CMS and the AMA do not rebase WRVUs for each CPT code each year. As a result, advances in medical technology and the development of new, innovative procedures lead to services being provided to patients who are unlisted on the MPFS. VMG Health has observed a sizeable uptick in unlisted services including, but not limited to, implants, imaging, surgical, and laparoscopic services.

When determining physician compensation for unlisted services, health systems should ensure the proposed payment is consistent with fair market value (FMV). In addition, contractual terms should be considered to prevent the potential for duplicate payments. One approach VMG Health has frequently observed in the marketplace is compensating the physician based on a percentage of revenue received for the unlisted service. A few important factors to consider:

Another approach when compensating a physician for unlisted procedures is a comparative code method and utilizing the WRVU associated with the comparative code. However, it can be difficult to confirm an accurate comparative code for certain procedures. This could understate or overstate the WRVU associated with the unlisted service. There are several factors to consider when selecting a comparison code such as:

As more new technology is introduced to the healthcare market, determining physician compensation for unlisted procedures will continue to be a topic of discussion for health systems. Before paying physicians for unlisted services, health systems should ensure that the compensation arrangements are commercially reasonable and do not result in compensation that exceeds FMV.

Written by Grant White, CPA, Colin Haslett, and Joe Scott, CPA

In the healthcare industry, investors evaluate potential investment opportunities that typically first come through sell-side marketing materials like teasers or confidential information memorandums (CIMs). These materials show the company’s financial performance over the past two years and projections for the current and next two to three years. It’s crucial to note that these projections naturally involve assumptions about future growth.

While these assumptions help buyers grasp the company’s strategic direction and growth opportunities, relying solely on them might lead to overestimations in purchase prices or underperformance post-acquisition. Financial projections have the potential to be biased and overly optimistic by overlooking potential market shifts or industry trends that may impact performance.

For instance, in the healthcare services industry, projected financial performance might hinge on key events such as:

Prudent investors recognize the importance of buy-side due diligence. This diligence serves not just to verify historical data, but also to test the credibility of projected financial assumptions. Diligence teams must reconcile key documents, analyze historical financial and operational trends, and engage in candid conversations with key management personnel to evaluate these assumptions.

To illustrate this point, consider two scenarios wherein a company projects $1 million in revenue from hiring a new provider in its CIM distributed to potential investors:

In summary, buy-side diligence is instrumental in verifying management’s claims and assessing the feasibility of a company’s projections. The insights gained through the diligence process help buyers make informed investment decisions, guard against inflated purchase prices, and provide buyers with more accurate expectations of post-close performance.

By Taylor Anderson, CVA, Taylor Harville, and Trent Fritzsche

The Department of Health and Human Services Office of Inspector General (OIG) posted Advisory Opinion No. 23-07 on October 13, 2023 (“Opinion”). The Opinion was related to the request submitted by a redacted requestor (“Requestor”) to pay bonuses to its employed physicians based on net profits derived from certain procedures performed by the physicians at ambulatory surgery centers (ASCs) operated by the Requestor (“Proposed Arrangement”). More precisely, the Requestor was seeking the opinion of the OIG about whether the Proposed Arrangement would lead to sanctions under the federal Anti-Kickback Statute (AKS).

Based on the relevant facts detailed in the Opinion, the Proposed Arrangement consisted of the following key facts and circumstances:

Ultimately, the OIG concluded the quarterly bonus structure would not generate prohibited remuneration under the federal AKS.

In the analysis summarized in the Opinion, the OIG highlighted several considerations that ultimately led to the conclusion. These included the following:

The OIG also noted that a compensation structure tied to profits generated from services provided to patients referred by the compensated party is suspect under the federal AKS, particularly in arrangements where the physician is an independent contractor or there is a different corporate structure. However, because the Proposed Arrangement satisfied the regulatory safe harbor for employees, the compensation would not be prohibited.

Lastly, the OIG noted that while the Proposed Arrangement would not generate prohibited remuneration under the federal AKS, it was clear that it expressed no opinion as to whether the Proposed Arrangement would implicate the physician self-referral law.

When developing unique compensation structures with physicians or any service provider it is important to be mindful of the various laws and statutes in place. Proper review and consideration of the federal AKS and other healthcare regulations is essential for any organization when structuring compensation plans to ensure proper regulatory compliance. Additionally, documentation of fair market value and commercial reasonableness is another key element of any provider compensation arrangement, especially if those providers are a source of potential referrals.

For additional guidance related to structuring and valuing provider compensation arrangements, please reach out to Managing Director Jonathan Helm at jonathan.helm@vmghealth.com to learn more.

*The Opinion noted there were two ASCs operating as corporate divisions of Requestor.

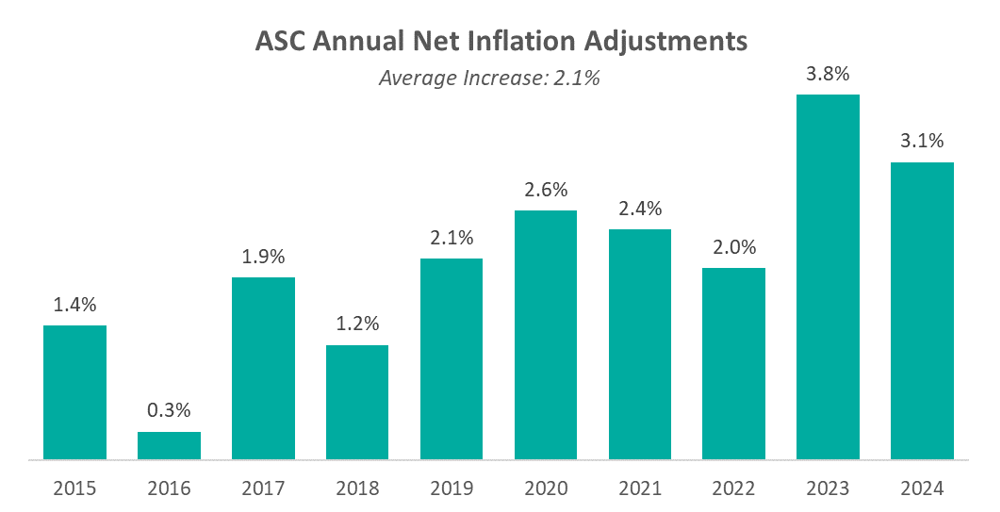

On November 2, 2023, the Centers for Medicare & Medicaid Services (CMS) released the CY 2024 Hospital Outpatient Prospective Payment System (OPPS) and Ambulatory Surgery Center (ASC) payment system policy changes and payment rates final rule. Based on the final ruling, CMS finalized its proposal to continue to align the ASC payment system by using the hospital market basket update, rather than the Consumer Price Index for All Urban Consumers (CPI-U) for an additional two calendar years through 2025. The final rule resulted in overall expected growth in payments equal to 3.1% in CY 2024. This increase was determined based on a projected inflation rate of 3.3% less the multifactor productivity (MFP) reduction of 0.2% mandated by the ACA. This is an increase of 0.3% from the proposed rule. In an official AHA statement on the CY 2024 OPPS final rule Executive Vice President of AHA Stacey Hughes said:

Presented in the chart below is a summary of the historical net inflation adjustments for CY 2015 through CY 2024. The annual inflation adjustments are presented net of additional adjustments, such as the MFP reduction, outlined in the final rule for the respective CY. The CY 2024 inflation adjustment is slightly lower than the increase observed last year, although it continues to be elevated compared to the adjustments observed prior to 2023 largely driven by labor and supply cost pressures.

CMS noted in its fact sheet that “in addition to finalizing payment rates, this year’s rule includes policies that align with several key goals of the Biden-Harris Administration, including promoting health equity, expanding access to behavioral health care, improving transparency in the health system, and promoting safe, effective, and patient-centered care. The final rule advances the Agency’s commitment to strengthening Medicare. It uses the lessons learned from the COVID-19 PHE to inform the approach to quality measurement, focusing on changes that will help address health inequities.”

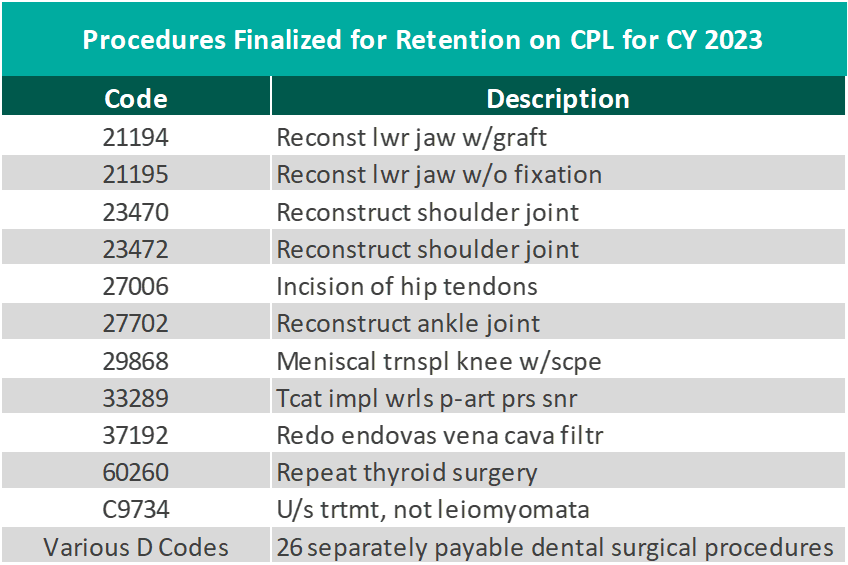

CMS finalized the addition of 37 surgical procedures to be added to the ASC CPL for CY 2024, outlined in the table below. These include 26 dental codes that were included in the proposed rule, and 11 surgical codes that were not included in the proposed rule -most notably total shoulder arthroplasty. These codes correspond to procedures that have little to no inpatient admissions and are widely performed in outpatient settings.

CMS has projected total ASC payments in 2024 will increase from approximately $207 million in 2023 payments to approximately $7.1 billion. The source of this increase in payments is a combination of enrollment, case mix, and utilization changes.

In conclusion, the trend of rising labor and supply costs continues to play out through 2023 and into the finalization of the CY 2024 payment system. CMS continues to show stability on the annual inflation adjustment by utilizing the hospital market basket to update rates and extending the five-year interim period. However, as Hughes has said, the costs of providing care continue to rise rapidly which directly impacts health systems’ margins and ability to provide effective care. CMS finalized the addition of 37 procedures to the ASC CPL for CY 2024, which is a substantial increase from the addition of only four codes in 2023. These additions have created positive feedback from outpatient providers due to the ability to continue to perform additional procedures in the ASC setting safely and successfully.

On November 2, 2023, the Centers for Medicare & Medicaid Services (CMS) unveiled a significant final rule marking the latest step in the administration’s comprehensive effort to create a more equitable, accessible healthcare system. The rule introduced policy changes that will impact Medicare payments under the Physician Fee Schedule (PFS), effective from January 1, 2024. Here are some key highlights and takeaways:

In CY 2024, CMS will enact a 1.25% reduction in overall payment rates under the PFS compared to CY 2023. However, this will be accompanied by substantial increases in payment for primary care and direct patient care. The final CY 2024 PFS conversion factor is set at $32.74 which represents a 3.4% decrease from the 2023 conversion factor of $33.89.

CMS is introducing a separate add-on payment for HCPCS code G2211, effective from January 1, 2024. This add-on code will recognize the resource costs associated with primary care and longitudinal care during evaluation and management visits. Use of the G2211 code will likely increase total wRVU volumes by 5-10% for many E/M-heavy specialties.

For CY 2024, CMS is revising the definition of a “substantive portion” of a split (or shared) visit. The substantive portion will be defined as either more than half of the total time spent by the physician or non-physician practitioner during the visit or a significant part of the medical decision-making process. This change is in response to public feedback, and it aims to provide more flexibility in billing for split (or shared) E/M visits. Previous indications from CMS did not include medical decision-making in the criteria for “substantive portion,” which would have had a considerably higher impact on provider wRVU volumes in inpatient settings.

CMS is expanding telehealth services under the PFS for CY 2024. This includes the expansion of telehealth originating sites to include patients’ homes, the inclusion of additional healthcare practitioners in the definition of telehealth practitioners, and the continuation of payment for telehealth services furnished by RHCs and FQHCs. The rule will also postpone the requirement for in-person visits before initiating mental health telehealth services.

In CY 2024, telehealth services furnished in patients’ homes will be paid at the non-facility PFS rate to ensure continued access to these essential services. The definition of direct supervision for telehealth will remain in place through December 31, 2024.

VMG Health’s experts can assist organizations by assessing the new Medicare Physician Fee Schedule changes including how it will impact physician compensation spend. For more insight on physician compensation strategies and alignment, download the 2023 Physician Alignment: Tips & Trends Report.

Written by Tyler Perper and Matthew Marconcini, CPA

The following article was published by Becker’s Hospital Review.

The landscape of healthcare is continually evolving, with a growing emphasis on providing better outcomes for patients while controlling costs. Value-based care (VBC) is a departure from the traditional fee-for-service (FFS) model and is transforming healthcare delivery into a capitated model that balances the total cost of care with the quality of patient outcomes. Investment within VBC or alternate payment models (APMs) quadrupled from 2019 to 2021, while investment in legacy-care delivery models has remained relatively flat. Additionally, the estimated number of Medicare enrollees participating in Medicare Advantage (MA) plans is expected to increase by more than 24% in 2023 compared to the 2022 MA enrollment growth. The explanation for the significant VBC investment and the growth in VBC players is primarily driven by the acknowledgment amongst U.S. policymakers, providers, and payers that VBC offers a sustainable model of care for patient populations across the country, as well as the opportunities presented by new technology and tech-enabled services that facilitate VBC for both providers and payers.

VBC is a payment model that incentivizes healthcare providers to focus on delivering high-quality care while containing the costs. Unlike the FFS payment model, in which providers are reimbursed based on the number of services they render, the APM model encourages providers to prioritize the patient’s health and well-being by promoting preventive measures, care coordination, and better health outcomes. In addition, as providers transition to value-based care their reimbursement model aligns more closely with that of payers. This shift requires providers to gain a fundamental understanding of the expertise needed for managing risk, similar to payers.

Managing risk and risk sharing in healthcare refers to the practice of distributing and managing the financial risks associated with healthcare services among different stakeholders, such as insurers, healthcare providers, and sometimes patients. It involves mechanisms and arrangements designed to ensure the financial burden and responsibility for healthcare costs are shared rather than being shouldered entirely by one party. The goal is to promote cost efficiency and improve healthcare quality.

Transitioning to VBC reimbursement models presents providers with a spectrum of options. At the outset, pay-for-performance models link claims reimbursement to quality and value. This means that providers are reimbursed using a fee-for-service structure while qualifying for value-based incentives or penalties based on quality and cost performance. Such models are particularly favorable for smaller practices lacking extensive health IT and data analytics infrastructure.

Moving further along the spectrum, shared savings arrangements offer higher financial rewards and allow providers to retain a portion of the savings if they reduce healthcare spending below established benchmarks. Shared risk models, where providers must cover healthcare costs exceeding benchmarks, foster greater accountability, especially within accountable care organizations.

Finally, capitation payments place full financial risk on providers and offer either global capitation with a fixed payment for all services or partial capitation covering specific services with all other care reimbursed through fee-for-service. While capitation models provide prepaid reimbursements and an incentive for innovation, they present challenges related to quality measures and data sharing. Overall, this spectrum allows providers to select the most suitable value-based reimbursement structure to enhance revenue and adapt to evolving healthcare reimbursement models.

Medicare, including both MA and traditional Medicare, serves as a hub for VBC innovation in the United States. Centers for Medicare & Medicaid Services (CMS) is the largest payer in the healthcare system and holds significant influence in shaping industry standards and promoting the adoption of APMs. The elderly population, which is covered by Medicare, tends to have higher rates of illness and multiple health conditions. This, coupled with the long-term coverage provided by Medicare, makes VBC interventions particularly impactful in reducing the cost of care for these patients.

Within traditional Medicare, the Medicare Shared Savings Program (MSSP) is a widely participated program. The program offers mild shared savings and shared-risk arrangements. The more intensive-risk ACO REACH program attracts more sophisticated VBC providers that are often engaged in MA-capitated contracts.

Currently, VBC is not as common within the Medicaid and commercial markets on a national basis for numerous reasons. For Medicaid, the lower rates of reimbursement (in comparison to Medicare and commercial payers) limit the VBC capitated care model. Also, the high fragmentation of Medicaid regulation from state to state limits the scalability of the APMs. There is a high level of enrollee turnover within Medicaid programs which makes it more difficult to understand individual patient populations over the course of time.

The lack of implementation within commercial markets is due to one main reason: the demographic profile of a typical commercial patient (skewed younger and of higher socioeconomic status) leads to lower health risks. This means that investing a dollar in primary care for a commercially insured individual results in lower, less substantial total cost of care savings compared to Medicare or Medicaid patients. However, the traction of Medicaid and commercial patients in risk-sharing arrangements depends on the market across the U.S. In certain markets, such as California, risk-based arrangements are more common due to the early adoption of health maintenance organizations and the way those programs have shifted into risk-bearing organizations. As data analytics improves and payor-provider convergence continues, the development of Medicaid and commercial VBC structures is increasing.

In the traditional FFS models, the primary relationship was between payors and providers. The shift towards value-based care has led to the evolution of the players involved. These relatively novel VBC participants can be categorized into three main groups, each with its own subcategories.

Many of the prominent VBC players fall within the provider management category. This category aims to back or acquire medical practices operating within VBC frameworks. There are several models that facilitate VBC provider management. There are those operators who seek to establish new clinics and healthcare practitioner recruitment by prioritizing consistent branding and patient experience while tackling capital-intensive challenges.

Other operators contract directly with self-insured employers by offering comprehensive primary care services that often include behavioral health and pharmacy, and by promoting clinic growth through employer contracts. Another provider management model of VBC is the acquisition of provider groups. This model transitions them into physician-owned primary care practices and shifts the revenue toward taking on riskier VBC contracts. Lastly, there are operators that focus on taking specialty practices, such as orthopedics, oncology, or nephrology, and transitioning them into VBC contracting. This is done by leveraging specialty-based operational sophistication and specific specialty VBC payment models.

The second category of VBC players comprises organizations that opt for collaboration with independent providers or medical groups rather than acquiring practices outright. These entities, often referred to as “VBC enablers,” play a pivotal role in facilitating the transition to value-based care. They offer a comprehensive suite of services, including advanced technological solutions, expert consulting, and various forms of support. Through their involvement, these enablers actively engage in the shared risk associated with value-based contracts, demonstrating their commitment to advancing healthcare transformation and fostering a culture of collaboration and innovation. By forging these strategic partnerships, VBC enablers empower independent providers and medical groups to navigate the complex landscape of value-based care successfully, ultimately improving the quality and efficiency of healthcare delivery for all stakeholders involved.

The third category encompasses the technological solutions and ancillary services that play a pivotal role in facilitating the shift from FFS to VBC. There are many different players within this category and the technology-based solutions these companies provide include patient population/risk management, care coordination, surgery coordination, outcomes measurement, and care management. Patient population management is software that helps providers track patient health outcomes, utilization patterns, and risks. It aids in identifying high-risk patients and implementing interventions to reduce costs. Care coordination is the technology behind building quality referral networks, ensuring closed-loop referrals, and sharing patient information among care providers. Surgery coordination is software used to orchestrate surgeries efficiently and manage costs, especially in a VBC context. Outcomes measurement highlights the importance of understanding the quality metrics of the care provided and managing costs of care. Furthermore, care coordination is what guides patients through the healthcare system to improve outcomes and minimize costs. This includes services for chronic condition management and care navigation. These players can provide one or multiple of the services previously described and often contract with other entities in the VBC environment.

The transformation towards VBC healthcare delivery models holds the promise of significant benefits that extend to both cost reduction and the enhancement of satisfaction among providers and patients alike. By concentrating on preventive measures and evidence-based treatments, VBC stands to ameliorate health outcomes and particularly benefit patients with chronic conditions. Furthermore, it promotes the efficient allocation of resources, thereby generating cost savings for both patients and healthcare systems, in particular. One pressing issue is the high rate of hospital readmissions, and it requires attention because it is. Currently hovering at approximately 15% within Medicare. Through an increased emphasis on care coordination and follow-up care, VBC aims to mitigate the frequency of avoidable hospital readmissions. Additionally, it underscores the importance of the patient’s experience and positions the patient at the core of the healthcare process. This ultimately results in heightened patient satisfaction and engagement. Lastly, it addresses physician satisfaction by reducing resource utilization while potentially maintaining reasonable compensation levels. Ultimately, VBC stakeholders expect to create a healthcare system that is more sustainable and centered around the needs of patients, while unlocking profitability and returns for investors.

Although promising, VBC presents its own set of challenges for providers and payers alike. Effective VBC relies on robust data collection and analysis capabilities which necessitates technological infrastructure upgrades for many healthcare organizations. Additionally, determining meaningful quality metrics for specialty care can be intricate due to the specificity of outcome measures required for different conditions. Providers may encounter financial risks if they fail to meet VBC targets, particularly in shared savings or full risk-sharing arrangements. Ensuring alignment of incentives among various stakeholders, including physicians, hospitals, and payers, is pivotal to the initiative’s success. These challenges must be navigated to fully realize the potential benefits of VBC.

Despite the significant hurdles in the way, the healthcare market’s accelerating shift to VBC signifies a profound change towards patient-centered and outcome-driven healthcare delivery. As the healthcare landscape continues to evolve, embracing VBC offers the prospect of enhancing patient outcomes, improving the patient experience, and promoting cost-effective care. However, to unlock the complete potential of this shift in payment models, it may be necessary to seek guidance from healthcare advisors who possess specialized expertise in this field. These advisors play a vital role in helping address patient population challenges, defining pertinent quality metrics, and aligning incentives effectively. In addition, transactions for entities in the VBC space, or healthcare operators looking to enter the VBC space have a need for a specialized understanding of these relatively novel APM models in terms of valuation, reimbursement dynamics, and related transaction agreements.

Written by Grayson Terrell, CPA, Brad Witt, CPA, and Joe Scott, CPA

Revenue cycle management (RCM) is a critical financial process adopted by healthcare institutions to effectively oversee the administrative and clinical aspects related to claims processing, payment collection, and revenue generation. This comprehensive process covers the identification, management, and collection of patient service revenue, and is essential to ensuring the continuous operation of medical practices while prioritizing patient care. The RCM process is initiated the moment a patient schedules an appointment. To ensure its seamless operation, healthcare facilities must prioritize front-end optimization, thereby reducing errors and complications that may hinder the reimbursement process and result in claim denials.

When selecting an RCM system, healthcare organizations must conduct a comprehensive assessment of the reporting capabilities of each system. Evaluation should include factors such as the implementation and management of payor contracted rates within the system, as well as the quality of the reporting outputs of the system. It is imperative to the efficiency and accuracy of the quality of earnings (QofE) process that the management team of a company is well-versed in the capabilities of their RCM system. It is also vital that they are familiar with the reports that can be generated to effectively illustrate their revenue performance and key metrics. This will not only assist with the QofE process but will give management better insight into the key performance indicators (KPIs) of their business which can drive efficiency and growth. Fostering a strong relationship with the selected RCM’s customer relations team is also imperative, as they can provide insight into the preparation of revenue-related QofE requests, as well as assist with preparing custom reports or analyses, if necessary.

Additionally, the management team needs to have a strong understanding of the overall timing of their RCM lifecycle, including how claims are entered into the system, how payments are posted, and if there are any inefficiencies in this process that can be corrected or highlighted for the QofE team. Having a comprehensive understanding of your payor mix, collection timelines, and typical payment patterns will improve both the overall performance of your business and the accuracy of your QofE report.

In cases where the transition to a new RCM vendor is contemplated in the period leading up to commencing the transaction process, practices should be aware that this change could potentially disrupt the timing of revenue cycle activities and the accuracy of data. As a result, this could hinder the quality and accuracy of the revenue analysis within the QofE. A change of this magnitude within the historical period that would be analyzed in the process could preclude the quality of earnings team from performing certain revenue analyses that produce more accurate results. This could ultimately lead to a negative impact on diligence-adjusted EBITDA which could potentially hinder transaction negotiations or result in a re-trade or termination of a deal. Therefore, if such a change must be made in the periods leading up to a transaction, it is imperative to ensure that management teams are aware of any potential impacts on the attainability, comparability, or accuracy of revenue data before and after a system conversion.

A fundamental procedure of financial due diligence in many middle-market healthcare deals is the conversion of the reported financial statements from cash-basis to accrual-basis. Strong RCM processes can alleviate the complexities of this transition, making revenue data more accessible and ensuring the quality of that data is up-to-par for the complex cash-to-accrual analyses performed by the quality of earnings team.

If management has an in-depth understanding of the organization’s RCM system, including its reporting capabilities, it can also empower practices throughout the QofE process in the following ways:

A robust and accurate revenue analysis vastly improves the organization’s ability to defend itself against scrutiny from opposing quality of earnings teams during transaction processes, especially with the aforementioned proforma adjustments. Complex revenue-driven proforma adjustments are often the primary focus of opposing QofE teams given that these adjustments tend to be forward-looking in nature and rely on certain assumptions. Therefore, detailed support from an RCM system and/or tangible proof of progress toward achieving future EBITDA is often required.

Whether you are contemplating the sale of a healthcare company or aiming for more efficient internal financial management, gaining a deeper insight into your practice’s RCM processes and system is paramount to the success of your organization. This knowledge directly influences your organization’s financial stability, growth, and, ultimately, its ability to provide high-quality patient care.

Written by Matthew Marconcini, CPA and Lukas Recio, CPA

In recent years, there has been a notable surge in hospitals and healthcare systems entering into joint ventures with private equity groups. This trend is driven by several different factors that reflect the ever-evolving landscape of the healthcare industry and it is expected to continue in the future.

Howard G. Berger, CEO and Board Chairman of RadNet, said, “Another one of our significant initiatives is expansion through hospital and health system joint ventures. In the past, we have stated that we see a path forward towards holding as much as 50% of our imaging centers in these partnerships.”

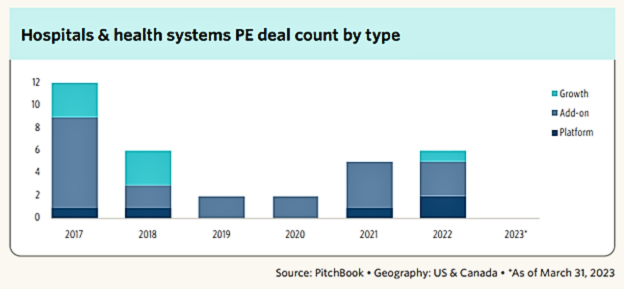

Additionally, based on the graph below, we can see there has been a continued increase from 2019 to 2022 in PE deal count for hospitals and health systems.

Firstly, the financial pressures faced by many healthcare providers have led them to seek external investments to bolster their resources. Private equity groups, with their substantial capital reserves, offer a lifeline to struggling hospitals, and enable them to invest in technology, infrastructure, and quality improvement initiatives.

Secondly, private equity firms bring expertise in business management and operational efficiency to the partnership. In an increasingly competitive healthcare environment, hospitals and health systems must find ways to streamline operations, reduce costs, and enhance patient care. Partnering with private equity allows healthcare organizations to tap into the financial and operational acumen of their partners which leads to more effective and efficient healthcare delivery. For instance, we have seen hospitals create joint ventures within their behavioral health operations because they want to keep the service but need to bring in a partner that has the financial resources and operational expertise to help turn it around. Another area where we have seen an increase in successful partnerships with private equity is hospitals looking for a better urgent care strategy. Private equity has the resources, financial backing, and expertise to bring in the right systems and people to create substantial value. Private equity firms help urgent care clinics standardize processes, consolidate overhead costs, and find new branch locations without saturating the market. This assistance helps relieve physicians from tasks that they are typically too busy to tackle.

Moreover, the shift towards value-based care models has necessitated investments in population health management and preventive care. Private equity investments can provide the necessary funds to develop and implement the necessary tools to accurately estimate the total cost of care with the goal of delivering better patient outcomes and increased cost savings in the long run.

Lastly, the COVID-19 pandemic exposed vulnerabilities in healthcare infrastructure and underscored the need for agile, resilient healthcare systems. Private equity partnerships can help healthcare providers strengthen their resilience, enhance their preparedness for future crises, and adapt to the rapidly changing healthcare landscape.

While there are many benefits hospitals are seeing by partnering with private equity groups, there are several areas, listed below, that need to be discussed between the parties as they consider this partnership:

In conclusion, the increasing collaboration between hospitals and health systems with private equity groups is a response to the multifaceted challenges and opportunities in the healthcare sector. These partnerships offer financial flexibility, operational expertise, and a pathway to innovation. All of these offerings are essential for healthcare organizations striving to provide high-quality care in a rapidly evolving marketplace. As healthcare continues to transform, such joint ventures are likely to remain a key strategy for hospitals looking to thrive in the years ahead.

Written by Kyle Spears and Nicole Montanaro, CVA

Per the U.S. Healthcare Staffing Market Size, Share & Trends Analysis Report, the U.S. healthcare staffing market is expected to reach USD 34.7 billion by 2030. The growing demand for healthcare staffing services has driven the rise in service agreements among related parties, some of which require a fair market value opinion. The underlying reasons for this high demand include:

Additionally, according to the U.S. Bureau of Labor Statistics’ Occupational Outlook Handbook, employment is expected to grow from 2022-2032 for registered nurses (6%), nurse anesthetists, nurse midwives, nurse practitioners (38%), physician assistants (27%), physical therapists (15%), occupational therapists (12%), speech-language pathologists (19%), EMTs and paramedics (5%), and physicians and surgeons (3%).

With this growing demand for healthcare workers, healthcare operators are increasingly seeking new ways to staff their facilities. For example, many have outsourced recruitment and staffing operations to third-party healthcare staffing firms. Another popular solution includes entering into third-party agreements and/or partnerships with other health systems, hospitals, and outpatient facilities that have a greater scope of in-house operations and better access to qualified talent.

The latter is often between parties that may be able to refer to one another which adds a layer of complexity to these arrangements. As with many healthcare arrangements, the fair market value requirement becomes an important part of the process before signing one of these agreements. As discussed in more detail below, VMG Health has provided insight as to what leaders should think through when entering into recruiting and leased staff agreements with related parties.

The typical recruiting services arrangement will include either a retained fee (payment made up-front) or a contingent fee (payment made upon placement) that is stated as a percentage of the candidate’s first-year salary.

Although recruiting services for various position levels (i.e., physicians, advanced practice providers, nurses, senior management, etc.) can be provided by the same personnel or service providers, it is important to note that the fees for each position level often vary based on factors including, but not limited to, the size of the qualified candidate pool, difficulty to recruit a certain position in a certain market, and the skill/expertise required of the candidate. Therefore, many recruiting services agreements will include a specific fee for each position level rather than one encompassing fee for all positions.

Due to the various scope of services and positions recruited, it may be difficult to find agreements in the market that could be considered directly comparable to a party’s recruiting needs. Therefore, from a valuation and compliance perspective, it is also important to consider the service provider’s costs to provide the recruiting services in addition to observed market fees, if available. This two-step process helps the contracting parties truly understand what services are being provided and assists with documenting FMV.

Similar to recruiting services, leased staff arrangements are highly tailored to both the specific needs of one party and the staffing availability of the service provider. That said, the fee structure for these arrangements is often based on a markup to the fully loaded personnel costs, in which the appropriate markup to costs varies depending on the nature of the staffing arrangement and the financial risk placed on the service provider.

From a high-level perspective, an important factor for a staffing arrangement is the nature in which the personnel will be provided, as laid out below:

Additionally, factors such as the contract period of the agreement, payment terms (actual costs vs. projected costs), and type of staff provided (clinical personnel or administrative personnel), may impact the financial risk placed on the service provider under the arrangement.

As the demand for competent healthcare staff continues to grow, healthcare leaders are identifying numerous types of companies that can fulfill their staffing needs. Since many of these companies are in a position to refer, it is important to ensure any recruiting and leased staff agreements are consistent with FMV principles. VMG Health has extensive experience valuing FMV payments for recruiting services and leased staff arrangements.

The following article was published by Becker’s Hospital Review.

Private equity (PE) investment in healthcare is soaring, as investors have raised large amounts of capital and see attractive opportunities in the industry — especially health services.

At the same time, while hospital and health system leaders grapple with narrow operating margins and limited resources, they see exciting possibilities in partnership and joint ventures with PE-based platforms.

To better understand the forces behind these trends, Becker’s Hospital Review recently spoke with Greg Koonsman, founder and CEO of VMG Health, a full-service healthcare advisory firm with extensive knowledge and expertise related to PE investments in healthcare services.

There is $7.6 trillion in PE globally, according to a recent McKinsey report. According to Mr. Koonsman, these funds have grown significantly over the past 15 years, as many institutional investors have increased their allocation of assets to this asset class. As institutional allocations to private capital have swelled, the number of private capital fund managers has grown from 3,700 to more than 13,000.

In the U.S., where healthcare represents about 20 percent of the economy, a proportional amount of PE is allocated to healthcare investments, representing about $500 billion. Of the PE funds allocated to healthcare, Mr. Koonsman estimates that at any given point, there is between $80 and $120 billion in “dry capital” waiting to be invested.

“The sheer size of the market has driven the increased interest in activity by private equity in healthcare services,” Mr. Koonsman said.

In the late 1990s and early 2000s, many PE firms shied away from healthcare services, Mr. Koonsman said. Their reluctance stemmed from the regulatory environment; the presence of nonprofit health systems, which dominated the market; and the powerful role of physicians. “For many years, healthcare services was, in a sense, avoided by many firms,” Mr. Koonsman said.

But in the past 15 years, more PE firms have started to invest in areas adjacent to the core of healthcare, as seen in veterinary medicine, dermatology, ophthalmology, contract research organizations and other ancillary healthcare services. “The oversupply of capital, together with the fact that private equity firms have gotten more accustomed to understanding the nuances of healthcare services and the regulatory environment, has resulted in more investments in healthcare services,” Mr. Koonsman said.

Now, PE firms are going a step further. They’re increasingly investing in healthcare services that are more fundamental to a health system’s core business. This includes investments in diagnostic imaging, ambulatory surgery, cancer treatment, and physician practices in areas like orthopedics, cardiology, primary care multispecialty care and urgent care.

Even with the economic challenges of recent years, PE investment in healthcare has remained strong. An April 2023 Becker’s Healthcare article highlighted key data from consulting firm Bain & Co: In 2021, $151 billion was invested in PE healthcare deals, followed by $90 billion in 2022 — the second-highest year on record. Mr. Koonsman expects this trend to continue in late 2023 and 2024.

As PE firms increasingly eye investments in areas of healthcare that have traditionally been core to hospitals and health systems — and hospitals and health systems struggle to grow in this capital-constrained environment — more discussions are transpiring between health systems and PE funds (or PE-backed platforms) about mutually beneficial partnerships and joint ventures.

Based on his extensive exposure to these types of partnerships and joint ventures, Mr. Koonsman sees immense benefits for both healthcare organizations and PE investors.

Health systems have strong, trusted brands within local geographies; size, scale and leverage within their respective markets; years of data; and relationships at all points in the provider chain. However, health systems, which typically provide services in dozens of verticals, have difficulty allocating their existing capital across multiple areas, lack sufficient capital for growth opportunities and lack the focus and management expertise to capitalize on promising opportunities.

These shortcomings are areas where PE funds and PE-backed platforms can bring tremendous value. PE has access to significant capital and excels in building professional management teams with a laser focus on specific growth opportunities. This combination of capital, management expertise and focus can accelerate the speed of maximizing growth opportunities and value.

“I think when you put those positive attributes together, a very good partnership can be developed,” Mr. Koonsman said.

However, in building successful partnerships, there will be obstacles. Among them is achieving alignment. Mr. Koonsman has found that PE firms often lack a deep understanding of health systems, especially nonprofit systems, and health systems often don’t understand or appreciate the value of a PE platform. When these parties make efforts to better understand one another’s goals, strengths and time horizons, misconceptions or knowledge gaps can be reconciled.

Further, a health system might consider participating as an investor in a PE platform. This provides the health system with insight to the benefits of the partnership and the equity value created. “It has been a mistake for health systems to create significant value in a platform without participating in this value,” Mr. Koonsman said. “There is an opportunity for a health system to create value in their local market through the partnership itself and also participate in a national platform that’s going to create outsized returns for their investment.”

Generally speaking, the types of PE firms looking at investments in healthcare services are funds with $500 million to $5 billion (middle market private equity) to invest. When considering a potential investor, health systems should look carefully for partners with a significant focus on healthcare. “Having a firm that understands healthcare is critical,” Mr. Koonsman said. “I would say that probably the experience and expertise in healthcare is the most important differentiator.”

It’s also critical that health systems look for “partnership-oriented firms.” Some investors will purchase 90 to 100 percent of a firm and then behave as an autocrat, which is not the type of a partner a health system wants. Health systems want investors who are collaborative and partnership-oriented. This is essential.

Mr. Koonsman said these partnerships are only going to expand. “They are fundamentally a part of the future of health systems,” he said, adding that he foresees more partnerships involving physician organizations in various specialties, including musculoskeletal, cardiology, oncology, OB-GYN, primary care, urgent care, post-acute care and more.

He envisions a new form of three-way partnership emerging that involves the health system, physicians and a PE-based platform. “I think there’s an opportunity for realignment of the relationship between health systems, physicians and private equity,” he said. “I think there’s a way the health system can accomplish their strategic objectives with their physician partners and roll them back into more of an ownership position alongside private equity-based businesses — almost like a three-way venture that realigns everyone’s economic interests.” While complex, such partnerships are possible, with the ambulatory surgery center business providing a prime example, he said.

There is significant opportunity in PE investments in healthcare today, given the tremendous amount of uninvested capital and a strong demand among investors, which is likely to continue for years.

At the same time, for health systems, PE represents an important source of capital that can help fuel necessary growth. The key is to identify PE partners with deep healthcare expertise and a partnership orientation.

Through effective partnerships, where there is alignment between health systems, physicians and equity-backed platforms, all parties can realize benefits.

Authors

Related Content