Orthopedic Medical Group Spotlight: Market Drivers and Alignment Opportunities

July 25, 2023

Written by Sydney Richards, CVA, Clinton Flume, CVA, and Patrick Speights

Orthopedics-focused ambulatory surgery centers (ASCs) are one of the fastest-growing segments of ASCs [1]. Orthopedics simplistically is the diagnosis, treatment, prevention, and rehabilitation of musculoskeletal system injuries and diseases. This specialty is evolving quickly to leverage demographic, payor, and technological marketplace shifts. Though the industry is still highly fragmented across the United States, VMG Health continues to see a demand for affiliations with strong orthopedic groups emerging from diverse contexts such as health systems, nationwide ASC operators, and private equity groups. Many orthopedics groups are considering whether now is the right time to pursue an affiliation or acquisition and how much their business could be worth to a potential buyer. Below, VMG Health experts highlight a few of the key trends impacting orthopedics providers in the U.S. We also identify what makes an orthopedics group attractive (Hint: It’s not just about the bottom line).

Compared to other specialties, orthopedics was hit disproportionately hard by the deferment of elective procedures during the COVID-19 pandemic and subsequent labor shortages. Through the second quarter of 2023, many markets have stabilized and recovered to pre-pandemic volumes. Over the next decade, orthopedics providers will continue to face unprecedented demand growth fueled by the aging population. Geriatric patients are naturally more susceptible to injury and disproportionally experience degenerative joint conditions compared to younger populations. As the population age shifts and there are continual technological innovations, people will live and work longer, which will create increased demand.

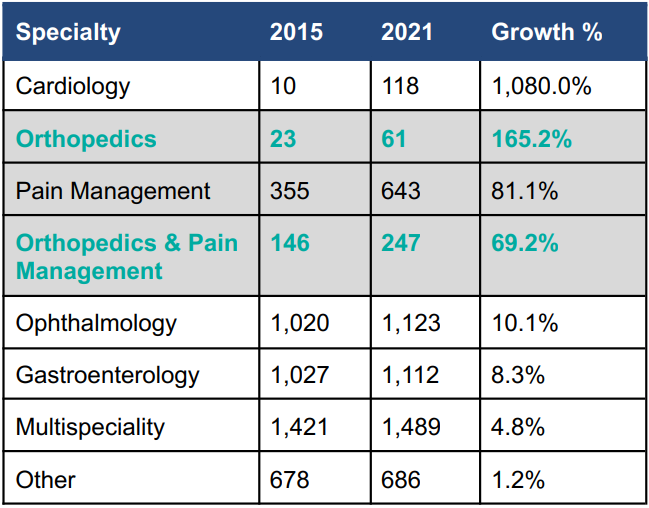

The population-driven demand for orthopedics services is further exacerbated by innovations and regulatory changes in the industry, such as the migration of inpatient-only procedures to ASC settings. It is estimated that moving total joint replacement cases from hospitals to ASCs lowers the cost of care by approximately 40% while maintaining the same outcomes [2]. As a result of this significant savings opportunity, around the beginning of 2019 [3] many commercial payors began requiring cases to be performed in ASCs rather than hospital surgery departments unless the latter were medically necessary due to complications or comorbidities. Medicare is also increasingly willing to pay for ASC procedures. For example, total knee replacements were approved for ASCs in 2020 and total hips were approved in 2021. Although the reimbursement is lower in an ASC than it would be in a hospital setting, according to VMG Health’s ASC benchmarking analysis, orthopedics cases are the highest-reimbursing cases performed in ASC settings nationally [4]. Many physicians also prefer operating in a specialized ASC setting where they can control the patient experience and operating room setup and earn returns for driving efficiency in expenses and operational metrics. As shown in the data below, in response to these opportunities orthopedics-focused ASCs are among the fastest-growing types of ASCs, along with cardiology and pain management. Nationwide, providers are investing heavily in the equipment and unique buildouts required to specialize in orthopedics, such as 23-hour-stay recovery suites.

Source: MedPAC, 2023

To service the forecasted demand volumes and ensure that capital spent developing orthopedics-focused ASCs is optimized, there is a growing demand for orthopedic medical groups among private equity representatives, ASC operators, and health systems alike. Physicians are also increasingly interested in partnerships. Macroeconomic factors, such as inflation and rising costs of capital, compound the already burdensome administrative challenges facing healthcare providers. Factors such as declining reimbursement, shifts in payment models (fee for service, bundle pricing, value-based care), labor shortages, rising medical supply costs, and retiring providers have boosted physicians’ desires for partnerships. In choosing the most appropriate alignment model for partnership, physicians will be interested in monetizing their business’ equity and structuring their compensation package and strategic partner’s future vision.

Stakeholder alignment with orthopedic groups focuses on several key factors, a few of which are outlined below. While this is not an exhaustive list, the topics below highlight many salient considerations and value drivers for a medical group affiliation:

Does the orthopedic medical group have a favorable reputation in the community? Has the practice invested in modern infrastructure to enhance patient care and optimize practice management?

What is the medical group’s competitive position in the market? How does the medical group’s reputation and growth trajectory compare to those of their peers? Individually, what are each of the orthopedic physicians’ future outlooks?

How do the medical group’s provider base and productivity compare to national benchmarks? Does the medical group leverage mid-level providers? What are the current and projected compensation structures? Are key producers nearing retirement? Post-transaction, what would be the opportunities for key provider income repair if a portion of the earnings were sold forward in a transaction?

What complementary ancillary services are provided by the medical group? For example, is there a comprehensive range of orthopedics services, such as a surgery center, imaging, or on-site physical therapy?

Below we have outlined private equity, hospital, health system, and corporate entity stakeholders and the value they may attribute to alignment with orthopedics groups.

Private Equity

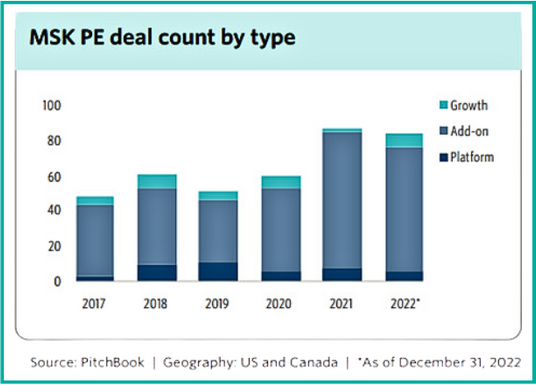

Orthopedics is one of the most active segments of the healthcare services industry for private equity investment. Compared to other clinical subspecialties, orthopedics remains highly fragmented across the nation. Moreover, the strong demand discussed above and a growing shortfall [5] of physician supply create highly favorable investment opportunities for private equity platforms seeking to form strategic partnerships with independent orthopedic groups. Below we have included a summary of the trending count of orthopedics-centered private equity deals in recent years.

Health Systems

For many health systems, partnering with orthopedic physician groups provides an opportunity to partially recapture profitable inpatient cases, as they have transitioned to physician-owned ASCs. We have seen numerous care models evolve and expand recently, such as joint ventures with local orthopedics groups to construct de novo, highly specialized orthopedic surgery centers. The benefits of such an arrangement could include the following:

Specialized ASCs allow for highly skilled staff and have facilities structured for top-tier patient quality and outcomes

Opportunities to create de novo ASCs and realize returns through joint affiliation

Physicians capitalizing on health system brands, debt rates, and supply chain efficiencies

Partnership with a health system may allow more favorable contracting compared to an independent context

ASC Operators

For ASC operators, orthopedic group partnerships represent an opportunity to gain market share and leverage their existing ASC expertise. The benefits of partnering with ASC operators could include the following:

Access to and guidance in operational best practices for ASCs, potentially improving care quality, patient outcomes, and returns

Relief of management/administrative burden on providers through access to a strategic partner, for example, recruitment assistance

Access to ASC operator debt rates and supply chain efficiencies

The right partnership can provide orthopedics groups with access to resources and expertise to improve their competitive advantage and patient care through the relief of administrative burdens and improved financial stability. Physicians should consider their long-term goals when evaluating potential partnerships and offers. For future stakeholders, including corporate entities, health systems, and/or ASC operators, the potential value of an orthopedics group extends beyond the bottom line of the organization. By joining forces, orthopedics providers and their partners can bridge the gap between expertise and resources. Alignment with the right partner can improve patient outcomes and elevate the standard of care for orthopedic patients at a more efficient cost.

The dermatology market has long stood out as an attractive space for private equity (PE) firms due to its continuous year-over-year revenue growth rate, and an expected 2023 CAGR of 13.4%, showcasing the potential for substantial returns [3]. Driven by rising demand for specialized skincare services and advancements in treatments, the industry is experiencing a robust growth trajectory due to PE’s interest in the sector’s potential for generating substantial returns and its proven resilience in the face of economic fluctuations (e.g., COVID-19).

The dermatology market’s allure lies in its promising market dynamics, including opportunities for consolidating practices, leveraging economies of scale, and optimizing operational efficiencies. Additionally, the growing consumer awareness and emphasis on skin health have contributed to a robust and expanding market demand. With relatively favorable reimbursement structures, evolving regulations, and technological advancements supporting the sector, PE firms are keen to invest in dermatology practices and capitalize on their growth potential.

Industry Overview

Since 2011, the dermatology sector has witnessed robust market activity and this trend shows no signs of slowing down. According to Pitchbook’s analysis of transaction activities and deal flows in the dermatology space, there were 134 private equity transactions recorded between 2020 and 2022, indicating a strong and consistent demand for investment when compared to the 171 transactions between 2017 to 2019. However, it is important to note these figures only include transactions that are strictly related to dermatology practices and do not include med spas or other aesthetic services. Additionally, even with the significant deal flow in the space, the market remains highly fragmented with no single participant owning 1.0%+ of the total market [3].

The growth and stability of the dermatology industry is fueled by several factors. First, the market itself is highly fragmented, as outlined above. Additionally, the industry benefits from an aging population with over 69% of dermatology patients being over the age of 40 [2]. Considering this age group accounts for 47.9% of the entire U.S. population in 2020 (U.S. Census Bureau), the demand for dermatological services is poised to rise. Moreover, the limited number of board-certified dermatologists further amplifies the favorable supply/demand dynamics [2]. Another driving force is the increased awareness of skin health due to more individuals recognizing the importance of early detection and treatment. For instance, skin cancer affects approximately 9,500 Americans daily with annual treatment costs estimated at $8.1 billion [6]. Consequently, the robust demand for dermatological services persists and ensures the industry’s continued growth.

Reimbursement Trends

It is interesting to note that while the demand and activity within the space are undoubtedly high, the Medicare reimbursement rates have decreased by roughly 10% between 2011 and 2021. In a peer-reviewed study published in 2022, doctors found management codes and both procedural and evaluation experienced an average decline in reimbursement over the span of 10 years. Out of the 20 codes tested, 15 had a higher average decrease in reimbursement [4]. However, it is important to mention the author also noted that this decrease is in line with similar trends observed in other medical specialties, albeit to a lesser extent.

A separate study on reimbursement rates between 2000 to 2020 further supports and confirms the overall decrease in reimbursement rates. This study identifies the decline was primarily attributable to changes in valuation by the relative-value scale update committee and healthcare policy changes aimed at reducing reimbursement. Additionally, the authors emphasized that reimbursement for other healthcare sectors experienced more significant decreases. For example, emergency medicine experienced a decrease of 29% over the same period [5].

Investment Considerations and Value Creation Opportunities

Private equity firms can add significant value to dermatology practices by streamlining administrative functions, leveraging their business expertise, and capitalizing on marketing and cross-selling opportunities. By consolidating practices to include the currently untapped cosmetic sub-industry, PE firms can utilize fresh capital pools. This can create platform companies to capture more market share and scale administrative tasks which allow dermatologists to focus on patient care. However, aligning goals between physicians and PE partners and maintaining long-term practice stability are essential considerations.

Recent Dermatology-Focused PE Transactions

D1 Investor: GarMark Partners | Operator: The Dermatology Specialists | May 1, 2023

GarMark Partners was founded in 1997 as a mezzanine investment firm and is headquartered in Stamford, Connecticut. GarMark provides junior debt and structured equity capital to middle-market companies with over $1.4 billion of capital invested across their entire portfolio, and over $685.0 million is within the healthcare space. GarMark’s goal is to employ flexible investment strategies that encompass a wide range of transaction types along with deep expertise in investing across the capital structure to achieve long-term business success. GarMark has completed three investments related to the healthcare industry, including dermatology, pediatrics, and nutrition.

The Dermatology Specialists (TDS), located in New York, New York, was founded in 2019 and is now the largest dermatology practice in New York City. The practice specializes in both medical and cosmetic treatments in the field of dermatology with over 30 locations across Manhattan, Brooklyn, Queens, the Bronx, and Long Island.

D2: Investor: ACE & Company | Operator: MedSpa Partners | April 1, 2023

ACE & Company (ACE) was founded in 2005 and is headquartered in Geneva, Switzerland. With over $1.7 billion of assets under management across over 150 companies worldwide, ACE’s goal is to leverage its relationship with top investment firms, corporate partners, and entrepreneurs to provide private investors with exceptional investment opportunities and solutions. ACE has completed six investments related to the healthcare industry, including healthcare IT, dermatology, pediatrics, and laboratory services.

MedSpa Partners (MSP), located in Toronto, Canada, was founded in 2019 and is the operator of an acquisition platform intended for medical aesthetic clinics. The platform acquires medical spas and cosmetic dermatology clinics. MSP focuses on providing support in areas such as clinic management, marketing, business intelligence, legal, and others to enable its acquisition partners to achieve their goals and create valuable customer experiences.

Outlook and Conclusion

The dermatology market is poised for continued growth with favorable industry trends offering significant opportunities for building and scaling platforms. However, the scarcity of board-certified dermatologists may pose challenges in initial hiring and retention. Adding cosmetic services to complement medical-surgical dermatology is expected to unlock untapped growth potential. As mergers and acquisitions reshape the landscape of dermatological care, these activities will drive advancements in patient care, fostering innovation, and unlocking new avenues for growth.

Key Findings from Private Equity’s Healthcare Play: Management Service Agreements

June 21, 2023

Written by Holden Godat, Taylor Anderson, CVA, and Trent Fritzsche

With the emergence of private equity (PE) firms attempting to align with physician practices, VMG Health has seen an increase in the number of management services agreements (MSAs). Due to the highly fragmented and regulated nature of healthcare, PE investment in healthcare is not as straightforward as in other industries. In states with some level of corporate practice of medicine (CPOM) adoption, PE’s interaction with physician practices usually involves a “Friendly PC” model with an affiliated management services organization (MSO) [1]. In return for providing most of the non-clinical assets and services to a physician practice, the MSO charges a management fee via an MSA. To better understand how these arrangements are structured in the market, VMG Health experts have outlined their findings from valuing over 120 MSAs and offer insight into how to generate more value from these agreements.

Key Observations

Targeted Specialties

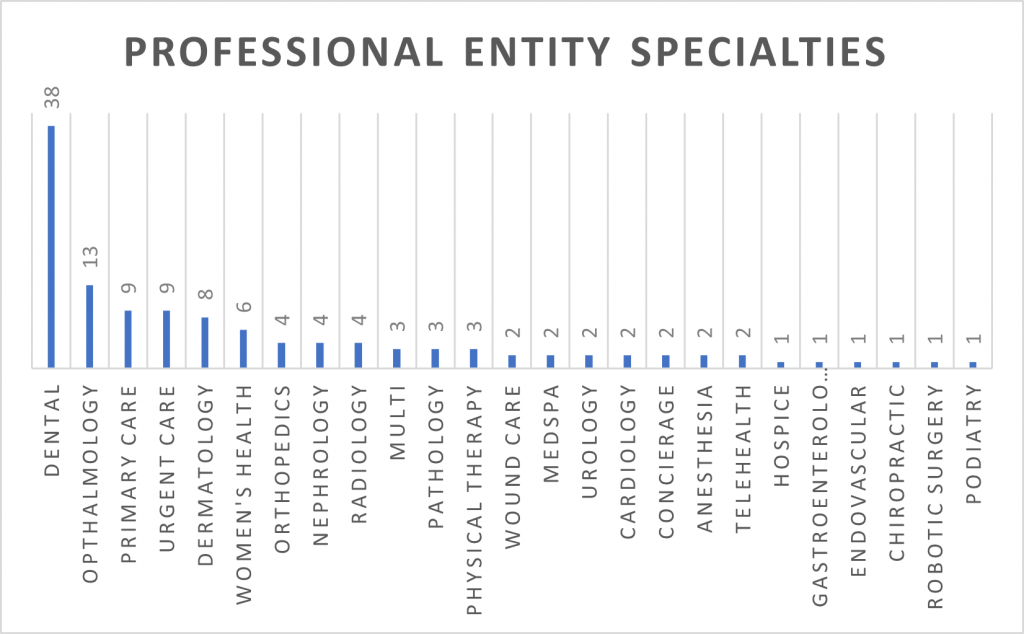

As private equity investment has increased over the years, climbing from $19.5 billion in 2015 to $74.4 billion in 2022, the variety of specialties targeted has also increased [2]. In 2015, VMG Health experts observed that the main specialties undergoing consolidation were anesthesia, dermatology, and gastroenterology. While those specialties are still prevalent today, there has been an emergence of transactions and consolidation in dental, ophthalmology, urgent care, primary care, and women’s health.

Observed States

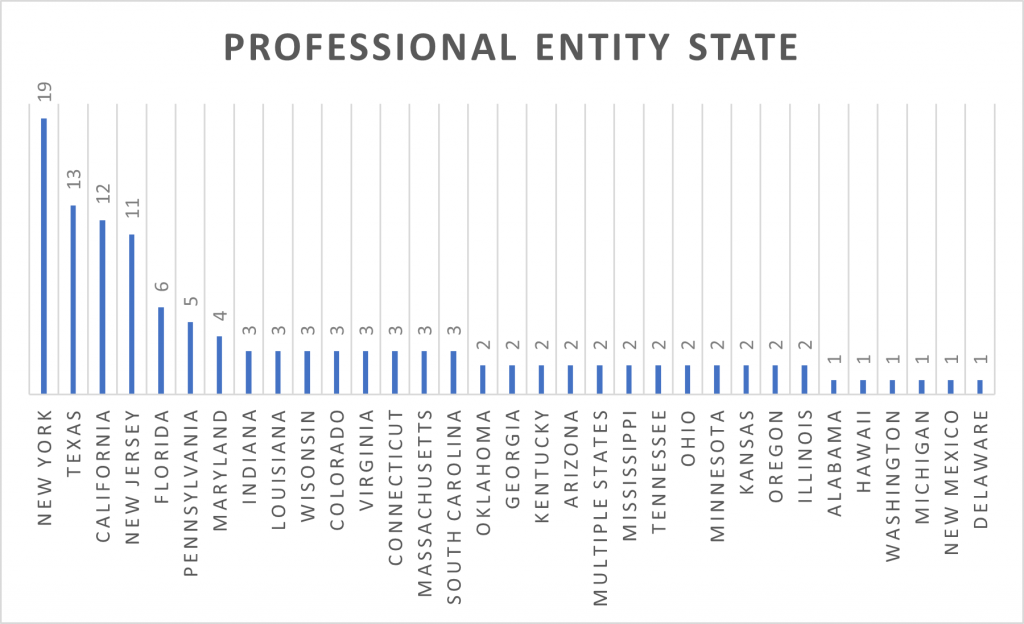

From large and diverse geographies to strict adoptions of CPOM, a doctrine developed to protect the quality of patient care by “prohibiting corporations from practicing medicine or employing a physician to provide professional medical services,” it is no surprise New York, Texas, California, and New Jersey have the most observed MSA valuations [3]. VMG Health experts note that while these states have dominated MSA valuations for the past few years, the arrival of other states to this chart demonstrates that consolidation and resulting PE investments are occurring nationwide.

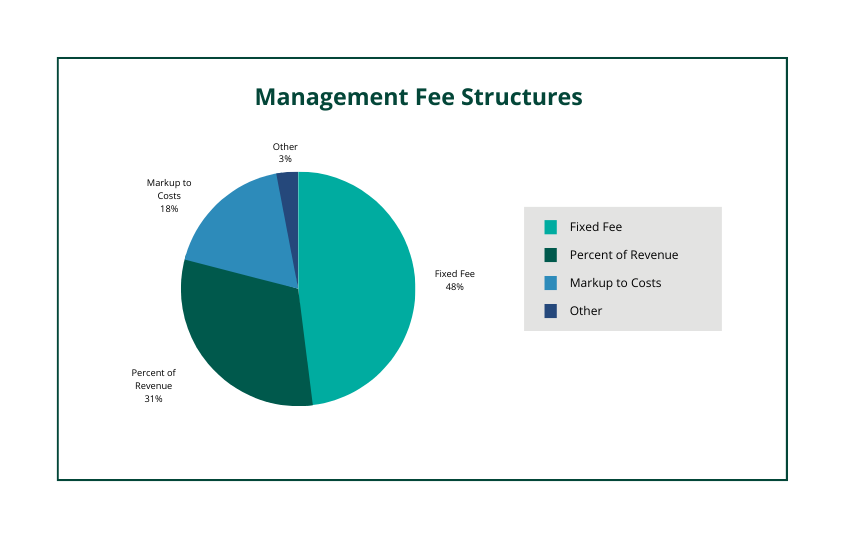

Varying Fee Structures

VMG Health observes the most common fee structures present in MSAs are fixed fees, percentage of revenue, and markup to costs. However, VMG Health has also seen management services organizations trying to get more creative in designing fee structures. This can take shape by implementing a combination of the three, creating variable tiers tied to performance, or creating a structure based on the number of providers. With CPOM, it is important to be aware of state-specific requirements when entering an MSA. As an example, many attorneys believe that New York’s CPOM adoption requires a fixed fee only in its fee structure, while Texas and California might allow for variable fee structures (i.e., percentage of revenue, a markup to costs, etc.).

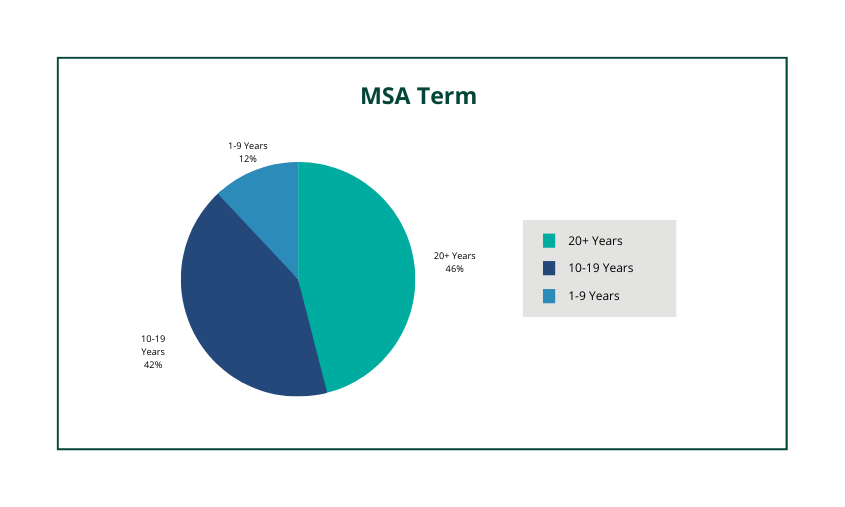

MSA Term

With platform practice multiples exceeding 10x, it is not uncommon to see MSA terms lasting more than 10 years. In fact, over 75% of observed MSAs had a term of 10+ years. While the total term can last for decades it is very common to see renewal periods that are in a two-to-five-year period.

Valuation Drivers

Within any MSA valuation, there are common terms that VMG Health looks for in assessing value. These terms assist in demonstrating where the ultimate business risk lies, which in turn leads to extracting the most value from the professional entity (i.e., the greater the risk, the greater the return, etc.). The following outlines some of the pertinent terms VMG Health experts look for in an MSA:

Contracted Services– In any MSA seeking to capture as much value as possible it is common for all legally permissible services to be the responsibility of the MSO. While it varies from state to state, this typically means that all expenses become the responsibility of the MSO except for clinical expenses and/or clinical personnel. Of the observed MSAs, 11% had the professional entity retain material services that are normally viewed as the responsibility of the manager. VMG Health notes that in these events there was usually a preexisting obligation that required the professional entity to retain the non-clinical expense (i.e., the professional entity was on the lease and the landlord prohibited a sub-lease arrangement).

Priority of Payments – Demonstrating that the management fee is subordinated to most other expenses and fees is imperative. This is because it places a greater risk on the MSO to efficiently budget costs to ensure the necessary funds are available to pay the management fee. Of the observed MSAs, 10% did not have any priority of payment language or had a waterfall of payments that did not subordinate the management fee.

Deficit Loan Funding – Another manner in demonstrating an MSO’s business risk in an MSA is through the inclusion of a deficit loan funding covenant. This typically puts the MSO at risk to cover any obligations (i.e., expenses, fees, etc.) in the event the professional entity does not generate enough revenue to cover those amounts. Of the observed MSAs, 47% of MSAs had a deficit loan funding covenant present.

When structuring an MSA it is important to consider all these factors to maximize value and to ensure compliance. In CPOM states, the management fees stated within MSAs must be set at fair market value. Upon drafting an agreement, a fair market value opinion from a third-party valuation expert can alleviate compliance concerns.

Understanding & Solving the New Reality for Anesthesia Services

June 15, 2023

Written byMallorie Holguin and Patrick McGinn

Over the last several years, healthcare executives and practice administrators have faced challenges in securing anesthesiology services, particularly in the inpatient setting. These challenges have been exacerbated over the past couple of years due to staffing shortages caused by the COVID-19 pandemic and an ever-increasing demand for anesthesia services.

At the outset of 2023, the United States population consisted of approximately 65.6 million adults eligible for Medicare with a projected growth to 76 million Medicare-eligible adults in 2030 [1]. The projected growth in the Medicare-eligible population will result in a corresponding increase in demand for inpatient procedures and diagnostic testing which may require anesthesia and the expertise of anesthesiologists, certified registered nurse anesthetists (CRNAs), and other anesthesia providers [2]. Meanwhile, current data reported by the Association of American Medical Colleges (AAMC) suggests only 43.1% of active anesthesiologists are under the age of 55, and there is a projected shortage of 12,500 anesthesiologists in 2033 [3,4]. Furthermore, anesthesiologists are largely practicing as independent providers to hospitals/health systems and are faced with decreasing reimbursement and increased expenses related to staffing, supply chain, and provider compensation.

Reimbursement Trends

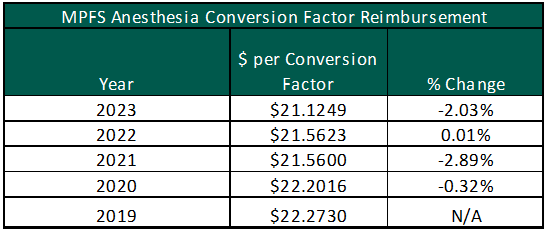

While the demand for anesthesia services increases, reimbursement for Medicare patients has decreased from $22.2730 per unit in 2019 to $21.1249 in 2023 under the Medicare Physician Fee Schedule (MPFS). The chart to the right illustrates the year-over-year percentage change in the anesthesia conversion factor under the MPFS. Anesthesia providers were further impacted by the implementation of the No Surprises Act (NSA) and the independent dispute resolution (IDR) process. The NSA has led to unintended consequences for anesthesia providers. Based on discussions with anesthesia practice leaders, payor insurers have utilized the IDR to reduce their required reimbursement by refusing to go in-network with the anesthesia providers [5,6]. As a result, VMG Health has been receiving an increasingly high number of requested subsidy arrangements for ambulatory surgery centers (ASCs). Hospitals and other free-standing surgery centers should partner with their anesthesia group and advocate for in-network contracts with all major payors in their market.

Staffing Shortages & Market Compensation Pressure

The reduction in federal and commercial reimbursement for anesthesia services compounds the increased cost pressures faced by anesthesia providers, particularly as it relates to provider staffing costs. Per Medscape’s 2023 Physician Compensation Report, anesthesiology reported a 10% increase in compensation which is consistent with market-observed trends and conversations with health system operators. The charts below show the most current compensation data for anesthesiologists and CRNAs from the AMGA, MGMA, SullivanCotter, Inc., and Gallagher compensation and productivity survey reports:

MGMA recently released its 2023 Provider Compensation and Production Survey Report, which shows further increases in median compensation levels: anesthesiology compensation falling close to $500,000 and CRNA compensation reported at approximately $215,000. At the same time, Merritt Hawkins reports record-level sign-on bonuses, relocation expenses, and medical education loan repayments.

New Reality for Anesthesiology Groups & Health Systems

The confluence of decreased federal and commercial reimbursement amid increased compensation associated with staffing anesthesia providers is challenging independent anesthesiology groups and health system/ASC partners. Going forward, health systems, ASCs, and anesthesia partners may need to consider alternative partnerships including acquiring the practice, negotiating a new professional services agreement or amending an existing one, and/or considering recruitment assistance. Regardless of the avenue, the anesthesia practice will likely require some sort of direct support (e.g., through revenue guarantees or subsidy arrangements) to ensure they are able to recruit and retain providers.

In each of the cases outlined above, documentation that illustrates the relationship between the parties has been established at fair market value (FMV) and represents best practices for compliance and regulatory purposes. Regarding the direct employment of anesthesiologists and CRNAs, the employment terms should be based on the personally performed services of the respective provider and the unique demands of the local market. For anesthesiology revenue guarantee and subsidy arrangements, key factors to consider are the number of anesthetizing locations, the proposed care team model (i.e., physician medical direction versus supervision), and the projected payor mix of the facility. As previously mentioned, the NSA has led to decreased commercial reimbursement which has led to the need for subsidy/revenue guarantee agreements for ASCs that historically have not been required.

As health systems, ASC systems, and anesthesia providers navigate the increasing demand for anesthesia services in the face of declining federal and commercial reimbursement, VMG Health can provide both FMV and strategic services for the various stakeholders.

The following article was published by the American Association of Provider Compensation Professionals.

Hospitals play a crucial role in healthcare, providing advanced medical services to patients requiring the most acute levels of care from specialized physicians. To ensure adequate physician coverage of various specialty service lines and timely high-quality patient care, hospitals often enter into coverage agreements with independent provider groups. Through these agreements, provider groups provide on-site clinical coverage, unrestricted on-call coverage, and administrative management services to hospitals, often in exchange for the right to bill and collect from patients/payors and compensation payable by the hospital.

In structuring these types of hospital coverage arrangements, due diligence is necessary to ensure the compensation terms are consistent with fair market value (FMV) and maintain compliance with the Stark Law and Anti-Kickback Statute. In this article, we’ll discuss the key fair market value and operational considerations for the most common hospital coverage agreement compensation structures.

Compensation Structures

The first step in structuring a service arrangement with an independent provider group is often determining which party will bill and collect for the professional services the group will provide. In many cases, the hospital, especially if affiliated with a larger health system, might enjoy better-contracted rates with major commercial payors due to market bargaining power. Hospitals may also benefit from economies of scale enabling more efficient revenue cycle management. In other cases, a provider group, especially if affiliated with a large national or regional entity, may already have the infrastructure, commercial contracts, and billing and coding expertise within their medical specialty to efficiently bill and collect for its professional services.

This article focuses on considerations in structuring hospital coverage arrangements in which the independent provider group bills and collects for its professional services rendered. Service arrangements in which the hospital bills and collects for professional services are not covered in this article.

Common Compensation Structures When Group Bills and Collects for Professional Services

Provider groups incur significant costs to staff a hospital coverage arrangement including provider salaries, benefits, malpractice insurance premiums, billing and collection, back-office support, and overhead costs.

In some hospital coverage arrangements, the professional collections generated by the group directly from patients/payors are sufficient to cover these expenses. However, in scenarios in which the professional collections generated by the group are not sufficient to cover its costs of providing the coverage, hospitals often pay additional compensation to the group to offset the shortfall of professional collections to costs incurred.

This shortfall may be due to relatively low case volume and collections relative to the on-site and on-call coverage required by the hospital. Additionally, some hospitals serve a high percentage of Medicaid, self-pay, and charity care patients resulting in relatively low professional collections generated by the provider group.

In these types of scenarios, there are two common structures to compensate the provider group: (1) a fixed subsidy or stipend, or (2) a collections guarantee. VMG Health has observed other compensation structures in hospital coverage agreements, but these two remain the most common.

Fixed Subsidy/Stipend Structure

This compensation structure compensates the provider group based on a pre-determined fixed amount to subsidize the group’s shortfall in professional collections relative to costs incurred to staff the service line.

Benefits of a Fixed Subsidy/Stipend from a Hospital’s Perspective

Easy to Administer: Because of the fixed nature of the compensation structure, this is a relatively simple compensation model to administer for the hospital once the coverage agreement is executed. Once the subsidy is established as FMV at the outset of the arrangement, the hospital pays the group the negotiated amount, typically without the need for data collection or reconciliation. The hospital may refresh the FMV analysis of the fixed subsidy periodically, often every one to two years to ensure the fixed subsidy does not exceed FMV based on changing patient volumes, coverage requirements, or professional collections.

Incentivizes Provider Group to Maintain Efficient Billing and Collection Processes: Because the provider group is receiving a fixed subsidy from the hospital, any collections the provider group receives above the projected professional collections would effectively result in incremental compensation to the group. This might incentivize the provider group to develop and maintain efficient billing and collection procedures.

Drawbacks of a Fixed Subsidy/Stipend from a Hospital’s Perspective

Compliance Risk: Conversely, because the subsidy amount payable to the provider group is determined at the outset of the arrangement, there is a risk that the compensation paid by the hospital to the provider group could exceed fair market value if the professional collections generated by the provider group exceed expectations.

Collections Guarantee Structure

A collections guarantee structure compensates the provider group based on the difference between a pre-determined collections guarantee and the actual professional collections generated by the provider group under the coverage arrangement for a given period. The negotiated collections guarantee is typically set at a level meant to cover the projected costs of the provider group to staff the service line.

Benefits of a Collections Guarantee from a Hospital’s Perspective

Self-Adjustment Mechanism: Because this compensation structure reconciles the difference between the negotiated collections guarantee and the actual collections generated by the provider group, the compensation payable by the hospital to the provider group self-adjusts for the precise shortfall of the provider group’s collections to its expenses incurred to provide the clinical coverage. Therefore, theoretically, the hospital would never overpay or underpay the provider group for periods in which the provider group has higher or lower professional collections than initially projected.

Less Compliance Risk: Because of the self-adjustment reconciliation process of a collections guarantee, if the provider group’s collections improve due to more a favorable payor mix, more efficient collections processes, higher patient volumes, etc., then the compensation paid by the hospital would self-adjust for these changes. Therefore, the hospital would have less risk of paying the provider group compensation that exceeds FMV and running afoul of the Stark Law and Anti-Kickback Statute.

Drawbacks of a Collections Guarantee from a Hospital’s Perspective

Greater Administrative Burden: Because the compensation structure requires a reconciliation of the negotiated collections guarantee and the actual collections for a given payment period, it may create a greater and more frequent administrative burden to the hospital relative to a subsidy compensation model. The hospital would need to collect accurate revenue data from the group periodically to compensate the provider group for the clinical coverage.

Less Incentive for the Provider Group to Maintain Efficient Billing and Collection Processes: Because the provider group would be compensated for the difference between a negotiated collections guarantee and actual professional collections, its total compensation from staffing the arrangement remains static regardless of professional collections generated. Therefore, there is theoretically less incentive for the provider group to invest resources to bill and collect efficiently for its professional services as the hospital would subsidize any shortfall. This could result in the hospital paying a higher compensation amount if the provider group does not bill and collect efficiently.

Conclusion

Hospital coverage agreements between independent provider groups and hospitals can help improve patient outcomes, reduce healthcare costs, and increase efficiency. Hospital administrators must balance compliance considerations, administrative burden, and operational alignment between the hospital and the provider group. When structuring these arrangements, it’s important to understand the risks and benefits of each model and to ensure the compensation structure and amounts result in compensation consistent with FMV.

Four Key Valuation Considerations When Converting the Imaging Operations of a Hospital Outpatient Department to a Freestanding Center

June 8, 2023

Written by Stephen H. Schulte, CVA, and Madison Higgins

The following article was published byVMG Health’s Imaging & Radiology Affinity Group

In recent years, the healthcare industry has experienced a shift toward freestanding sites of service as more patients opt for lower-cost, convenient, and specialized care. This trend is particularly evident in outpatient imaging services where patients are increasingly opting for the comfort and accessibility of freestanding imaging centers over hospital outpatient departments (HOPDs). As a result, hospitals and health systems are becoming increasingly eager to partner with established operators of freestanding imaging centers. These partnerships often include the acquisition of an ownership interest in an existing freestanding center but may also include the contribution of their HOPD imaging operations to an existing freestanding center or potentially to a new joint venture (JV). When considering the conversion of an imaging HOPD to a freestanding center, there are several important factors to consider from a fair market value (FMV) valuation perspective. These include the proper identification of the volumes to be included in the conversion, the potential impact on patient volumes and reimbursement, changes to the operating expense structure, and the contribution of necessary equipment.

Scan Volume

Correctly identifying the specific volumes that would be a part of this transition is one of the most critical factors to consider when valuing an imaging HOPD that will convert to a freestanding imaging center. Imaging volumes within an HOPD may include volumes related to different service lines such as emergency room visits, outpatient surgical procedures, routine outpatient imaging services, etc. Based on our experience in these situations, the volumes related to routine outpatient imaging services are the most likely to transition. With that said, the volumes related to emergency room visits and outpatient surgical procedures are less likely to transition due to logistics and other clinical factors.

Once the appropriate volumes have been identified, it is important to understand what impact, if any, there would be upon the transition to freestanding operations. The operations of an imaging HOPD may have a large volume of high-acuity scans for patients with more severe health conditions which could be at risk in a freestanding setting. Alternatively, freestanding imaging centers typically provide more convenience for patients since they are generally located closer to residential areas, have their own dedicated parking areas, and patients do not have to navigate the larger hospital environment. This convenience factor can lead to an increase in patient volumes across all modalities but is particularly evident for routine imaging procedures such as X-rays, mammography, and bone density scans. Additionally, as mentioned above, freestanding imaging centers tend to be the low-cost provider compared to an HOPD which may also positively impact volumes. Due to the complexity surrounding these factors, future volume expectations should be discussed in detail with those who are familiar with the current volumes, area demographics, and the competitive landscape in the local marketplace.

Reimbursement/Net Operating Revenue

Another key consideration is the potential shift in reimbursement rates and the impact on the net operating revenue. Reimbursement rates at an HOPD level may not be directly achievable for a freestanding center for a variety of reasons. HOPDs receive Medicare reimbursement rates according to the Outpatient Prospective Payment System (OPPS) set forth by the Centers for Medicare & Medicaid Services (CMS), while freestanding facilities receive Medicare reimbursement rates according to the Medicare Physician Fee Schedule (MPFS).

In general, OPPS rates tend to be higher than MPFS rates for the same service and can result in an expected decrease in Medicare reimbursement that must be accounted for in a valuation. Additionally, commercial payors typically reimburse at rates equal to or higher than Medicare. For valuation purposes, the assumed commercial payor rates should be theoretically achievable by any hypothetical market participant. The reimbursement rate for a given service will depend on many factors, including the location of the provider, local market dynamics, and changes in federal and state healthcare regulations.

Operating Expenses

Imaging HOPDs are typically accounted for as distinct operating units within the internal framework of the hospital. In many instances, the hospital will track certain elements of the cost structure to operate the unit, but detailed operating expenses are not available. The operating expenses accounted for may include costs that are simply allocated to the unit from the overall hospital operations and may not represent the true operating expenses needed to fully run the business. Additionally, the operating expenses that are reported internally may simply represent the direct costs that are easily identified and would not include the full picture. For instance, the internal financial statements for an HOPD typically do not include certain expenses such as facility rent, utilities, janitorial, and administrative functions such as billing and collection services, legal services, etc. In these situations, it is important to remember the intention of the valuation analysis is to simulate the business as if it were operating on a freestanding basis. Accordingly, the valuation will likely include adjustments to the operating expense profile to match the projected net revenues and volumes. In many cases, this will include a full build-up of operating expenses to include all applicable staff salaries and wages, benefits, occupancy costs, supplies, etc. This may be an iterative exercise that could include input from both the appraiser and the hospital to be certain the appropriate operating expenses are fully accounted for and are consistent with both industry and local market dynamics.

Equipment

When valuing an imaging HOPD, it is critical to account for the equipment needed to provide the projected volumes and net revenues. This equipment includes the imaging machines, computers, and software required to perform the imaging procedures. Depending on the structure of the imaging HOPD, certain pieces of equipment may be utilized to service both the outpatient and inpatient volumes of the hospital. In this case, the hospital may choose to retain the equipment and not contribute it as part of the potential transaction since it will continue to provide services at the hospital even after the properly identified outpatient volume is transitioned out of the HOPD. If the hospital chooses to retain the equipment or certain pieces of equipment, it is essential for the valuation to make a deduction to account for the equipment not being contributed. In addition, this dynamic has both operating and transaction implications since the freestanding imaging center will either need to be able to service the projected volumes with existing equipment or it will need to adequately plan for the capital purchase to acquire the additional equipment.

In summary, outpatient imaging joint ventures have been common in recent years with many hospitals and health systems considering the contribution of their HOPD imaging operations. With the continued focus of patients on convenience and their desire to utilize lower-cost options, it is expected that this type of transaction will continue to be a consideration for hospitals and health systems in the future.

Strategic Options to Strengthen Cardiovascular Medical Group Affiliations

March 30, 2023

Written by Clinton Flume, CVA, Cordell J. Mack, Tim Spadaro, CFA, CPA/ABV, Christopher Tracanna, Colin McDermott, CFA, CPA/ABV

The following article was published byVMG Health’s Physician Practice Affinity Group

Cardiovascular disease ranks as the leading cause of death in the United States, so it should come as no surprise that healthcare executives are placing an increasing emphasis on the stability and growth of cardiovascular services. In addition to the aging U.S. population, management is being forced to take strategic action due to industry factors such as shifting physician employment trends, patient procedures transitioning to lower-cost outpatient care settings, and payor models changing from fee-for-service to value-based care. To ensure continuity of alignment for cardiology providers and stakeholders, executives need to consider the strategic impact of cardiovascular medical group affiliations in their decisions. These decisions include investment in comprehensive cardiac care services, external affiliation models (joint ventures or joint operating agreements), and alignment models with private equity.

Employment Trends

According to the Physician Advocacy Institute, as of January 2022 approximately 67.3% of cardiologists were employed by hospitals or health systems, 17.9% were employed by other corporate entities, and the remaining 14.8% were in independent practices. The combined hospital/health system and corporate entity employment (85.2%) was 12.2% higher than the number of cardiologists (73.0%) employed by these entities in January 2019 [1]. Due to the high concentration of employment for cardiology, this specialty has been insulated from the traditional roll-up activity seen in the orthopedic, gastroenterology, and ophthalmology spaces. This suggests the industry is primed for a reversal of employment back to private practice as providers look for ways to diversify from legacy employment models and engage in outside investment opportunities, such as private practices and surgical centers.

Shift to Outpatient

Health systems, payors, providers, and, most importantly, patients are increasingly seeking high-quality and lower-cost options for routine cardiovascular care. Outpatient cardiology services began to see a transition to the outpatient setting in 2016 when the Centers for Medicare and Medicaid Services (CMS) approved pacemaker implants for the ambulatory surgery center (ASC) covered procedure list (CPL) [2]. In the 2019 Final Rule, CMS added 17 cardiac catheterization procedures to the ASC CPL, and in the 2020 Final Rule, CMS allowed physicians to begin performing six additional minimally invasive procedures (percutaneous coronary interventions) in ASCs. Additionally, several states have followed CMS’ lead by removing barriers to accessing cardiovascular care in ASCs [3]. The continued approval of procedures to the CPL and expanded access to care are major catalysts for the shift in cardiology services to the outpatient setting and the desire of providers to engage in external clinical investment opportunities.

Reimbursement and Payor Impacts

Cardiologists have long sought refuge from rising costs and downward reimbursement pressure by aligning with larger entities that have more leverage and pricing power. This often materialized through traditional health system employment with many hospital providers looking to operate traditional in-office ancillaries in an adjunct hospital outpatient department. The arbitrage in reimbursement (HOPD versus freestanding) was an offset to the ever-increasing physician compensation inflation. However, challenges continue to mount.

The Medicare Physician Fee Schedule (MPFS) conversion factor has fallen year-over-year since CY 2020. On November 1, 2022, CMS released the 2023 MPFS which continued to lower the conversion factor and resulted in cardiology reimbursement falling an estimated 1.0% [4]. During the same period, many health systems are reporting larger net professional losses per cardiologist as costs continue to rise faster than revenue.

These factors, coupled with bundled pricing initiatives and trends focused on value-based care initiatives, are compelling cardiologists to consider all alternative employment scenarios in response to slowing compensation growth. Whether cardiologists continue to be employed by health systems and corporate entities or they venture into private settings to explore outside investment opportunities, there is no doubt cardiology will continue to face financial pressure from rising operating costs in tandem with reimbursement cuts.

Cardiology employment trends, increasing access to outpatient cardiology services, and changes in payor models are all leading indicators that impact the strategic alignment of cardiology medical groups. The following are key external and internal drivers that serve as signals of the fragmentation of the cardiology market. Healthcare executives should be proactive in their evaluation of these market factors which can dictate how cardiology coverage is delivered and can impact current and future affiliations.

Physician Alignment

Degree to which cardiology services are provided by independent cardiologists, employed providers, or a group professional services agreement.

High Impact – To determine the top-line revenue impact between two parties’ contracts.

Entrepreneurial Leadership

The presence of forward-thinking medical leadership.

High Impact – Visionary leadership required to change the market status quo, and generally visionary leaders see today’s disruption (rate pressure, ambulatory migration, etc.) as opportunity.

Economic Sustainability

Degree to which current employed or contracted cardiology economics remains financially viable.

High Impact – Health system alignment can result in inflated market compensation and greater economic burdens for healthcare organizations. The higher the degree of financial unsustainability, the higher the likelihood of stakeholders (health systems, payors, and providers) are open to alternative structures.

Physician Contracts

Degree to which physicians are subject to a noncompete or other similar provisions.

Medium Impact – This may delay fragmentation, but ultimately a large cadre of cardiologists seeking an alternative care model will likely prevail.

Payor Fragmentation

Depth of managed care and commercial contract consolidation.

Medium Impact – The more consolidated the managed care community is in a market, the stronger the likelihood of evolving lower total-cost care models.

Upon evaluation of the internal and external environment, health systems have strategic options that range from staying the course with minimal change through employment to proactively migrating the cardiology care delivery model in partnership with a private equity-backed platform. Below are strategic opportunities for organizations to consider when developing long-term cardiovascular medical group affiliations.

Investment in a Comprehensive Cardiac Institute

Service line realization that the tertiary nature of cardiology requires continued hospital/health system investment in integrated and differentiated clinical programs.

Enhanced service offerings, improved governance (including physician participation), and the development of cardiac operations focused on retaining and attracting community and practicing physicians.

If successful in the implementation of a cardiovascular institute, the likelihood of third-party competitive investment is diminished.

Joint Venture Management Services Organization (MSO) Model

Migration of employed physician practice to an alternative, independent practice structure. This could be a health system-endorsed response depending on current practice economics.

Migration of in-office ancillaries (nuclear, echocardiography, stress testing, etc.) to support primary cardiology services.

Development of a joint venture MSO model owned by physicians and health systems.

Separate ASC joint venture syndication with community cardiologists.

Partnership with Private Equity

Migrate physician practice to private equity and incorporate an income-less expense model for provider compensation.

Make it optional for health systems or stakeholders to be in the capitalization table of supporting practice MSOs. While most PE sponsors may question a role for health system involvement, a regional sub-MSO could at a minimum create value leveraged by the health system’s competitive position.

A comprehensive joint venture ASC strategy with three-way ownership (health system, private equity, and cardiologists).

Staying the Course

The existing environment affords continued incremental strategic investment and limited overall repositioning.

A high likelihood that self-assessment results in limited exposure to fragmentation.

As healthcare executives evaluate the overall strategic positioning of cardiovascular services, industry factors such as physician employment trends, a shift to lower-cost outpatient care, and changing payor models will continue to change the cardiovascular landscape. Mindful executives with a strong pulse on external and internal factors, such as physician alignment and service line stability, will have an advantage in tactical decision-making. Position opportunities, such as investment in comprehensive cardiac institutes, joint ventures with MSOs, and partnerships with private equity firms, are all potential models for long-term strategic success.

Sources

Physicians Advocacy Institute Research & Avalere Health. (June 2022). Physician Employment and Acquisitions of Physician Practices 2019-2021 Specialties Edition. Physicians Advocacy Institute.

Significant Insights from the Doximity & Curative 2023 Physician Compensation Report

March 24, 2023

Written by Caroline Dean, CVA

Doximity, Inc., an online networking and news website for medical professionals, has published its 2023 Physician Compensation Report (Doximity Report)1, with the survey results noting a number of important trends and challenges related to physician compensation in the United States. According to the Doximity Report, which included responses from over 190,000 U.S. doctors over six years and over 31,000 within the last year, there has been a 2.4% decline in average pay for doctors in 2022 compared to a 3.8% increase in 2021. Furthermore, the physician market continues to see a gender pay disparity with males earning almost $110,000 more annually than female equivalents. Aside from compensation trends, nationwide economic strains and expanding physician shortages have led to increasing rates of reported work-related burnout.

Utilizing data from a wide range of medical specialties, employment types, and locations, the survey is a valuable tool to aid in understanding diverse factors impacting healthcare and medical professionals today. The following paragraphs dive deeper into some of the significant insights contained in the Doximity Report.

Compensation Trends

While 2021 data saw a slight increase in compensation across all specialties, 2022 data showed physician compensation remained relatively flat or saw a slight decrease for many specialties. The top three specialties that reported the largest increases were emergency medicine (6.2%), pediatric infectious disease (4.9%), and pediatric rheumatology (4.2%). This is likely a result of the increased demand for these specialties due to lingering waves of COVID-19 and rising respiratory syncytial virus (RSV) cases amongst children. In addition, the Doximity Report notes compensation growth varied by employment setting. Specifically, after controlling for specialty, those employed with a single or multiple specialty group reported a 0.7% decrease in compensation growth, whereas those employed with a solo practice or health system reported a 3.0% and 1.4% increase in compensation growth respectively. A factor that could further impact this slight downward trend in 2023 is the 2% cut in Medicare payments which may have a greater impact on small private practices without the facility charges to supplement a decrease in professional payments.

The Doximity Report continues to demonstrate a significant compensation gap amongst male and female physicians. However, the 2022 compensation data indicated a slight decrease in the gender pay gap from a 28% disparity in 2021 to a 26% disparity in 2022. The top three specialties with the largest pay gaps include oral and maxillofacial surgery, pediatric pulmonology, and allergy and immunology. The top three specialties indicating the smallest pay gaps include nuclear medicine, pediatric cardiology, and pediatric gastroenterology.

Physician Demand & Burnout

With an aging U.S. population, the demand for physicians continued to grow in 2022. The highest in-demand specialties reported were in the realm of primary care with the top five specialties including family medicine, psychiatry, internal medicine, emergency medicine, and child and adolescent psychiatry. Psychiatry moved into two of the top five spots in 2022. Even before the COVID-19 pandemic increased rates of anxiety and depression there was a shortage of psychiatry physicians, and this deficit is expected to worsen.2

Contributing to the physician shortages are increased levels of work-related burnout. A Doximity survey of over 2,000 physicians found that 86% of respondents reported feeling overworked and 66.7% reported considering an employment change. In addition, the Doximity Report found that female physicians reported more overwork than their male counterparts. Burnout could also impact physician compensation trends as 71% of survey respondents reported they would be willing to accept or have already accepted, lower compensation in exchange for greater autonomy and work-life balance, and that percentage is closer to 80% in female physicians.

Economic Factors

Despite growing levels of work-related burnout, economic factors such as inflation and Medicare payment cuts could potentially counteract any trends toward lower-paying roles. The Doximity Report notes that approximately 47% of respondents indicated they are likely to compensate for economic factors by pursuing additional income streams, increasing patient caseloads, or working additional hours. In addition, 62% of survey data respondents said they have a noncompete clause in their employment contracts that prevents them from earning additional income through side jobs. However, with the Federal Trade Commission proposing a rule to ban noncompete clauses, there may be a growing movement of physicians seeking locum tenens or telehealth arrangements outside of their full-time employer.

Conclusion

The Doximity Report detailed a variety of challenges facing the healthcare market over the last year and into the future. Economic strain, increased levels of burnout, and an ever-growing physician shortage will continue to be issues. As a result, physicians are expected to pursue alignment opportunities with both private equity firms and health systems to shield themselves from some of these issues. However, achieving alignment while also having competitive compensation will be difficult due to the negative reimbursement pressures and maintaining compliance with the various laws and regulations surrounding physician compensation. VMG Health experts are available to assist with these challenges by helping to ensure physician practice alignment and that the compensation is consistent with fair market value.

Academic Medical Center Growth & Strategic Opportunities

March 13, 2023

By: John Meindl, CFA

Academic Medical Centers (AMCs) are facing unique challenges and opportunities in the current environment. With healthcare systems becoming more complex and dynamic, AMCs are adapting their strategies to preserve their inherent strengths and capitalize on evolving industry dynamics. One of the main challenges facing AMCs is the shortage of physicians, which is predicted to become more acute in the coming years. At the same time, revenue from higher-margin care is eroding as new businesses are capturing market share. As AMCs play an outsized role in solving labor shortages, they have also been forced to adapt to the financial pressures. Here we examine some of the major financial and strategic opportunities available to AMCs.

1.) Academic Medical Center Partnerships

Many successful academic medical centers have adopted a hub-and-spoke model where the AMC serves as the hub and partners with community hospitals, medical complexes, for-profit hospitals, and pure-play service providers as the spokes. This model can improve care coordination to the appropriate site of care while expanding the population basis to support the growth or addition of specialty service lines.

AMCs entering new partnerships are doing so from a position of strength. Typical AMCs have a unique ability to effectively deliver highly complex care. Additionally, most AMCs have a strong and trusted brand in the communities they serve. However, access has long been a traditional weakness with patients struggling to access AMC facilities promptly. To address the access issue while capitalizing on strengths, AMCs are rethinking their approach to partnerships to provide easier channels for reaching their patients. Access to a more diverse population improves patient experiences, lowers cost structures, and provides revenue opportunities. Successful AMC partnerships may even end up being site-of-care agnostic, achieving the most optimum clinical outcomes while compensating all parties for their respective contributions.

However, partnering with non-academic medical centers poses some challenges. AMCs need to ensure that their partners provide the same quality of care and adhere to best practices, while also maintaining the AMC’s own high standards.

2.) Go At It Alone

Well-capitalized AMCs can invest individually in ancillary services to access additional revenue streams and expand their patient base. The right mix of ancillary service lines allow an AMC to expand its footprint, improve clinical offerings, and generate incremental revenue. AMC’s investing in ancillary service lines should consider whether or not to allow the ancillary to use the AMC’s brand name. As outlined below, AMCs typically have a trusted and strong brand name built on a history of excellence. Allowing the ancillary to use the brand can either 1) enhance the volume of ancillary services, 2) dilute the AMC brand name, or 3) a mix of both. Common ancillary services may include ASCs, imaging centers, urgent care, and other retail facilities.

3.) Co-Branding

As mentioned above, AMCs often maintain a strong reputation and brand name. This intellectual property reflects valuable consumer trust built on a history of clinical excellence. With the right strategic partner, AMCs can capitalize on their individual brand to become market makers through brand licensing, co-branding agreements, care network subscriptions, or external affiliations.

Conclusion

By building hub and spoke partnerships with community hospitals and medical complexes, academic medical centers can leverage their inherent strengths to maintain their industry reputation for excellence. AMCs that prefer an individualized approach may choose to invest directly in ancillary services or develop branding or affiliation agreements in order to generate additional revenue streams and expand patient access.

Hospice Medical Directors: Compliance Considerations

February 1, 2023

Written by Britt Martin, CFA

The hospice market continues to grow, and medical directors have always held a prominent role in compliance and operations. The Centers for Medicare and Medicaid Services (CMS) regularly revise existing hospice regulations governing coverage and payment for hospice care under the Medicare programs and continue to identify hospice medical directors as a key component. As a result, understanding guidance around this role is critical for both compliance and business operations. Further, CMS typically places more investigative resources in places where there is growth.

Growth in the Hospice Sector

As baby boomers, the second largest age group in America, begin to reach retirement age the healthcare industry is planning the best way to serve this population across all healthcare services. Most notably, long-term care and hospice care are both poised to see the most significant impact of the baby boomers’ toll on America’s already overburdened healthcare infrastructure.

To keep up with this emerging and anticipated demand the number of hospice agencies has grown significantly. Per the VMG Health 2022 Healthcare M&A Report, the number of hospice agencies increased 3.8% annually from 3,498 in 2010 to 5,058 in 2020. This increase was primarily attributable to growth in for-profit hospice providers. In certain states like California, government organizations have noted that the number of newly licensed providers does not correlate with community needs and can potentially create an incentive for fraudulent practices. [1]

Compliance Guidance

The Department of Health and Human Services Office of Inspector General (OIG) has published numerous warnings and reports since 1995 highlighting hospice fraud and abuse. In 2021, the OIG noted hospice as a top area for criminal recoveries. [2] Beginning in 2023, an audit of hospice eligibility will be conducted by the OIG. The audit will focus on patients who did not have hospitalization, or an emergency department visit prior to electing hospice. [1] A focus on compliance processes is crucial for hospice providers to successfully navigate this increased scrutiny.

A key component of a compliant hospice program is the oversight of a qualified medical director. Per government regulations, all hospices must designate a physician to serve as the medical director of the hospice. [3] The duties of a hospice medical director generally include:

Oversight of hospice clinical services at the facility.

Developing a plan of care for each patient.

Certification of Terminal Illness (CTI) that is recertified every 90 days.

Acting as a resource to hospice staff, patients, family members, and attending physicians regarding pain and symptom control measures.

Monitoring quality control measures.

Develop clinical protocols and patient care policies.

Fair Market Value Tips

Due to the potential ability of the medical director to refer patients to the hospice programs they might oversee, the compensation paid by the hospice program to the medical director must be set at fair market value (FMV). Obtaining a third-party fair market value opinion and understanding the appropriate interpretation of the fair market value compensation is key in structuring a compliant medical director arrangement.

Key Considerations for a Fair Market Value Analysis of a Hospice Medical Directorship

Specialty – Pay close attention to the medical specialty survey data selected. If the medical director is an orthopedic surgeon, but the hospice medical director’s duties do not require that level of medical specialty, then this medical specialty selection may be incorrect for the determination of hospice medical director compensation.

Limitations in Specialty Survey Data – The surveys utilized may categorize hospice medical directorship compensation under a separate specialty if the majority of a respondent’s work is in another specialty. For example, a family medicine physician who spends most of their time in family practice but also provides hospice medical director services may have the compensation categorized under the family medicine medical director dataset. An understanding of the survey and how it interprets the respondent’s information is key.

Percentile of Survey Data – Another key consideration in a fair market value analysis is what percentile to select or what indication to select within the fair market value range provided. Higher percentiles of compensation may be warranted for medical directors with more administrative experience or other credentials that might benefit the quality of care provided at the hospice (certified hospice medical director, etc.).

The role of the hospice program will continue to become a more prominent component of healthcare continuity of care. Also, with the increased prominence there will be increased scrutiny of the government to ensure compliant programs.