CY 2023 Medicare OPPS and ASC Payment System Final Rule

Rachel Linch

December 6, 2022

Written by Jack Hawkins, Ryan Mendez, and Colin Park, CPA/ABV, ASA

The following article was published by Becker’s ASC Review

2022 saw a continuation of 2021 trends as the healthcare industry further rebounded from the coronavirus (COVID-19) pandemic. The Ambulatory Surgery Center (ASC) subindustry largely recovered in 2021, but certain specialties that lagged in 2021 saw a further recovery in 2022. The ASC industry continued to consolidate throughout 2022 despite not having the major platform-level transactions that were observed in 2021. There were trends that started pre-pandemic that continued to be observed in 2022 such as the shift of higher-acuity procedures from the inpatient setting to the outpatient setting, consolidation of ASCs by management companies, and a push by hospitals to grow their ambulatory footprint with a particular focus on the outpatient setting.

Along with these recurring trends, the subindustry was impacted by macroeconomic trends related to upward pressure on labor, supply, and general costs resulting from a tight labor market and elevated inflationary pressures. The continued trend of increased Medicare reimbursement rates saw its largest escalation ever as a direct result of these pressures.

In March 2020, the world was impacted by the spread of the COVID-19 pandemic, and subsequently, 2021 was a year of rebuilding and recovering from the lasting effects brought on by the pandemic. ASCs in 2021 had an increase in case volumes across almost all specialties. This was primarily due to patients who were willing to resume elective procedures that were postponed and centers that kept their doors open.

In 2022, ASCs saw case volume return to pre-pandemic levels or experienced continued growth if they had not already experienced a return to normal operations. Specialties that were hit especially hard by COVID-19, such as ENT, returned to pre-COVID levels in 2022 as schools and school activities returned to pre-pandemic normalcy. In 2022, the impact of the pandemic on ASCs was less related to revenue and more related to expenses. The lingering effects of COVID-19 were related to the shortage of healthcare workers and the supply chain issues that continued to pressure the profitability of surgery centers. Looking into 2023, controlling labor and supply costs will be a point of focus for ASCs.

The trend of higher-acuity procedures shifting from an inpatient or HOPD setting to a freestanding ASC setting continued throughout 2022. In 2022, specialties that increased their footprint in ASCs included cardiology, orthopedics, and higher-acuity spine procedures. According to data from the ASC Association, orthopedics was the most common specialty serviced by ASCs in 2022.

Director of ASC Operations at Virtua Health Catherine Retzbach said ASCs that perform these high acuity cases “offer patients more options to have procedures be performed in a high-quality, low-cost environment.” Furthermore, according to the most recent Ambulatory Surgery Center report published by Research and Markets, ASCs are projected to perform half of all cardiology procedures by the mid to late 2020s.

The ASC subindustry continues to focus on higher-acuity specialties when considering both organic growth and M&A opportunities. President of Tenet Saum Sutaria noted the continued focus of the ASC business toward higher-acuity service lines in the company’s Q3 2022 earnings call. Tenet is the parent company of USPI and is the largest outpatient surgery center operator in the United States. The company reported that these procedures made up 20% of USPI’s year-to-date volume due to growth in their orthopedic and spine business. Sutaria further said “the [USPI] team is focused on organic growth, [and] increase in higher-acuity services and M&A.” These insights highlight the ASC subindustry’s focus on higher-acuity service lines, and indicate the shift towards ASCs for these types of procedures is likely to continue in the future.

In 2022, we saw the continued expansion of a prominent large-level ASC platform player highlighted by the finalization of a large platform-level transaction that began in 2020. In addition, there were a significant number of transactions at the individual-facility level. Consistent with the observed larger platform-level transaction, the fragmented ASC industry has continued to consolidate. It is worth noting that although the industry continues to consolidate approximately 70% of ASC facilities remain independent as of 2022. This leaves room for further consolidation at the individual-facility level.

In 2020, Tenet Health finalized a deal for $1.1 billion to acquire 45 ASCs from SurgCenter Development. This was the first stage of a multi-part acquisition, and in Q4 of 2021, USPI entered a $1.2 billion deal to acquire SurgCenter Development’s remaining centers and established a long-term development deal. The transaction included acquiring ownership interest in an additional 92 ambulatory surgery centers, other support services in 21 states, and providing continuity for future de novo development projects. In 2022, USPI made substantial strides in consolidating the 92 ASCs it acquired from SurgCenter Development. This process is expected to continue into 2023 as the centers are further consolidated. The acquisition has enabled Tenet and USPI to expand their footprint and solidify their position as a leader in the ambulatory surgery center market.

“There’s anticipated additional synergies related to the SCD transactions that will continue to grow as we move through next year as well. And the other thing is the M&A activity that USPI will execute on. The pipeline is robust.”

-Dan Cancelmi, Chief Financial Officer

On June 21, 2022, USPI and United Urology Group formed a joint venture partnership in 22 ASCs. USPI acquired a portion of United Urology Group’s ownership interests in ASCs located in Maryland, Colorado, and Arizona. The ASCs will be owned and operated by the joint venture, and USPI will provide management and support services to the ASCs. The transaction closed in the third quarter. In February 2022 The Rise Fund, an impact investing strategy managed by TPG, announced the acquisition of Blue Cloud Pediatric Surgery Centers which is the largest operator of pediatric dental ASCs in the United States. TPG Rise is a large impact investing platform with more than $13 billion in assets across its various funds, including The Rise Funds, TPG Rise Climate, and the Evercare Health Fund.

On December 9, 2022, Michigan-based Sparrow Health System and Michigan Medicine, formerly the University of Michigan Health System, announced an $800 million partnership. Michigan Medicine will invest $800 million into the expansion of Sparrow’s ASC and neonatal care unit.

In April 2022, UnitedHealth Group’s Optum announced the purchase of Kelsey-Seybold, a Houston-based physician group for $2 billion. The acquisition expanded Optum’s presence in the primary care market. As part of this acquisition, Optum gained two ASCs that were owned by Kelsey-Seybold.

Finally, on May 3, 2022, Surgery Partners and ValueHealth announced a partnership that aims to construct new ASCs and implement ValueHealth’s value-based surgical programs at Surgery Partners’ existing and upcoming locations. Additionally, Surgery Partners will manage and take over ValueHealth’s stake in three current ASCs and four centers that are in the development phase.

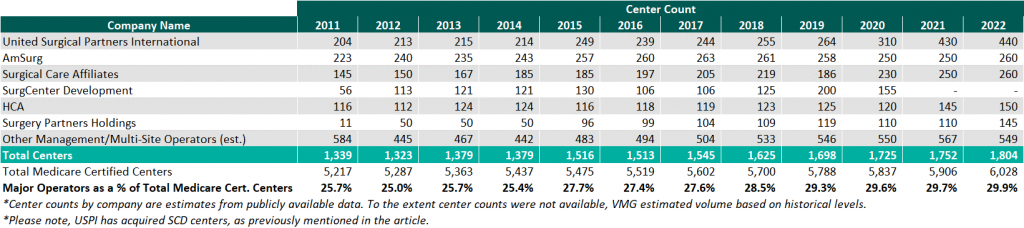

As of December 31, 2022, the largest operators (in terms of the number of ASCs) are United Surgical Partners International (USPI), Envision Healthcare/Amsurg Corporation, and Surgical Care Affiliates (SCA), with ownership of approximately 440+, 260+, and 260+ ASCs, respectively.

As noted in the chart below, the number of total centers under partnership by a national operator, as a percentage of total Medicare-certified centers, saw an increase from 2021 to 2022 growing from approximately 1,752 centers to 1,804 centers. Additionally, the top five management companies have increased the number of centers under management by approximately 511 centers since 2011 which represents a compound annual growth rate of 5.37%. As management companies have increased in size they are able to increasingly provide a greater level of strategic value by bringing greater leverage with commercial payors, enhanced management and reporting capabilities, and improved efficiency related to staffing, supplies procurement, and other general and administrative expenses.

On November 2, 2021, the Medicare reimbursement fee schedule for ASCs in 2022 was finalized by the Centers for Medicare & Medicaid Services (CMS). Consistent with previous years for CYs 2019 through 2023, CMS will update the ASC payment system using the hospital market basket update instead of the Consumer Price Index for All Urban Consumers (CPI-U). CMS published the 2021 ASC payment final rule which resulted in overall expected growth in payments equal to 2.0% in CY 2022. This increase is determined based on a hospital market basket percentage increase of 2.7% less the multifactor productivity (MFP) reduction of 0.7% mandated by the ACA.

Moreover, the ASC payment final rule for CY 2023 was released by CMS on November 1, 2022, and resulted in overall expected growth in payments equal to 3.8% in CY 2023. This increase is determined based on a projected inflation rate of 4.1% less the MFP reduction of 0.3% mandated by the ACA. The 3.8% growth in payments represents the largest increase in projected payments year over year and is a direct result of the increase in labor, supplies, and other cost pressures seen over the last year. Although the industry recognizes the increase in payments as a win, many major players believe the increase was insufficient given the extraordinary cost pressures hospitals and ASCs are facing. The way ASCs navigate the dynamic macroeconomic environment currently in place will be a major point of interest over the coming years.

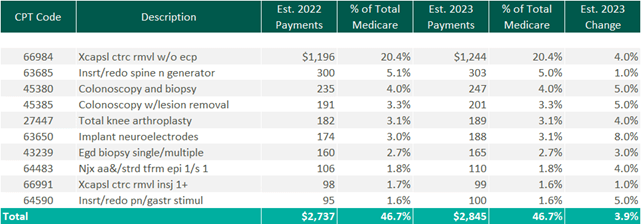

The table below reflects a summary of the estimated Medicare ASC payments for 2022 and 2023 for the top 10 CPT codes performed in ASCs in 2022. As noted below, the observed 2022 payments by Medicare for the top 10 CPT codes are projected to increase by 3.9% through the estimated 2023 payments.

CMS has implemented a new policy that will provide complexity adjustments for certain ASC procedures in CY 2023. These adjustments will be applied to combinations of primary procedures and add-on codes deemed eligible under the hospital outpatient prospective payment system (OPPS). In the past, add-on codes did not receive additional reimbursement when bundled with primary codes. However, with this new policy Medicare will provide adjustments to the payment rate for certain primary procedures to account for the additional cost of performing specific add-on services.

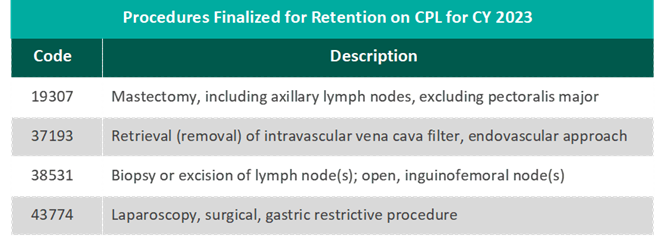

CMS considered 64 recommendations for new procedures to be added to the ASC CPL for CY 2023. After reviewing the clinical characteristics of these procedures, four were chosen to be added to the CPL for the upcoming year. These procedures are typically performed in outpatient settings and have little to no inpatient admissions. The four procedures are outlined in the table below. However, the addition of only four codes resulted in pushback and a continued desire for additional procedures to be added to the CPL that is being performed safely and successfully by ASCs.

“CMS’s decision to add only four new procedures to the ASC-CPL for 2023 after ASCA proposed 47 procedures that ASCs are performing safely and successfully for privately insured patients is a serious mistake and denies beneficiary access to high-value care. Forcing otherwise healthy Medicare beneficiaries to receive care in higher-cost settings for these procedures needlessly increases costs to the Medicare program and undercuts Medicare’s mission of serving as a responsible steward of public funds.”

– Bill Prentice, Chief Executive Officer, ASCA

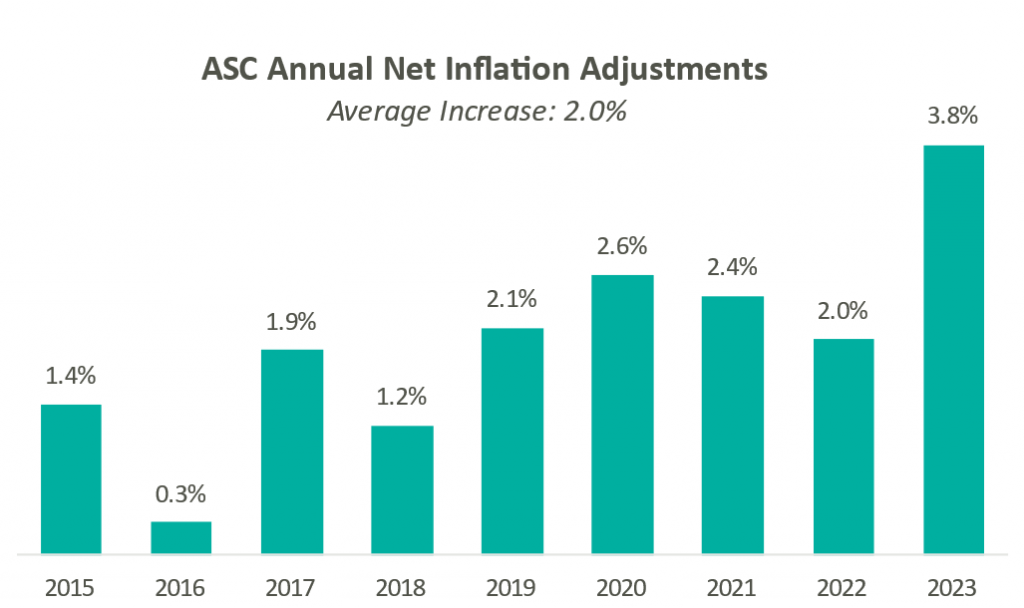

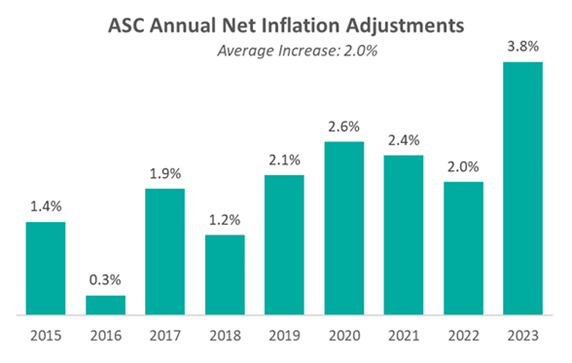

Presented in the chart to the right is a summary of the historical net inflation adjustments for CY 2015 through CY 2023. The annual inflation adjustments are a presented net of additional adjustments, such as the MFP reduction, outlined in the final rule for the respective CY. The CY 2023 inflation adjustment is nearly double the increase we have observed in each of the last eight years and is largely driven by labor and supply cost pressures.

Overall, the final ruling to increase ASC payments by CMS and the increased recovery from COVID-19 both indicate an expected increase in total ASC payments. Ultimately, CMS has projected total ASC payments in 2023 to increase by approximately $230 million from 2022 payments to approximately $5.3 billion.

In conclusion, 2022 was a year of growth throughout the ASC industry and a year of continued recovery from the effects of the pandemic. Key trends to look for going forward are the effects of increased cost pressures impacting the healthcare industry as a whole, and specifically how ASCs respond. Expectations for 2023 are continued growth and consolidation in this sub-industry. The ASC setting provides a convenient, cost-effective way for patients to receive high-quality care. The continued shift of higher-acuity procedures to the outpatient setting should give optimism to the success of the subindustry as a whole as long as cost pressures are mitigated properly. Overall, ASCs at the center level are expected to continue the positive momentum that persisted in 2022 and the subindustry is expected to see the level of transactions increase through 2023.

Written by Anthony Domanico, CVA

As a strategy consultant focusing on the physician enterprise, and more specifically on physician compensation design, one question I frequently get asked is how to develop a strategic plan for managing physician and advanced practice provider (APP) compensation. Specifically, organizations look for guidance on how often they should be rebasing and/or recalibrating their compensation plans to ensure their compensation program remains competitive and contemporary.

When answering this question, I often advise clients to follow the “1-3-5 Rule.” Here is a breakdown of the rule and what each component means:

To ensure your compensation program remains market competitive, it is important to rebase your salary, productivity, and other compensation rates on an annual basis. Many organizations choose to tie their rates to a target market percentile of the physician compensation and productivity surveys. This subjects their physicians to market-based increases typically in the 2-3% range.

There has been high market volatility in 2022 and it is expected in 2023 due to the COVID-19 pandemic, inflationary growth and cost of living challenges, the 2021 Medicare Physician Fee Schedule, and other factors. Because of this many organizations are adjusting their approach to continue to provide reasonable increases to their physician compensation pool. Regardless of the methodology used, rebasing your compensation levels on an annual basis is essential to ensure your providers’ compensation levels keep up with the market and avoid potential retention issues.

After going through a compensation plan design process, it may be tempting to just “set it and forget it.” After all, a lot of work went into setting levels of base salary, quality, and productivity incentives in the new compensation program. Also, the compensation rebases annually to ensure the total remuneration remains competitive, and surely that should be enough, right?

Not necessarily.

Payor contracts tend to come up for renewal every three years or so. As the industry continues to move from volume to value-based reimbursement, more of an organization’s revenue will be tied to quality and other non-productivity-based outcomes the next time a contract comes up for renewal. Those contract renewals could impact what an organization might do in its provider compensation program.

For example, consider an organization with a compensation model that is 90% base salary, 7.5% wRVU-based productivity, and 2.5% quality. Then, consider that organization’s payor contracts shift such that 80% of revenue is driven through fee for service and 20% through quality and shared savings programs. In that case, the organization should consider shifting those percentages to align its compensation program with its payor contracts.

The healthcare industry is changing with an increased focus on providing high-quality, low-cost care to patients. As this trend continues, new types of compensation programs have emerged to shift the focus away from things like wRVUs and toward panel management and outcomes-based payment arrangements. Over time, as more organizations consider and adopt alternative compensation models, these models will become more mainstream and may make legacy models look a bit antiquated. This can create recruitment and retention challenges for an organization.

About every five years, organizations should evaluate their strategic plans relative to the physician enterprise. This should be done to determine if the compensation structure (e.g., the 90% base, 7.5% wRVU, 2.5% quality model) remains contemporary and competitive with modern physician compensation programs.

When considered in totality, the “1-3-5 Rule” can help organizations better manage their physician compensation and alignment models. In turn, this will ensure the organization is always able to best compete in an increasingly competitive marketplace.

Written by Caroline Dean, CVA and Bartt B. Warner, CVA

The Department of Health and Human Services Office of Inspector General (OIG) published Advisory Opinion No. 22-20 (Advisory Opinion) on December 19, 2022 related to the OIG’s application of its fraud and abuse authorities regarding an arrangement including remuneration to referral sources in the form of employed nurse practitioners (NPs) to perform services typically performed by attending physicians (Physicians) at no cost to the Physicians.

[1] The Advisory Opinion considers if this type of arrangement may violate the federal Anti-Kickback Statute (AKS) as the provision of NP services at below fair market value could potentially induce referrals from Physicians who take part in the arrangement. The OIG ultimately determined that although the arrangement would be considered remuneration under the AKS, the arrangement included several safeguards that mitigated risk of fraud and abuse. As a result, the OIG has provided crucial insight into how these arrangements are looked at from the government’s perspective and key guardrails that should be followed.

Under the arrangement assessed by the OIG (Arrangement), the hospital utilized its NPs to assist in providing services the Physicians would typically perform including, but not limited to: initiating care plans, implementing care protocols, making rounds, responding to laboratory or imaging studies, arranging follow-up testing, educating and supporting patients and families, overseeing unit-based quality improvement projects, and discharge planning. The hospital certified that all Physicians with privileges in two designated medical units at the hospital were informed of the Arrangement and the volume or value of referrals was not considered when offering participation in the Arrangement. In addition, Physicians taking part in the Arrangement were largely primary care physicians and the hospital certified that it prohibits participating Physicians from billing for the services furnished by the NP.

In reviewing the Arrangement, the OIG noted and reaffirmed that any arrangement involving the provision of free or below-market-value goods or services to referral sources has the potential to violate the AKS. Specifically, the Arrangement allows Physicians to offload services to NPs that would otherwise require their time and attention. This allows the physicians to perform other services reimbursable by federal healthcare programs, potentially increasing the cost to federal health care programs which is one of the key issues the AKS was enacted to avoid. Specifically, the OIG stated:

“Under the Arrangement, services performed by Requestor’s NPs on behalf of any Participating Physician potentially relieve the Participating Physician of a range of tasks and services for which they otherwise would have to expend their time and resources. For example, an NP performing services on behalf of a Participating Physician might save that physician the time and costs associated with having to return to the hospital or taking calls from the hospital to make treatment decisions. These services also might allow Participating Physicians to use the time they would have spent performing these tasks to perform other separately billable services.”

Furthermore, the cost of NPs for the use of physician efficiency is often passed on to the physicians themselves and offering these services to Physicians for free or below market value poses a potential compliance risk as it could be used to induce referrals. The OIG presented what they consider to be a suspect arrangement and offered the following example:

“…for example, hospitals permit their employed NPs to provide services to physicians’ patients at no cost to the physicians, and the physicians then bill payors, including Federal health care programs, for the services performed by these NPs.”

In the Advisory Opinion, the OIG notes several safeguards included in the Arrangement that help to mitigate potential risk of fraud and abuse under the AKS. First, the Physicians participating in the Arrangement were predominantly primary care physicians, not profitable referral sources such as surgical or specialized providers. Also, the arrangement was not aimed at any specific physicians with a history or expectation of higher referral volume.

In addition, the Physicians were not receiving production credit or any additional compensation for services performed by NPs under the Arrangement. To assuage potential quality concerns, all services performed by the NPs were done with communication and collaboration with the Physicians. The Physicians were also required to round daily and maintain ultimate accountability for the patient’s care. The hospital also attested that the availability of NPs to assist with patient care improved the quality of care, speed, and efficiency of treatment. The OIG went on to state the addition of the NPs services “may ensure an appropriate level of care for patients in these units.”

Perhaps the most important guardrail that mitigates risk under the Arrangement is that the hospital does not bill any payors, including federal health care programs, for services performed by the NPs, though these services may be separately reimbursable. As a result, there is likely no increased costs to federal health care programs under the Arrangement.

In conclusion, the OIG determined it would not pursue administrative sanctions against the hospital pursuant to the Arrangement as the required intent to induce referrals under the AKS was not present in the Arrangement. However, even though the OIG noted the Advisory Opinion was limited in applicability to the subject Arrangement, the OIG gave unique insight into suspect arrangements and provided multiple guardrails for employed NP arrangements. A cautious approach should be taken with employed NP arrangements and best practices should always include:

As previously discussed, although advisory opinions only apply to the requestors of the opinion, any arrangement involving remuneration to referral sources should involve careful consideration or involvement of a valuation expert to ensure compliance.

Written by David LaMonte, CFA and Max Swan

On November 1, 2022 the Centers for Medicare & Medicaid Services (CMS) released the calendar year (CY) 2023 Medicare Physician Fee Schedule (MPFS) final rule as well as the Hospital Outpatient Prospective Payment System (HOPPS) final rule with both rules going into effect January 1, 2023.

Reimbursement decreases were seen previously under the MPFS annual rules for radiology in 2021 and 2022 when CMS first began phasing in the plan to reallocate reimbursement to physicians who consistently bill for E&M codes. However, these cuts were mitigated by legislation that increased the conversion factor in 2022 after the final rule was issued. Considering the previous precedent and similar political pressures, many industry participants are hoping for similar legislation in order to mitigate the cuts reflected in the final rule this year.

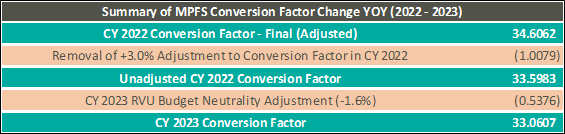

As the chart below illustrates, the CY 2022 Conversion Factor is adjusted to exclude the 3.0% one-time increase allowed by legislation which came after the final rule was issued. Additionally, the CY 2023 conversion factor reflects a reduction of 1.6% related to budget neutrality requirements. As a result, the MPFS Conversion Factor will decrease from 34.6062 in CY 2022 to 33.0607 in CY 2023 reflecting a 4.47% decrease.

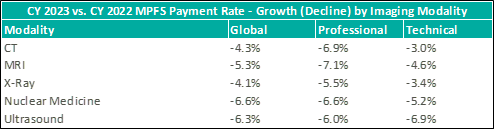

Concerning radiology specifically, the final rule is expected to result in even further decreases in payment rates relative to CY 2022 levels. The table below illustrates changes in global, professional, and technical payment rates for specific modalities based on CMS’ published CPT-level payment data for CY 2022 and CY 2023. In addition to the conversion factor change, imaging and radiology providers have indicated the declines are attributable to changes in how relative value units (RVUs) are determined for several imaging procedures.

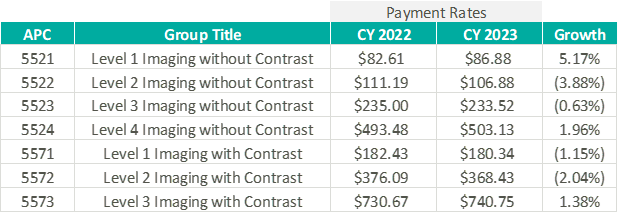

The final HOPPS rule included a 3.8% increase in the conversion factor relative to CY 2022 to reach 85.59 for CY 2023. The conversion factor, which is similar in function to MPFS, impacts all types of outpatient procedures and is updated annually. Below is a chart that outlines payment rates and growth relative to CY 2022 for the seven imaging ambulatory payment classifications (APCs). These APCs are also updated each year with weightings specific to individual procedure types that serve as an indicator of complexity and use of resources.

“With respect to our growth initiatives, we believe the opportunities for continuing consolidation could accelerate as a result of reimbursement pressures.”

– Mark D. Stolper, CFO of RadNet, Q3 2022 Earnings Call discussing the CY 2023 MPFS Final Rule

The reimbursement pressures noted above should continue to drive acquisition activity by larger operators of free-standing diagnostic imaging facilities. This is due to their ability to mitigate the impacts of reimbursement cuts with synergies realized from reduced overhead and other cost-savings that come from their scale and operational expertise. Outright acquisitions of these practices and facilities should continue in the future with the continuing drops in reimbursement under MPFS for most imaging modalities.

“Another one of our significant initiatives is expansion through hospital and health system joint ventures. In the past, we have stated that we see a path forward toward holding as much as 50% of our imaging centers in these partnerships. Most hospitals have been challenged by the loss of patient volumes to outpatient free-standing facilities who offer significantly lower pricing along with better and more convenient patient experience.”

– Howard G. Berger, CEO of RadNet, Q3 2022 Earnings Call

Reimbursement for imaging and radiology services under MPFS has created difficulties for operators for several years now. However, hospitals and hospital outpatient departments (HOPDs) struggle with a different set of problems as it relates to imaging and radiology services. Outpatient imaging volumes at hospitals have steadily declined as patients increasingly migrate to outpatient free-standing facilities due to more favorable costs for the patient. As noted above, larger independent operators of free-standing facilities expect that hospitals and health systems will continue to be targeted for partnership opportunities through joint venture models allowing them to retain some level of control and influence over the patient trajectory.

By: Madi Whyde, Savanna Ganyard, CFA, Jordan Tussy, and Madison Higgins

VMG Health reviewed the earnings calls of publicly traded healthcare operators that reported earnings for the third quarter that ended on September 30, 2022. By focusing on the major players in select subsectors defined below, we analyzed the frequency of certain keywords including inflation, COVID-19, interest rates, premium labor, and others. We used these keywords to identify which topics commanded the room this earnings season. Highlights from the calls are summarized in this article.

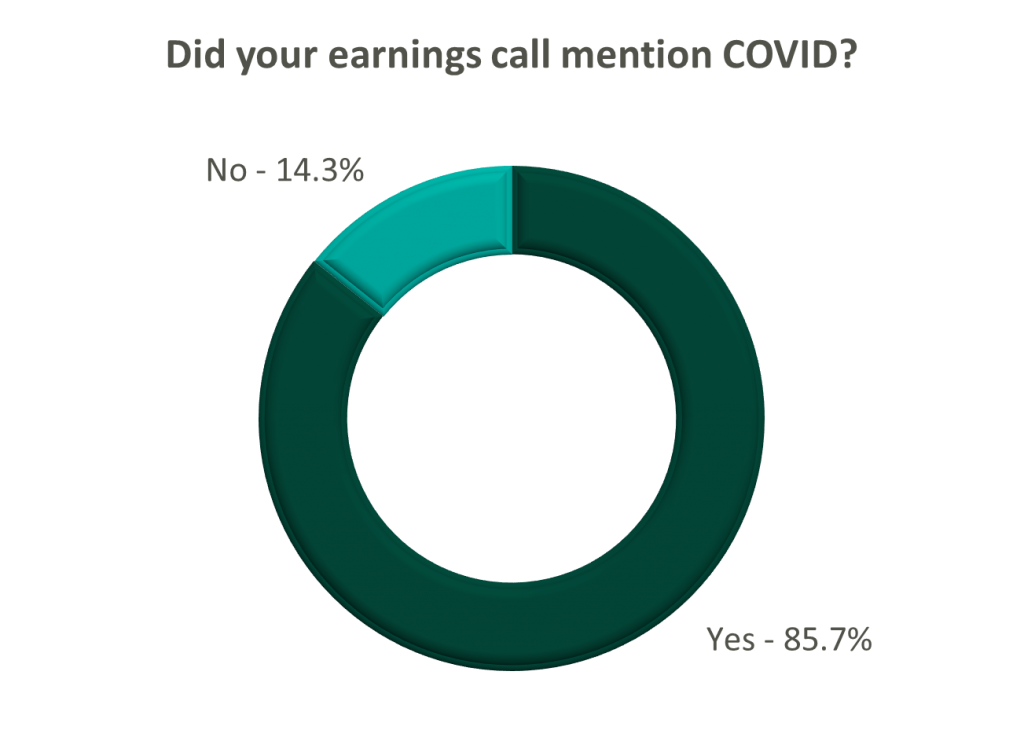

Volume: Although volume trends are unique to each industry sector nearly all operators remained focused on the impacts of COVID.

Poll: Did the earnings call mention COVID-19?

On a same-facility basis, admission volumes declined as much as 5.0% from the comparable prior year quarter (Q3 2021) for acute care hospital operators. Despite the weakening of COVID-19, the decline in volumes was attributed to higher-than-average cancellation rates (THC), the migration of certain procedures to outpatient status (CYH and HCA), and capacity constraints (HCA). Inpatient volumes generally remained at or below pre-pandemic levels.

Ambulatory surgery center (ASC) operators reaped the benefits of the migration to the outpatient setting and reported positive volume trends when compared to Q3 2021. Surgical volumes were reported as consistent with 2019 pre-pandemic levels (THC), and one operator claimed the business did not experience any material direct impact related to COVID-19 during Q3 2022 (SGRY).

The post-acute sector reported mixed results in volume trends. One operator reported a year-over-year decline of 14.0% in hospice admissions, citing capacity constraints and reduced referrals from acute care hospitals (EHAB). However, another operator indicated that increases in admissions in the second half of the third quarter showed growth that they “haven’t experienced since the start of the pandemic” (CHE).

Volume trends among other industry players including dialysis providers, risk-bearing organizations, and physician services were also affected by COVID-19 in Q3 2022. Headwinds in dialysis volumes are expected to persist for the foreseeable future (DVA), and inpatient volumes for risk-bearing organizations remain below pre-pandemic levels (AGL). Notably, AGL also reported a rebound in physician office visits and outpatient volumes were in line with pre-pandemic levels.

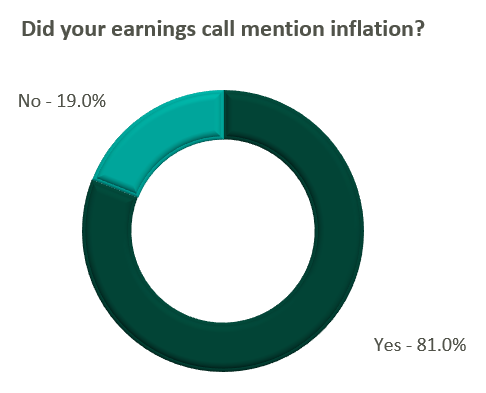

Reimbursement: Declining COVID-19 volumes mean less incremental government revenue for certain industry players who also now contend with an uncertain inflationary environment.

Poll: Did the earnings call mention inflation?

Declining COVID-19 volumes resulted in lower acuity patients and reduced incremental government reimbursement. This softened the reimbursement per admission for the acute care hospital segment. Further exacerbated by inflation, these dynamics were evident in reported EBITDA margins which declined as much as 17.0% (CYH) over Q3 2021. In response, some acute care hospital operators are turning to commercial payor negotiations. Rate increases for the next year are anticipated to range from a minimum of 3.0% (THC) to upwards of 6.0% (CYH).

The post-acute sector did not release specific figures regarding contract rate hikes. However, the sector is optimistically looking for high single-digit rate increases (SEM) to provide relief in the current inflationary environment.

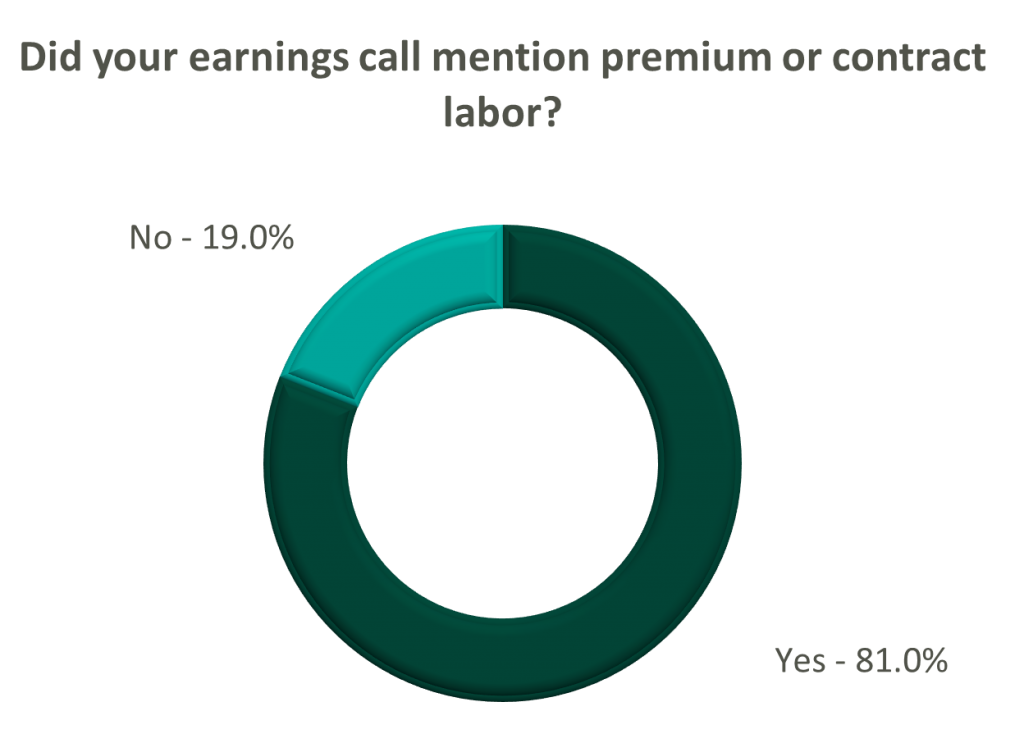

Labor: Unsurprisingly, management teams across the sector were faced with questions about labor trends and management techniques during their earnings calls. Contract labor remained pivotal for the operations of some, but premium labor appears to have softened during the quarter.

Poll: Did the earnings call mention premium or contract labor?

The reliance on contract labor continued its downward trend in Q3 helping moderate expenses. HCA even indicated overall labor costs were stable due to targeted market adjustments. However, contract labor and premium pay remain at uncomfortably high levels for most acute care hospital operators. UHS revealed during their call it will be unlikely to reach pre-pandemic levels in the near future.

Staffing challenges persisted among the post-acute operators and directly impacted volume by as much as 60.0% (AMED). Increased indirect labor costs including orientation, training, and sign-on bonuses were the leading drivers of decreased EBITDA (AMED). Wage inflation, particularly for nursing positions, is expected to rise as much as 5.0% next year (SEM). However, several management teams are optimistic wages will stabilize to historical levels (SEM, EHC) in the near future.

Other industry players, including dialysis and physical therapy providers, also faced challenges with contract labor during the quarter. USPH reported labor costs were approximately 200 basis points higher than Q3 2021 levels, and DVA indicated such costs showed no improvement.

Go Forward Expectations and Guidance: Considering the quarter’s performance, the companies we reviewed were divided relatively evenly in terms of revised FY 2022 revenue guidance, (i.e., raised, lowered, unchanged). In general, the quarter brought about a more pessimistic view of FY 2022 EBITDA, and the majority of public companies lowered their guidance for the year. Further, most stakeholders were left with no guidance for FY 2023.

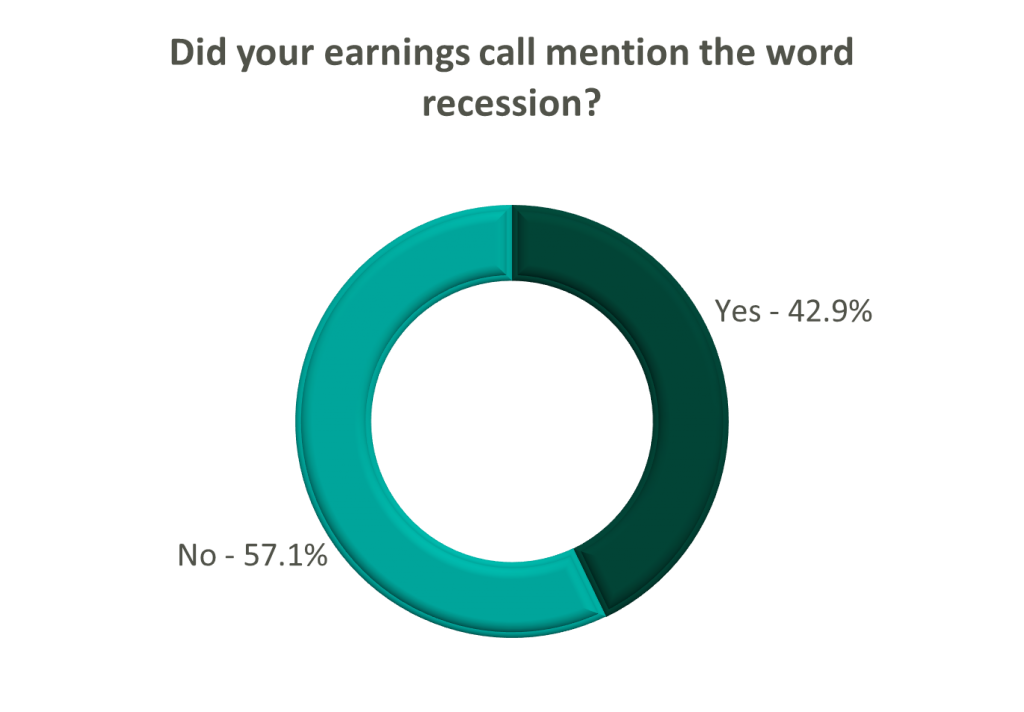

Poll: Did the earnings call mention a recession?

FY 2022 revenue and EBITDA guidance among the acute care hospital operators was generally left unchanged except for THC which lowered EBITDA guidance. However, all companies that were reviewed declined to provide FY 2023 guidance during the call, and primarily cited economic uncertainty (HCA).

The post-acute sector appeared nearly unanimous in the outlook for the rest of 2022, and most operators lowered their revenue and EBITDA guidance. Unsurprisingly, no one offered FY 2023 guidance during the earnings calls.

Interestingly, risk-bearing organizations mostly raised their revenue guidance for FY 2022 (AGL, CMAX, PRVA). However, EBITDA guidance was less predictable and was lowered (AGL, TOI), raised (PRVA), and unchanged (CMAX).

Most other healthcare operators followed similar patterns in terms of providing guidance for FY 2023. Of the companies we reviewed, only DVA revealed an outlook for the next year. The company anticipates revenue to be flat (driven by unfavorable volume trends) and margins to continue to feel the impact of labor market pressures.

Written by James Tekippe, CFA and Carla Zarazua

Key opinion leaders (KOLs) have traditionally served as strategic partners to the pharmaceutical industry. They do so by providing their experience and expertise in the research and development of novel medicines, treatments, and devices in addition to serving as liaisons for the education and promotion of these products. Given their thought leader status, KOLs are frequently engaged by life sciences companies and other healthcare companies in consulting relationships to further specific business goals and initiatives. With the increased scrutiny of the arrangements between these companies and healthcare providers over the past decade, it is more important than ever to understand how to engage with these KOLs in a compliant manner with compensation set at fair market value (FMV).

For the past decade, pharmaceutical and device manufacturers and group purchasing organizations have been required to report any payments and transfers of value to physicians and hospitals under The Physician Payment Sunshine Act. In this instance, the manufacturers and organizations are referred to as “Reporting Entities” by CMS and the physicians and hospitals are referred to as “Covered Recipients.” The purpose of this requirement is part of a push to increase transparency and accountability in the relationships between pharma and KOLs.

CMS has made this information publicly available since 2014 through its “Open Payments” program. This program allows anyone to understand what specific Reporting Entities are paying out to Covered Recipients, and the specific payments and transfers of value Covered Recipients are receiving. In 2018, the Substance Use-Disorder Prevention that Promotes Opioid Recovery and Treatment for Patients and Communities Act, also known as the Support Act, expanded upon the Sunshine Act by requiring Reporting Entities to include certain non-physician providers in the list of Covered Recipients. This list included physician assistants, nurse practitioners, clinical nurse specialists, certified registered nurse anesthetists, anesthesiologist assistants, and certified nurse midwives. The reporting requirements began in 2021, and 2022 has been the first year CMS included data for the expanded list of Covered Recipients.

The expansion of which relationships and transfers of value are required to be reported to CMS and the recent legal settlements with both Reporting Entities and Covered Recipients are indicators of a long-term trend. Due to the scrutiny of these relationships with KOLs and the desire for increased transparency into the payments between Reporting Entities and Covered Recipients, this is going to continue to be with us for the long haul.

To better understand the relationship between KOLs and the life sciences industry, it is important to begin by defining how these healthcare providers differ from their peers. KOLs are distinguished through the experience and expertise they have accumulated in activities that include publishing research, speaking at conferences, acting as investigators or advisors for clinical trials, and aligning themselves with medical societies, among others. This breadth of clinical knowledge can be invaluable to life sciences companies that utilize this expertise to further their own business goals.

The arrangements between life sciences companies and KOLs are often established to utilize a particular KOL’s expertise in various supportive tasks. These tasks include writing abstracts and manuscripts, giving promotional or scientific speeches, supporting an investigational drug’s clinical development, supporting a brand’s promotion, and participating in or leading an advisory board. As KOLs are not inclined to provide these services without compensation, any company engaging with a KOL that either directly or indirectly could refer business to that entity should follow these steps when establishing a compensation arrangement:

The remainder of this article will outline the major factors to consider when going through these steps in KOL arrangements.

The first step any entity should take when establishing a relationship with a KOL is documenting a legitimate business need for the arrangement absent the potential for referrals. In its updated Code of Ethics from 2022, AdvaMed indicated that:

“A legitimate need arises when a Company requires the services of a Health Care Professional to achieve a specific objective, such as the need to train Health Care Professionals on the technical components of safely and effectively using a product; the need for clinical expertise in conducting product research and development; or the need for a physician’s expert judgment on clinical issues associated with a product. Designing or creating an arrangement to generate business or to reward referrals from the contracted Health Care Professional (or anyone affiliated with the Health Care Professional) are not legitimate needs for a consulting arrangement.”

Once a legitimate need has been identified and documented, an arrangement with a KOL should establish at minimum the following in a written document:

These factors should be reviewed periodically to ensure any material changes are reflected in the arrangement and compensation to a KOL.

After establishing a legitimate need and written arrangement, the next step is determining compensation that is consistent with FMV. The Centers for Medicare and Medicaid Services’ (CMS) updated Physician Self-Referral Law (commonly referred to as the Stark Law) provides the following guidance on its definition of FMV:

For general compensation arrangements, FMV is defined as the value in an arm’s length transaction, consistent with the general market value of the subject transaction.

The general market value of compensation in the final rule is defined as: Compensation – with respect to compensation for services, the compensation that would be paid at the time the parties enter into the service arrangement as the result of bona fide bargaining between well-informed parties that are not otherwise in a position to generate business for each other.

Determining FMV rests on various factors specific to a particular arrangement, but there are certain hallmarks of this process to keep in mind which include the following:

Establishing FMV may be viewed as the major hurdle in forming a compliant arrangement, but regulatory authorities may question both the amount of payment and the reasons for this payment. As such, establishing a formalized compliance policy in writing that outlines the various steps taken by a company is a prudent step to safeguard against suspicion and sham arrangements. The steps outlined in the policy will allow for a consistent approach to engaging with physicians and for establishing FMV compensation. In addition to outlining a policy, it is important to appoint compliance personnel to oversee the policy. This includes selecting KOLs and regularly auditing the program. In the “OIG Special Fraud Alert: Speaker Programs” issued November 16, 2020, a potential risk factor noted was the selection of providers being made or influenced by the sales or marketing team. With that said, utilizing compliance personnel over the sales or marketing team will help decrease the risk of fraudulent arrangements.

The scrutiny of arrangements with KOLs only appears to be increasing for the foreseeable future as indicated by the recent OIG special fraud alert and recent court cases relating to these types of arrangements. These arrangements with KOLs can be vital for the research and promotional goals of the pharmaceutical and healthcare industry. Therefore, these relationships do not appear to be going anywhere either. Understanding the regulatory environment and establishing compliance protocols to define the need for these arrangements, with compensation that is consistent with FMV, is vital for companies trying to engage with KOLs in an appropriate manner.

Written by Jack Hawkins and Ryan Mendez

The following article was published by Becker’s Hospital Review.

On November 1, 2022, the Centers for Medicare & Medicaid Services (CMS) released the CY 2023 Hospital Outpatient Prospective Payment System (OPPS) and Ambulatory Surgery Center (ASC) payment system policy changes and payment rates final rule.

Based on the final ruling, CMS will continue to update the ASC payment system using the hospital market basket update rather than the Consumer Price Index for All Urban Consumers (CPI-U) for CYs 2019 through 2023.

As 2023 is slated to be the last year of the trial, CMS indicates in this final rule that the agency intends to “update the public on [its] assessment of service migration and other factors in the CY 2024 OPPS/ASC proposed rule.” The final rule resulted in overall expected growth in payments equal to 3.8% in CY 2023. This increase is determined based on a projected inflation rate of 4.1% less the multifactor productivity (MFP) reduction of 0.3% mandated by the ACA.

“While the AHA is pleased that CMS will provide hospitals and health systems with an improved update to outpatient payments next year compared to the agency’s proposal in July, the increase is still insufficient given the extraordinary cost pressures hospitals face from labor, supplies, equipment, drugs, and other expenses. As we urged, CMS will use more recent data in its calculations on the payment update, resulting in more accurate data that better reflects the historic inflation and tremendous financial pressures hospitals and health systems have confronted recently. However, hospitals are still dealing with a wide range of challenges in providing care which is why the AHA is urging Congress for additional support by the end of the year.”

Stacey Hughes, Executive Vice President, AHA

Presented in the chart below is a summary of the historical net inflation adjustments for CY 2015 through CY 2023. The annual inflation adjustments are presented net of additional adjustments, such as the MFP reduction, outlined in the final rule for the respective CY. The CY 2023 inflation adjustment is nearly double the increase we have observed in each of the last eight years and is largely driven by labor and supply cost pressures.

CMS is shaking things up for ASCs with the finalization of a new policy related to complexity adjustments for CY 2023. The policy will provide complexity adjustments for combinations of specific procedures and add-on procedure codes deemed eligible for the complexity adjustment under the hospital outpatient prospective payment system (OPPS). By themselves, add-on codes do not receive supplementary reimbursement when they are bundled with primary codes. However, the addition of add-on codes to a primary procedure code will often change the assigned complexity of a procedure and make it more costly in the process. As a result of the policy finalized by CMS, Medicare will provide complexity adjustments that affect the payment rate for certain primary procedures to make up for the additional cost of performing specific add-on services.

CMS received 64 recommendations for potential procedures to be added to the ASC CPL for CY 2023. Based on the review of clinical characteristics conducted by CMS, four out of the 64 procedures were added to the CPL for CY 2023. The four procedures are outlined in the table below. These codes correspond to procedures that have few to no inpatient admissions and are widely performed in outpatient settings.

“CMS’s decision to add only four new procedures to the ASC-CPL for 2023 after ASCA proposed 47 procedures that ASCs are performing safely and successfully for privately insured patients is a serious mistake and denies beneficiary access to high-value care. Forcing otherwise healthy Medicare beneficiaries to receive care in higher-cost settings for these procedures needlessly increases costs to the Medicare program and undercuts Medicare’s mission of serving as a responsible steward of public funds.”

-Bill Prentice, Chief Executive Officer, ASCA

CMS has projected total ASC payments in 2023 to increase from approximately $230 million in 2022, to approximately $5.3 billion. The source of the increase in payments is a combination of enrollment, case-mix, and utilization changes. In conclusion, we have continued to see the trend of rising labor and supply costs play out throughout 2022 and continue into the finalization of the CY 2023 payment system. CMS continues to show stability on the annual inflation adjustment utilizing the hospital market basket to update rates. With that said, ASCA Chief Executive Officer Bill Prentice and AHA Executive Vice President Stacey Hughes have pointed out how the costs of providing care continue to rise rapidly. CMS finalized the addition of four procedures to the ASC CPL for CY 2023. However, the addition of only four codes from the 47 proposed procedures resulted in further pushback and a continued desire for additional procedures to be added to the CPL that are being performed safely and successfully by ASCs.

By: Anthony Domanico, CVA and Nicole Montanaro

The following article was published by the American Association of Provider Compensation Professionals

While the healthcare industry has been moving from volume to value for the last two decades, the movement toward true value-based care has really taken off within the last few years. This is because the way health systems are paid has been largely based on fee-for-service payments with a relatively small share of a health system’s revenue being driven through “value.”

The 2022 MGMA Practice Operations Survey found that health systems see approximately $31,000 in value-based revenue per FTE physician [1]. While that figure is just a small portion of what organizations bring in for the typical physician, the expectation among leaders in the healthcare provider and the payor industries is this trend of shifting revenue away from fee-for service and towards value-based care is going to grow significantly over the next several years. As the way organizations are reimbursed moves towards quality and other non-productivity-based metrics, how those organizations pay their physicians needs to evolve in similar ways. Many organizations we work with at VMG Health are engaging our firm in the following ways:

The remainder of this article will focus on common ways organizations are implementing value into their physician compensation plans. It will also include guidance to organizations on how to select meaningful value-based metrics to provide the most value to the organization.

For those organizations just starting on this journey from volume to value, the most important decision is how to start including quality in plans that have previously paid physicians solely based on the volume of their work. Organizations often start by adding a modest amount of compensation tied to value, and typically it is an amount that guarantees a physician’s base salary or rate per wRVU does not need to decrease to make room for the quality incentive while staying within budgetary expectations.

For example, a productivity model at $55 per wRVU with an expected 2.5% budget increase in 2023 might leave the conversion factor at $55 and add a 2.5% quality incentive as a bonus. Over time, that percentage tied to quality can increase as physicians become more familiar with and trusting of value-based metric reports as they are with wRVU reports. However, this process generally starts small and typically tops out somewhere in the 10-20% range for organizations on the value-based side of the volume-to-value continuum.

Once the magnitude of compensation is determined, there are a few main ways organizations typically structure value-based incentives in their physician compensation plans. These structures are typically based on how the organization’s leadership team answers the following question:

Question: “Should quality be the same for everyone, or should there be some variability for factors like productivity, tenure, base salary differences, or other factors?”

These organizations typically pay all physicians the same flat dollar amount, regardless of physician subspecialty area. As an example, every physician, whether a neurosurgeon or a family practitioner, would have the same $20,000 quality opportunity.

These organizations typically use a percent of market (usually median) approach that pays everyone within the same specialty the same total dollars for quality. As an example, every family medicine doctor would receive up to $13,500 (~5% of median), and every neurosurgeon would receive $37,500 (~5% of median).

These organizations typically use a percentage of-base salary approach where the base salary is set according to organizational policies. This might provide a differentiated level of base compensation for factors like tenure, experience, productivity level, or other factors, and each physician can receive 5% of their individualized base salary as a quality bonus. As an example, Family Medicine Physician A with a $230,000 base salary is eligible for an incentive of up to $11,500, and Family Medicine Physician B with a $250,000 base salary can earn up to $12,500.

These organizations typically use either a quality rate per wRVU or a percentage of total production-based comp approach. Under a pure productivity-based plan, if the compensation plan targets a compensation per wRVU rate of $50 then$47.50 per wRVU might be earmarked for wRVU productivity, and an additional $2.50 per wRVU is set aside, and paid based on quality performance. This type of incentive provides different (and sometimes significantly different) quality incentive opportunities for physicians with different levels of productivity.

Regardless of which of these quality compensation structures is selected, when considering supporting quality bonus payments to physicians a key factor is having a substantive set of quality metrics.

VMG Health collected industry research and identified multiple healthcare articles, publications, and other sources related to quality bonuses paid to physicians. The takeaways about value driver considerations related to the metrics are summarized below. While this list is not exhaustive, it does provide the most common and important factors that support quality bonus payments to physicians.

Generally, factors such as paying for the achievement of “superior” performance standards and selecting patient clinical quality metrics demonstrably impacted by the subject physician(s) help to justify higher-quality bonus payments.

Further, the following chart outlines some best practices to consider for identifying and selecting meaningful metrics, as well as factors to consider before including value-based incentives in a compensation model.

It is important to note the considerations described herein are most pertinent when a party wishes to fund its own value-based compensation program. Alternatively, and subject to certain facts and circumstances, if the funding for a value-based compensation program were to be tied to incremental quality or savings payments from a governmental or commercial payor, other factors may be relevant to consider. Some examples of factors are the incremental revenue/actual savings generated, and the risk and responsibility of the parties.

Organizations that are already far along on the value-based care continuum with a robust quality department/program are starting to expand beyond the quality incentive programs outlined above. These groups are starting to include patient access or acuity-adjusted panel size factors to further focus their compensation plans on population health management. Patient access can include incentives for things like open panels, time to third-next-available appointments, or other factors that get layered on top of productivity and quality compensation.

Acuity-adjusted panel size is an alternative productivity metric to wRVUs that attempts to measure how large a panel of patients a particular physician is charged with caring for. Raw panels (actual number of patients) are adjusted for some level of patient acuity factor – an age and sex adjustment factor, hierarchical condition categories (HCCs), or a multitude of other factors to ensure panel comparability. Unfortunately, there is no perfect acuity-adjustment factor, which makes comparing panel sizes to the external market a unique challenge.

Finally, some organizations are using incentives embedded in payor contracts – quality incentives, shared savings, and other payments – as additional incentives in the provider compensation formula. Typically, organizations take some percentage of dollars received from payors to cover costs incurred by the system and to provide some level of additional remuneration to physicians.

As these value-based programs continue to evolve, organizations have many levers to provide competitive levels of compensation to their physicians. These options help move physicians’ focus from being solely on production to providing high-quality care to patients and reducing unnecessary procedures.

With this complexity, however, organizations must be more diligent than ever to ensure their provider compensation programs continue to align with federal fraud and abuse laws. These regulations are also changing and providing additional levels of protection to organizations that ask physicians to take on meaningful downside risk in their compensation plans. Therefore, careful consideration should be taken in establishing a compensation strategy to ensure the compensation levels remain both competitive and compliant.

Written by Taryn Nasr, ASA and Madeline Noble

The following article was published by Becker’s Hospital Review.

The demand for lithotripsy procedures is expected to increase in the coming years. This expected increase is supported by a review of the Global Lithotripsy Devices Market. It is forecasted to grow at a 5.5% CAGR and is expected to be valued at $2.03 billion by 2027. [1] While several factors have contributed to this rising demand, the primary drivers are the increasing incidence of kidney stones among the geriatric population and the advancements in lithotripsy technology. Healthcare systems and facilities must meet increasing patient demands for lithotripsy services.

The most common lithotripsy procedure is referred to as extracorporeal shock wave lithotripsy (ESWL). ESWL is a noninvasive procedure that uses high-intensity acoustic pulses, or shockwaves, generated by a lithotripter machine to break up kidney stones that are too large to pass through the urinary system. Another common lithotripsy procedure is ureteroscopy with laser lithotripsy which utilizes a ureteroscope and laser fibers to break up the kidney stones. ESWL is typically used for stones inside the kidneys while ureteroscopy is typically used for stones inside the ureter.

Lithotripsy procedures can be performed on an outpatient basis in a variety of formats such as fixed-site, transportable, and mobile. While there are many providers of lithotripsy services throughout North America, the two most recognized names in the mobile lithotripsy space are NextMed and United Medical Systems (UMS). In addition to these nationwide providers, there are smaller, physician-owned providers that service healthcare facilities on a geographic/regional basis.

One approach for facilities to meet the increasing demand for lithotripsy services is to enter into arrangements with lithotripsy providers through professional service agreements. Oftentimes, healthcare facilities find it to be financially prudent to purchase lithotripsy services on an as-needed basis rather than purchase equipment, employ dedicated staff, and fund other expenses associated with the service. In those instances, the hospital or ambulatory surgery center (ASC) will contract with a lithotripsy provider to assume responsibility for all costs related to the operation of the lithotripsy service. In return, the hospital or ASC will pay a predetermined fee to the provider for the services rendered.

The contracted fees are structured to compensate the lithotripsy providers for equipment, personnel, and other costs related to the lithotripsy service. The agreements are usually structured on a mutual, nonexclusive basis with key responsibilities delegated between the facility and the provider. Typically, the provider is responsible for transporting and maintaining the lithotripsy equipment, training and licensing the technician to assist with the procedure, and providing the supplies required to support the procedures.

The most common fee structure consists of a price per lithotripsy procedure. In addition, many agreements consider a maximum annual payment for lithotripsy services to determine the commercial reasonableness of the services agreement. In other words, it must be financially prudent for the facility to purchase lithotripsy services on an as-needed basis rather than purchasing the equipment,

employing the staff, and funding the other operating costs associated with the provision of the services. Other fees that may be included in a lithotripsy services agreement include cancellation fees, minimum on-site charge fees, and after-hours/holiday fees. Regardless of the fee structure of the agreement, the arrangement between the facility and the provider must be understood and followed by both parties for regulatory compliance.

For lithotripsy and similar equipment-based arrangements to maintain compliance, the compensation stated in a service agreement between a facility and a provider must be set at fair market value (FMV). To determine the FMV of service agreements, the environment surrounding healthcare must be considered. The bodies of law often considered include the federal Anti-Kickback Statute and the Physician Self-Referral Law (Stark Law). These statutes provide guidance in determining whether service agreements between facilities and providers, such as lithotripsy service agreements, are compliant and based on FMV.

The Stark Law prohibits physicians from ordering designated health services (DHS) for Medicare patients from entities with which the physician has a financial relationship. However, lithotripsy services are not considered DHS for purpose of the Stark Law. Therefore, lithotripsy services agreements are not governed by regulations regarding per-click leasing arrangements. It is important to note the lithotripsy services agreement must be structured to provide full-service lithotripsy services, and not just a lease of the lithotripsy equipment.

When completing an FMV analysis of lithotripsy services agreements, one must consider the rising cost of equipment and technology advances, staffing pressure causing rising labor costs, requests for quality assurance programs, and market-specific trends such as volume trends and service areas. As the demand for lithotripsy services continues to rise, it will become increasingly important for healthcare facilities to execute proper due diligence and ensure regulatory compliance. To avoid violations of the federal Anti-Kickback Statute and the Stark law, parties must document why an agreement for lithotripsy services is at fair market value.

Written by Clinton Flume, CVA, Tim Spadaro, CFA, CPA/ABV, Olivia Chambers, and Blake Toppins

The following article was published by Becker’s Hospital Review.

The physician medical group sector remains a hot transaction space that outperforms expectations each quarter. This sector’s strong prospects are driven by interest from private equity groups, health systems, and value-based care organizations. However, before buyers operate in this robust sector, they must consider the unique transaction intricacies of such deals, including physician alignment, compensation structure, and due diligence considerations.

For more in-depth insight on this sector, refer to VMG Health’s 2022 Healthcare M&A Report which describes the nature of this sector and summarizes the robust transaction environment experienced in 2021. This report also projected the ongoing elevated deal activity in 2022 which has been confirmed by the 170 deals in Q3 2022 alone (representing a 63.0% increase over Q3 2021).1

Below are three key considerations when executing a physician medical group deal.

Effective medical group alignment strategies are imperative to a healthcare organization’s growth, and the two most common strategies are direct employment and equity investment. The latter can be accomplished through joint ventures or investment in a management service organization (MSO). MSOs are an increasingly popular alignment strategy in states that adopt the corporate practice of medicine (CPOM) doctrine. For more information on MSOs and how they work, read “Physician Practice Strategy: The Private Equity Play.”

According to the Physician Advocacy Institute, 74% of physicians are employed by hospitals or corporate healthcare entities (a 19% increase since 2019).2 The main drivers of this trend include physicians’ financial security, physicians’ professional and work-life balance, the payor environment’s evolution from fee-for-service to value-based care, and the administrative complexities of running a business. In many instances, a direct employment model enables physicians to receive market compensation consistent with their productivity and to focus more closely on clinical initiatives which alleviates their day-to-day administrative responsibilities. From a buyer’s perspective, direct employment models mitigate the risks associated with provider contractual arrangements and enable more definitive long-term planning.

Joint venture structures with physicians may also constitute an attractive proposition for alignment. A joint venture opportunity may take the form of an equity investment in a medical practice (state specific based on CPOM) or in a physician-aligned business, such as an ambulatory surgery center or retail healthcare business. Joint venture affiliations can strengthen physician alignment through synergies such as reimbursement lifts, growth capital, and economies of scale. Along with governance rights, each of these elements plays a key role in defining post-transaction equity alignment structures.

Due to the regulated healthcare industry and strict guidance around physician transactions needing to be consistent with Fair Market Value, it is important that both the business being valued and the compensation offered is documented to be Fair Market Value. Further, there are a myriad of structural nuances that should be considered from a legal, operational, and clinical perspective. As a result, leaning on experts focused on the physician practice sector is highly recommended.

Compensation can be the single most important negotiation item in a medical group transaction. As private equity, insurance companies, and for-profit management organizations enter the sector, compensation models demand careful attention to ensure a good alignment of physician productivity, physician pay, and medical group returns.

External alignment allows providers to benefit from direct investment when shifting to an employment model. Although complex, it has increasingly become the norm for compensation models to factor a physician’s external interests into an agreement.

Compensation arrangements continue to require ongoing innovation to stay competitive and relevant. As transaction activity intensifies and healthcare shifts from a volume-based system of care to a value-based system of care, compensation arrangements must be designed to evolve with the dynamic intricacies of the industry. Understanding the latest compensation models, and how to design those models and a transition plan, has proven to be a critical factor for success with physician practice strategy. For recent insight on design, further information can be found here.

The competitive environment for medical group assets has intensified as capital continues to flow into the sector. As part of the deal process, performing both pre- and post-acquisition due diligence is now the standard for high-value deals. Due diligence focuses on the following areas:

In a unique, complex, and dynamic transaction landscape, expertise in healthcare-specific attributes can transform a transaction. Considering the surge in physician medical group deals as the expected continuing high rate of activity, buyers will have to increase their knowledge of the sector’s intricacies to remain competitive and achieve their strategic goals. At every stage of a transaction, VMG Health’s expertise as the leading provider of healthcare transaction and strategy services provides the advantage needed to execute successful deals.