Written by Jack Hawkins and Colin Park, CPA/ABV, ASA

2019 was another busy year for the healthcare industry full of large-scale transactions aimed at gaining greater vertical and horizontal integration. While the healthcare market as a whole saw mega-mergers in 2019, such as CVS-Aetna and Dignity-CHI, there were no large-scale transactions within the Ambulatory Surgery Center (“ASC”) sub-industry. Despite there being no platform-level transactions within the ASC market in 2019, the fragmented ASC industry continued to consolidate. For ASC’s, several prominent trends continued from 2018 through 2019: the shift of higher acuity procedures from the inpatient setting to the outpatient setting, increased Medicare reimbursement rates, continued consolidation within the ASC sector, and increased activity by hospitals seeking to grow their ambulatory footprint with a particular focus on ASCs.

Transaction Activity

In 2019, we saw a high number of transactions at the individual-facility level. While there were no mega-mergers in 2019, the fragmented ASC industry continued to consolidate. It is worth noting that although the industry continues along the trend of consolidation, approximately 71% of ASC facilities remain independent, leaving room for further consolidation at the individual-facility level. Notable ASC transactions in 2019 include:

- Talomon Capital, a London-based investment firm, amassed roughly 2.6 million shares, or approximately 5.0% of Surgery Partners, Inc., as of August 14, 2019.

- Miami-based Gastro Health, LLC acquired Seattle-based Puget Sound Gastroenterology on September 23, 2019. The deal included Puget Sound’s practices, four ASCs, and 24 physicians and support staff. This is one of three separate acquisitions by Gastro Health in 2019.

- On December 6, 2019, Varsity Healthcare Partners completed a recapitalization and growth capital partnership with Peak Gastroenterology Associates, the largest provider of gastroenterology services and ancillary patient diagnostic and remedial treatment services in Colorado. PGA has a network of 12 outpatient locations and 21 ambulatory and hospital-based endoscopy centers throughout Colorado.

- On October 16, 2019, GI Alliance partnered with Arizona Digestive Health (“ADH”). ADH is the largest GI practice in Arizona and serves patients in 26 office locations and 11 affiliated endoscopy centers.

- Private equity firms continued to be a major player in the ASC industry. The increasingly active marketplace for PE firms can be illustrated by the number of PE-firms becoming involved in physician specialties such as gastroenterology (“GI”), ophthalmology, orthopedics, and urology.

The ASC marketplace continues to be an active transaction arena as major operators look to consolidate and look for new opportunities in this space. This topic was at the forefront of Surgery Partner’s 4Q Earnings call where Executive Chairman Wayne Scott DeVeydt noted, “As we enter 2020, we see increased opportunity for acquisitions at attractive multiples.”

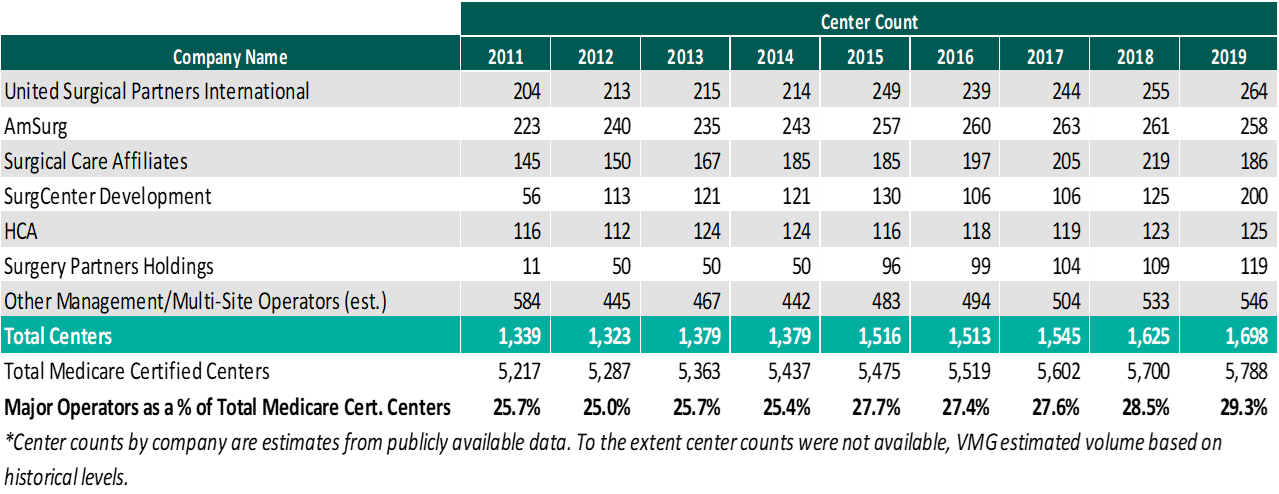

As of December 31, 2019, the largest operators (in terms of number of ASCs) are United Surgical Partners International (“USPI”), Envision Healthcare/Amsurg Corporation, and Surgical Care Affiliates (“SCA”), with ownership of approximately 264, 258, and 186 ASCs, respectively. As noted in the chart below, the number of total centers under partnership by a national operator, as a percentage of total Medicare certified centers, saw a slight increase from 2018 to 2019 growing from approximately 5,700 centers to 5,788 centers. Additionally the top 5 management companies have increased the number of centers under management by approximately 359 centers since 2011, which represents a compound annual growth rate of 4.2%. As management companies have increased in size, they are able to increasingly provide a greater level of strategic value by bringing greater leverage with commercial payors, enhanced management and reporting capabilities, improved vendor contracts, etc. to acquisition targets.

Reimbursement

On November 1, 2018, the Medicare reimbursement fee schedule for ASCs in 2019 was finalized by the Centers for Medicare & Medicaid Services (“CMS”). For CYs 2019 through 2023, CMS will update the ASC payment system using the hospital market basket update, rather than the Consumer Price Index for All Urban Consumers (“CPI-U”). CMS published the 2019 ASC payment final rule, which resulted in overall expected growth in payments equal to 2.1% in CY 2019. This increase is determined based on a hospital market basket percentage increase of 2.9% less the multifactor productivity (“MFP”) reduction of 0.8% mandated by the ACA. Moreover, the ASC payment final rule for CY 2020 was released by CMS on November 1, 2019, and the rate will increase by 2.6% in CY 2020. This increase is determined based on a hospital market basket percentage increase of 3.0% less the MFP reduction of 0.4% mandated by the ACA. The ASC industry sees the 2019 and 2020 reimbursement increases as a win as CMS continued to follow its proposal to align update factors, moving ASCs to the hospital market basket which historically was used to update HOPD payments. Under the final rule, CMS will use the hospital market basket to update ASC payments through CY 2023.

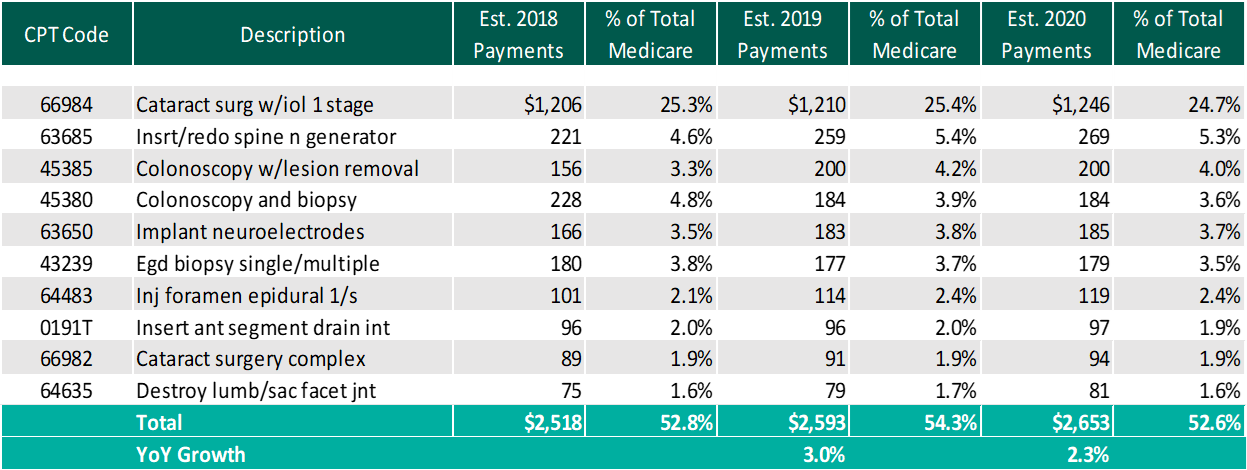

The table below reflects a summary of the estimated Medicare ASC payments for 2018, 2019 and 2020 for the top 10 CPT codes performed in ASCs in 2019. As noted below, the estimated 2020 payments by Medicare for the top 10 CPT codes for 2019 is projected to increase 2.3% through the estimated 2020 payments.

Procedures

On November 1, 2018, CMS released the 2019 OPPS and ASC Payment System final rulings, which finalized the addition of 12 cardiac catheterization procedures that were in the proposed rule, as well as added five additional procedures performed during cardiac catherization procedures to the list of ASC covered surgical procedures.

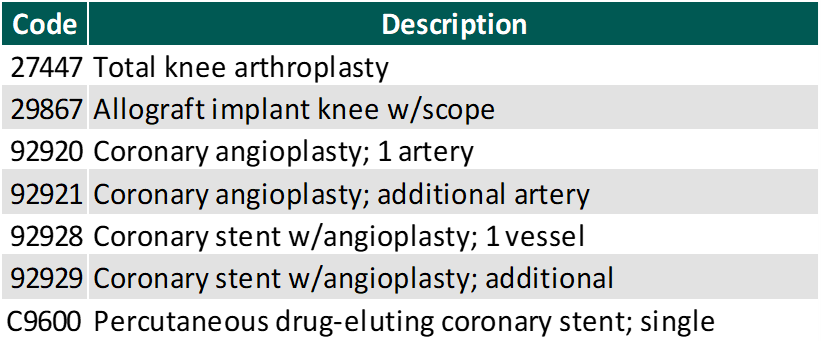

In addition to the codes above, CMS released on November 1, 2019 the addition of 8 CPT codes to the ASC-Payable List, meaning they are eligible for Medicare payment in the ASC setting in 2020. Most importantly these codes include total knee arthroplasty (knee replacement surgery), allograft knee implant (knee reconstruction), and six coronary intervention procedures. These codes are listed below.

Along with the eight codes added to the ASC-Payable List, seven codes were removed from the Inpatient-Only List, meaning they are eligible to be paid by Medicare in the hospital outpatient setting in addition to the hospital inpatient setting. The removal of these codes from this list is similar to what we saw in 2017-2018 with total knees, where those codes were then ultimately added to the ASC covered procedures list. This could be an indicator of the continued shift of higher acuity cases to the outpatient setting.

With the addition of the new codes and the final ruling for increases to ASC payments by CMS, it would be expected that total Medicare ASC payments in 2020 would increase compared to 2019. Ultimately, CMS has projected total ASC payments in 2020 to increase approximately $230 million from 2019 payments, to be approximately $4.96 billion. The source of the increase in payments is a combination of enrollment, case-mix, and utilization changes. It should also be noted that CMS reduced the device intensive threshold for ASC procedures to 30% for CY 2019 and subsequent years.

Conclusion: ASCs in 2019

In conclusion, we are continuing to see themes from 2018 play out in 2019 and into 2020. The expectation is that there would be further consolidation within the ASC market with a greater involvement by private equity companies. At the center level, higher acuity case volume will continue to shift from the inpatient setting further cementing the ASC as the low-cost, efficient alternative to the hospital setting.