CY 2023 Medicare OPPS and ASC Payment System Final Rule

Rachel Linch

December 6, 2022

Written by Jack Hawkins, Ryan Mendez, and Colin Park, CPA/ABV, ASA

The following article was published by Becker’s ASC Review

2022 saw a continuation of 2021 trends as the healthcare industry further rebounded from the coronavirus (COVID-19) pandemic. The Ambulatory Surgery Center (ASC) subindustry largely recovered in 2021, but certain specialties that lagged in 2021 saw a further recovery in 2022. The ASC industry continued to consolidate throughout 2022 despite not having the major platform-level transactions that were observed in 2021. There were trends that started pre-pandemic that continued to be observed in 2022 such as the shift of higher-acuity procedures from the inpatient setting to the outpatient setting, consolidation of ASCs by management companies, and a push by hospitals to grow their ambulatory footprint with a particular focus on the outpatient setting.

Along with these recurring trends, the subindustry was impacted by macroeconomic trends related to upward pressure on labor, supply, and general costs resulting from a tight labor market and elevated inflationary pressures. The continued trend of increased Medicare reimbursement rates saw its largest escalation ever as a direct result of these pressures.

In March 2020, the world was impacted by the spread of the COVID-19 pandemic, and subsequently, 2021 was a year of rebuilding and recovering from the lasting effects brought on by the pandemic. ASCs in 2021 had an increase in case volumes across almost all specialties. This was primarily due to patients who were willing to resume elective procedures that were postponed and centers that kept their doors open.

In 2022, ASCs saw case volume return to pre-pandemic levels or experienced continued growth if they had not already experienced a return to normal operations. Specialties that were hit especially hard by COVID-19, such as ENT, returned to pre-COVID levels in 2022 as schools and school activities returned to pre-pandemic normalcy. In 2022, the impact of the pandemic on ASCs was less related to revenue and more related to expenses. The lingering effects of COVID-19 were related to the shortage of healthcare workers and the supply chain issues that continued to pressure the profitability of surgery centers. Looking into 2023, controlling labor and supply costs will be a point of focus for ASCs.

The trend of higher-acuity procedures shifting from an inpatient or HOPD setting to a freestanding ASC setting continued throughout 2022. In 2022, specialties that increased their footprint in ASCs included cardiology, orthopedics, and higher-acuity spine procedures. According to data from the ASC Association, orthopedics was the most common specialty serviced by ASCs in 2022.

Director of ASC Operations at Virtua Health Catherine Retzbach said ASCs that perform these high acuity cases “offer patients more options to have procedures be performed in a high-quality, low-cost environment.” Furthermore, according to the most recent Ambulatory Surgery Center report published by Research and Markets, ASCs are projected to perform half of all cardiology procedures by the mid to late 2020s.

The ASC subindustry continues to focus on higher-acuity specialties when considering both organic growth and M&A opportunities. President of Tenet Saum Sutaria noted the continued focus of the ASC business toward higher-acuity service lines in the company’s Q3 2022 earnings call. Tenet is the parent company of USPI and is the largest outpatient surgery center operator in the United States. The company reported that these procedures made up 20% of USPI’s year-to-date volume due to growth in their orthopedic and spine business. Sutaria further said “the [USPI] team is focused on organic growth, [and] increase in higher-acuity services and M&A.” These insights highlight the ASC subindustry’s focus on higher-acuity service lines, and indicate the shift towards ASCs for these types of procedures is likely to continue in the future.

In 2022, we saw the continued expansion of a prominent large-level ASC platform player highlighted by the finalization of a large platform-level transaction that began in 2020. In addition, there were a significant number of transactions at the individual-facility level. Consistent with the observed larger platform-level transaction, the fragmented ASC industry has continued to consolidate. It is worth noting that although the industry continues to consolidate approximately 70% of ASC facilities remain independent as of 2022. This leaves room for further consolidation at the individual-facility level.

In 2020, Tenet Health finalized a deal for $1.1 billion to acquire 45 ASCs from SurgCenter Development. This was the first stage of a multi-part acquisition, and in Q4 of 2021, USPI entered a $1.2 billion deal to acquire SurgCenter Development’s remaining centers and established a long-term development deal. The transaction included acquiring ownership interest in an additional 92 ambulatory surgery centers, other support services in 21 states, and providing continuity for future de novo development projects. In 2022, USPI made substantial strides in consolidating the 92 ASCs it acquired from SurgCenter Development. This process is expected to continue into 2023 as the centers are further consolidated. The acquisition has enabled Tenet and USPI to expand their footprint and solidify their position as a leader in the ambulatory surgery center market.

“There’s anticipated additional synergies related to the SCD transactions that will continue to grow as we move through next year as well. And the other thing is the M&A activity that USPI will execute on. The pipeline is robust.”

-Dan Cancelmi, Chief Financial Officer

On June 21, 2022, USPI and United Urology Group formed a joint venture partnership in 22 ASCs. USPI acquired a portion of United Urology Group’s ownership interests in ASCs located in Maryland, Colorado, and Arizona. The ASCs will be owned and operated by the joint venture, and USPI will provide management and support services to the ASCs. The transaction closed in the third quarter. In February 2022 The Rise Fund, an impact investing strategy managed by TPG, announced the acquisition of Blue Cloud Pediatric Surgery Centers which is the largest operator of pediatric dental ASCs in the United States. TPG Rise is a large impact investing platform with more than $13 billion in assets across its various funds, including The Rise Funds, TPG Rise Climate, and the Evercare Health Fund.

On December 9, 2022, Michigan-based Sparrow Health System and Michigan Medicine, formerly the University of Michigan Health System, announced an $800 million partnership. Michigan Medicine will invest $800 million into the expansion of Sparrow’s ASC and neonatal care unit.

In April 2022, UnitedHealth Group’s Optum announced the purchase of Kelsey-Seybold, a Houston-based physician group for $2 billion. The acquisition expanded Optum’s presence in the primary care market. As part of this acquisition, Optum gained two ASCs that were owned by Kelsey-Seybold.

Finally, on May 3, 2022, Surgery Partners and ValueHealth announced a partnership that aims to construct new ASCs and implement ValueHealth’s value-based surgical programs at Surgery Partners’ existing and upcoming locations. Additionally, Surgery Partners will manage and take over ValueHealth’s stake in three current ASCs and four centers that are in the development phase.

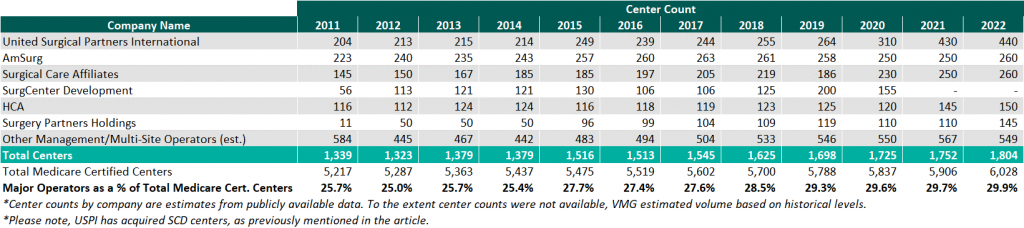

As of December 31, 2022, the largest operators (in terms of the number of ASCs) are United Surgical Partners International (USPI), Envision Healthcare/Amsurg Corporation, and Surgical Care Affiliates (SCA), with ownership of approximately 440+, 260+, and 260+ ASCs, respectively.

As noted in the chart below, the number of total centers under partnership by a national operator, as a percentage of total Medicare-certified centers, saw an increase from 2021 to 2022 growing from approximately 1,752 centers to 1,804 centers. Additionally, the top five management companies have increased the number of centers under management by approximately 511 centers since 2011 which represents a compound annual growth rate of 5.37%. As management companies have increased in size they are able to increasingly provide a greater level of strategic value by bringing greater leverage with commercial payors, enhanced management and reporting capabilities, and improved efficiency related to staffing, supplies procurement, and other general and administrative expenses.

On November 2, 2021, the Medicare reimbursement fee schedule for ASCs in 2022 was finalized by the Centers for Medicare & Medicaid Services (CMS). Consistent with previous years for CYs 2019 through 2023, CMS will update the ASC payment system using the hospital market basket update instead of the Consumer Price Index for All Urban Consumers (CPI-U). CMS published the 2021 ASC payment final rule which resulted in overall expected growth in payments equal to 2.0% in CY 2022. This increase is determined based on a hospital market basket percentage increase of 2.7% less the multifactor productivity (MFP) reduction of 0.7% mandated by the ACA.

Moreover, the ASC payment final rule for CY 2023 was released by CMS on November 1, 2022, and resulted in overall expected growth in payments equal to 3.8% in CY 2023. This increase is determined based on a projected inflation rate of 4.1% less the MFP reduction of 0.3% mandated by the ACA. The 3.8% growth in payments represents the largest increase in projected payments year over year and is a direct result of the increase in labor, supplies, and other cost pressures seen over the last year. Although the industry recognizes the increase in payments as a win, many major players believe the increase was insufficient given the extraordinary cost pressures hospitals and ASCs are facing. The way ASCs navigate the dynamic macroeconomic environment currently in place will be a major point of interest over the coming years.

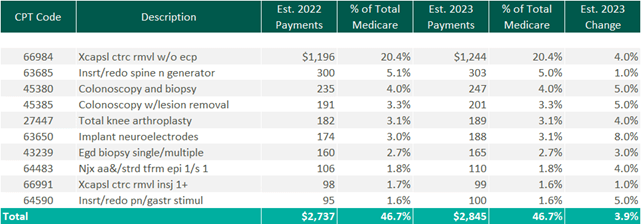

The table below reflects a summary of the estimated Medicare ASC payments for 2022 and 2023 for the top 10 CPT codes performed in ASCs in 2022. As noted below, the observed 2022 payments by Medicare for the top 10 CPT codes are projected to increase by 3.9% through the estimated 2023 payments.

CMS has implemented a new policy that will provide complexity adjustments for certain ASC procedures in CY 2023. These adjustments will be applied to combinations of primary procedures and add-on codes deemed eligible under the hospital outpatient prospective payment system (OPPS). In the past, add-on codes did not receive additional reimbursement when bundled with primary codes. However, with this new policy Medicare will provide adjustments to the payment rate for certain primary procedures to account for the additional cost of performing specific add-on services.

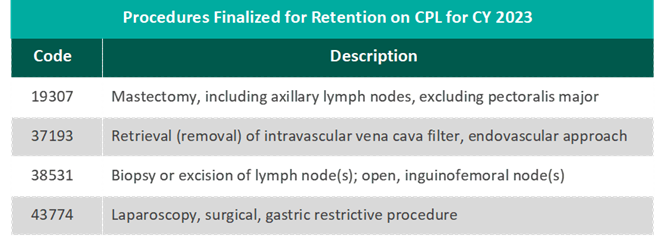

CMS considered 64 recommendations for new procedures to be added to the ASC CPL for CY 2023. After reviewing the clinical characteristics of these procedures, four were chosen to be added to the CPL for the upcoming year. These procedures are typically performed in outpatient settings and have little to no inpatient admissions. The four procedures are outlined in the table below. However, the addition of only four codes resulted in pushback and a continued desire for additional procedures to be added to the CPL that is being performed safely and successfully by ASCs.

“CMS’s decision to add only four new procedures to the ASC-CPL for 2023 after ASCA proposed 47 procedures that ASCs are performing safely and successfully for privately insured patients is a serious mistake and denies beneficiary access to high-value care. Forcing otherwise healthy Medicare beneficiaries to receive care in higher-cost settings for these procedures needlessly increases costs to the Medicare program and undercuts Medicare’s mission of serving as a responsible steward of public funds.”

– Bill Prentice, Chief Executive Officer, ASCA

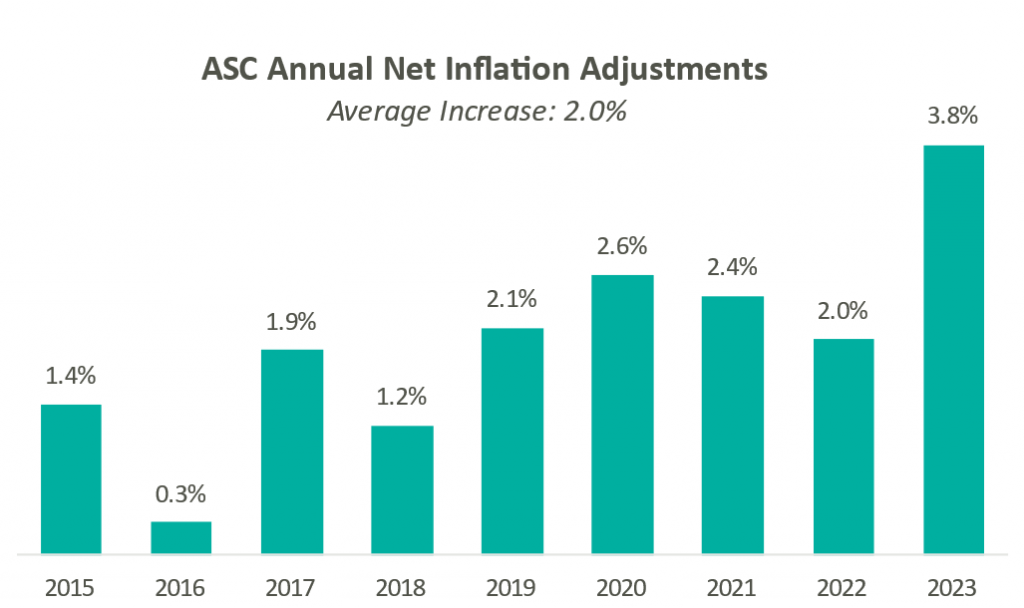

Presented in the chart to the right is a summary of the historical net inflation adjustments for CY 2015 through CY 2023. The annual inflation adjustments are a presented net of additional adjustments, such as the MFP reduction, outlined in the final rule for the respective CY. The CY 2023 inflation adjustment is nearly double the increase we have observed in each of the last eight years and is largely driven by labor and supply cost pressures.

Overall, the final ruling to increase ASC payments by CMS and the increased recovery from COVID-19 both indicate an expected increase in total ASC payments. Ultimately, CMS has projected total ASC payments in 2023 to increase by approximately $230 million from 2022 payments to approximately $5.3 billion.

In conclusion, 2022 was a year of growth throughout the ASC industry and a year of continued recovery from the effects of the pandemic. Key trends to look for going forward are the effects of increased cost pressures impacting the healthcare industry as a whole, and specifically how ASCs respond. Expectations for 2023 are continued growth and consolidation in this sub-industry. The ASC setting provides a convenient, cost-effective way for patients to receive high-quality care. The continued shift of higher-acuity procedures to the outpatient setting should give optimism to the success of the subindustry as a whole as long as cost pressures are mitigated properly. Overall, ASCs at the center level are expected to continue the positive momentum that persisted in 2022 and the subindustry is expected to see the level of transactions increase through 2023.