Written by Ryan Mendez, Jack Hawkins, and Colin Park, CPA/ABV, ASA

The following article was published by Becker’s ASC Review.

The ambulatory surgery center (ASC) sector continued to evolve in 2023, reflecting a trend of steady growth, higher-acuity cases, and some changing regulations. 2023 featured continued consolidation through a combination of investment by prominent ASC platforms and acquisitions made by new entrants in the market.

Higher acuity cases continued to decant to the outpatient setting, and with the Centers for Medicare & Medicaid Services (CMS) moving total shoulder arthroplasty to the ASC Covered Procedures List, we expect this shift to continue. In addition to these trends, 2023 saw significant changes in the regulatory landscape, particularly with the liberalization of Certificates of Need (CON) requirements for certain states. The changing of CON regulations is poised to further accelerate the development opportunities of ASCs, enhancing their ability to meet the increasing demand for outpatient surgical care. 2023 continued to solidify the ASC’s role as a dynamic force in healthcare, poised to meet the surging demand for efficient, accessible surgery.

Ambulatory Surgery Center Market Overview

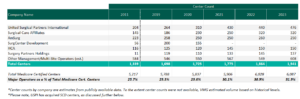

As of December 31, 2023, the largest operators (in terms of number of ASCs) are United Surgical Partners International (USPI), Envision Healthcare/Amsurg Corporation, and Surgical Care Affiliates (SCA), with ownership in approximately 476, 320, and 250 ASCs respectively. As noted in the chart below, the number of total centers under partnership by a national operator saw an increase from 2011 to 2023, growing from approximately 1,339 centers to 1,941 centers, which represents a compound annual growth rate of 3.14%. Additionally, the top five management companies have increased the number of centers under management by approximately 578 centers since 2011, which represents a compound annual growth rate of 4.85%. As management companies have increased in size, they can increasingly provide a greater level of strategic value by bringing greater leverage with commercial payors, enhanced management and reporting capabilities, and improved efficiency related to staffing, supplies procurement, and other general and administrative expenses.

Market Dynamics

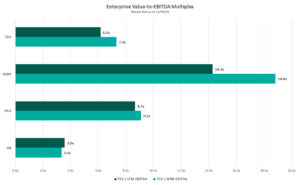

Public companies in the ASC market such as HCA Healthcare (HCA), Tenet Healthcare (THC), Surgery Partners (SGRY), and Medical Facilities Corporation (DR) offer insights into the ASC industry’s trends, challenges, and transaction data. These firms’ valuation multiples, illustrated in the figure below, serve as indicators of market valuation that are key to understanding the broader trends within the sector. Considering these multiples requires a nuanced approach, especially since larger organizations like HCA and THC have diversified operations beyond ASCs, which affect their market valuation and risk profiles. For example, HCA manages a large number of hospitals within its extensive healthcare services network, and THC’s ASC management platform, USPI, significantly impacts its profitability despite THC also operating numerous hospitals. To gain a comprehensive understanding of the ASC industry, it is beneficial to examine the detailed financial disclosures of these public companies. These include investor presentations and SEC filings, which offer a deeper insight into their performance and prospects than valuation multiples alone can provide.

For those interested in exploring the ASC industry further, including obtaining benchmarking information and analysis of ASCs across the United States, VMG Health’s Intellimarker is a valuable resource. The Intellimarker is an advanced, multi-specialty ASC benchmarking tool designed to facilitate a better understanding of ASCs’ relative financial and operational performance. Additionally, VMG Health’s Pulse on The Public Market provides coverage of various healthcare verticals in addition to the ASC sector.

Surgery Partners

In Q3 2023, Surgery Partners showcased a solid performance in the ASC sector, with surgical cases rising nearly 6% year –over year to over 172,000, after adjusting for divested facilities. This growth was driven by an emphasis on higher acuity cases and strategic acquisitions, as noted by Executive Chairman Wayne DeVeydt, culminating in $674.1 million in net revenue and $105.5 million in adjusted EBITDA for the quarter. The company experienced an uptick in total joint replacements, which increased by approximately 60% year –to date, supported by the recruitment of nearly 500 new physicians who specialize in musculoskeletal procedures into their centers. Despite facing challenges like anesthesia coverage and cost pressures, CEO Eric Evans is optimistic about the company’s long-term prospects, underlining its strategic focus on complex, higher-margin surgeries. Surgery Partners’ strategic acquisitions throughout the year have both bolstered its competitive position and broadened its geographical footprint and specialty mix, reinforcing its standing in high-growth markets and specialties.

Tenet Healthcare: United Surgical Partners International (USPI)

During Tenet Healthcare’s Q3 2023 earnings call, the company highlighted its strong performance in ASC operations by its subsidiary, USPI. The ASC arm of THC reported a robust quarter with $370 million in adjusted EBITDA, a 16% increase from the same period in 2022, driven by a 7.9% rise in same-facility revenues and sustained margins. The subsidiary experienced notable volume growth in high-acuity service lines, including a mid-teens increase in total joint replacements, attributed to attracting high-quality physicians and leveraging increased patient demand for ambulatory surgery care. Additionally, THC expanded its ASC portfolio in Q3 by adding six new centers focused on higher-acuity orthopedic services in states like Nevada, Maryland, Texas, and Florida, featuring top musculoskeletal specialists. According to CEO Saum Sutaria, USPI’s aggressive expansion strategy includes over 30 centers in development, emphasizing high-value, specialized healthcare services. This expansion, part of a broader effort to advance site of service value-based care, aims to position USPI for sustained growth and profitability by tapping into high-growth, high-margin healthcare services and meeting patient demand for specialized ambulatory care.

HCA Healthcare

In Q4 2023, HCA Healthcare reported a robust performance, with CEO Sam Hazen highlighting the strong demand across service lines and the improved operational efficiencies that led to a significant revenue increase to $17.3 billion. This performance, which surpassed expectations, was supported by a near 14% increase in adjusted EBITDA compared to the same quarter last year. This growth was driven by an 11% increase in same-facility revenue and improvements in operating margins, highlighting HCA’s ability to leverage increased revenue effectively. CFO Rutherford identified HCA’s ambulatory surgery division contributions to this success, demonstrating the company’s strategic focus on expanding its high-acuity service offerings and enhancing patient care through strategic acquisitions and network expansion.

Medical Facilities Corporation

During the 2023 Q3 earnings call, Medical Facilities Corporation demonstrated a strong financial performance, driven by strategic divestitures and a concentrated effort on core operations, resulting in a 7.4% rise in facility service revenue to $104.6 million. The executives highlighted significant operational improvements, including a 13.7% increase in EBITDA, attributed to enhanced efficiency and cost-saving strategies. Interim President Jason Redman noted that the increased performance was largely due to case mix, but that surgical case volumes also increased by 1%. Medical Facilities Corporation saw three of their surgical hospitals recognized for excellence in joint replacement, emphasizing the strategic shift towards managing higher-acuity cases in outpatient settings.

Continued Trend of Higher Acuity Cases in ASCs

The trend of shifting higher-acuity procedures from inpatient or Hospital Outpatient Department (HOPD) settings to ASCs continued to grow throughout 2023. Specialties like cardiology, orthopedics, and advanced spine procedures increasingly marked their presence in ASCs. Throughout the year, many ASCs doubled down on their high-acuity procedures to drive revenue growth. Annu Navani, founder of Comprehensive Spine & Sports Center in Campbell, CA, elaborated: “The growth in orthopedics, spine and pain has been steady and will remain so. These are safe specialties, as the need is always there and will continue to thrive…” It is more than just a concept, as Surgery Partners CFO, David Doherty, provided some insight into how higher-acuity cases have spurred growth during the company’s Q3 earnings call. Doherty noted, “On a same-facility basis, total revenue increased 14.2% in the third quarter, with case growth at 2.9%. Net revenue per case was 11.0%, higher than last year, primarily driven by higher-acuity procedures.” This continued shift towards higher-acuity procedures being performed in ASCs is a clear indicator of the sector’s adaptation and growth, meeting the evolving demands of healthcare while offering efficient and cost-effective solutions for complex medical needs.

In 2023, ASC operators focused on both organic growth within their existing high-acuity specialties and actively pursued M&A opportunities as a key strategy to expand their footprint. During Surgery Partner’s Q1 earnings call, CEO Eric Evans noted that, “With an increase in the share of orthopedic and cardiac procedures moving into lower-cost, high-quality, short-stay surgical facilities, we are considering all options to capture our fair share, including sourcing and managing a robust M&A pipeline…”

Similarly, during THC’s Q3 earnings call, CEO Saum Sutaria, reiterated that THC is committed to scaling their ASC portfolio: “During the quarter, we added six new centers, the majority of which were focused on higher-acuity orthopedic services.” These developments illustrate the sector’s dynamic response to changing healthcare demands, positioning it for sustained growth and wider service reach as more high-acuity cases continue to shift to the ASC setting.

Procedures

CMS noted in its fact sheet that, “in addition to finalizing payment rates, this year’s rule includes policies that align with several key goals of the Biden-Harris Administration, including promoting health equity, expanding access to behavioral health care, improving transparency in the health system, and promoting safe, effective, and patient-centered care. The final rule advances the Agency’s commitment to strengthening Medicare. It uses the lessons learned from the COVID-19 PHE to inform the approach to quality measurement, focusing on changes that will help address health inequities.”

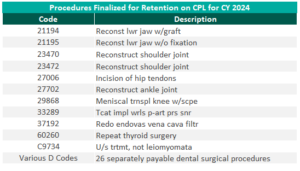

CMS finalized the addition of 37 surgical procedures to be added to the ASC CPL for CY 2024, outlined in the table below. These include 26 dental codes that were included in the proposed rule, and 11 surgical codes that were not included in the proposed rule—most notably total shoulder arthroplasty. These codes correspond to procedures that have little to no inpatient admissions and are widely performed in outpatient settings.

“We thank CMS for heeding our request to move additional surgical procedures—including total shoulder arthroplasty—onto the ASC payable list. Doing so benefits both Medicare beneficiaries, who now have a lower-cost choice for the care they need, and the Medicare program itself, which will save millions of dollars as volume moves to the high-quality surgery center site of service.” – Bill Prentice, Chief Executive Officer, ASCA

Reimbursement

On November 1, 2022, the Medicare reimbursement fee schedule for ASCs in 2023 was finalized by CMS. Consistent with previous years, For CYs 2019 through 2023, CMS will update the ASC payment system using the hospital market basket update, rather than the Consumer Price Index for All Urban Consumers (CPI-U). CMS published the 2022 ASC payment final rule, which resulted in overall expected growth in payments equal to 3.8% in CY 2022. This increase is determined based on a hospital market basket percentage increase of 4.1% less the multifactor productivity (MFP) reduction of 0.3% mandated by the ACA. The 3.8% growth in payments represented the largest increase in projected payments year over year and was a direct result of the increase in labor, supplies, and other cost pressures seen over the last year.

Moreover, CMS released the ASC payment final rule for CY 2024 on November 2, 2023, resulting in overall expected growth in payments equal to 3.1% in CY 2023. This increase is determined based on a projected inflation rate of 3.3% less the MFP reduction of 0.2% mandated by the ACA. This is an increase of 0.3% from the proposed rule. Many healthcare industry leaders think the recent payment hike is too small given the intense cost pressures on hospitals and ASCs. How ASCs manage in today’s changing economic climate will be closely watched in the coming years

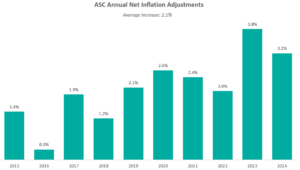

The chart below presents a summary of the historical net inflation adjustments for CY 2015 through CY 2024. The annual inflation adjustments are presented net of additional adjustments, such as the MFP reduction, outlined in the final rule for the respective CY. The CY 2024 inflation adjustment is slightly lower than the increase observed last year, although it continues to be elevated compared to the adjustments observed prior to 2023 largely driven by labor and supply cost pressures.

The table below reflects a summary of the estimated Medicare ASC payments for 2023 and 2024 for the top 10 CPT codes performed in ASCs in 2023. As noted below, the estimated 2024 payments by Medicare for the top 10 CPT codes from 2023 are projected to remain relatively flat overall, though there are some notable changes at the individual CPT level, including large decreases to three spinal/neuro stimulator codes.

CMS has projected total ASC payments in 2024 to increase to approximately $7.1 billion, an increase of approximately $207 million compared to estimated CY 2023 Medicare payments.

Transaction Activity

In 2023, we saw the continued consolidation of the ASC market with individual transactions by prominent, large-level ASC platform players and M&A activity at the lower-middle-market level with a newly founded, private equity (PE) backed ASC development management company acquiring two centers to begin its platform. Although the industry continues to consolidate, as of 2023, approximately 68% of ASC facilities remain independent, leaving room for further consolidation at the individual-facility level.

The ASC market has seen a continued trend of intentional PE activity with interest in ASCs in recent years, most often tied to related physician practice portfolio companies. Driven by favorable tailwinds, this type of investment in ASCs allows PE investors to capture additional revenue streams related to their physician practice investments. PE interest in an ASC strategy outside of a physician practice portfolio company has also increased recently. Based on data from PitchBook’s Q3 2023 Healthcare Services Report, the ASC industry saw six trackable PE deals through September 30, 2022. These deals were mostly add-on investments, with one deal being a growth investment. PE total deal activity in the ASC space has remained fairly consistent over the last five years, though 2023 notably marks the first time since 2020 when no platform PE deals were tracked through PitchBook’s report. However, October 2023 saw the announcement of a PE-backed ASC platform.

In October 2023, a newly founded, multispecialty ASC development and management company, SurgNet Health Partners, Inc. (SurgNet), announced the acquisition of two ASCs in Michigan and Ohio. SurgNet is newly backed by Fulcrum Equity Partners, Leavitt Equity Partners, and Harpeth Capital. A $50 million equity check was syndicated to launch the platform, and presumably, additional investments will follow to support further investments. SurgNet, together with its equity partners, is expected to rapidly expand in the outpatient surgery market through aggressive growth strategies, including acquisitions, de novo ventures, and effective center management.

On February 9, 2023, United Musculoskeletal Partners (UMP) partnered with two orthopedic practices based in Dallas-Fort Worth. All-Star Orthopaedics, with four clinic locations, and OrthoTexas Physicians and Surgeons, PLLC, operating five clinics and one surgery center, were both acquired by the UMP platform. In August, UMP expanded this partnership by acquiring an ortho-focused surgery center, Pinnacle Orthopaedics, in an add-on LBO transaction.

In May 2023, The Office of Health Strategy (OHS) approved two settlement agreements allowing Hartford HealthCare (HHC) to acquire two outpatient surgical centers in Connecticut. On May 12, 2023, Surgery Center of Fairfield County, a subsidiary of HCA Health, was acquired by HHC, for an undisclosed amount. Further, in October 2023, HHC acquired Lichfield Hills Surgery Center, also for an undisclosed amount.

Covenant Physician Partners expanded its ASC footprint with the merger of its St. Vincent Eye Surgery Center and Wilshire Center for Ambulatory Surgery, adding an additional facility for surgeries.

On September 18, 2023, Unifeye Vision Partners (UVP), a management and support services company with an ophthalmology and optometry practice network including 13 ASCs, announced the acquisition of Insight Vision Group, a comprehensive eyecare platform in California. Insight Vision Group is made up of 10 clinics and two multi-specialty ASCs. UVP was active in the M&A space earlier in the year, acquiring Premier Surgery Center of Santa Maria, through an LBO for an undisclosed amount.

Surgery Partners further expanded its reach in September 2023, with the announcement of the acquisition and partnership with NorCal Orthopedic Surgery Center in San Ramon, CA. The center, an out-of-network ASC originally comprised of nine separate operating entities along with 25 physician partners, was advised by Merrit Healthcare Advisors in structuring the merger of the nine entities into one ASC to then be sold to Surgery Partners.

TriasMD, the parent company of DISC Surgery Centers and another musculoskeletal management company, declared its acquisition of Pinnacle Surgery Center in October 2023. This strategic move extends DISC’s data- and evidence-driven ASC model into Northern California, marking the second acquisition within the past six months. TriasMD previously acquired Gateway Surgery Center in Santa Clarita in February.

In November 2023, Regent Surgical Health acquired majority ownership in Oregon Surgical Institute (OSI), expanding a joint venture partnership that started in 2016. Notably, OSI was the northwest US’ first ASC to focus on complex spinal and total joint replacement cases. Regent COO Jeff Andrews said, “Our evolved partnership was made possible by the trust OSI’s leadership team has placed in us, and this will bolster both value and access by strengthening OSI’s position as a home for the growing list of procedures being delivered through ambulatory surgical centers nationally.” This development highlights the continued emphasis on pushing more complex cases to the outpatient setting through health system joint venture partnerships.

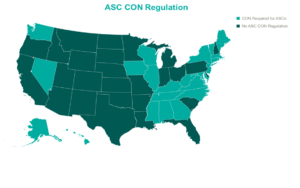

Certificates of Need

In 2023, the landscape of Certificates of Need (CONs) for ASCs underwent notable changes. South Carolina led the way with significant reform, eliminating CON requirements for most health facilities, including ASCs. North Carolina amended its CON law, reflecting a trend toward liberalizing these regulations. North Carolina’s modifications to its CON law specifically targeted easing the process for ASCs and certain medical facilities by adjusting the threshold for review. By raising the financial thresholds for mandatory review, ASCs can undertake significant investments in innovative technologies, expansions, or renovations without the need for a lengthy CON application and review process. The complete repeal of ASC CONs in North Carolina is expected in the coming years. In parallel, Mississippi and Georgia engaged in legislative actions to reevaluate their CON laws as well. Mississippi put forward a provision that would allow Hospitals to establish single-specialty ASCs without the requirement of a CON. Georgia proposed a bill that would eliminate CON requirement for hospitals and establish a unique healthcare service licensure process. With a potential domino effect that could sweep through many states, these regulation changes are important to keep an eye on in the coming years. The relaxation of CON laws may foster growth in the ASC sector with new center development, with more states likely to follow suit in the future, potentially leading to increased access to ASC services and further transformations in healthcare delivery and facility expansion.

The ASC sector experienced significant growth in 2023, driven by factors like industry consolidation, continued shift of care to outpatient settings, and new revelations in the regulatory environments. Key players expanded their operations, reflecting an overall increase in the number of centers managed by national operators. Higher-acuity cases continue the shift into outpatient settings as more procedures are added to the ASC Covered Procedures List. CMS’ policies and reimbursement rates played a crucial role in shaping the sector alongside the evolving landscape of CON regulations. Overall, the ASC market in 2023 demonstrated resilience and adaptability, positioning itself for continued growth and a more significant role in healthcare delivery.