Utilizing Telehealth Services to Improve Access to Behavioral Healthcare

Rachel Linch

August 9, 2022

Written by William Teague, CFA; Justin Vachon; and Ash Midyett, CFA

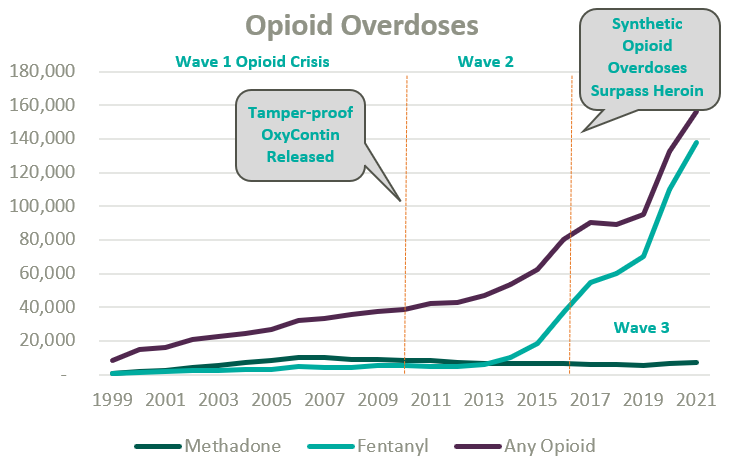

Since the start of the opioid epidemic in the late 1990s, over one million overdoses have been recorded. This figure continues to climb at an accelerated rate following the COVID-19 pandemic and the proliferation of fentanyl. Since 2020, opioid overdoses increased 64%, prompting lawmakers and regulators alike to initiate widespread deregulation and funding of Medication Assisted Treatment (MAT) for Opioid Use Disorder (OUD) to increase access to care amidst what is widely considered a national crisis.1

Medication-assisted treatment (MAT) is a primary method for treating opioid use disorder (OUD) and integrates prescription opioid agonists, which can help manage cravings and withdrawal symptoms, with comprehensive care. Typically, this care combines prescription medications with behavioral health and occupational therapy, drug screenings and occupation advocacy, and other counseling services. MAT can widely be categorized as formal opioid treatment programs (OTPs) and less formalized office-based opioid treatment programs.

OTPs were first established in the mid-1960s from the established medical community’s reluctance to treat the stigmatized patient group and unwillingness to prescribe opioid drugs to those suffering from OUD. Traditionally, OTPs have relied on Methadone, a synthetic analgesic drug similar to morphine, to ease opioid withdrawal symptoms while patients simultaneously attended mental health and occupational counseling.

Office-based opioid treatment (OBOT) refers to outpatient treatment services provided outside of licensed OTPs by clinicians. OBOT treatment allows patients to obtain care at the convenience of their typical primary care provider or local healthcare facilities and does not require comprehensive behavioral health services to be integrated into the delivery model.

Methadone treatment remains the preferred drug type for high-acuity addiction and can be prescribed by a physician, physician’s assistant, nurse practitioner, or clinical nurse specialists, and is typically administered daily through a liquid shot and occasionally as a pill. After a detoxification process at progressive dosing, the patient’s response is typically monitored through a series of physicals. Afterward, maintenance dosages are prescribed on a daily frequency for a recommended one-year period. Methadone may only be distributed through a SAMHSA-certified and DEA-registered OTP clinics.

Since its initial approval by the FDA in 2002, Buprenorphine, a partial opioid agonist, is increasingly relied upon within the OTP and OBOT settings for OUD detoxification and maintenance for less acute addiction. As a partial opioid agonist, Buprenorphine has a lower risk profile than methadone and is thus more widely accessible. For instance, while Methadone may only be distributed in an OTP setting, Buprenorphine can be distributed in an OBOT setting. By market share, Buprenorphine currently dwarfs similar medications for opioid use disorder.2

Because opioid agonists are inherently prone to abuse, regulation of MAT has been historically stringent to prevent further misuse or illicit trade. All OTPs are required to receive full certification by the Substance Abuse and Mental Health Services Administration (SAMHSA), and many states require a Certificate of Need. SAMHSA also regulates prescription protocols and procedures.

On January 31, 2024, SAMHSA made the most impactful change to MAT regulation in decades by finalizing recommendations initiated during the COVID-19 pandemic.3 Most notably, SAMHSA eliminated the one-year OUD qualification and further expanded eligibility for Methadone take-home doses. Additionally, guideline updates granted permanent approval for Buprenorphine telehealth induction without an in-person exam, expanded the definition of “practitioner,” and eliminated the X-waiver requirement, which formerly authorized the outpatient use of Buprenorphine and stipulated patient caps per prescriber.

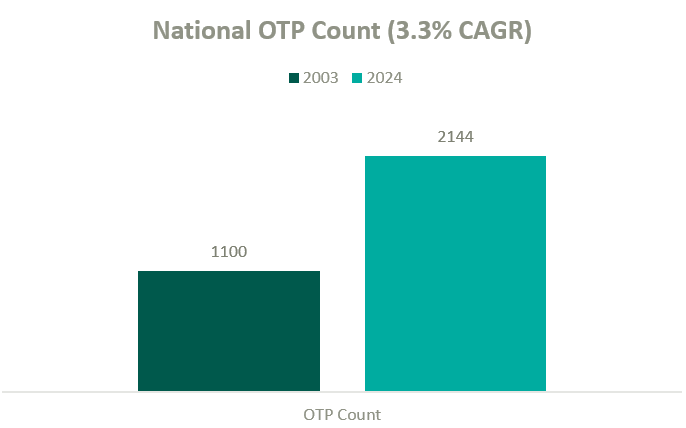

According to the Opioid Treatment Program Directory, patient demand in conjunction with deregulation and clinical advocacy has resulted in a near doubling of OTP clinics nationally over the past two decades. As federal funding and popular outcry grows, OTP growth continues to gain momentum.

The growth in OTPs over the past two decades has resulted in a highly fragmented industry where several notable players hold significant leverage in what will likely become a consolidating market. There are many examples of private equity (PE)–backed companies beginning to participate in merger and acquisition activity in the MAT space.

BayMark Health Services, backed by Webster Equity Partners, claims to be the largest provider of MAT services in North America. BayMark, with over 280 facilities in North America, has acquired over a dozen facilities since the pandemic throughout the U.S.

Acadia Healthcare is the largest publicly traded behavioral health provider in the United States and maintains a significant focus on opioid use disorder. Recent comments from Acadia’s CEO, Chris Hunter, chart an ambitious acquisition strategy to acquire 14 OTPs in fiscal year 2024 after kicking off the year with two MAT acquisitions in North Carolina.4

Key players in the behavioral health industry that are building a presence in the MAT space include, but are not limited to, the following:

Other notable behavioral healthcare providers growing their presence in the industry’s substance use disorder (SUD) and MAT sub-sector include Acadia Health and Universal Health Systems. However, it’s difficult to determine how many stand-alone MAT clinics they have in operation from publicly available information.

Based on data from Irving Levin Associates, Inc., SUD transaction activity has grown significantly over the past decade while having receded marginally from pandemic highs.

MAT clinics operate with a unique reimbursement model compared to other healthcare sectors, and OTPs specifically bill under a set of HCPCS G-Codes. Upon admittance, new patients are billed under an intake code while maintenance visits are reimbursed by the Centers for Medicare & Medicaid Services with bundled payments based on weekly episodes of care.

The table below outlines frequently utilized HCPCS G-Codes for OTP services:

| HCPCS Code | Description of Services |

| G2076 | Intake activities, including medical exam, physical evaluation, initial assessment, and preparation of comprehensive treatment plan. |

| G2067 | Weekly bundle for medication assisted treatment (Methadone). Includes the drug itself, administration, substance use counseling, therapy, and toxicology testing. |

| G2068 | Weekly bundle for medication assisted treatment (Buprenorphine, oral). Includes the drug itself, administration, substance use counseling, therapy, and toxicology testing. |

| G2078 | 7-day, take-home supply of Methadone |

| G2079 | 7-day, take-home supply of Buprenorphine |

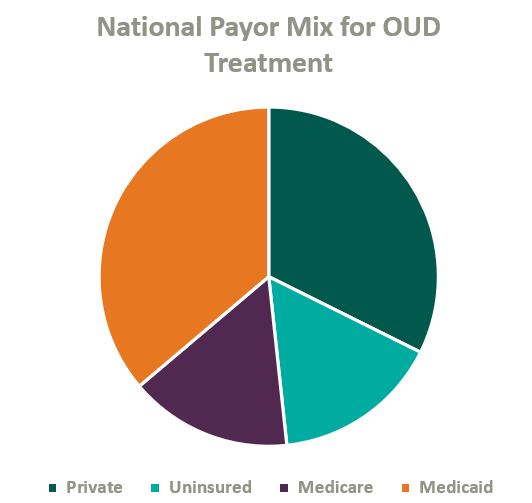

Over the past two decades, Congress has made strides to expand public and private insurance coverage for MAT care. According to the National Survey on Drug Use and Health, roughly 84% of those who suffer from OUD in the United States are covered by some form of insurance (see chart below for total payor mix). Nonetheless, out-of-pocket expense for OUD treatment remains prohibitively expensive for many patients, and sporadic and disparate coverage discourages many operators from accepting insurance. This may change as Congress continues to pass legislation improving affordability of OUD treatment.

On January 1, 2020, Congress passed the SUPPORT Act,5 which established a new Medicare Part B benefit for OUD treatment services provided by OTPs and mandated that all states cover OTP services in their Medicaid programs effective October 1, 2020.6

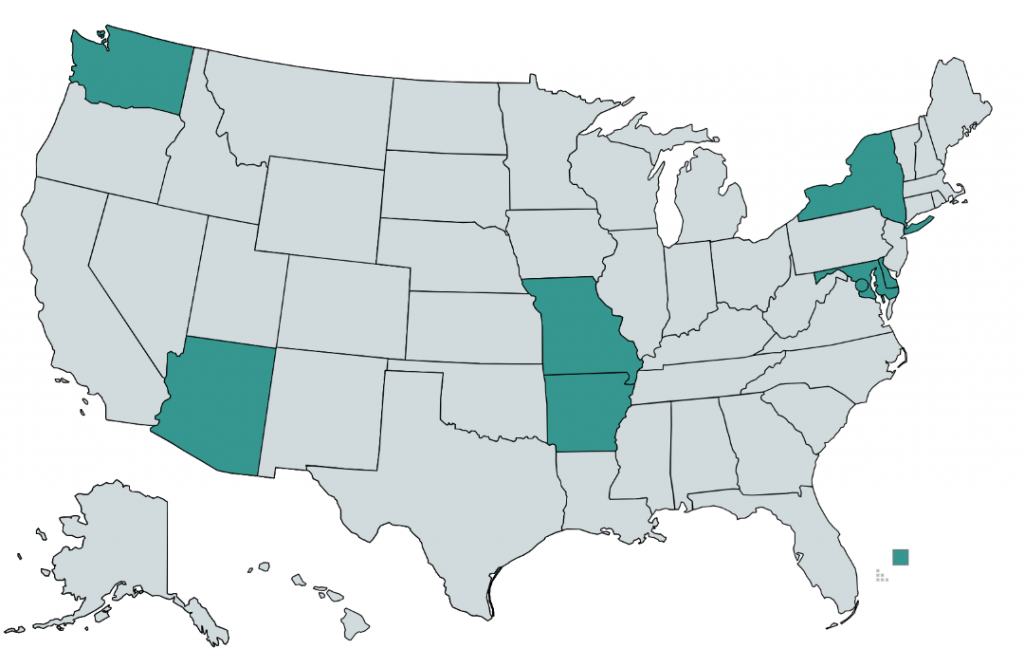

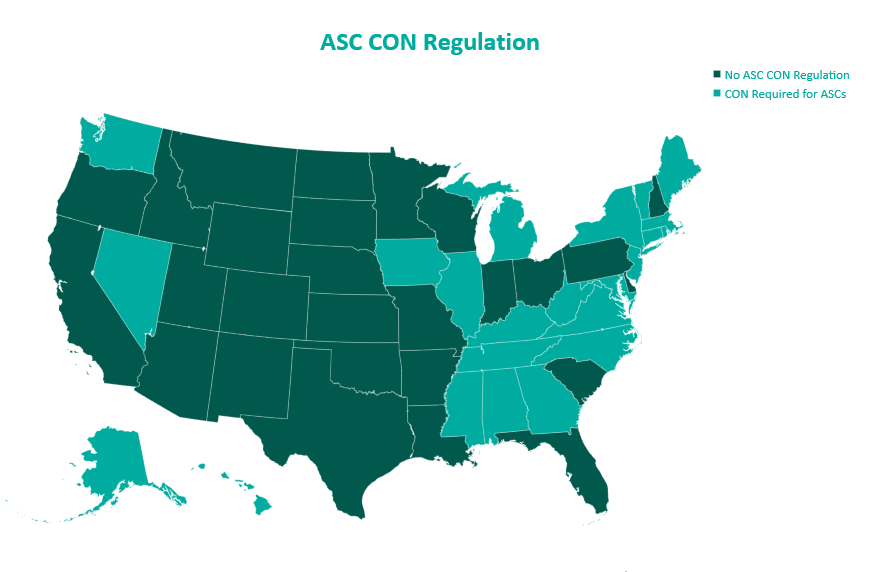

As of 2020, only eight states and the District of Columbia require commercial insurers to provide coverage of medications for opioid use disorder (see map below).7 Although many plans provide coverage regardless of state requirements, coverage is often restricted to a provider network or limited to a cap on services and many MAT clinics choose to pursue an out-of-network or self-pay strategy.8

Grant revenue is critical in lowering out-of-pocket costs for OUD patients and can play a significant role in the operational sustainability of MAT clinics. In 2017, the U.S. Department of Health and Human Serviced committed $485 million in grants to be distributed through SAMSHA, which is intended to increase access for patients, bolster existing MAT operations, and catalyze continued facility expansion.

As access and reimbursement for OUD treatment expands, we expect the supply of care to continue to lag demand for the foreseeable future. In addition, we expect PE-backed platforms to continue consolidating the fragmented industry, driving transaction activity. We also anticipate federal funding, patient inelasticity, and a lack of competition within many markets to fortify pricing while demand continues to attract practitioners into the market—ultimately incentivizing further industry growth and higher valuations.

1 NSC. (2021.) Drug Overdoses. Injury Facts. https://injuryfacts.nsc.org/home-and-community/safety-topics/drugoverdoses/data-details/

2 Faizullabhoy, M. et. al. Opioid Use Disorder Market – By Drug (Buprenorphine [Sublocade, Belbuca, Suboxone, Zubsolv], Methadone, Naltrexone), By Age, By Route of Administration (Intravenous, Oral), By Distribution Channel, Global Forecast 2023-2032. GMI. https://www.gminsights.com/industry-analysis/opioid-use-disorder-market#:~:text=OUD%20Drug%20Market%20Analysis&text=Based%20on%20drug%20type%2C%20the,continue%20during%20the%20forecast%20period

3 SAMHSA. (2024). The 42 CFR Part 8 Final Rule Table of Changes. SAMHSA. https://www.samhsa.gov/medications-substance-use-disorders/statutes-regulations-guidelines/42-cfr-part-8/final-rule-table-changes

4 Larson, C. (2024). Acadia Healthcare CEO: ‘M&A Will Be a Focus for Us in 2024 and Beyond. Behavioral Health Business. https://bhbusiness.com/2024/03/15/acadia-healthcare-ceo-ma-will-be-a-focus-for-us-in-2024-and-beyond/?mkt_tok=NjI3LUNQSy0xNjIAAAGR8QypR-X5kqkF13vlTMemkLPjc9HrQkCohRl5m3BJW-6PGihP1pbXWREONNPExs-ZmjjZapnsDC1-6TKdnqewr8hn5XCGQleZfTGK-JO7lgw

5 CMS. (2020). Opioid Treatment Programs: Enrolling in Medicare. Medicare Learning Network. https://www.cms.gov/files/document/opioid-treatment-program-training-slides.pdf

6 CMS. (2023). Opioid Treatment Programs: Medicaid. https://www.cms.gov/medicare/payment/opioid-treatment-program/medicaid

7 Staff, P. (2020). Commercial Insurance and Medicaid Coverage of Medications for Opioid Use Disorder Treatment. PDAPS. https://pdaps.org/datasets/medication-assisted-treatment-coverage-1580241551

8 Aetna. (2024). Opioid FAQs for individuals and families. https://www.aetna.com/faqs-health-insurance/opioid-faqs.html

Written by Ingrid Aguirre

Update (April 23, 2024): On April 23, 3034 the Federal Trade Commission issued a final rule to generally ban non-compete clauses for most workers. According to the FTC, the final rule will become effective 120 days after publication in the Federal Register.

On January 5, 2023, the Federal Trade Commission (FTC) indicated that it would be proposing a rule to ban non-compete clauses.

Non-compete clauses are industry agnostic and cover a wide gamut of professions. The purpose of a non-compete is to protect the employer’s interest when hiring new employees. The non-compete inhibits an employee from opening a competing business or joining a competing firm within a certain geographical distance and for a certain period. The FTC argues that, in addition to inhibiting competition, non-compete clauses also lower wages for workers who are subject to them as well as workers who are not. The FTC has provisioned an exception to this ban, which would be applicable in the sale of a business where the person subject to a non-compete has an ownership interest of at least 25%.

Within the healthcare industry, physician non-competes are common and often accompany an employment agreement. Whether large health systems or smaller physician groups, many providers are subject to non-competes when employed by these entities. For example, if a physician owner hires two other providers to operate out of her practice, those two physicians may be subject to non-compete agreements. In hiring and training the two new providers, the physician owner may use her eminence in the marketplace, time, patient contacts, and resources to establish the two new providers in the market. Without a non-compete, those two new physicians would be able to join any competing practice nearby to the detriment of their first employer. This problem may become cyclical. The practice that hired those physicians would also be subject to the same risk and, without non-compete agreements, may see those same physicians leave to another competing practice around the corner. VMG Health has been engaged in various situations to determine the value of buying out a non-compete for either litigated matters or transactional matters.

It is important to note, however, that as health systems expand and more physicians are employed by those health systems, it becomes more difficult for physicians to practice out of the geographic limitations set forth by the non-compete if they do choose to leave their employer.

Following this announcement by the FTC, some states have begun moving legislature regarding non-competes. Recently, in January 2024, New York Governor Kathy Hochul vetoed a similar proposal to ban non-competes. Delaware Supreme Court recently ruled in favor of holding non-competes in place in a ruling regarding a financial services company. For example, in California, Oklahoma and North Dakota, non-competes are either not enforceable or outright banned.

The American Medical Association (AMA) echoed the limitations of non-competes noted by the FTC. The AMA supports any policy that would “prohibit covenants not-to-compete for all physicians in clinical practice.”1 The case could also be made for the removal of non-compete agreements due to the current provider shortage around the country.

In drafting non-compete agreements, employers may consider a liquidated damages provision in anticipation of damages. This provision could speak to a reasonable buy-out requirement for a physician seeking to leave and compete nearby. Given the complexities of valuing the buy-out of a non-compete, it is important to engage an expert who understands certain key components: the term of the non-compete, enforceability of the non-compete, the market and competitive landscape, and the financial impact of potential competition.

Across its client base, VMG Health has been engaged to quantify any damages resulting from a client’s workforce leaving for a competitor or to form their own business entity to then compete with their prior employer in the same geographical area. In situations like these, VMG Health has been engaged to determine the value of a non-compete for a litigated matter or for transactional purposes.

It is important to note that the enforceability of physician non-compete agreements can vary depending on the specific language of the agreement, the jurisdiction in which the case is heard, and the facts and circumstances of the case. If you are facing a legal issue related to a physician non-compete agreement, it is imperative to seek legal advice from a qualified attorney and valuation expert who can provide you with personalized guidance based on your situation.

Written by Jordan Tussy, Colin McDermott, and Madi Whyde

Contributing researchers: Bill Jordan, Ryan Mendez, Molly Smith, Rashika Tomar, and Michael Welcer

The public sector often provides valuable insights on broader industry trends, which may be particularly helpful for the private sector in planning for the 2024 calendar year and beyond. VMG Health has identified a select number of companies that operate within the healthcare sector and reviewed the latest earnings calls to develop an understanding of how recent financial and operational trends may provide an indication of future utilization. Identified companies include distributors, equipment suppliers, facility operators, and managed care organizations, all of which are integral in the deployment of healthcare services in the United States and deeply invested in the underlying drivers of future utilization.

We have included some of the most interesting statements made by the leaders of these organizations below.

For medical equipment suppliers and distributors, 2024 predictions were primarily driven by 2023’s utilization, with many companies reporting continued growth over 2023 due to persisting patient backlogs.

“…Average system utilization [procedures per installed clinical system] continues to be above long-term trends, increasing by 9.0% for the full year of 2023. Higher system utilization reflects both a higher mix of shorter-duration, benign procedures and the need to address patient backlogs.” – Jamie E. Samath, Senior Vice President and Chief Financial Officer, Intuitive Surgical, Inc. FQ4 Earnings Call, January 23, 2024.

“During the quarter, we saw strong procedural demand… Additionally, demand for our capital products remained very robust in the quarter, with double-digit organic growth in Medical, Instruments and Endoscopy.” – Jason Beach, Vice President of Investor Relations, Stryker Corporation. FQ4 2023 Earnings Call, January 30, 2024.

“Second quarter revenue increased 3.0% to $3.9 billion, which, as Jason alluded to, reflects quarterly revenue growth for the Medical segment for the first time in over two years. This increase was driven by growth in both at-home solutions and global medical products and distribution…” – Aaron E. Alt, Chief Financial Officer, Cardinal Health, Inc. FQ2 2024 Earnings Call, February 1, 2024.

“There is a bolus of patients coming out into the market after COVID-19, which has made 2023 market growth faster than historical averages.” – Joaquin Duato, Chief Executive Officer and Chairman, Johnson & Johnson. FQ4 2023 Earnings Call, January 23, 2024.

As key customers of medical equipment suppliers and distributors, healthcare operators mirrored their observations of continued growth in utilization, particularly in the fourth quarter of 2023.

“But at a structural level, there is nothing to suggest that our surgical volume trends are going to change for the year, we had really solid volume growth in surgery. And we continue to invest heavily in our programs, both on the outpatient side and supporting our inpatient activity with more acute in complex program offerings.” – Samuel N. Hazen, Chief Executive Officer and Director, HCA Healthcare, Inc. FQ4 2023 Earnings Call, January 30, 2024.

“We finished the year strong and delivered results in the fourth quarter that were well above the expectations we set. This was driven by continued volume strength as well as cost and utilization management.” – Saum Sutaria, Chairman and Chief Executive Officer, Tenet Healthcare Corporation. FQ4 2023 Earnings Call, February 8, 2024.

These companies were also consistent in crediting the elevated utilization trends to volume growth in a few key specialties.

“As we have noted, we believe that in 2023, we saw recovery in demand that included some impact from deferred volume, particularly in GI and ENT services. – Saum Sutaria, Chief Executive Officer, Tenet Healthcare Corporation. FQ4 2023 Earnings Call, February 8, 2024.

“Throughout the year, we saw ongoing strength and recovery in GI, urology and ENT procedures. This organic growth was driven by continued expansion of service lines and growth in our population of partnered and affiliated physicians as well as the fundamental tailwinds of patient demand for safe and convenient surgical care options.” – Saum Sutaria, Chief Executive Officer, Tenet Healthcare Corporation. FQ4 2023 Earnings Call, February 8, 2024.

“Starting first with procedures, growth for the full year was 22.0%. Areas of strength included general surgery in the United States… In the U.S., general surgery procedure growth was led by cholecystectomy, with foregut procedures rising as well. Colon and hernia procedure growth was also healthy for the year. Bariatric procedures grew year-over-year.” – Gary S. Guthart, Chief Executive Officer and Director, Intuitive Surgical, Inc. FQ4 2023 Earnings Call, January 23, 2024.

While volume recovery resulted in top line revenue growth for operators and their vendors, payors expressed higher-than-expected medical costs driven by the strong utilization.

“…In the non-inpatient space, despite the recent decline in observation events, we saw a sequential uptick in overall medical cost per member per month (PMPM) in the fourth quarter, driven largely by increases in physician, outpatient surgical and supplemental benefits cost categories.” – Humana Inc. Fourth Quarter 2023 Prepared Management Remarks, January 25, 2024.

“Care patterns remain consistent with those we shared with you in the first half of ‘23. Activity levels continue to be led by outpatient care for seniors—with orthopedic and cardiac procedure categories among the more prominent. As we’ve noted, our benefit design approach assumed these activity levels persist throughout ’24, and the care patterns we observed exiting ’23 reconfirm that decision.” – John Rex, Chief Financial Officer, UnitedHealth Group. FQ4 2023 Earnings Call, January 12, 2024.

The companies were nearly unanimous in their expectations that 2023 growth trends will persist throughout 2024, driven by the elevated backlogs, stabilizing macroeconomic trends, and an aging population.

“We project MedTech operational sales growth to be relatively consistent throughout the year, expecting procedures in 2024 to remain above pre-COVID levels.” – Joseph J. Wolk, Executive Vice President and Chief Financial Officer, Johnson & Johnson. FQ4 2023 Earnings Call, January 23, 2024.

“And we see that trend [faster market growth post-COVID] continuing into a good part of 2024. And therefore, being a tailwind into 2024. There’s a lot of factors playing into that. But overall, we see the amended procedures continuing into, at least, the first half of 2024.” – Joaquin Duato, Chief Executive Officer and Chairman, Johnson & Johnson. FQ4 2023 Earnings Call, January 23, 2024.

“…We continue to see an increased volume of procedures in orthopedics based on coming out of COVID. And we don’t see any change in that, neither in the hips or in the knee area, or in any of the segments that we compete. So, we are optimistic about our orthopedics trajectory.” – Joaquin Duato, Chief Executive Officer and Chairman, Johnson & Johnson. FQ4 2023 Earnings Call, January 23, 2024.

“So, embedded in the guidance for 2024, which we’re very confident on the 5.0% to 6.0%, is macro and micro reasons. So, from a macro perspective… the markets are going to continue to be healthy. You got better patient demographics, younger patients, you got the dynamic of cases moving into an ASC… You’ve seen shorter, better rehabilitation processes.” – Ivan Tornos, Chief Operating Officer, President, Chief Executive Officer, and Director, Zimmer Biomet Holdings, Inc. FQ4 2023 Earnings Call, February 8, 2024.

“The size of our pipeline is twice what it used to be in 2018… This is not the same market growth profile that we used to have. Patient demand is strong. Procedure volume is very strong given a variety of reasons.” – Ivan Tornos, Chief Operating Officer, President, Chief Executive Officer, and Director, Zimmer Biomet Holdings, Inc. FQ4 2023 Earnings Call, February 8, 2024.

“Procedure volumes are strong. The capital markets are very strong. Hospitals are spending. We have exited the year with more backlog than we began the year, which means, obviously, our orders are continuing to be strong for capital equipment.” – Kevin A. Lobo, Chairman, Chief Executive Officer, and President, Stryker Corporation. FQ4 2023 Earnings Call, January 30, 2024.

“We continue to expect the ortho markets will remain strong in 2024, driven by continued adoption in robotic-assisted surgery, demographics, a more favorable pricing environment, and healthy patient activity levels with surgeons… Hospital CAPEX budgets remain healthy, and our capital order book remains elevated as we enter 2024.” – Jason Beach, Vice President of Investor Relations, Stryker Corporation. FQ4 2023 Earnings Call, January 30, 2024.

“Based on our momentum from 2023, strong procedural volumes, healthy demand for capital products, and a stabilizing macro-economic environment, we expect 2024 organic net sales growth to be in the range of 7.5% to 9.0%.” – Glenn S. Boehnlein, Vice President and Chief Financial Officer, Stryker Corporation. FQ4 2023 Earnings Call, January 30, 2024.

“…Our overall procedure guidance range assumes that growth moderates from last year, given the elevated backlog benefit we experienced in 2023.” – Brian King, Head of Investor Relations, Intuitive Surgical, Inc. FQ4 2023 Earnings Call, January 23, 2024.

“…Utilization continues to be quite good and predictable. So, we’re in a nice environment for ongoing growth…” – Jason M. Hollar, Chief Executive Officer and Director, Cardinal Health, Inc. FQ2 2024 Earnings Call, February 1, 2024.

“The volume strength was also very good during the year. And so, I think that we believe that we’ll continue to see acute care recovery in 2024 like we saw in 2023. And if we’re able to open up capacity effectively to service the demand that we want, which again is consistent with our high acuity strategy, I think that’s what gets us to the upper end of our guidance, right? It’s really the volume potential there.” – Saum Sutaria, Chief Executive Officer, Tenet Healthcare Corporation. FQ4 2023 Earnings Call, February 8, 2024.

“…I think we’re reading continued strong demand. We saw really strong enrollment in the health insurance exchanges across our states… We believe we continue to see strong economic indicators and employments and our access to contracted lives remaining well.” – William B. Rutherford Executive VP and Chief Financial Officer, HCA Healthcare. FQ4 2023 Earnings Call, January 30, 2023.

“…We are really judging our business and thinking about 2024 optimistically around where the demand for healthcare is at least in our markets.” – Samuel N. Hazen, CEO and Director, HCA Healthcare. FQ4 2023 Earnings Call, January 30, 2023.

“Our initial assumption for volume growth assumes that volume will build as the year progresses, reflecting the historically high same-store case growth that we saw in the first quarter of 2023. We are very confident in the long-term growth rates of this business.” – Saum Sutaria, Chief Executive Officer, Tenet Healthcare Corporation. FQ4 2023 Earnings Call, February 8, 2024.

“Given the recency and magnitude of the uptick in the utilization trend, we have prudently assumed that the higher costs seen in the fourth quarter persist throughout 2024. Based on our review of our initial claims data, we believe that the seasonal factors are not driving the increase.” – Bruce Dale Broussard, Chief Executive Officer and Director, Humana Inc. FQ4 2023 Earnings Call, January 25, 2024.

“Looking at January data, which is very early—so we only have really some look into the first two weeks—we would say [utilization] is continuing to stay at the elevated levels that we saw in the fourth quarter.” – Susan Marie Diamond, Chief Financial Officer, Humana Inc. FQ4 2023 Earnings Call, January 25, 2024.

The prevailing theme noted in the earnings calls VMG Health reviewed pertained to the elevated utilization in 2023 and its persistence into 2024. Particularly notable were the trends around volumes recovering post-COVID (especially for otolaryngology, orthopedics, and urology services). This was coupled with a recovering macroeconomic environment and favorable patient dynamics. While an encouraging trend for operators, device companies and distributors, higher utilization translated to increased medical claims on the payor side.

Based on this commentary and insight from the public sector, the VMG Health team is optimistic that 2024 will be a strong utilization year for our healthcare service provider clients.

Written by Ben Minnis, Tyler Navarro, and Anthony Domanico

With significant changes to the Medicare Physician Fee Schedule (MPFS) in recent years and an aging physician population leading to potentially significant shortages of over 100,000 physicians by 2030,1 how organizations recruit and retain these key healthcare providers continues to evolve and become more competitive. As we hit the midway point of 2024’s first quarter, VMG Health’s experts have identified important trends in physician enterprise strategy that will impact the physician landscape in 2024 and beyond.

In today’s competitive recruitment landscape, organizations are innovating their approaches to attract and retain top physician talent. Beyond traditional compensation packages, which still include higher pay and signing bonuses in specialties facing shortages, institutions are prioritizing lifestyle enhancements like flexible scheduling and remote work options. Institutions are also promoting several non-traditional benefits and enhancements that attract and retain physicians:

The era of one-size-fits-all compensation models in multispecialty healthcare is coming to an end. As service lines within healthcare delivery settings evolve, so do their operational dynamics and corresponding compensation structures. Each service line has unique requirements, such as call coverage, sub-specialization (e.g., heart failure, ERCP), and supervision of advanced providers, among others. Attempts to enforce rigid standardization across various specialties within a physician enterprise are increasingly impractical and counterproductive in today’s complex landscape. Instead, organizations are recognizing the need to tailor compensation models to suit specific circumstances. Striking a balance between innovation and standardization is key for organizations seeking to optimize their compensation frameworks, as evidenced by VMG Health’s experience working with a variety of organizations and approaches.

Physicians are placing an increasing emphasis on achieving a healthier work-life balance. This shift in priorities is prompting healthcare organizations to reassess and refine their compensation packages to better align with the needs of modern physicians. Flexible scheduling options, including compressed work weeks or part-time arrangements, are gaining popularity because they allow physicians to better manage their time and commitments outside of work. Moreover, the widespread adoption of telemedicine has opened new avenues for physicians to practice medicine remotely, offering them greater flexibility in how and where they work. Additionally, paid time off (PTO) allowances are expanding to ensure physicians have ample opportunity for rest, relaxation, and personal pursuits.

A 2023 survey by Merritt Hawkins2 asked final year medical residents, “What is important to you as you consider practice opportunities?” Notably, 82% of respondents marked “lifestyle” as very important, indicating a clear preference for work arrangements that afford them the time and freedom to pursue personal interests and maintain a healthy work-life balance. Similarly, 80% of respondents cited the importance of having adequate personal time. Financial considerations remain unsurprisingly significant, with 78% of respondents emphasizing the importance of a good financial package. However, it is more and more evident that the pursuit of a fulfilling lifestyle and sufficient personal time are increasingly taking precedence in the minds of physicians when evaluating practice opportunities. This trend underscores the importance for healthcare organizations to adapt their compensation strategies to meet the evolving needs and priorities of today’s medical professionals.

The Centers for Medicare & Medicaid Services (CMS) have continued to delay implementation of proposed changes to the time-only definition of “substantive portion” of a split/shared E/M visit in the facility setting until December 31, 2024. Delays are due to a reportedly large backlash by facilities, with concerns over care team disruptions and issues with integrating a time-based rule into billing and EHR systems.

While VMG Health anticipates additional delays or even changes to the policy, it would be wise for organizations to prepare inpatient care models and related compensation models to ensure a proper plan is in place—or could quickly be implemented—when final rule changes do take effect.

In contemporary compensation structures, non-productivity incentives often include a substantial portion of compensation tied to high-quality metrics, ideally serving as a significant motivator and leading to better patient outcomes. While certainly not limited to a 2024 trend, forward-thinking organizations are continuing to leverage compensation design initiatives to bolster their ACO/CIN strategies, particularly those with health plans and/or substantial capitation risk within their payor contracts. As these organizations assume greater risk, compensation models can be tailored to distribute value-based earnings among physicians.

While physician shortages and increased demand continue to drive organizations to innovate compensation models and incentives, it’s crucial to operate within regulatory boundaries and adhere to laws governing healthcare practices. This point is underscored by recent cases, such as the one involving Community Health Network Inc., which agreed to pay $345 million to settle allegations of violating the False Claims Act by unlawfully submitting Medicare claims.3 The lawsuit alleged that Community Health Network overpaid specialists and awarded bonuses tied to referrals, ignoring warnings and providing false compensation figures. The settlement includes a five-year Corporate Integrity Agreement with HHS-OIG. The case originated from a whistleblower complaint filed in 2014. The government’s intervention underscores its commitment to combat healthcare fraud using tools like the False Claims Act.

In FY2022, the U.S. Justice Department collected $2.2 billion in settlements and judgments, the second-highest amount ever recorded in a single year. These statistics underscore the critical need for maintaining vigilance and compliance, particularly in an environment where regulatory scrutiny is significant.

Health systems are increasingly turning to advanced practice providers (APPs) as a strategic solution to address the pervasive challenges of physician shortages. Unlike for physicians, where organizations are competing nationally for talent, supply and demand trends for APPs are driven by local factors.

The rise of nurse practitioners, physician assistants, and other APPs is seen as a pragmatic response to the growing demand for healthcare services. These providers bring advanced education and training, offering a multifaceted approach to patient care that aligns with the evolving needs of modern healthcare. Organizations are looking to APPs for cost-effectiveness and because APP training programs are generating a higher number of graduates than medical schools. This allows organizations to fill needed vacancies quicker while considering changes to the care model that will drive down the total cost of care.

With competitive recruitment strategies and tailored compensation packages, health systems recognize the crucial role that APPs play in ensuring the continued delivery of high-quality and accessible healthcare services. This collaborative model enhances patient access, care coordination, and overall efficiency and fosters a supportive work environment where professionals can learn from one another and leverage their respective skills and expertise.

The trends shaping provider compensation in 2024 reflect a strategic response to ongoing challenges like physician shortages, regulatory constraints, and evolving workforce preferences. Physician enterprises will continue to face these challenges from a care model and compensation model perspective. VMG Health’s experts in physician enterprise strategy and compensation design can help your organization establish and refine your physician enterprise strategy to ensure your organization’s continued ability to recruit and retain top physician and APP talent.

1 Chakrabarti, R., et. al.(2021). The Complexities of Physician Supply and Demand: Projections from 2019 to 2034. American Association of Medical Colleges. https://www.aamc.org/media/54681/download?attachment.

2 AMN Healthcare. (2023). Survey of Final Year Medical Residents. https://www.amnhealthcare.com/siteassets/amn-insights/surveys/survey-of-final-year-medical-residents-2023.pdf

3 United States Department of Justice. (2023). Indiana Health Network Agrees to Pay $345 Million to Settle Alleged False Claims Act Violations. https://www.justice.gov/opa/pr/indiana-health-network-agrees-pay-345-million-settle-alleged-false-claims-act-violations

Written by Jordan Tussy, CVA; Hunter Hamilton; and Vincent Kickirillo, CVA, CFA

Following the emergence of several oncology private equity (PE)–backed platforms in 2018, there has been an uptick of tuck-in acquisition activity in the oncology space, both by these PE-backed entities, as well as by other prominent public and corporate-backed oncology platforms. These platforms have targeted geographic expansion and economies of scale through strategic affiliations with practices and physicians.

In fact, a Harvard study published in JAMA Internal Medicine indicated that over 700 oncology practices had partnered with or had been acquired by a PE firm from 2003 to 2022. According to the study, this number represented approximately 10% of total oncology practice locations in the US.

While increased regulatory scrutiny and a more difficult funding environment have hampered overall physician practice transaction activity, several notable platform and tuck-in acquisitions have defined the recent environment for investment in oncology.

After a quiet couple of years from Pharos Capital Group’s Verdi Oncology, it was announced in November 2023 that the platform’s two practices, Nashville Oncology Associates and Horizon Oncology, had joined The US Oncology Network. Additionally, Verdi Cancer and Research Center of Texas, formed in August 2019, announced its closure in September 2023. With Verdi Oncology having been founded in March 2018 through the initial acquisition of Horizon Oncology, Pharos Capital Group’s assumed exit after nearly six years aligns with typical PE holding period expectations.

Perhaps most notable among recent transactions in the oncology space was the $2.1 billion acquisition of OneOncology from General Atlantic by TPG and AmerisourceBergen Corporation, which closed in June 2023. TPG will be the majority owner in the new joint venture, as AmerisourceBergen reportedly purchased a minority interest of approximately 35% for around $685 million in cash. TPG also has a one-year put option effective on the third anniversary of the deal closing. If exercised, this option would require Amerisource Bergen to purchase the remaining interest in OneOncology at a price equal to 19.0x the company’s adjusted EBITDA for the most recently ended 12-month period. AmerisourceBergen will also have a call option to purchase the remaining interest at the same price between the third and fifth anniversaries. Applying the 19.0x multiple to the transaction price of $2.1 billion would imply approximately $110 million of EBITDA for OneOncology today.

General Atlantic originally invested $200 million in OneOncology in September 2018 and held the investment for nearly five years. In that time, OneOncology has expanded considerably in both size and geography. The platform now includes 19 practices across 15 states with just under 1,000 providers. The structure is that of an affiliation model in which OneOncology charges a management fee and introduces partner practices to new ancillaries (e.g., oral pharmacy, laboratory services, radiation therapy) as well as lower drug-purchasing costs. Providers further benefit from a reduction in administrative burden and a resulting increase in clinical autonomy. In addition, OneOncology also has robust data analytics capabilities, which it utilizes to help define better clinical pathways, improve outcomes, and monetize the data.

Since the announcement of OneOncology’s acquisition by TPG and AmerisourceBergen in April, several additional practice partnerships have been announced, including the affiliation of Coastal Cancer Center and Pacific Cancer Care in May, Mid Florida Cancer Centers in November, and Pacific Cancer Medical Center, Maury Regional Medical Group, and Genesee Cancer and Blood Disease Treatment Centers in December. On January 12, 2024, it was announced that OneOncology had finalized a partnership with Huntsville, Alabama–based Clearview Cancer Institute, which—with 25 medical oncologist providing care across 13 clinics—was identified in the announcement as one of the five largest community oncology practices in the nation and the largest in Alabama.

After its recapitalization by Silver Oak Services Partners in October 2018, Integrated Oncology Network (ION) has continued its geographic expansion and now operates from more than 50 centers across 14 states in the US. Like OneOncology’s model, the independence of partner practices is also maintained under ION’s model, which, in addition to the preservation of clinical autonomy, offers to reduce the regulatory burden and increase access to the enhanced technology and resources of a larger network. ION specifically advertises its fully supported EHR and the immediate access its providers have to accurate data analytics. Most notably, in April 2022, ION announced the acquisition of California Cancer Associates for Research and Excellence (cCARE), an integrated cancer care network that provides medical oncology, radiation oncology, diagnostic imaging, and other ancillary services in the Fresno and San Diego markets. Furthermore, the platform expanded its cCARE operations with the September 2023 acquisition of High Desert Oncology of Victorville, California as well as the December opening of its new clinic in Riverside, California.

KKR-backed GenesisCare filed for Chapter 11 bankruptcy in June 2023, announcing that its US operations would be spun out from the broader enterprise. At the time of the announcement, David Young, CEO of GenesisCare, said, “The past three years have presented significant operational and financial challenges, requiring a comprehensive restructuring of the operations and balance sheet of the company.” No disruption of patient care was anticipated, and in November 2023, it was reported that GenesisCare had developed a reorganization plan to reduce its debt load by approximately $1.7 billion, down from the $2.0 billion it had at the time of filing. The US segment will continue to operate as a sister company to the businesses in Australia, Spain, and the UK, as the enterprise entertains interest from potential buyers.

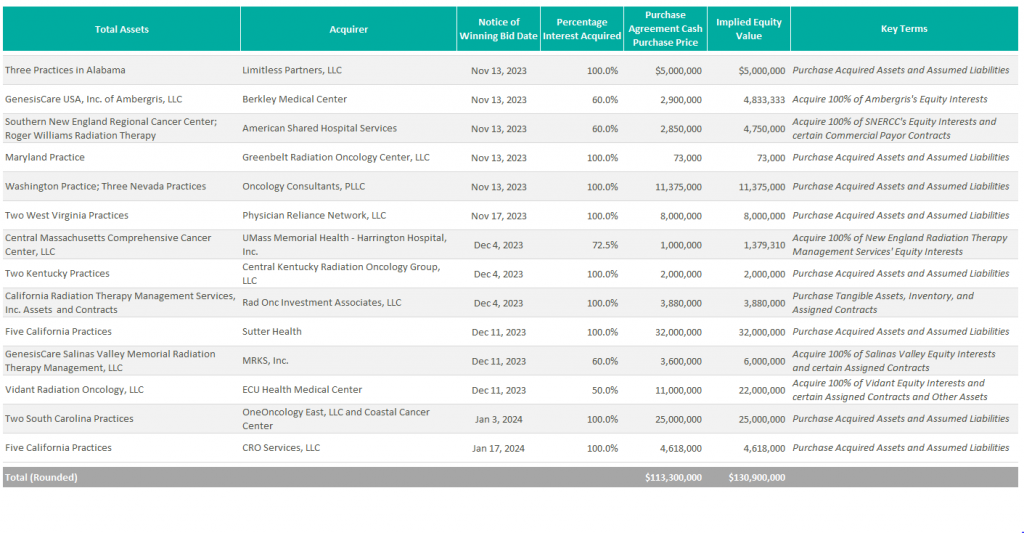

According to bankruptcy filing documents, a number of winning bids for GenesisCare assets across the country have already been announced. Assuming these transactions close at the indicated prices (as defined in the respective purchase agreements), it would imply total cash proceeds of over $100 million. Furthermore, the sales of these 31 practices have an implied consolidated equity value of approximately $131 million.

Additionally, it was announced in October 2023 that GenesisCare’s Orange County radiation oncology centers were acquired by UCI Health.

New to the scene is Oncology Care Partners (OCP). Backed by Welsh, Carson, Anderson, & Stowe’s healthcare platform, Valtruis, and partnering with oncology and cardiology care management provider Evolent Health, OCP opened its first two practices in Phoenix and Miami in January 2023 with the goal of advancing value-based care, particularly among Medicare Advantage patients. Based on the launch announcement of these first two practices, OCP appears to operate a hybrid model of practice partnership. The launch of its Arizona practice came in partnership with American Oncology Network, while its Miami-based medical group practice appears to have been an outright acquisition. Under both agreements, OCP says it will provide value for payors and at-risk primary care groups through the introduction of a new patient journey and digital tools to allow community providers to spend more time with their patients and reduce barriers to access. With the launch of its most recent location in Broward County, Florida in October 2023, OCP plans to continue expansion efforts across the country to further accelerate its value-based care initiatives.

McKesson’s The US Oncology Network (The Network) has also remained active expanding its footprint in California, New Mexico, and Kansas with the 2023 acquisitions of Epic Care, Nexus Health, and Cancer Center of Kansas, respectively. In April 2023, The Network also announced a strategic partnership with Regional Cancer Care Associates, a multispecialty oncology with more than 20 sites of service and over 60 providers throughout the Northeast. As previously mentioned, it was announced in the fourth quarter that Verdi Oncology’s Nashville Oncology Associates and Horizon Oncology had joined The Network as well. Under The Network’s affiliation model, the operational and clinical activities of its partner practices are converted to value-based care through greater focus on the negotiation of value-based contracts for revenue optimization, empowerment of practice transformation with proven solutions, alignment of GPO and payer contracts, and support for all oncology specialties. As of the most recent transactions, The US Oncology Network’s total provider count exceeds 2,400.

Previous stand-alone operator Cancer Treatment Centers of America (CTCA) was acquired by City of Hope in February 2022 for $364.4 million. At the time of its acquisition, the business operated three oncology hospitals located in Atlanta, Chicago, and Phoenix, as well as five outpatient facilities. On the one-year anniversary of the transaction, it was announced that CTCA was officially being re-branded to bear the City of Hope name at its facilities, further cementing the evolution of the organization into a national system.

In April 2023, American Oncology Network (AON) received a $65 million strategic growth investment from AEA Growth Partners “to help further AON’s goals of supporting community practices and improving the patient experience,” according to the Company’s press release. As a result of the investment, AEA Growth gained a minority interest in the business. AON opened Lone Star Oncology in Georgetown, Texas in June and announced the affiliation with Florida Oncology & Hematology in Safety Harbor, Florida in July. AON also ventured into urology through its affiliation with Triple Crown Urology on September 1. As a result of this transaction, AON’s platform now includes over 200 providers across 85 locations in 19 states and the District of Columbia. AON has a partnership model through which affiliated practices enter a management agreement and are charged a central services fee. Synergies realized through a partnership with AON are advertised as new revenue streams through centralized ancillaries, including oral pharmacy, clinical lab, and pathology as well as economies of scale with vendor services and drug pricing. With such revenue enhancements and cost reductions, providers can earn more than they otherwise might have as independent practices.

Most notable among AON’s recent transaction activity was the closing of a business combination with Digital Transformation Opportunities Corp., a special purpose acquisition company (SPAC), in September 2023. As a result of the transaction, AON began trading on the Nasdaq on September 21, 2023 under the ticker AONC. The transaction had an implied enterprise value of $497 million, with an implied TEV/Revenue multiple of 0.4x and an implied TEV/EBITDA multiple of 13.8x.

In November 2021, The Oncology Institute (TOI) was acquired by DFP Healthcare Acquisitions Corp., a SPAC, and became the first publicly traded oncology company. At the time of the acquisition, TOI’s pro forma enterprise value was $842 million. Underperforming initial expectations, the company ended 2023 with an enterprise value of approximately $148 million. To address these issues, TOI completed a corporate restructuring in Q2 2023 and has a strategic plan to eliminate cash burn and generate positive adjusted EBITDA by the end of 2024. According to their most recent earnings call, the company also plans to improve margins in legacy markets through expansion in capitated partnerships, radiation oncology, and clinical trials program. As part of this initiative, TOI acquired Southland Radiation Oncology Network in June 2023, which includes five radiation oncology clinics in the Los Angeles market. Despite the operational difficulties, The Oncology Institute remains the largest value-based care oncology operator in terms of lives served and revenue under value-based arrangement. To advance these efforts, The Oncology Institute acquires and employs the providers of its partner practices. The synergies it promotes include access to clinical trials, transfusions, and additional care delivery models more typically associated with the most advanced care delivery organizations.

Burdened with reimbursement headwinds and rising costs, it is anticipated that oncologists will continue to seek out strategic affiliations. Platforms such as OneOncology and The US Oncology Network offer an attractive alternative that allows physicians to maintain their independence while receiving the infrastructure and growth support of a large entity.

Furthermore, the long-term performance of major players in the oncology value-based care space remains to be seen, as does The Oncology Institute’s ability to achieve on its path to profitability in 2024.

Lastly, with the acquisition of OneOncology, ION is one of the last pureplay, PE-backed oncology platforms that has yet to recapitalize. Given Silver Oak Services Partners has held onto this investment for over five years now, it would not be surprising if there was a recapitalization of this platform within the next couple of years.

Silver Oak Services Partners LLC. (2023). Integrated Oncology Network acquires California Cancer Associates for research & excellence. PR Newswire. https://www.prnewswire.com/news-releases/integrated-oncology-network-acquires-california-cancer-associates-for-research–excellence-301530782.html

Integrated Oncology Network. (2023). Integrated Oncology Network announces High Desert Oncology joins cCare. PR Newswire. https://www.prnewswire.com/news-releases/integrated-oncology-network-announces-high-desert-oncology-joins-ccare-301933873.html

Integrated Oncology Network. (2023). Integrated Oncology Network announces cCare expansion with specialty clinic in Riverside, California. PR Newswire. https://www.prnewswire.com/news-releases/integrated-oncology-network-announces-ccare-expansion-with-specialty-clinic-in-riverside-california-302009492.html

Sebastian, D. (2023). KKR-Backed Radiotherapy Group GenesisCare Files for Bankruptcy. Wall Street Journal. https://www.wsj.com/livecoverage/stock-market-today-dow-jones-06-01-2023/card/kkr-backed-radiotherapy-group-genesiscare-files-for-bankruptcy-LIVUzBoTLS8Z2Z8qPcP9

GenesisCare. (2023). GenesisCare’s Plan of Reorganization Confirmed by Bankruptcy Court with Overwhelming Support from Voting Creditors. GenesisCare Newsroom. https://www.genesiscare.com/us/news/genesiscares-reorganisation-plan-confirmed-with-overwhelming-support-from-voting-creditors

UCI Health. (2023). UCI Health purchases GenesisCare radiation oncology centers. UCI Health News. https://www.ucihealth.org/news/2023/10/fountain-valley-radiation-oncology#:~:text=Acquisition%20expands%20access%20to%20world,cancer%20care%20in%20Orange%20County&text=Orange%2C%20Calif.,filed%20for%20Chapter%2011%20bankruptcy.

American Shared Hospital Services. (2023). American Shared Hospital Services Enters Into Agreement to Acquire 60% Majority Interest in Three Radiation Therapy Cancer Centers in Rhode Island. GlobeNewsWire. https://www.globenewswire.com/news-release/2023/11/20/2783147/0/en/American-Shared-Hospital-Services-Enters-Into-Agreement-to-Acquire-60-Majority-Interest-in-Three-Radiation-Therapy-Cancer-Centers-in-Rhode-Island.html

United States Securities and Exchange Commission. (2023). Form 8-K for American Shared Hospital Services. https://app.quotemedia.com/data/downloadFiling?webmasterId=101803&ref=317881267&type=PDF&symbol=AMS&cdn=1833bea1c9c3490a4573fbbc20a1fc5e&companyName=American+Shared+Hospital+Services&formType=8-K&formDescription=Current+report+pursuant+to+Section+13+or+15%28d%29&dateFiled=2023-11-21

Oncology Care Partners. (2023). Oncology Care Partners Launches First Three Locations, Bringing Patient Experience Focus to Cancer Care in Phoenix, Miami. PR Newswire. https://www.prnewswire.com/news-releases/oncology-care-partners-launches-first-three-locations-bringing-patient-experience-focus-to-cancer-care-in-phoenix-miami-301724825.html

Oncology Care Partners. (2023). Oncology Care Partners Launches Broward Location Expanding Value-Based Cancer Care in South Florida. PR Newswire. https://www.prnewswire.com/news-releases/oncology-care-partners-launches-broward-location-expanding-value-based-cancer-care-in-south-florida-301947441.html

American Oncology Network. (2023). American Oncology Network, a Rapidly Growing Network of Community-Based Oncology Practices, Receives Strategic Investment from AEA Growth. American Oncology Network News. https://www.aoncology.com/2023/04/28/american-oncology-network-receives-strategic-investment-from-aea-growth/

Written by Dylan Alexander, CVA and Gerrit Elzinga, CVA

As of January 2024, Definitive Healthcare reports that there are over 338,000 physician group practices in the United States. In an independent physician practice, shareholder physicians typically take home all earnings of their business and have discretionary expenses. The compensation package of the shareholder physicians negotiated during a transaction often differs from the compensation structure of the practice pre-transaction and should be taken into consideration in the valuation of a physician practice. An inverse relationship often exists between physician compensation and the valuation of independent physician groups. This means that higher post-transaction physician compensation results in less available earnings for the practice owners to sell, ultimately leading to a lower valuation for the physician practice. Post-transaction physician compensation structure plays a significant role in the value of physician practices.

There are many forms of physician compensation. Here are a few of the most common types:

Physician compensation levels vary from practice to practice. As previously mentioned, shareholder physicians typically take home all practice earnings; therefore, the post-transaction compensation structure will determine whether the subject practice has earnings or compensation to monetize in a transaction. Numerous factors determine whether physicians have compensation available to sell. Productivity and reimbursement are the main components for driving fee-for-service revenue at a physician practice. Practices with productive physicians, favorable reimbursement, and ancillary service offerings generate higher revenue, which results in increased profitability. Furthermore, practices that effectively leverage mid-level providers tend to have greater profitability than those that do not, as mid-level providers deliver many of the same services at a fraction of the cost. Expense management is key; a practice overburdened with operating expenses will be less profitable. For certain practices, historical physician compensation and its attributes may not leave meaningful earnings to sell.

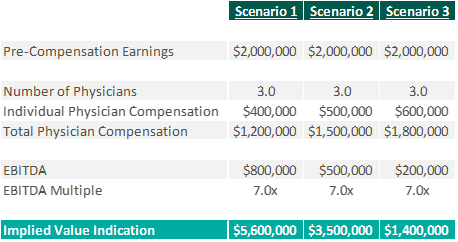

Physician practices are most often valued utilizing three methodologies: income approach, cost approach, and market approach. The income approach considers the future earning potential of a physician practice and discounts the projected cash flows back to its present value. The value of a physician practice is sensitive to the total amount of physician compensation and how that compensation is structured. The greater the physician compensation, the lower the projected free cash flows will be. Ultimately, a high level of post-transaction physician compensation results in a lower valuation for the practice. Conversely, lower levels of post-transaction physician compensation create increased projected free cashflows. However, total compensation should be consistent with market levels. If the compensation structure is below market, there are sustainability risks associated with retaining and recruiting new physicians after the transaction. Setting physician compensation in line with the market for physicians with similar productivity can mitigate these risks.

The market approach compares an individual practice to similar physician practice transactions in the market through the application of an earnings multiple. Practice transactions often use the application of earnings before interest, taxes, depreciation, and amortization (EBITDA) multiples. It is important to note that EBITDA is calculated after taking into consideration the post-transaction structure for all providers. The multiple is determined based on a review of similar transactions in the marketplace, attributes specific to the practice, market factors, and on perceived risk of practice profitability amongst other factors. As illustrated below, physician compensation impacts the market approach similarly to the income approach—the greater the physician compensation, the lower the earnings for which to apply an earnings multiple.

If too much physician compensation is sold, the market multiple may need to decrease to account for physician sustainability risk. Low levels of physician compensation in relation to productivity can lead to physician attrition.

The cost approach is an asset-based approach that analyzes an entity’s tangible and identifiable intangible assets. A level of post-transaction physician compensation that is consistent with the historical amounts or higher may eliminate positive future cash flows, causing the practice to be valued based on its assets versus earnings. It is not uncommon for practices to be valued using the cost approach due to the lack of attributes enabling them to monetize compensation while being consistent with market levels of compensation post-transaction.

Physician practices have the unique freedom to determine the services they provide, who provides those services, and how physicians can be compensated. There are multiple factors that determine the profitability of a physician practice, which directly impacts physician compensation. The amount of compensation and the way it is structured can have material impacts on the value of a practice, regardless of valuation approach. It is imperative to understand the link between post-transaction physician compensation and the fair market value of a physician practice for both buyers and sellers.

Definitive Healthcare. (2024). Number of physician group practices by state. Healthcare Insights. https://www.definitivehc.com/resources/healthcare-insights/number-physician-group-practices-by-state#:~:text=According%20to%20our%20database%2C%20there,them%20access%20to%20more%20patients

Kelleher, S. (2023). Understanding Physician Compensation Models. Health eCareers. https://www.healthecareers.com/career-resources/residents-and-fellows/understanding-physician-compensation

PayrHealth. (2022). Ancillary Services in Healthcare: Finding the Right Level for Your Practice. Managed Care Contracting Blog. https://payrhealth.com/resources/blog/list-of-ancillary-services-in-healthcare/

Written by Colin Haslett and Grayson Terrell, CPA

Healthcare transactions are known for their complex nature, given their rigorous regulatory compliance requirements, diverse revenue streams, intricate insurance and reimbursement policies, and significant capital requirements. Like a medical examination, financial due diligence evaluates the vital signs of a healthcare business, providing a comprehensive assessment of its financial health. By identifying potential financial risks and validating the company’s underlying valuation, due diligence helps to diagnose the current state of the business and predict its future health. No matter the size of the healthcare transaction, financial due diligence is a necessary element in the process. It provides valuable insights into the buy-side and sell-side, ensuring all parties clearly understand the financial aspects of the deal.

One important aspect of financial due diligence in healthcare transactions is the quality of earnings process, which focuses on adjusting or normalizing EBITDA. This process involves adjusting or removing the impact of any non-recurring or one-time items from EBITDA, providing a more accurate picture of the company’s true cashflows. Throughout this process, key facts about the company that could impact the company’s EBITDA may arise, highlighting the importance of thorough financial due diligence relative to the healthcare transaction. During the quality of earnings process, it is important to carefully examine the impact of various factors on EBITDA. Some potential examples include:

In addition to examining the impact of adjustments to EBITDA, the letter of intent (LOI) will include language outlining that the proposed transaction will be completed on a cash-free, debt-free basis. As such, another focus of due diligence is identifying the debt and debt-like items within the company’s financials. These items may include deferred revenues and compensation, outstanding legal proceedings and exposures, and accrued interest. Sometimes, these items are not included in a company’s financial statements, especially if they are on a cash-basis or are off-balance sheet. Furthermore, the LOI will state a normalized level of net working capital (NWC), agreed upon by the buyer and seller, needed to run the business post-transaction. Diligence procedures will often include an NWC analysis that ensures the buyer or seller is not allowing the targeted NWC to be set too high or low, which can be costly if the target levels are not met.

In conclusion, financial due diligence is not just a check-the-box exercise, but a critical process that mitigates risk and safeguards the likelihood of success for the transaction. Therefore, it’s an investment worth making. Adjustments to EBITDA made during the diligence process can often pay for the cost of diligence itself when the multiple of the transaction is considered. Neglecting to perform financial due diligence can have serious repercussions. Without a thorough understanding of the involved entity’s financial health, companies may overlook hidden liabilities, overestimate current and future earnings of the company, or underestimate the costs associated with integration.

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

My portion of the presentation was about the valuation of academic healthcare brands. I talked through different valuation methodologies, which are the income cost and market approach, by discussing the specifics related to brand valuation. Additionally, I spoke about the key things to consider in a brand valuation or in a transaction involving a brand, like how to structure the payment—whether it’s through a variable or fixed license rate—and some of the pros and cons to different affiliation structures.

In academic brand valuations, the owners of the academic brands tend to think their brand is extremely valuable. However, from an actual fair market value transaction perspective, the value of that brand is based on the licensee’s return, even if the brand is powerful and may drive allocations higher. If the licensee can’t make a monetary return on it, there won’t be a huge value that they have to pay. Otherwise, they’d be negative.

Leaders can look for opportunities with this knowledge. Brands are not a common part of a joint venture arrangement. Adding a health system’s brand to a joint venture may result in an additional return or credit for something that the system is contributing to the joint venture. Historically, leaders may not have valued brands, but they can.

The blog, Healthcare Brand Valuation: Purpose, Strategy, and FMV Implications, is a great supplemental resource for those looking to learn more about incorporating brand in healthcare transactions. Additionally, another article is coming to the VMG Health website soon, and it will focus on brand valuation. Watch our site for that upcoming content.

Brands can and should be considered, and possibly included, in healthcare transactions.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.

Related Content