The Rise of Hospital and Health System Joint Ventures with Private Equity

Rachel Linch

October 19, 2023

Written by Tyler Perper and Matthew Marconcini, CPA

The following article was published by Becker’s Hospital Review.

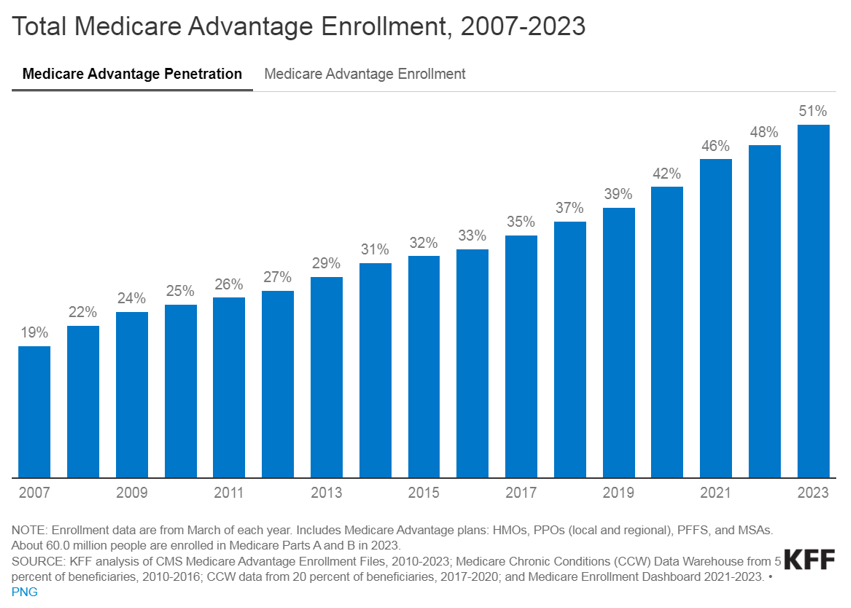

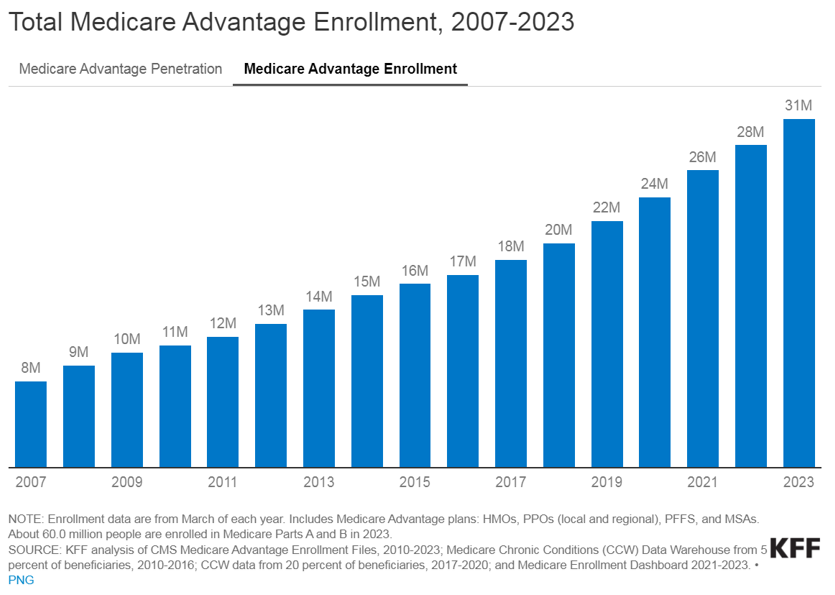

The landscape of healthcare is continually evolving, with a growing emphasis on providing better outcomes for patients while controlling costs. Value-based care (VBC) is a departure from the traditional fee-for-service (FFS) model and is transforming healthcare delivery into a capitated model that balances the total cost of care with the quality of patient outcomes. Investment within VBC or alternate payment models (APMs) quadrupled from 2019 to 2021, while investment in legacy-care delivery models has remained relatively flat. Additionally, the estimated number of Medicare enrollees participating in Medicare Advantage (MA) plans is expected to increase by more than 24% in 2023 compared to the 2022 MA enrollment growth. The explanation for the significant VBC investment and the growth in VBC players is primarily driven by the acknowledgment amongst U.S. policymakers, providers, and payers that VBC offers a sustainable model of care for patient populations across the country, as well as the opportunities presented by new technology and tech-enabled services that facilitate VBC for both providers and payers.

VBC is a payment model that incentivizes healthcare providers to focus on delivering high-quality care while containing the costs. Unlike the FFS payment model, in which providers are reimbursed based on the number of services they render, the APM model encourages providers to prioritize the patient’s health and well-being by promoting preventive measures, care coordination, and better health outcomes. In addition, as providers transition to value-based care their reimbursement model aligns more closely with that of payers. This shift requires providers to gain a fundamental understanding of the expertise needed for managing risk, similar to payers.

Managing risk and risk sharing in healthcare refers to the practice of distributing and managing the financial risks associated with healthcare services among different stakeholders, such as insurers, healthcare providers, and sometimes patients. It involves mechanisms and arrangements designed to ensure the financial burden and responsibility for healthcare costs are shared rather than being shouldered entirely by one party. The goal is to promote cost efficiency and improve healthcare quality.

Transitioning to VBC reimbursement models presents providers with a spectrum of options. At the outset, pay-for-performance models link claims reimbursement to quality and value. This means that providers are reimbursed using a fee-for-service structure while qualifying for value-based incentives or penalties based on quality and cost performance. Such models are particularly favorable for smaller practices lacking extensive health IT and data analytics infrastructure.

Moving further along the spectrum, shared savings arrangements offer higher financial rewards and allow providers to retain a portion of the savings if they reduce healthcare spending below established benchmarks. Shared risk models, where providers must cover healthcare costs exceeding benchmarks, foster greater accountability, especially within accountable care organizations.

Finally, capitation payments place full financial risk on providers and offer either global capitation with a fixed payment for all services or partial capitation covering specific services with all other care reimbursed through fee-for-service. While capitation models provide prepaid reimbursements and an incentive for innovation, they present challenges related to quality measures and data sharing. Overall, this spectrum allows providers to select the most suitable value-based reimbursement structure to enhance revenue and adapt to evolving healthcare reimbursement models.

Medicare, including both MA and traditional Medicare, serves as a hub for VBC innovation in the United States. Centers for Medicare & Medicaid Services (CMS) is the largest payer in the healthcare system and holds significant influence in shaping industry standards and promoting the adoption of APMs. The elderly population, which is covered by Medicare, tends to have higher rates of illness and multiple health conditions. This, coupled with the long-term coverage provided by Medicare, makes VBC interventions particularly impactful in reducing the cost of care for these patients.

Within traditional Medicare, the Medicare Shared Savings Program (MSSP) is a widely participated program. The program offers mild shared savings and shared-risk arrangements. The more intensive-risk ACO REACH program attracts more sophisticated VBC providers that are often engaged in MA-capitated contracts.

Currently, VBC is not as common within the Medicaid and commercial markets on a national basis for numerous reasons. For Medicaid, the lower rates of reimbursement (in comparison to Medicare and commercial payers) limit the VBC capitated care model. Also, the high fragmentation of Medicaid regulation from state to state limits the scalability of the APMs. There is a high level of enrollee turnover within Medicaid programs which makes it more difficult to understand individual patient populations over the course of time.

The lack of implementation within commercial markets is due to one main reason: the demographic profile of a typical commercial patient (skewed younger and of higher socioeconomic status) leads to lower health risks. This means that investing a dollar in primary care for a commercially insured individual results in lower, less substantial total cost of care savings compared to Medicare or Medicaid patients. However, the traction of Medicaid and commercial patients in risk-sharing arrangements depends on the market across the U.S. In certain markets, such as California, risk-based arrangements are more common due to the early adoption of health maintenance organizations and the way those programs have shifted into risk-bearing organizations. As data analytics improves and payor-provider convergence continues, the development of Medicaid and commercial VBC structures is increasing.

In the traditional FFS models, the primary relationship was between payors and providers. The shift towards value-based care has led to the evolution of the players involved. These relatively novel VBC participants can be categorized into three main groups, each with its own subcategories.

Many of the prominent VBC players fall within the provider management category. This category aims to back or acquire medical practices operating within VBC frameworks. There are several models that facilitate VBC provider management. There are those operators who seek to establish new clinics and healthcare practitioner recruitment by prioritizing consistent branding and patient experience while tackling capital-intensive challenges.

Other operators contract directly with self-insured employers by offering comprehensive primary care services that often include behavioral health and pharmacy, and by promoting clinic growth through employer contracts. Another provider management model of VBC is the acquisition of provider groups. This model transitions them into physician-owned primary care practices and shifts the revenue toward taking on riskier VBC contracts. Lastly, there are operators that focus on taking specialty practices, such as orthopedics, oncology, or nephrology, and transitioning them into VBC contracting. This is done by leveraging specialty-based operational sophistication and specific specialty VBC payment models.

The second category of VBC players comprises organizations that opt for collaboration with independent providers or medical groups rather than acquiring practices outright. These entities, often referred to as “VBC enablers,” play a pivotal role in facilitating the transition to value-based care. They offer a comprehensive suite of services, including advanced technological solutions, expert consulting, and various forms of support. Through their involvement, these enablers actively engage in the shared risk associated with value-based contracts, demonstrating their commitment to advancing healthcare transformation and fostering a culture of collaboration and innovation. By forging these strategic partnerships, VBC enablers empower independent providers and medical groups to navigate the complex landscape of value-based care successfully, ultimately improving the quality and efficiency of healthcare delivery for all stakeholders involved.

The third category encompasses the technological solutions and ancillary services that play a pivotal role in facilitating the shift from FFS to VBC. There are many different players within this category and the technology-based solutions these companies provide include patient population/risk management, care coordination, surgery coordination, outcomes measurement, and care management. Patient population management is software that helps providers track patient health outcomes, utilization patterns, and risks. It aids in identifying high-risk patients and implementing interventions to reduce costs. Care coordination is the technology behind building quality referral networks, ensuring closed-loop referrals, and sharing patient information among care providers. Surgery coordination is software used to orchestrate surgeries efficiently and manage costs, especially in a VBC context. Outcomes measurement highlights the importance of understanding the quality metrics of the care provided and managing costs of care. Furthermore, care coordination is what guides patients through the healthcare system to improve outcomes and minimize costs. This includes services for chronic condition management and care navigation. These players can provide one or multiple of the services previously described and often contract with other entities in the VBC environment.

The transformation towards VBC healthcare delivery models holds the promise of significant benefits that extend to both cost reduction and the enhancement of satisfaction among providers and patients alike. By concentrating on preventive measures and evidence-based treatments, VBC stands to ameliorate health outcomes and particularly benefit patients with chronic conditions. Furthermore, it promotes the efficient allocation of resources, thereby generating cost savings for both patients and healthcare systems, in particular. One pressing issue is the high rate of hospital readmissions, and it requires attention because it is. Currently hovering at approximately 15% within Medicare. Through an increased emphasis on care coordination and follow-up care, VBC aims to mitigate the frequency of avoidable hospital readmissions. Additionally, it underscores the importance of the patient’s experience and positions the patient at the core of the healthcare process. This ultimately results in heightened patient satisfaction and engagement. Lastly, it addresses physician satisfaction by reducing resource utilization while potentially maintaining reasonable compensation levels. Ultimately, VBC stakeholders expect to create a healthcare system that is more sustainable and centered around the needs of patients, while unlocking profitability and returns for investors.

Although promising, VBC presents its own set of challenges for providers and payers alike. Effective VBC relies on robust data collection and analysis capabilities which necessitates technological infrastructure upgrades for many healthcare organizations. Additionally, determining meaningful quality metrics for specialty care can be intricate due to the specificity of outcome measures required for different conditions. Providers may encounter financial risks if they fail to meet VBC targets, particularly in shared savings or full risk-sharing arrangements. Ensuring alignment of incentives among various stakeholders, including physicians, hospitals, and payers, is pivotal to the initiative’s success. These challenges must be navigated to fully realize the potential benefits of VBC.

Despite the significant hurdles in the way, the healthcare market’s accelerating shift to VBC signifies a profound change towards patient-centered and outcome-driven healthcare delivery. As the healthcare landscape continues to evolve, embracing VBC offers the prospect of enhancing patient outcomes, improving the patient experience, and promoting cost-effective care. However, to unlock the complete potential of this shift in payment models, it may be necessary to seek guidance from healthcare advisors who possess specialized expertise in this field. These advisors play a vital role in helping address patient population challenges, defining pertinent quality metrics, and aligning incentives effectively. In addition, transactions for entities in the VBC space, or healthcare operators looking to enter the VBC space have a need for a specialized understanding of these relatively novel APM models in terms of valuation, reimbursement dynamics, and related transaction agreements.

Authors

Related Content