Mistakes are magnified in frothy capital markets when transaction prices and deal multiples are high. The healthcare sector continues to garner the attention of investors as private equity investment and consolidation drive multiples higher across the healthcare spectrum. Elevated multiples paid on healthcare businesses call for expert financial due diligence and quality of earnings analyses to navigate the nuances of each subindustry and provide investor protection. At VMG Health, we work with clients across the healthcare investment spectrum – from private equity to strategic buyers – on deals ranging from large, platform businesses to small, tuck-in acquisitions. We’ve observed many reporting mistakes and neglected risks over our 25 years of healthcare transaction experience. Based on these experiences, here are our top five lessons to consider during your next deal:

Lesson 1: It’s (mostly) all about revenue

Allocate adequate time to thoroughly assess revenue.

In financial due diligence (“FDD”) and healthcare quality of earnings (“QoE”) engagements, we’ve found that a considerable amount of time must be spent understanding the revenue composition (i.e., payor mix, procedure mix, reimbursement contracts, etc.) and revenue recognition policies of a target business. We’ve also found that the rapid changes occurring in healthcare can have a material impact on revenue estimates. Changes to be considered include:

- Increasing popularity of high-deductible health plans and the resulting shift toward increased patient responsibility, which may impact bad debt implicit in net revenue estimates;

- Industry-specific reimbursement across healthcare verticals frequently change; and,

- Business-specific revenue mix changes due to shifts in procedure mix, payor mix, or reimbursement based on payors contracts.

It’s critical to understand management’s assessment of these potential issues and how they have been incorporated into their accrual revenue estimates.

Lesson 2: Accrual revenue estimates require frequent back testing of collectability assumptions

Run your own revenue analysis and compare it to management’s estimate.

Building off lesson 1, revenue mixes and reimbursement rates can change rapidly for healthcare businesses. Each year the Medicare Payment Advisory Commission (“MedPAC”) provides analysis and policy advice, related in part to Medicare reimbursement rates, to the Centers for Medicare and Medicaid Services (“CMS”). Revenue collectability assumptions that were relevant in prior periods may no longer be relevant if there have been CMS reimbursement changes. Revisions to Medicare reimbursement can also impact commercial payor and Medicaid reimbursement if the business’s contracted commercial rates are negotiated as a percentage of Medicare rates. Be sure to research current and announced CMS reimbursement changes to understand the potential impact. Ultimately, management’s methods for estimating revenue may be outdated and imprecise if adequate consideration isn’t given for these types of shifts.

Comparing cash collected by date of service to reported net revenue (“back testing”) may uncover material variances. Run your own revenue analysis, such as a cash waterfall analysis or zero balance account analysis, to test and compare the results to management’s estimate. By doing so, you may uncover revenue misses or aging accounts receivable balances.

Lesson 3 – Cash to accrual conversion creates a more informed buyer

Converting cash to accrual produces a clearer picture of current operations.

Many healthcare businesses record transactions on a cash basis. Whether a business’s financial statements are presented on a cash or accrual basis can yield meaningful differences – cash often lags accrual and can delay the recognition of earnings growth trends or accruals being captured on the balance sheet. Consequently, cash basis financials often don’t depict an accurate picture of current business operations.

To illustrate, assume a business has significant drugs and medical supplies costs, such as retina drugs for an ophthalmology practice. These supplies should be expensed when used in a procedure. Instead, drugs and medical supplies are often expensed when purchased in bulk for volume discounts or more generous payment terms from the vendor (i.e., 30, 60, 90 days, or held on consignment) that don’t necessarily align with the actual usage of these drugs and supplies. This mismatch may present a significantly different picture of the business’s earnings and could create off-balance sheet liabilities.

Lesson 4 – Don’t blindly rely on audited financial statements

Reviewing audited financials are a good first step, but they’re ultimately management’s representation.

It can be helpful to the diligence process when a target business has audited financial statements for many reasons. First, footnotes included in audited financial statements often provide background on the business, an overview of the business’s accounting policies, and additional detail beyond the face of the financial statements. Second, it’s encouraging to know that an independent third party works with business management on financial reporting. Finally, discussions with auditors may be able to provide qualitative insight into the business’s operations beyond what the numbers may tell you.

Keep in mind, however, that audited financial statements are ultimately management’s representation of the business and are not the auditor’s responsibility. Also, audited financial statements present historical periods and may not reflect current trends as discussed in lessons 1 and 2. Recognizing differences between historical and current operations can uncover meaningful findings, particularly on the revenue side of the business where we’ve seen material misses between reported revenue and cash ultimately collected. Because of these factors, be sure to back test audited financial statements against your own revenue and expense analyses.

Lesson 5 – Not all healthcare verticals are the same

Understand value drivers and inherent risks associated with your target’s subindustry.

Each healthcare vertical has specific nuances to be analyzed, including different value drivers, opportunities, and risks. The influx of private equity capital in the healthcare market across nearly all subindustries means there’s an increased need for healthcare-specific expertise. Health systems that decide to expand into new verticals may also need to look externally for expertise in a specific subindustry.

By properly identifying the risks in your target’s subindustry, you can be more efficient in your diligence by allocating time to the most sensitive areas. This leaves you more time to discuss the key findings so that you’re better prepared to negotiate and close the deal.

Healthcare Quality of Earnings: The Big Picture & Application

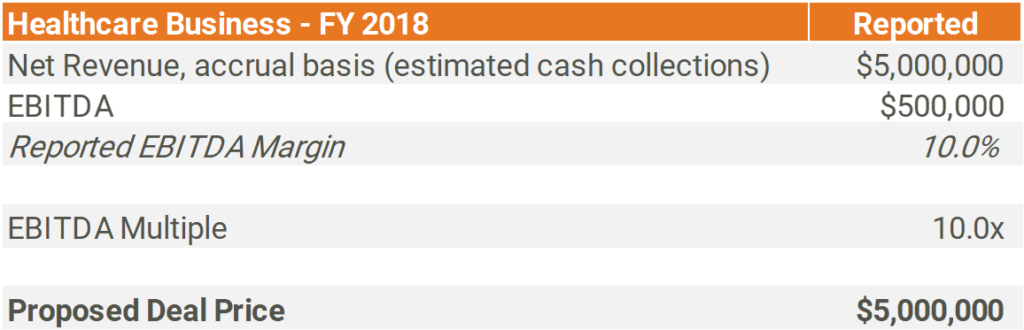

Elevated deal multiples amplify errors and can be incredibly costly to a healthcare investor. To illustrate a simple example of the costliness of errors, consider a hypothetical deal with the following facts:

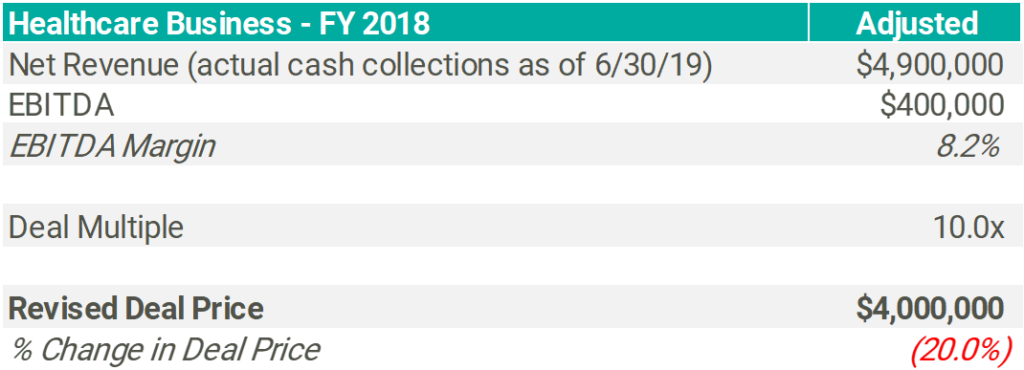

Back testing actual cash collected (by date of service) to reported accrual basis net revenue for a mature historical period creates an apples-to-apples comparison that can identify material variances.

For this example, assume the following:

- FY 2018 charges are considered closed (i.e. no further collections are expected related to services performed during FY 2018)

- Accrual revenue reported on the FY 2018 audited income statement is $100,000 more than actual cash collected for services performed in FY 2018

- The subject business’s expense profile is 100% fixed (i.e. not dependent on revenue)

The ($100,000) or (2.0%) revenue variance above then results in a 20.0% decline in EBITDA, adjusting the deal price by ($1.0 million) due to the elevated multiple used in this transaction.

Of course, this is a simplified example as there are many factors that warrant consideration and testing for each healthcare vertical. VMG Health’s highly qualified CPA’s can quickly navigate financial statements to identify and focus on the material risk factors by leveraging the knowledge gained over 25 years of healthcare transaction experience. This experience combined with the lessons listed above allows for a refined healthcare quality of earnings and financial due diligence process that helps protect our clients.