Behavioral Health Service Market Overview

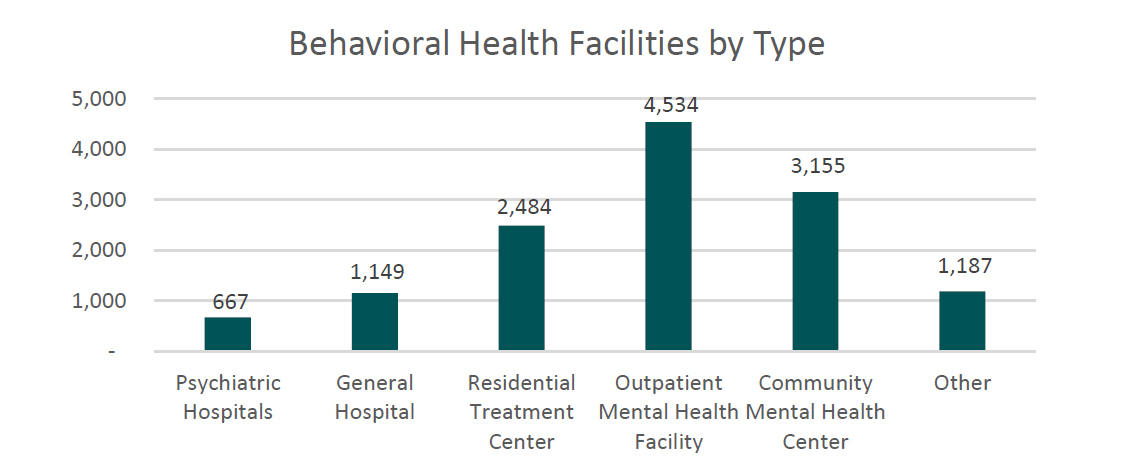

The behavioral health industry has historically been a fragmented market comprised mainly of independent freestanding operators, state institutions and acute care hospital departments. Current estimates by the Federal Substance Abuse and Mental Health Services Administration indicate that approximately 64.2% of behavioral health facilities are privately owned and operated as non‐profits, 18.4% are governmental facilities, and the remaining 17.4% are for‐profit entities (1). In total, the mental health and substance abuse industry in the United States has a combined annual revenue of approximately $50 billion with 13,000 facilities detailed by type below (2):

Recently the industry has undergone a wave of consolidation with the emergence of multi-location chains and growth of for-profit operators. Some of the largest operators of behavioral health facilities in the nation are listed below3:

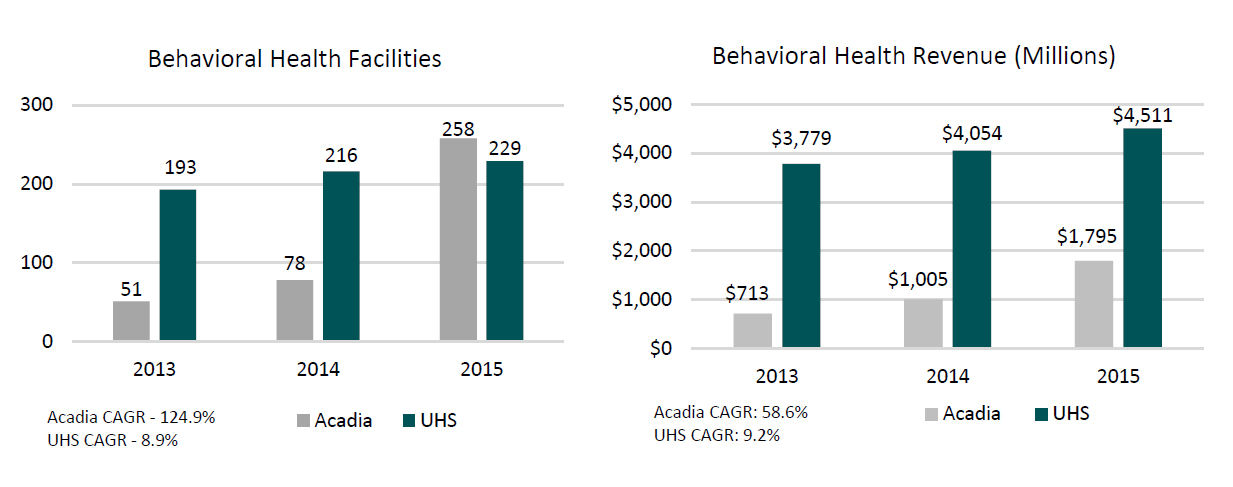

The consolidation in the industry can also be demonstrated through the recent growth in the two largest for-profit operators of behavioral health facilities, Universal Health Services, Inc. (“UHS”) and Acadia Healthcare Company, Inc. (“Acadia”). The facility count and revenue for these two companies has expanded dramatically over the last three years (4):

A major reason behind the growth in for-profit operators has been regulatory changes. This includes the 2016 revision of the Medicaid Institutions for Mental Diseases (“IMD”) Exclusion, the Mental Health Parity and Addiction Equity Act of 2008, and the Affordable Care Act of 2010. These legislative changes have expanded insurance coverage for mental health services, lifted restrictions on freestanding facilities, expanded the demand for behavioral healthcare in general and increased reimbursement. This along with a limited supply in the number of psychiatric beds nationwide has driven higher levels of private investment in the industry spurring consolidation trends.

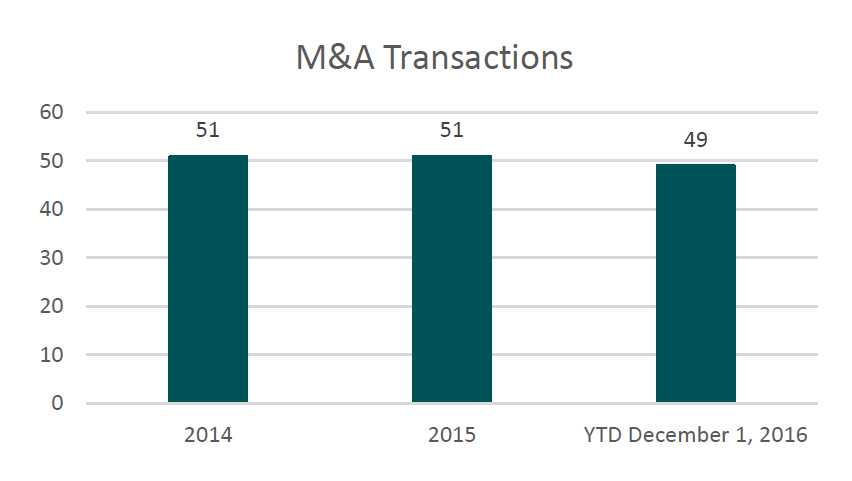

The industry consolidation has mainly been achieved through the acquisition of existing independent facilities. As illustrated below, recent merger & acquisition activity in the behavioral space has been significant (5):

Although not as common as outright acquisitions, joint venture transactions between non-profit health systems and for-profit operators have started to become more prevalent. Recent examples include Acadia’s 2016 announcements of separate partnerships with Ochsner Health and Greenville Health System to build inpatient psychiatric hospitals. In addition, UHS also announced joint ventures with Lancaster General Health and Providence Health Care to build inpatient psychiatric hospitals.

Steven Filton, Senior VP and CFO of UHS, highlighted the joint venture trend on the latest UHS earnings call (6):

“We have talked a great deal of the last few quarters about the fact that we are having much more frequent conversations with acute care hospitals about, in some way, penetrating and sharing in the economics of their behavioral health facilities”

“We continue to view the opportunity to penetrate or integrate the behavioral units within these acute care hospitals as a tremendous development opportunity for us, not just in the next year or two but, frankly, for the intermediate and long term.”

“We probably have about a dozen other conversations that I would describe as likely resulting in some sort of arrangement but still a little too early to discuss them with any level of specificity.”

Joey Jacobs, CEO of Acadia, echoed these sentiments on the latest Acadia earnings call (7):

“We also remain actively engaged with our acquisition pipeline and we continue to believe that our 2017 acquisition and joint venture activity will be heavily weighted to acute facilities in the U.S.”

“We also look very good – I think in my last count, we have about 16 discussions with joint ventures, with large not-for-profit systems and a joint venture hospital will cost about $25 million to $30 million in construction cost”

These joint venture models are similar in structure to transactions widely employed by different verticals within the healthcare industry. Examples of this include the arrangements United Surgical Partners International (“USPI”) has with non-profit health systems in the ambulatory surgery center space. In addition, HealthSouth, Inc. has utilized similar models in the inpatient rehabilitation market. Generally speaking, transactions consist of a non-profit health system contributing its service line and use of its brand while the for-profit operator contributes capital and provides management services post transaction.

Based on the comments from the large public operators’ executives and recent transaction activity, it seems likely that joint venture activity will be common for the foreseeable future. Health system executives should be aware of this trend and understand how a potential joint venture could possibly effect their organization.

Motivations Behind The Joint Venture Model

Why would a non-profit hospital want to joint venture their behavioral health service line with a for-profit operator? Based on our experience and discussions with industry professionals, motivations for these transactions from a health system perspective may include the following:

- The hospital emergency room provides care to a large number of patients with mental health issues. These patients are then subsequently admitted as inpatients for stabilization which limits bed capacity that could otherwise be utilized for more profitable service lines. A joint venture allows a hospital to admit these patients to a facility off campus, continue to realize a portion of the financial benefit from treating said patients, and free up inpatient capacity.

- The hospital has capital constraints and the physical plant for the inpatient psychiatric unit is aging and needs to be replaced/upgraded. The joint venture model enables the infusion of new capital from the for-profit operator which in many cases is utilized to construct a new facility. In addition, for-profit operators oftentimes have superior access to capital and credit ratings when compared to smaller community hospitals and are able to tap debt markets easier with more favorable interest rates.

- The hospital has high leverage and wishes to pay down debt by monetizing a portion of the behavioral health business segment as part of a transaction.

- The hospital’s behavioral health unit is poorly managed and/or unprofitable. For-profit operators have considerable expertise with behavioral health businesses and many times can increase profitability post transaction through the management of expenses. Although the hospital is giving up a portion of the ownership in the service line, it is possible that with management from the for-profit operator post transaction, distributions to the hospital from the joint venture will be equal to or even exceed profit levels of the department historically.

- There is a shortage of psychiatry providers in the marketplace and the hospital has difficulties in recruiting physicians for the service line. Large for-profit operators have physician recruiting departments and a large existing network of psychiatric providers. The national operators can leverage these relationships to help attract new providers to the joint venture post transaction.

From a for-profit operator perspective, some of the major motivations behind the joint venture model are as follows:

- Ability to access new markets without the potential of competition from major established providers like the local hospital.

- Opportunity to leverage the hospital reputation and trade name to improve facility visibility in the marketplace and attract potential volume.

- Hospital emergency rooms act as large referral sources to behavioral health facilities. Many times these referrals are currently being directed to outside parties and not to the hospital’s behavioral health unit due to capacity constraints or other reasons. Affiliation with a health system with busy emergency rooms will help drive patient volume to the joint venture post transaction.

- Access to health system contracts and leverage with commercial payors that could result in higher revenue for services rendered.

- Ability to improve the expense profile of facilities post transaction through superior supplier/pharmaceutical contracts, staffing models, etc.

Establishing the Fair Market Value of a Contributed Service Line

The respective equity ownership for parties in a joint venture is established by their relative contributions to the new entity. As previously discussed, the contribution from a hospital perspective in these transactions usually consists of the behavioral health service line along with use of the hospital trade name. The for-profit operator will then usually contribute enough capital to reach the mutually agreed upon ownership percentages. From a financial point of view, establishing an accurate valuation of the hospital’s contributed service line is a critical component of the joint venture process. Notwithstanding financial considerations, the valuation of the service line has regulatory and compliance implications as well. Generally speaking, the hospital will be a large referral source to the new joint venture and as a result, any transaction must be compliant with regulations such as the Stark Law, the Anti-Kickback Statue and possibly private inurement considerations when the hospital is a non-profit entity. In order to ensure compliance with these regulations, the valuation of the hospital’s behavioral health service line should be consistent with Fair Market Value (“FMV”). FMV is defined as follows (8):

“The price, expressed in terms of cash equivalents, at which a property would change hands between a hypothetical willing and able buyer and a hypothetical willing and able seller, acting at arm’s-length in an open and unrestricted market, when neither is under compulsion to buy nor to sell, and when both have reasonable knowledge of the relevant facts.”

Having an independent third party appraisal performed by an experienced firm can mitigate the risks in ensuring that the value of the contributed service line is consistent with FMV and does not include any consideration for the volume or value of referrals. As part of this process, it is critical that the appraiser has extensive expertise in the healthcare industry and understands the unique regulations, facts and circumstances surrounding behavioral health businesses.

An FMV analysis should consider the Income, Market, and Cost Approaches to value. Briefly, the Cost Approach identifies the cost to recreate a business or asset, the Market Approach computes value by examining the purchase price of similar companies or assets in a free and open market, and the Income Approach projects a future income stream attributable to a business or asset and then discounts those earnings back to present value. In most cases, the Cost Approach is utilized to establish a floor value of an enterprise and is not relied upon when the Income and Market Approaches generate values greater than the cost to recreate the identified assets. As a result, this article focuses on the Income and Market Approaches to value.

Income Approach

The Income Approach estimates value by projecting future cash flows attributable to the subject entity’s operations and then discounts those earnings back to the present value utilizing an appropriate discount rate that takes into consideration the risk of the forecast. As previously discussed, the FMV standard assumes a hypothetical buyer/seller and as a result, the expenses/revenues included in an analysis should reflect what a typical buyer/seller can reasonably expect to incur. In other words, an FMV appraisal must simulate operations of the service line on a freestanding basis.

When operating as a department of a hospital, service lines many times do not directly record certain expenses incurred by the parent on their departmental financial reports. Examples of these expenses often include facility related costs, billing & collection, management functions, insurance, etc. In other instances, expenses such as supplies, pharmaceuticals, security, maintenance, etc. are allocated to the department financials based on methodologies such as relative charges, collections, patient days or some other metric. Due to certain expenses either not being recorded at all or allocated in an imprecise fashion, the expense profile on departmental financials is oftentimes not an accurate representation of costs to operate the service line on a freestanding basis. A hypothetical buyer such as a for-profit operator, individual or private equity firm would have to incur these expenses post transaction. As a result, an FMV analysis should carefully consider the reasonableness of the expenses included on the departmental reports, benchmark them against industry peers, include other expenses not recorded and ensure all estimates are justified to operate as a standalone facility. An improperly burdened expense profile may in turn result in an inaccurate FMV indication under the Income Approach. Respected healthcare valuation firms usually have extensive experience with similar businesses, access to proprietary databases and other market information that are critical to simulating the line of business as a freestanding enterprise.

When a new facility is being constructed as part of the joint venture, an FMV rental rate for this property should be included in any cash flow projections. In this scenario, the hospital is not contributing the current real estate to the joint venture, so operations must be burdened with FMV rent to reflect an accurate representation of the contributed assets. Ultimately, a real estate appraisal will help ensure that the rental rate is FMV and not a preferred rate which could be construed by regulators as consideration for patient referrals.

In addition, reimbursement for the service line when structured as a department of the hospital might not be achievable on a freestanding basis. Reasons for a revenue differential could include the inability of a joint venture to assume hospital commercial contracts post transaction, additional reimbursement for the hospital having an emergency department and add-ons for trauma or other forms of acute care provided. An FMV analysis should adjust the revenue stream to reflect freestanding market reimbursement to ensure consistency with FMV.

Once freestanding operations are accurately simulated, an Income Approach analysis would project patient volumes, length of stay, reimbursement by payor, operating expenses, incremental working capital and capital expenditures to calculate net discretionary cash flow into perpetuity. A valuation should pay particular attention to capacity constraints (private vs. semi-private beds), regulatory changes, relative staffing levels, competitive position in the local market and other factors when projecting future financial performance. These cash flows would then be discounted back to present value utilizing the weighted average cost of capital to establish a value indication under the Income Approach methodology. The weighted average cost of capital should account for the specific risks related to the entity under question as well as for the aggressiveness/conservatism of the financial forecast.

Market Approach

The Market Approach methodology relies on the economic principle of substitution when establishing a value indication for a subject enterprise. The logic behind this approach is that similar assets should sell for similar prices in a free and open market. Under this approach, the value of comparable business and consideration included similar transactions is calculated as a multiple of some financial/operational metric. Based on our experience and discussions with industry professionals, the most common multiples quoted in the behavioral health industry are in terms of revenue, earnings before interest taxes and depreciation (“EBITDA”) or licensed beds. These multiples are then applied to the subject entity’s metrics to establish a value indication under the Market Approach.

Generally speaking, the hospital is contributing its entire behavioral health service line to the joint venture, and therefore, the valuation should be performed at a controlling or enterprise level of value. As a result, market multiples utilized in a Market Approach analysis should be on a controlling level of value (as opposed to a minority/non-controlling level) to be comparable.

Access to accurate, comparable transaction data is critical to any Market Approach analysis. Well established valuation firms with experience in the healthcare industry usually have proprietary transaction databases with relevant information, exposure to relevant market participants and experience dealing with similar transactions. Multiples obtained from available market data should be adjusted for factors such as size, geography, diversification, access to capital, growth prospects, profitability and liquidity among other factors. In addition, transactions for multiple facilities typically result in significantly higher multiples paid than for a single location. Finally, an FMV analysis should avoid related party transactions and transactions where the seller is financially distressed as the indicated multiples would not be consistent with the definition of FMV.

As for current pricing trends in the behavioral health marketplace, Joey Jacobs CEO of Acadia, gave some general insight on a recent Acadia conference call (9):

“John, I would think the larger transactions are going to get around that nine times. A single transaction is probably going to get closer to the seven times. I think the bankers are beginning to realize that the multiples have come down and are coming down. And if they want to engage Acadia in the process that we’ve set those expectations that we’re going to verify the trailing EBITDA earnings and that’s the multiple we put to it. And if we lose the transaction, we lose the transaction, that’s okay with us. We’re going to do a good transaction, so that’s where the market’s at right now.”

Conclusion

After considering all three approaches to value, an FMV analysis should then reconcile the indications to develop a range. If certain assets necessary to operate the business are not contributed to the joint venture, an adjustment to the value indication should be made. Examples being when the equipment and current staff will remain with the hospital post transaction or the joint venture will not be able to utilize the health system tradename or branding. As a result, estimates for the value of the equipment, trained workforce, and hospital tradename should be deducted from the value indication of the enterprise.

In summary, the valuation of a behavioral health service line is a complicated process that requires expertise in valuation techniques as well as a deep understanding of the healthcare industry. Steven Filton, Senior VP and CFO of UHS, stated the following on how UHS approaches the valuation process of service lines for joint ventures (10):

“In terms of commenting on valuations of the two businesses, I think it’s difficult for us to do. We clearly look at individual acquisition opportunities on a standalone, discrete basis and the growth potential in an individual behavioral facility or individual behavioral company versus an acute is really dependent on the markets they’re in, what their specific market position is, what the strategies are for growth, et cetera. So we certainly don’t go into any acquisition, either acute or behavioral, with a notion of kind of there’s a fixed sort of a valuation that make sense.”

As indicated by Mr. Filton, each valuation has its own set of unique facts and circumstances that must be considered. Using a blanket type approach does not usually result in a conclusion that accurately reflects the current state of operations. With increased regulatory scrutiny, it is critical that the value of the contributed service line be consistent with FMV. Hiring an independent third party valuation firm can ensure the proposed transaction meets the FMV standard.

Footnotes

- National Mental Health Services Survey (N-MHSS): 2014.

- National Mental Health Services Survey (N-MHSS): 2014.

- Internal VMG research of related company websites and/or annual reports

- Acadia Healthcare Co., Inc. Annual Reports 2013, 2014, 2015; Universal Healthcare Services, Inc. Annual Reports 2013, 2014, 2015.

- Capital IQ & company press releases.

- Seeking Alpha – UHS 4th Q 2016 Earnings Call Transcript

- Seeking Alpha – ACHC 4th Q 2016 Earnings Call Transcript

- NACVA Professional Standards, http://web.nacva.com/TL-Website/PDF/ NACVA_Professional_Standards.pdf.

- Seeking Alpha – ACHC 3rd Q 2016 Earnings Call Transcript

- Seeking Alpha – UHS 3rd Q 2016 Earnings Call Transcript