Physician Practice Strategy: The Private Equity Play

Rachel Linch

October 20, 2022

Written by Holden Godat, Taylor Anderson, CVA, and Trent Fritzsche

With the emergence of private equity (PE) firms attempting to align with physician practices, VMG Health has seen an increase in the number of management services agreements (MSAs). Due to the highly fragmented and regulated nature of healthcare, PE investment in healthcare is not as straightforward as in other industries. In states with some level of corporate practice of medicine (CPOM) adoption, PE’s interaction with physician practices usually involves a “Friendly PC” model with an affiliated management services organization (MSO) [1]. In return for providing most of the non-clinical assets and services to a physician practice, the MSO charges a management fee via an MSA. To better understand how these arrangements are structured in the market, VMG Health experts have outlined their findings from valuing over 120 MSAs and offer insight into how to generate more value from these agreements.

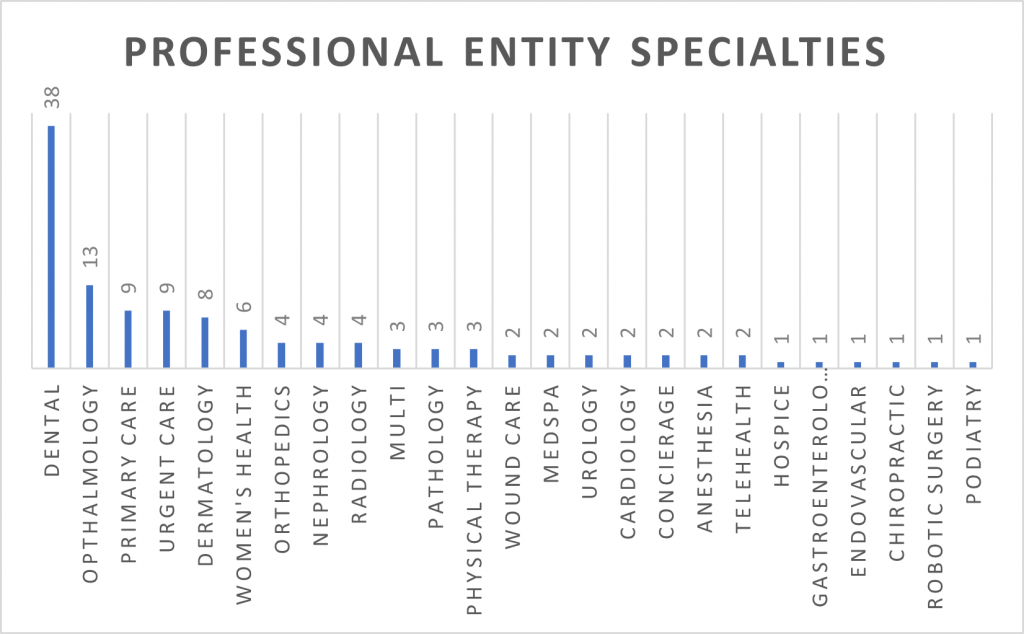

As private equity investment has increased over the years, climbing from $19.5 billion in 2015 to $74.4 billion in 2022, the variety of specialties targeted has also increased [2]. In 2015, VMG Health experts observed that the main specialties undergoing consolidation were anesthesia, dermatology, and gastroenterology. While those specialties are still prevalent today, there has been an emergence of transactions and consolidation in dental, ophthalmology, urgent care, primary care, and women’s health.

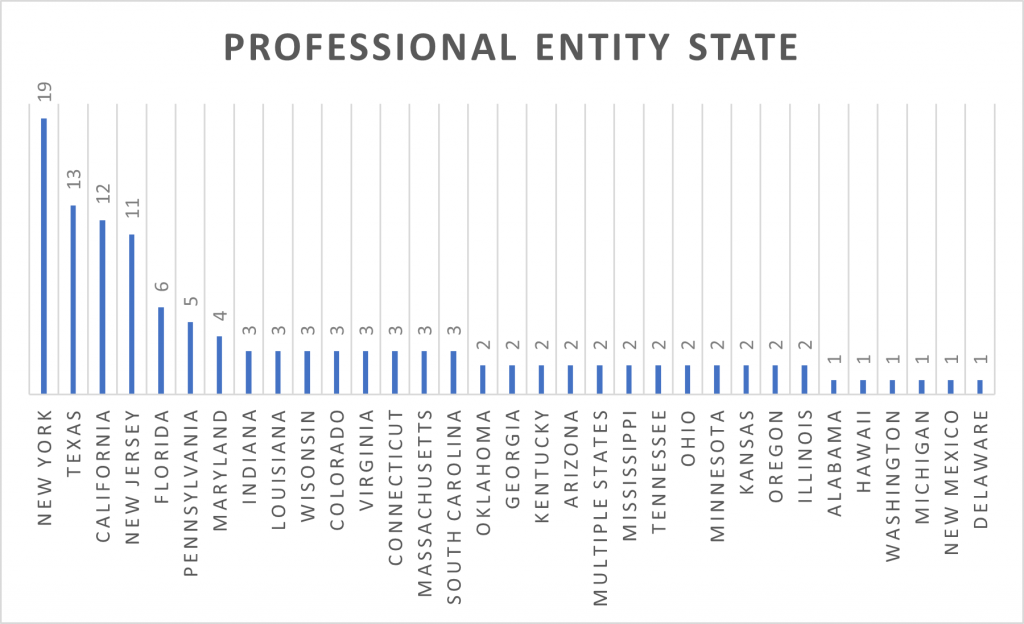

From large and diverse geographies to strict adoptions of CPOM, a doctrine developed to protect the quality of patient care by “prohibiting corporations from practicing medicine or employing a physician to provide professional medical services,” it is no surprise New York, Texas, California, and New Jersey have the most observed MSA valuations [3]. VMG Health experts note that while these states have dominated MSA valuations for the past few years, the arrival of other states to this chart demonstrates that consolidation and resulting PE investments are occurring nationwide.

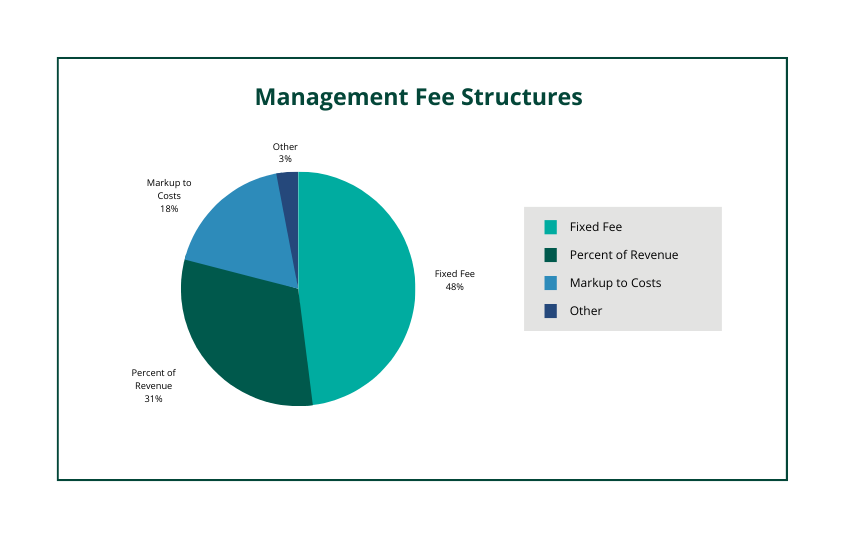

VMG Health observes the most common fee structures present in MSAs are fixed fees, percentage of revenue, and markup to costs. However, VMG Health has also seen management services organizations trying to get more creative in designing fee structures. This can take shape by implementing a combination of the three, creating variable tiers tied to performance, or creating a structure based on the number of providers. With CPOM, it is important to be aware of state-specific requirements when entering an MSA. As an example, many attorneys believe that New York’s CPOM adoption requires a fixed fee only in its fee structure, while Texas and California might allow for variable fee structures (i.e., percentage of revenue, a markup to costs, etc.).

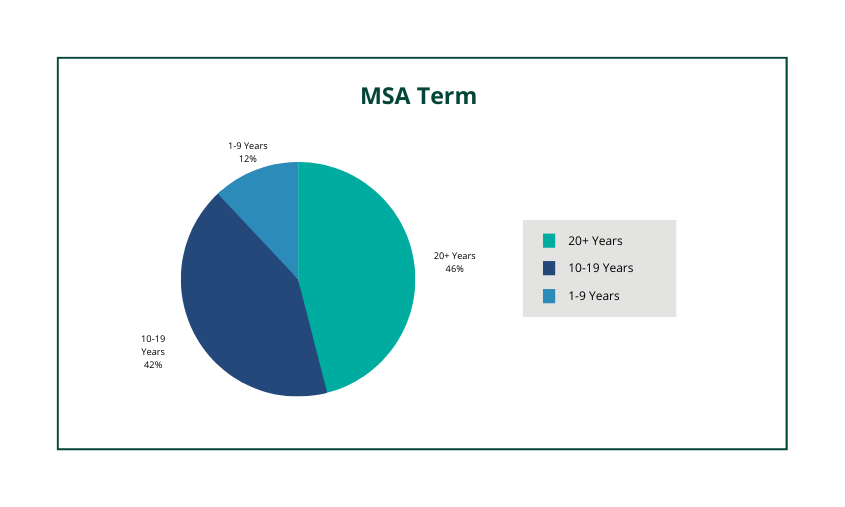

With platform practice multiples exceeding 10x, it is not uncommon to see MSA terms lasting more than 10 years. In fact, over 75% of observed MSAs had a term of 10+ years. While the total term can last for decades it is very common to see renewal periods that are in a two-to-five-year period.

Within any MSA valuation, there are common terms that VMG Health looks for in assessing value. These terms assist in demonstrating where the ultimate business risk lies, which in turn leads to extracting the most value from the professional entity (i.e., the greater the risk, the greater the return, etc.). The following outlines some of the pertinent terms VMG Health experts look for in an MSA:

When structuring an MSA it is important to consider all these factors to maximize value and to ensure compliance. In CPOM states, the management fees stated within MSAs must be set at fair market value. Upon drafting an agreement, a fair market value opinion from a third-party valuation expert can alleviate compliance concerns.

Authors