Written by Sydney Richards, CVA, Clinton Flume, CVA, and Patrick Speights

Orthopedics-focused ambulatory surgery centers (ASCs) are one of the fastest-growing segments of ASCs [1]. Orthopedics simplistically is the diagnosis, treatment, prevention, and rehabilitation of musculoskeletal system injuries and diseases. This specialty is evolving quickly to leverage demographic, payor, and technological marketplace shifts. Though the industry is still highly fragmented across the United States, VMG Health continues to see a demand for affiliations with strong orthopedic groups emerging from diverse contexts such as health systems, nationwide ASC operators, and private equity groups. Many orthopedics groups are considering whether now is the right time to pursue an affiliation or acquisition and how much their business could be worth to a potential buyer. Below, VMG Health experts highlight a few of the key trends impacting orthopedics providers in the U.S. We also identify what makes an orthopedics group attractive (Hint: It’s not just about the bottom line).

Compared to other specialties, orthopedics was hit disproportionately hard by the deferment of elective procedures during the COVID-19 pandemic and subsequent labor shortages. Through the second quarter of 2023, many markets have stabilized and recovered to pre-pandemic volumes. Over the next decade, orthopedics providers will continue to face unprecedented demand growth fueled by the aging population. Geriatric patients are naturally more susceptible to injury and disproportionally experience degenerative joint conditions compared to younger populations. As the population age shifts and there are continual technological innovations, people will live and work longer, which will create increased demand.

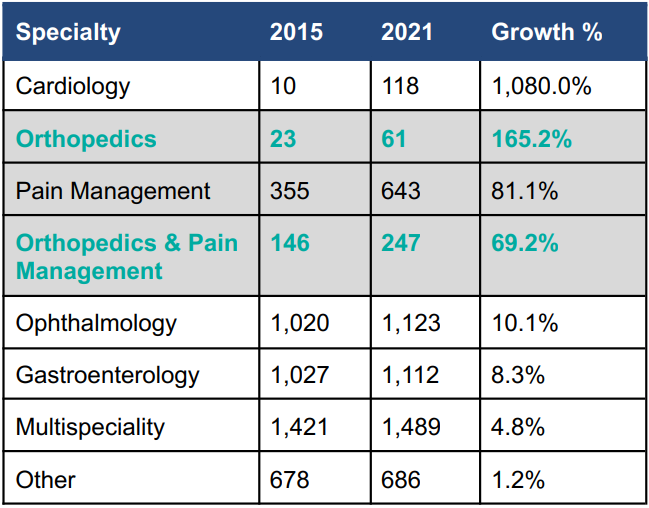

The population-driven demand for orthopedics services is further exacerbated by innovations and regulatory changes in the industry, such as the migration of inpatient-only procedures to ASC settings. It is estimated that moving total joint replacement cases from hospitals to ASCs lowers the cost of care by approximately 40% while maintaining the same outcomes [2]. As a result of this significant savings opportunity, around the beginning of 2019 [3] many commercial payors began requiring cases to be performed in ASCs rather than hospital surgery departments unless the latter were medically necessary due to complications or comorbidities. Medicare is also increasingly willing to pay for ASC procedures. For example, total knee replacements were approved for ASCs in 2020 and total hips were approved in 2021. Although the reimbursement is lower in an ASC than it would be in a hospital setting, according to VMG Health’s ASC benchmarking analysis, orthopedics cases are the highest-reimbursing cases performed in ASC settings nationally [4]. Many physicians also prefer operating in a specialized ASC setting where they can control the patient experience and operating room setup and earn returns for driving efficiency in expenses and operational metrics. As shown in the data below, in response to these opportunities orthopedics-focused ASCs are among the fastest-growing types of ASCs, along with cardiology and pain management. Nationwide, providers are investing heavily in the equipment and unique buildouts required to specialize in orthopedics, such as 23-hour-stay recovery suites.

Source: MedPAC, 2023

To service the forecasted demand volumes and ensure that capital spent developing orthopedics-focused ASCs is optimized, there is a growing demand for orthopedic medical groups among private equity representatives, ASC operators, and health systems alike. Physicians are also increasingly interested in partnerships. Macroeconomic factors, such as inflation and rising costs of capital, compound the already burdensome administrative challenges facing healthcare providers. Factors such as declining reimbursement, shifts in payment models (fee for service, bundle pricing, value-based care), labor shortages, rising medical supply costs, and retiring providers have boosted physicians’ desires for partnerships. In choosing the most appropriate alignment model for partnership, physicians will be interested in monetizing their business’ equity and structuring their compensation package and strategic partner’s future vision.

Stakeholder alignment with orthopedic groups focuses on several key factors, a few of which are outlined below. While this is not an exhaustive list, the topics below highlight many salient considerations and value drivers for a medical group affiliation:

Does the orthopedic medical group have a favorable reputation in the community? Has the practice invested in modern infrastructure to enhance patient care and optimize practice management?

What is the medical group’s competitive position in the market? How does the medical group’s reputation and growth trajectory compare to those of their peers? Individually, what are each of the orthopedic physicians’ future outlooks?

How do the medical group’s provider base and productivity compare to national benchmarks? Does the medical group leverage mid-level providers? What are the current and projected compensation structures? Are key producers nearing retirement? Post-transaction, what would be the opportunities for key provider income repair if a portion of the earnings were sold forward in a transaction?

What complementary ancillary services are provided by the medical group? For example, is there a comprehensive range of orthopedics services, such as a surgery center, imaging, or on-site physical therapy?

Below we have outlined private equity, hospital, health system, and corporate entity stakeholders and the value they may attribute to alignment with orthopedics groups.

Private Equity

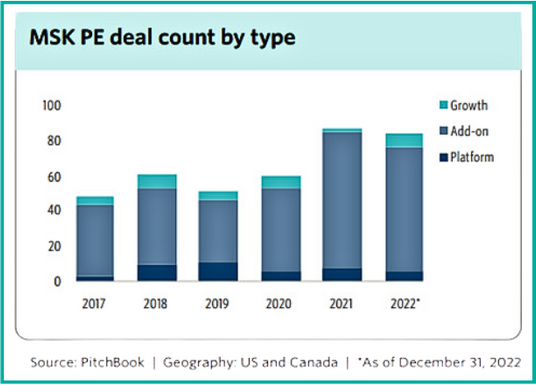

Orthopedics is one of the most active segments of the healthcare services industry for private equity investment. Compared to other clinical subspecialties, orthopedics remains highly fragmented across the nation. Moreover, the strong demand discussed above and a growing shortfall [5] of physician supply create highly favorable investment opportunities for private equity platforms seeking to form strategic partnerships with independent orthopedic groups. Below we have included a summary of the trending count of orthopedics-centered private equity deals in recent years.

Health Systems

For many health systems, partnering with orthopedic physician groups provides an opportunity to partially recapture profitable inpatient cases, as they have transitioned to physician-owned ASCs. We have seen numerous care models evolve and expand recently, such as joint ventures with local orthopedics groups to construct de novo, highly specialized orthopedic surgery centers. The benefits of such an arrangement could include the following:

Specialized ASCs allow for highly skilled staff and have facilities structured for top-tier patient quality and outcomes

Opportunities to create de novo ASCs and realize returns through joint affiliation

Physicians capitalizing on health system brands, debt rates, and supply chain efficiencies

Partnership with a health system may allow more favorable contracting compared to an independent context

ASC Operators

For ASC operators, orthopedic group partnerships represent an opportunity to gain market share and leverage their existing ASC expertise. The benefits of partnering with ASC operators could include the following:

Access to and guidance in operational best practices for ASCs, potentially improving care quality, patient outcomes, and returns

Relief of management/administrative burden on providers through access to a strategic partner, for example, recruitment assistance

Access to ASC operator debt rates and supply chain efficiencies

The right partnership can provide orthopedics groups with access to resources and expertise to improve their competitive advantage and patient care through the relief of administrative burdens and improved financial stability. Physicians should consider their long-term goals when evaluating potential partnerships and offers. For future stakeholders, including corporate entities, health systems, and/or ASC operators, the potential value of an orthopedics group extends beyond the bottom line of the organization. By joining forces, orthopedics providers and their partners can bridge the gap between expertise and resources. Alignment with the right partner can improve patient outcomes and elevate the standard of care for orthopedic patients at a more efficient cost.