Hospitals and health systems have been developing strategies for vertical integration with physician groups for decades. Through the premise of integrated care delivery, “defined as a coherent set of methods and models on the funding, administrative, organizational, service delivery and clinical levels,” U.S. policymakers, healthcare operators and payors expect to improve the quality, service and efficiency of healthcare services. Results of value generated through integrated delivery models are mixed, and the operating model is often confounded with varying market dynamics (payor concentration, culture, physician supply/demand, leadership, etc.) by community.

Regardless of integrated care delivery success, health system employment continues to increase and today accounts for greater than 50% of all practicing physicians. Interestingly and unknown to many, other strategics (private equity, Optum, CVS, etc.) account for approximately another 25%, leaving approximately a quarter of physicians organized in a private practice.

Figure 1: 2023 Physician Employment by Type

Source: Physicians Advocacy Institute: Physician Practice Trends Specialty Report

Across many integrated delivery systems, physicians are organized under a formal medical group structure, often with supporting leadership, governance, and practice management systems. This structure essentially groups the collective interests of primary care, surgical subspecialists, medical subspecialists, and hospital-based physicians together. Unlike independent, multispecialty practices who have an underpinning of sharing economics, most multispecialty groups in integrated delivery systems lack material financial alignment across subspecialties.

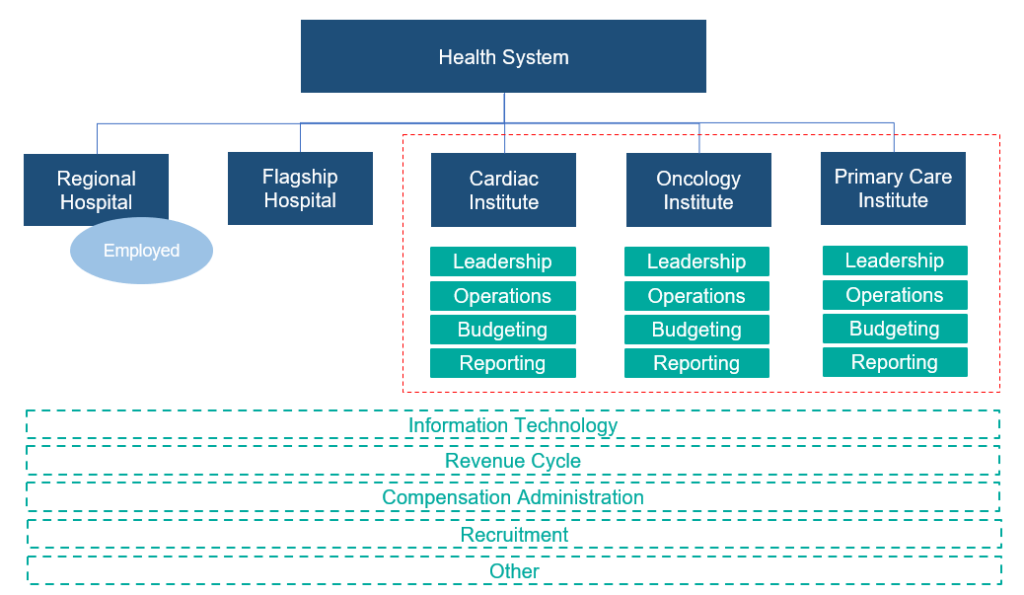

To this end, there are several challenges with a multispecialty group structure in health systems, including an aggregation of physician losses whereby various revenue streams (e.g., in-office ancillaries) have been integrated with hospital operations, sensitivity to practice losses based on confounding facts as to the true operating performance, silo board and/or decision making, and frustration by large clinical service lines due to widely held convention that everything needs to be the same for all physicians across the physician enterprise. Figure 2 outlines the most prevalent medical group structure and its multispecialty orientation.

Figure 2: Prevalent Medical Group Structure for Employed Physicians

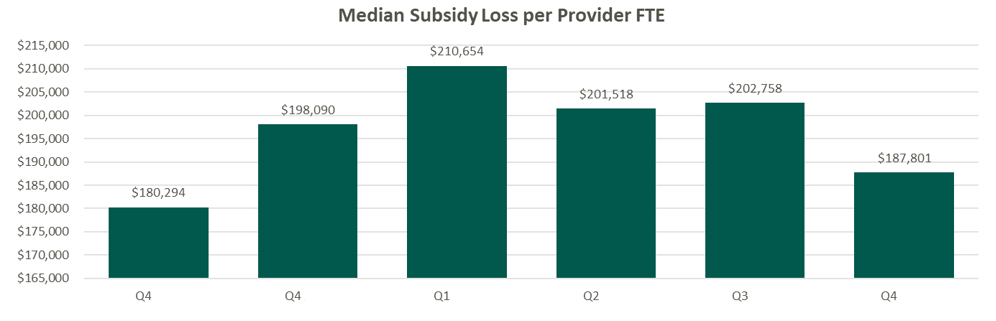

Financial system reporting remains inconsistent across organizations; however, there are data repositories that suggest continued median subsidies for employed providers. As figure 3 outlines, regardless of timing and/or subspecialty orientation, there remains a significant net investment per provider.

Figure 3: Median Subsidy (Combined Subspecialty Mix)

Source: Kaufman Hall Flash Reports

Based on VMG Health’s experience, significant financial reporting subsidies lead to suboptimized decision making, as significant pressure is placed on medical group leadership to reduce practice losses and improve overall practice performance. This has led to a variety of strategic missteps for organizations operating in competitive markets.

As an alternative, VMG Health has been working with clients to reorganize physician enterprise offerings inside of integrated delivery systems, including the development of financial reporting, management, and governance systems that better align care delivery across service lines. These more contemporary structures, while variable system to system, are all designed to:

- Boost physician loyalty to their primary clinical practice location (e.g., office based, value-based orientation, hospital, ASC, etc.).

- Improve leadership, financial reporting, and budgeting so that business units are accountable for both facility- and professional-level operations and key performance indicators.

- Afford focus on best-in-class infrastructure to support all professional practice applications.

- Remove silo barriers and outdated concepts of medical group subsidies and associated strategic implications from an antiquated structure.

Figure 4: Contemporary Medical Group Structure

Conclusion

The landscape of physician organizational structures within hospitals and health systems remains in transition. While traditional, multispecialty group practice models remain prevalent, challenges such as physician losses and inconsistent financial reporting have spurred the need for more contemporary structures. Through strategic reorganization and improved governance, health systems can enhance physician loyalty, accountability, growth, and operational efficiency, ultimately optimizing care delivery and aligned (or improved) financial performance.

Sources

Heeringa, J., et. al. (2020). Horizontal and Vertical Integration of Health Care Providers: A Framework for Understanding Various Provider Organizational Structures. National Library of Medicine. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC6978994/