Written by Josh Miner, Savanna Ganyard, CFA, and Taryn Nasr, ASA

The Ambulatory Surgery Center (ASC) market is a fast-growing sector of healthcare that is attracting considerable interest from private equity (PE) funds across the country. The following outlines the current state of the market as well as key factors driving ASC market growth and attracting PE investment.

Private Equity Industry Outlook

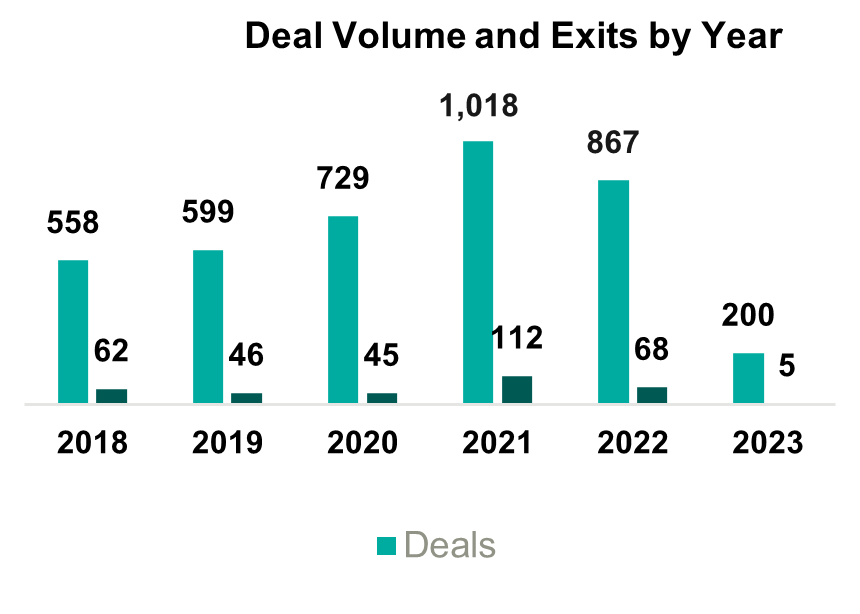

2021 saw the most PE-related healthcare transactions in history, with an estimated 1,018 transactions occurring throughout the year. During the first quarter of 2023, transaction activity slowed from the pace set in 2021, primarily due to macroeconomic factors including inflationary pressures, rising interest rates, and higher labor costs. Additionally, rising interest rates and tight credit have increased the cost of debt leading to a reduction in leverage of one to one-and-a-half turns. Uncertainty surrounding the bank debt market has led PE investors to turn to private credit and other deal strategies. These strategies include searching for smaller deals where securing financing may be easier or targeting add-ons that are small enough to purchase without debt.

Despite the recent slowdown in activity, it is likely that the deal volume will rebound as macroeconomic uncertainty eases, but, in the short term, PE firms will likely continue to target smaller platform deals and add-ons. These transactions will likely involve independent targets, as other institutional investors may not attempt an exit in the current economic conditions.

Ambulatory Surgery Center Industry Overview

The ASC market was recently sized at $84 billion in 2020 and is projected to grow at a compounded annual growth rate (CAGR) of 3.9% to $131 billion by 2031. The industry is highly fragmented with 70% of ASCs independently owned and the remaining owned by larger conglomerates. Over the past several years, PE ownership in the ASC space has steadily increased. Two of the largest players in the industry, AmSurg and Surgery Partners, have PE ownership. Other major ASCs with PE ownership include Covenant Physician Partners, EyeCare Partners, Gastro Health, GI Alliance, HOPCo, PE GI Solutions, and Value Health. Notably, Bain Capital’s $3 billion leveraged buy-out (LBO) of Surgery Partners in 2017 remains the largest deal completed in this space.

The expected growth in the ASC industry is driven by numerous factors including a shift towards lower cost procedures. On average, patients save $684 per procedure at an ASC as compared to a hospital based on a 2021 report from UnitedHealth Group. Specifically, orthopedics is a growth area driven by cost savings. On average, ASCs reduced the cost of orthopedic procedures by 17% to 43%. These cost savings at an ASC lessen the burden on the patient and help boost margins in an ASC setting. As a result, orthopedics continues to be a popular specialty for investors pursuing an ASC strategy.

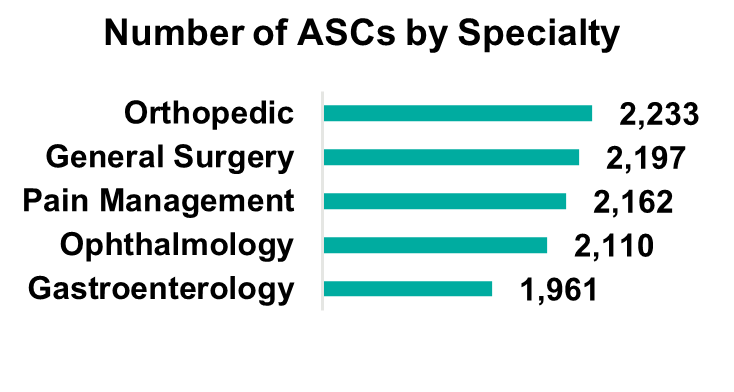

Orthopedics remains the most popular specialty, but gastroenterology, pain management, and ophthalmology make up large portions of the market. Notably, cardiology has become the fastest-growing specialty as ASCs invest in technology and higher acuity procedures continue to move to the ASC setting. The demand for cardiology is driven by an aging population and the level of cardiovascular disease in U.S. adults (e.g., half of all U.S. adults have cardiovascular disease). While cardiology is currently primarily a hospital-based specialty, with 70% of cardiologists employed by hospitals, as this specialty moves into ASCs there is a unique opportunity for PE firms to secure a foothold in a fast-growing segment.

On January 31, 2023, Lee Equity Partners (LEP) completed a buyout of the Cardiovascular Institute of the South (CIS) for an undisclosed amount (of note, LEP deals typically range from $50 to $150 million in equity). CIS has 21 locations across two states and employs over 60 physicians. This deal represents one of the larger buyouts of an ASC in recent memory and illustrates the growth of cardiology as a specialty in ASCs.

As more cases and specialties shift to an ASC setting, there is an increasing patient demand for multi-specialty ASCs. Patients are seeking convenience in the ability to receive treatment for a multitude of treatments in one place. The number of multispecialty ASCs is forecasted to expand at a 4.3% CAGR, outpacing general ASC market growth.

Ambulatory Surgery Centers and Private Equity

These industry characteristics coupled with the PE industry outlook should continue to drive transactions within this space, specifically among the 70% of independently owned ASCs. Due to recent macroeconomic factors, we expect PE firms to continue to pursue smaller add-on deals aimed at consolidating several ASCs in an area. These types of transactions allow PE firms to capitalize on industry trends, optimize cost-cutting opportunities, and generate attractive returns. On the other hand, these transactions are also attractive to independent and physician-owned ASCs due to the benefits of a larger growth infrastructure which can leave more time for physician owners to focus on patient care.

Conclusion

ASCs can offer cost savings and convenience to consumers without sacrificing quality of care. Due to increasing demand, the number of specialties, and the ability to perform high-acuity procedures, the ASC market is projected to grow steadily over the next decade. Market growth, combined with the availability of investment opportunities due to the fragmentation of the market, will continue to attract PE investment. As macroeconomic conditions become less uncertain, it is likely that PE investment will continue to rebound to historical levels in the healthcare industry. Furthermore, the many attractive qualities of the ASC industry should draw investment in the space.

Sources

- BH Sales Group. (2023). Industry Overview June 2023. ASC Data.

- Avanza Healthcare Strategies. (2022). 2022 Key ASC Benchmarks and Industry Figures.

- PitchBook. (2023, May 9). Healthcare Services Report: Q1 2023.

- Newitt, P. (2022, November 29). The specialties driving ASC growth. Becker’s ASC Review.

- Newitt, P. (2023, May 4). 3 numbers pointing to ASC growth. Becker’s ASC Review.

- Condon, A. (2021, October 7). 3 key trends driving ASC market growth. Becker’s ASC Review.

- VMG Health. (2023). 2023 Annual Healthcare M&A Report.

- BH Sales Group. (2023). ASC Industry Overview.