Written by Grace McWatters, Victor McConnell, MAI, ASA, CRE, Larry Snyder, MAI

Largely driven by growth in the biotechnology research and development segment, real estate associated with the life sciences, which utilizes a combination of office, flex, and lab space, has emerged as a highly favored asset. Accounting for approximately 100 million square feet of product[1], these facilities are primarily concentrated in approximately a dozen markets throughout the United States.

In 2020, the life sciences sector has continued to grow, demonstrating its resilience despite the COVID-19 pandemic. While the industry’s resistance to economic downturns is not new, increased global attention has been spurred, in part, by the international effort to develop a vaccine for COVID-19. Billions of government dollars have been directed to the sector via Operation Warp Speed (OWS)[2] in order to accelerate the development and distribution of a vaccine. Increased government funding combined with the continued flow of capital via NIH research grants and venture capital investment serves to illustrate the industry’s current growth climate.

This article will outline overall trends within the life sciences sector, with a particular focus on the real estate market. Furthermore, we will identify the primary and emerging hubs within the United States, document a decade’s worth of expansion in terms of employment and funding, outline key players in the industry, identify trends resulting from the outbreak of COVID-19, and illustrate the sector’s market fundamentals in terms of supply and demand, rents and vacancy, and cap rates and pricing.

Demographics and Trends

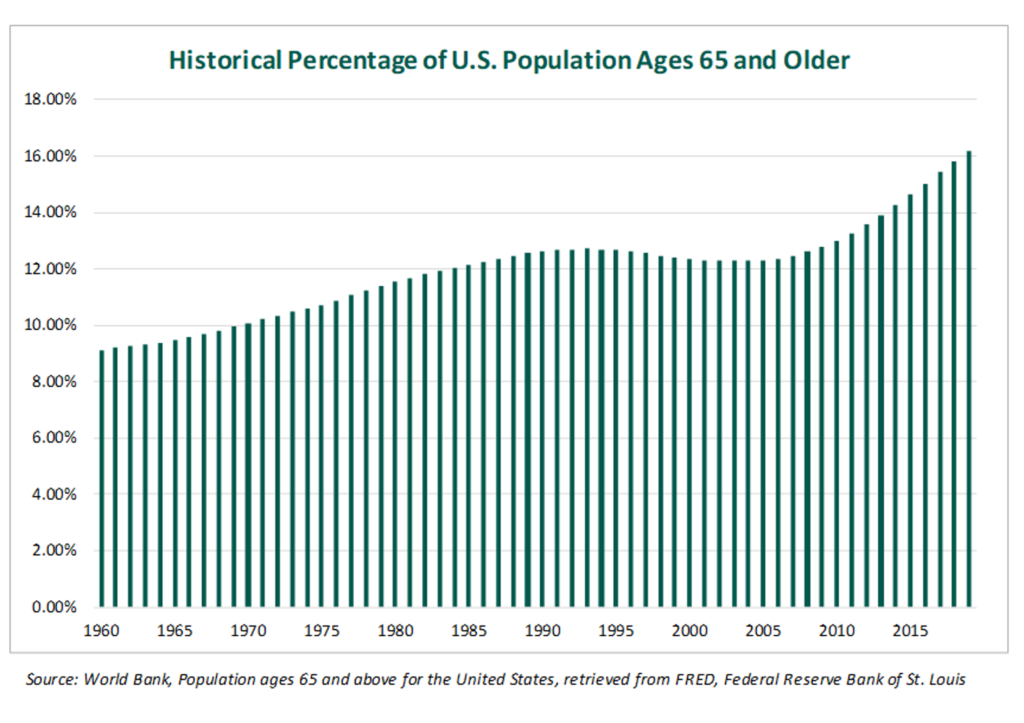

The sector has continued to expand as technological innovation affords more medical breakthroughs to an aging population. According to the U.S. Census Bureau, in 2005, the median age in the U.S. was 36.2 years.[3] In 2018, the median age was 38.2 years[4]. The median age in 2030 is projected to be over 40 years.[5] Moreover, by 2030, the number of people 65 and older is projected to surpass 73 million, or about 21% of the population.[6] Overall, the American population is, on average, growing older, and life spans continue to increase. Like most healthcare verticals, the life sciences sector is expected to benefit from the current demographic trends in the United States.

The following graph[7] shows the historical percentage of the U.S. population ages 65 years and older as of 2019.

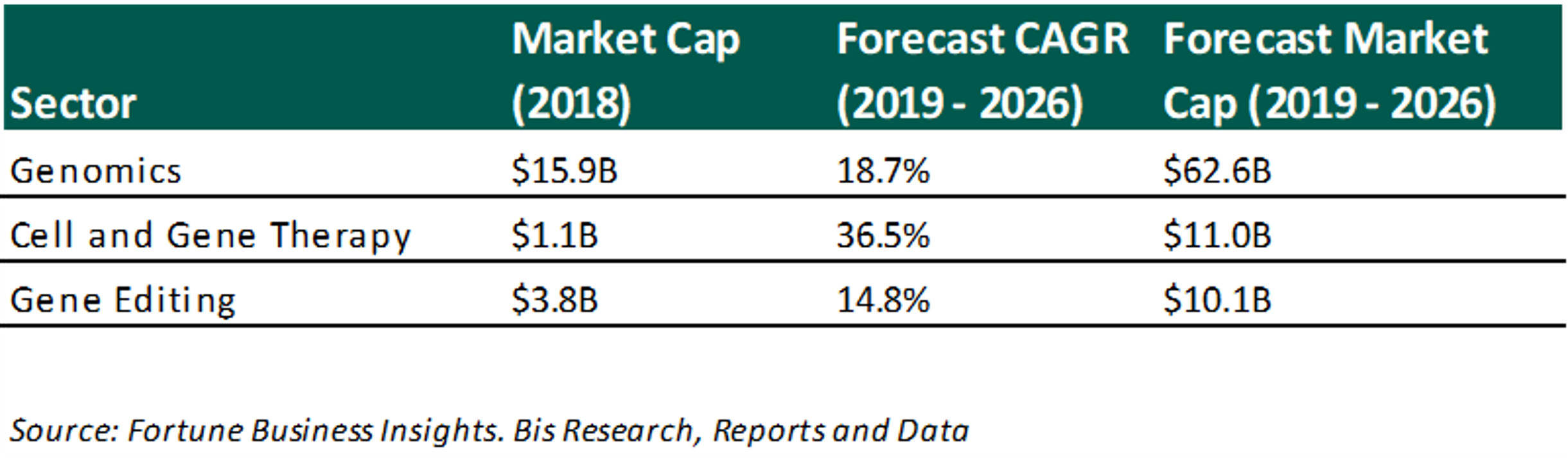

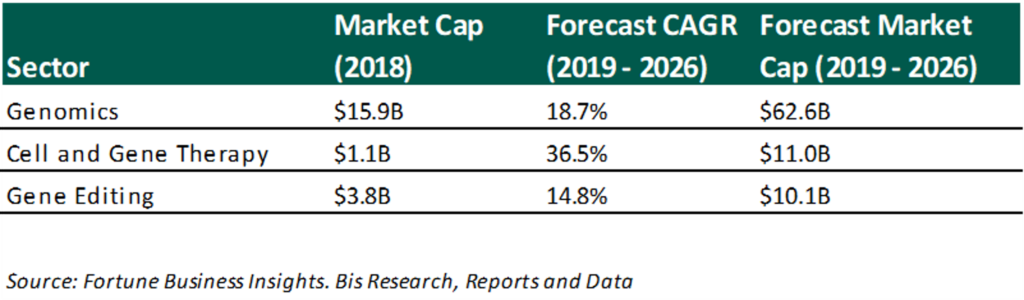

With more consumers on the horizon and technological advancements lowering both costs and failure rates, the life sciences sector expects robust growth in the next decade. Several subsectors, shown below, have compounded annual growth rates projected to exceed 10%[8]. The subsectors with the most growth are related to identifying and potentially modifying DNA in order to reduce risk of disease in humans, animals, and agriculture.

Primary and Emerging Hubs

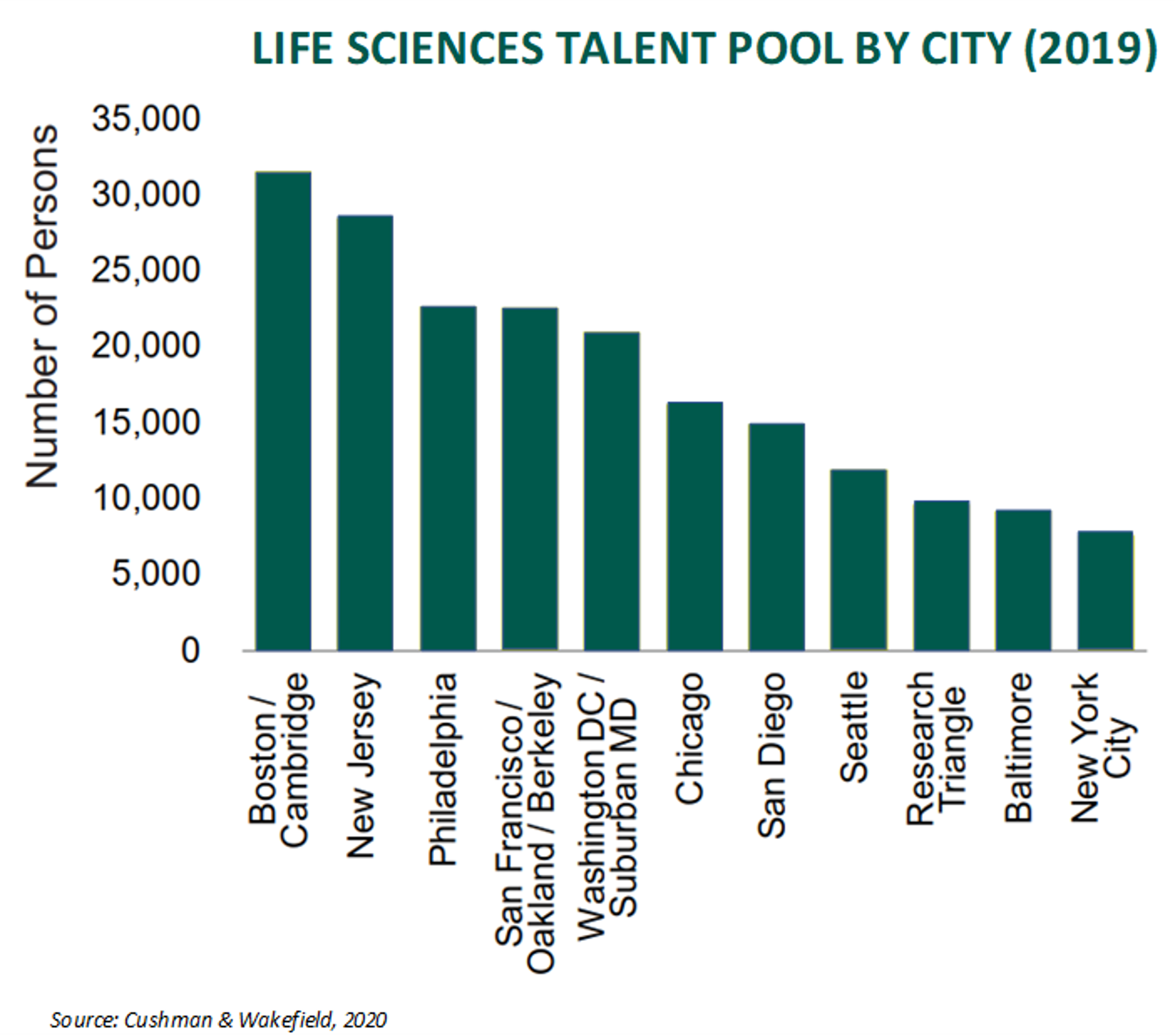

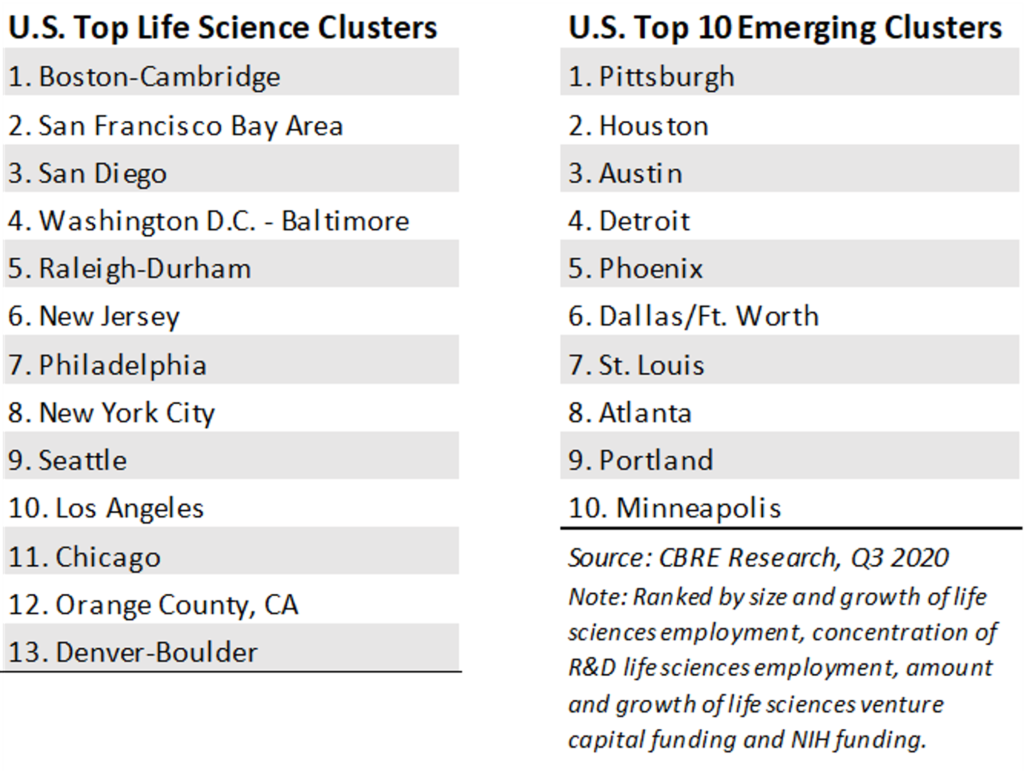

As the influence of life sciences grows, more cities are catering to the industry’s needs. Life sciences are concentrated in over a dozen markets in the United States. Facilities are strategically located within these markets to follow talent and access outside funding. It is easier to acquire funding in a primary market because, if a facility “goes dark,” an investor/landlord will need to re-lease the space or sell to a new owner/user, which could take a considerable time and considerable investment in tenant improvements; a location in a primary market improves a landlord’s ability to re-tenant. Proximity to other life science tenants, access to funding, and a strong talent pool decreases the lease-up time for abandoned facilities, partially mitigating risk associated with a highly specialized build out. Cities or metros where these facilities are concentrated are referred to as “clusters.” Boston-Cambridge, the San Francisco Bay area, and San Diego are the three largest clusters for life sciences within the United States. The following chart identifies the top and emerging life science clusters in the country.[9]

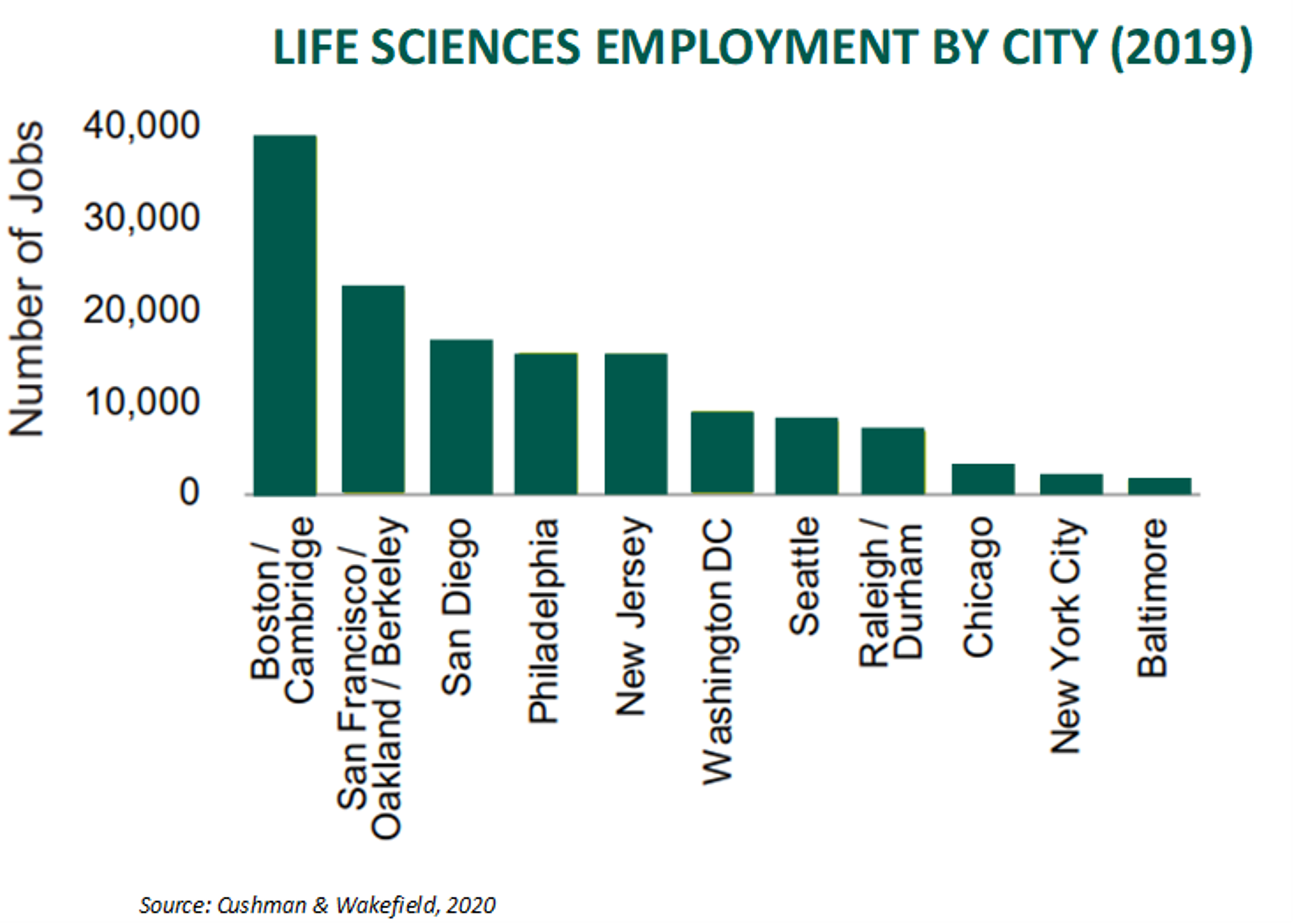

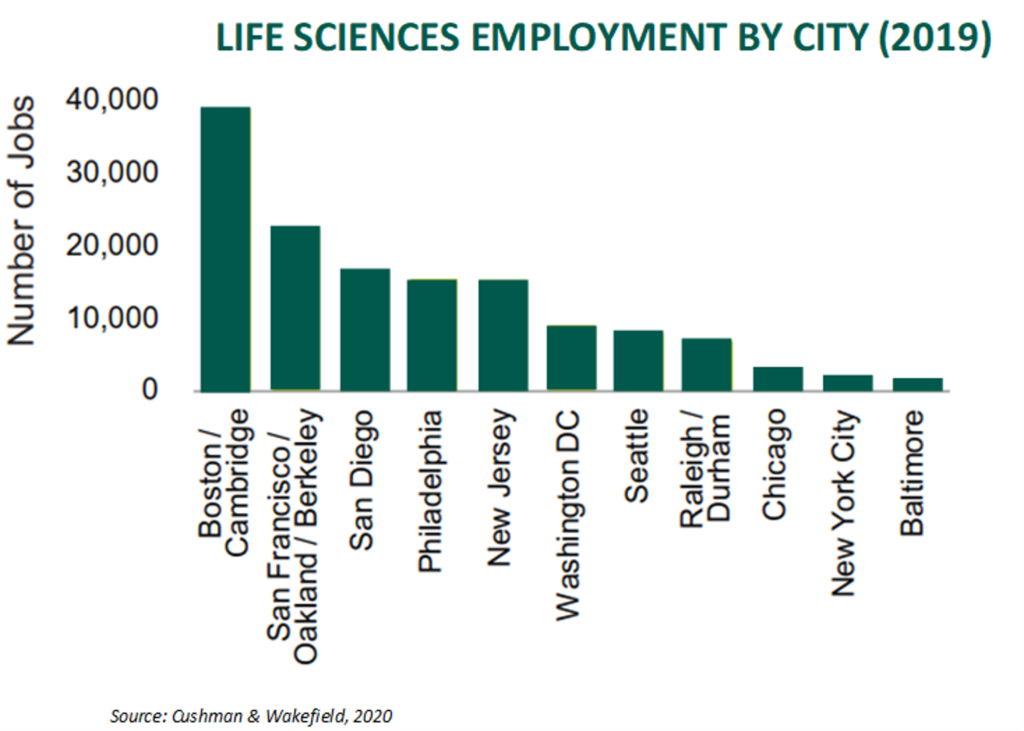

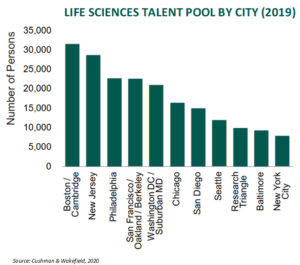

Employment in life sciences totaled 204,800 in 2019. 67% of these jobs were located within eleven clusters, shown as follows.[10]

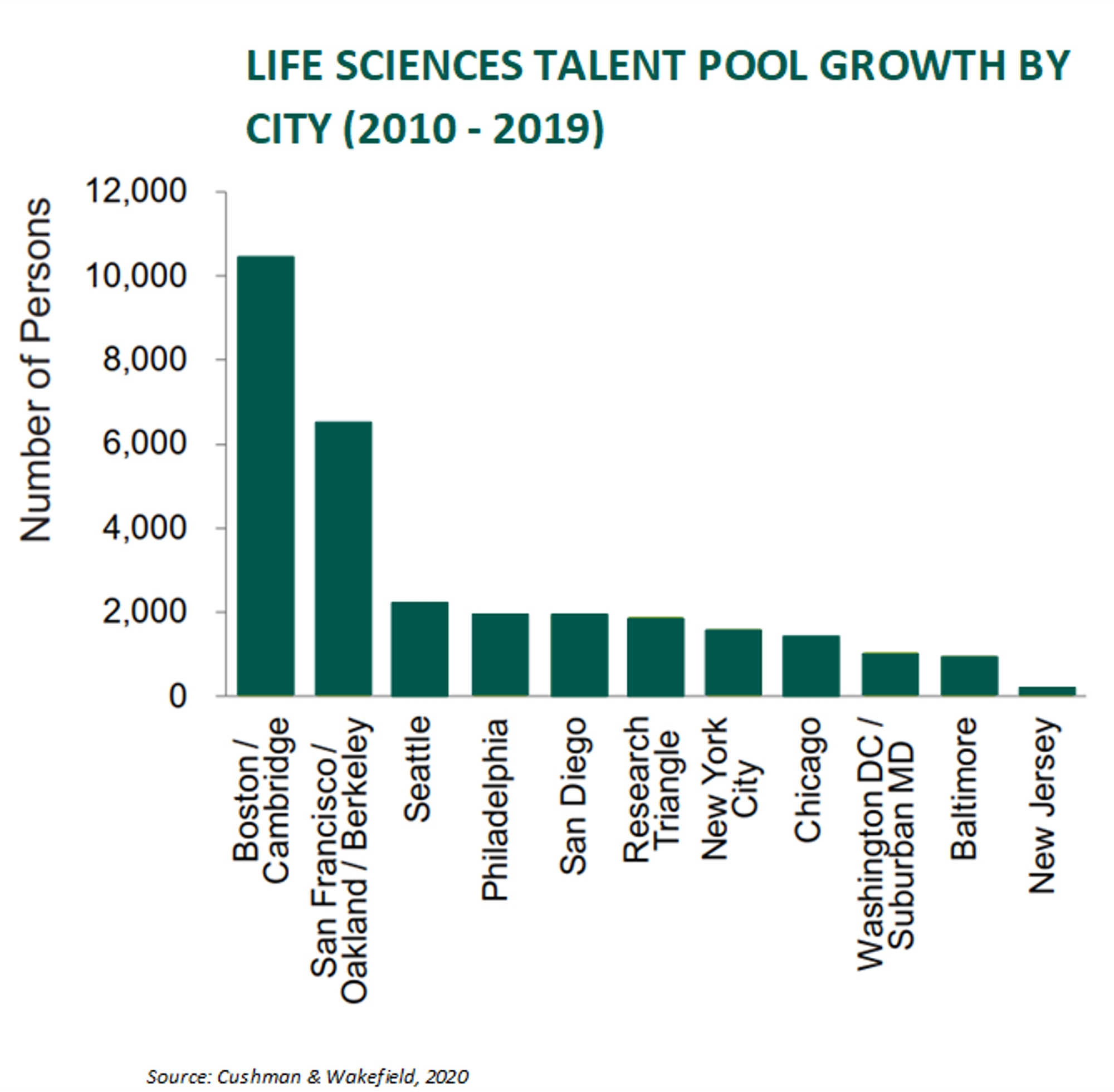

San Francisco Bay area, Boston-Cambridge, and San Diego have the most employees and highest square footage of life sciences real estate in the United States.[11]

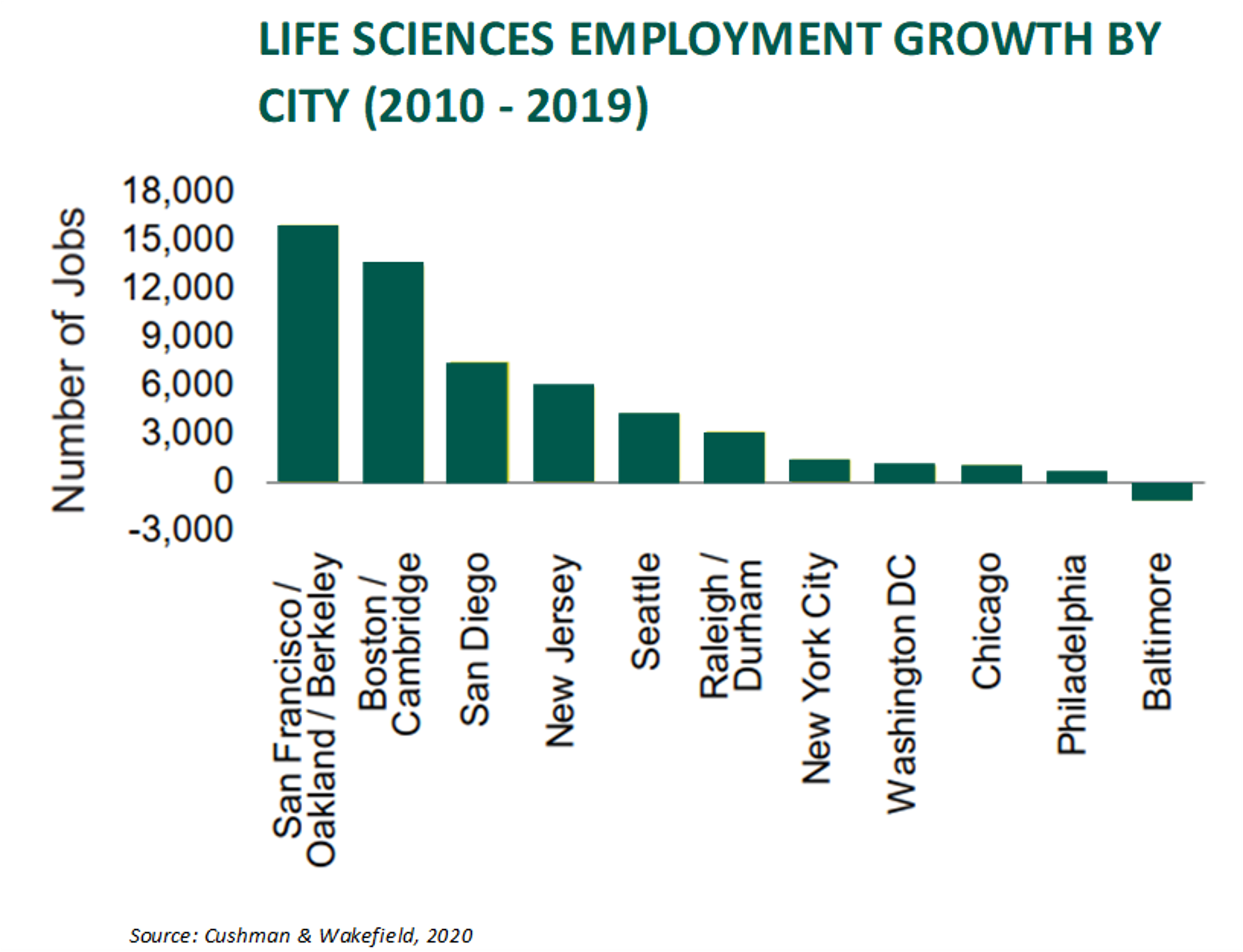

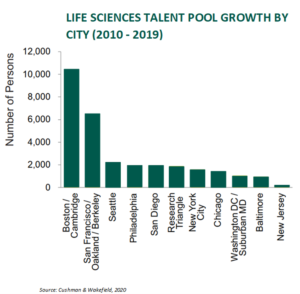

New Jersey is recognized as having a strong talent pool because it is home to several major pharmaceutical manufacturers.[12] However, the area’s talent pool has not grown much in the last decade. The majority of the growth has been in Boston-Cambridge and the San Francisco Bay area.

Employment Growth

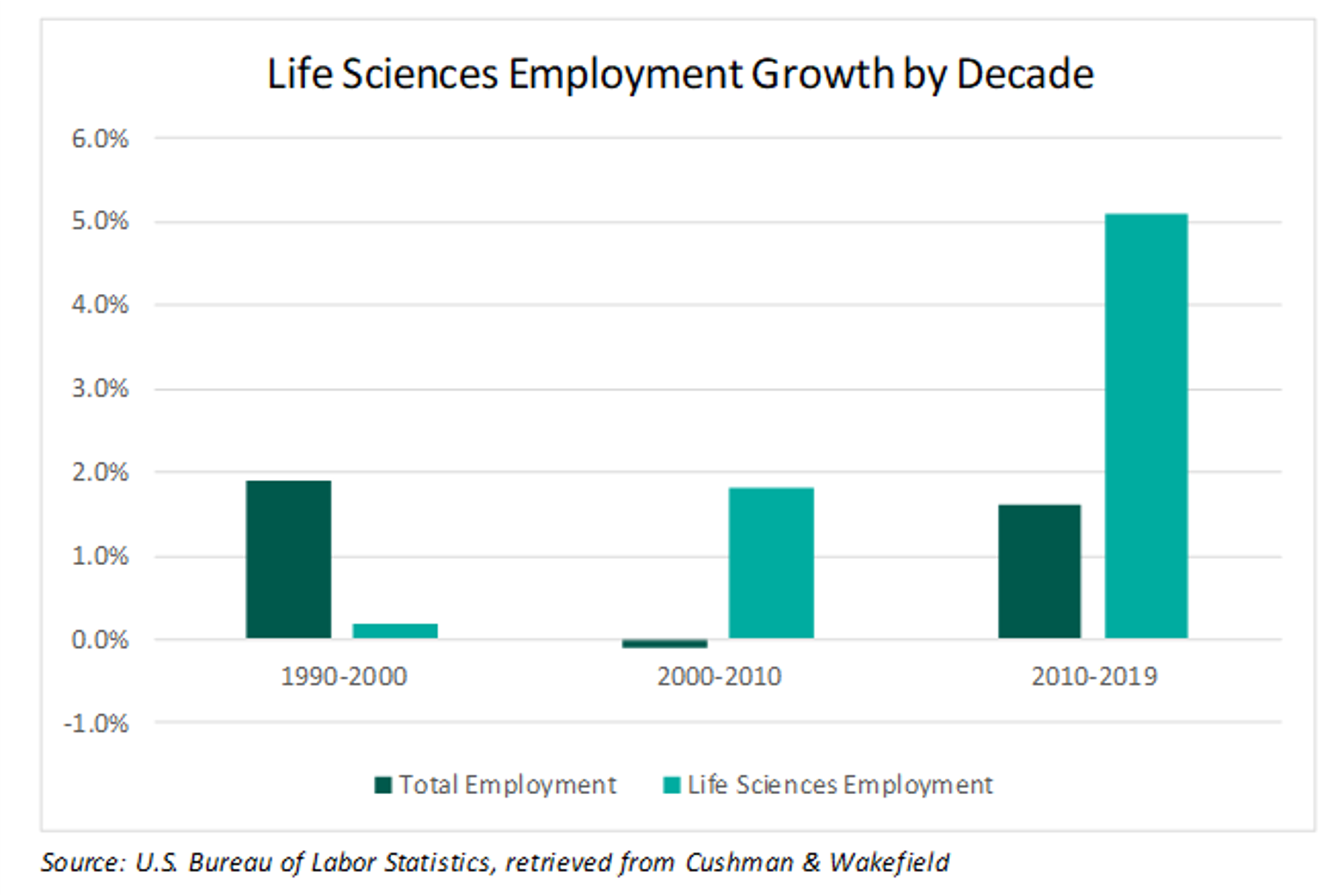

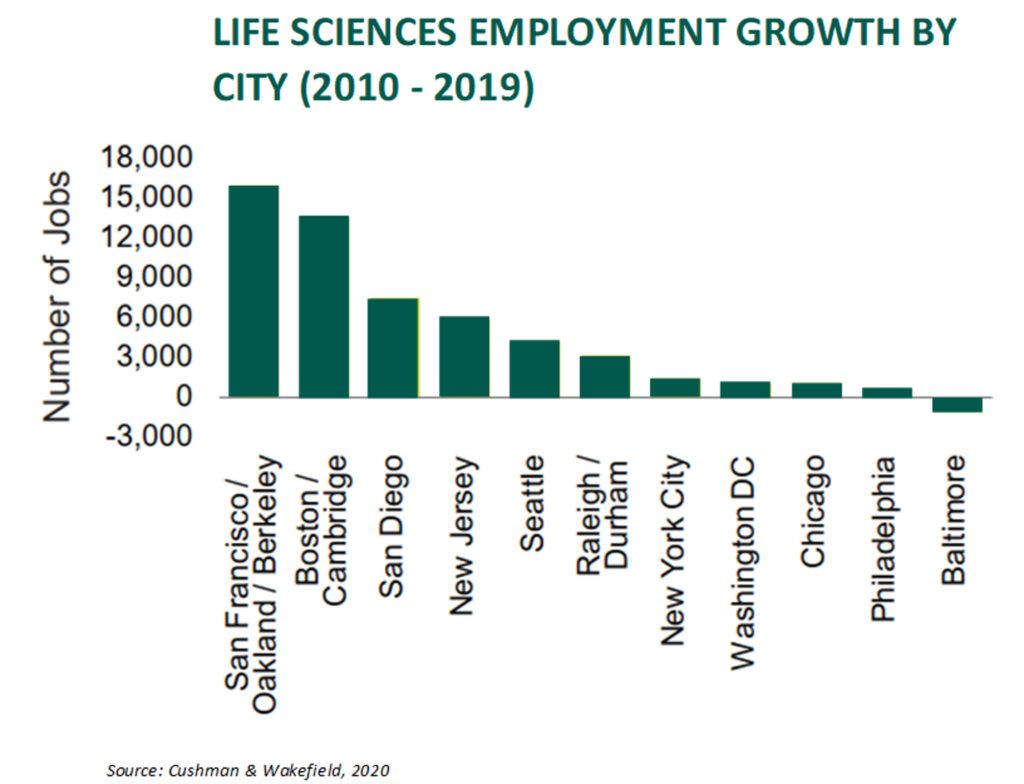

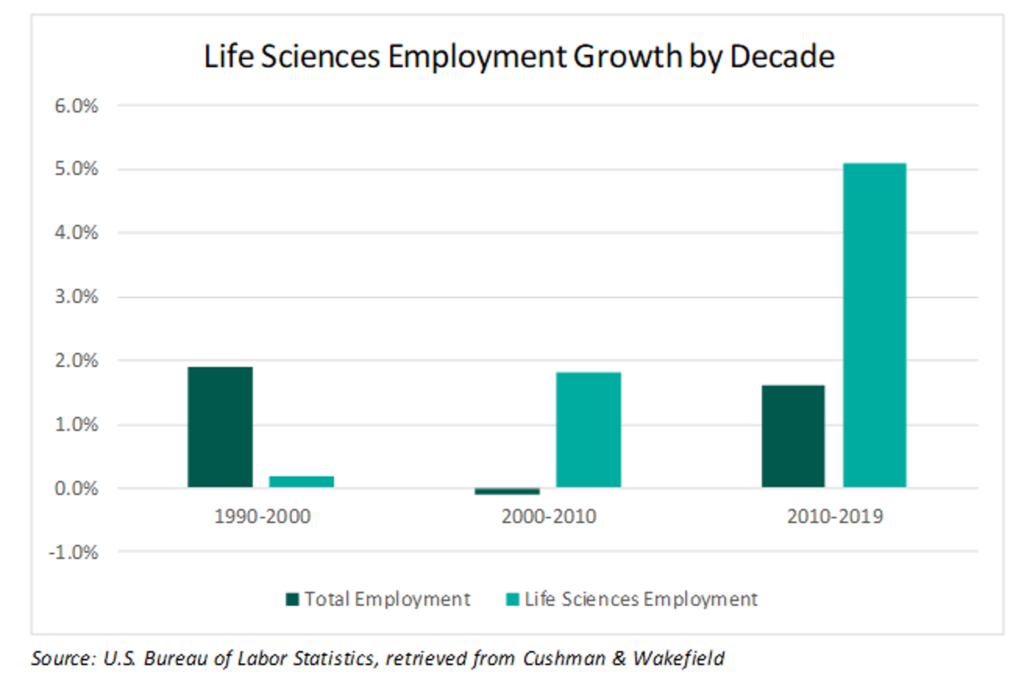

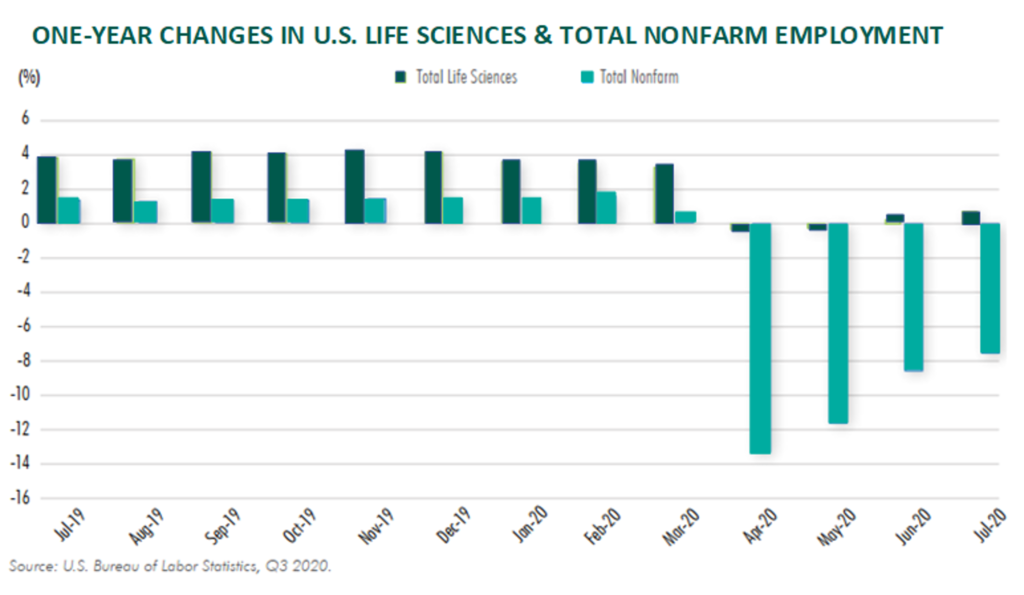

The life sciences labor market grew in 2020 despite the high levels of joblessness across the country due to the COVID-19 pandemic. CBRE finds that life science employment is 1% higher than a year ago.[13] CBRE also notes that Biotech R&D saw the greatest employment gains: they are up 4.9% from a year ago.[14] This subsector has grown over 88% from 1999 to 2019.[15] Life sciences employment is growing rapidly and has, on average, outpaced total employment growth since 2000.[16]

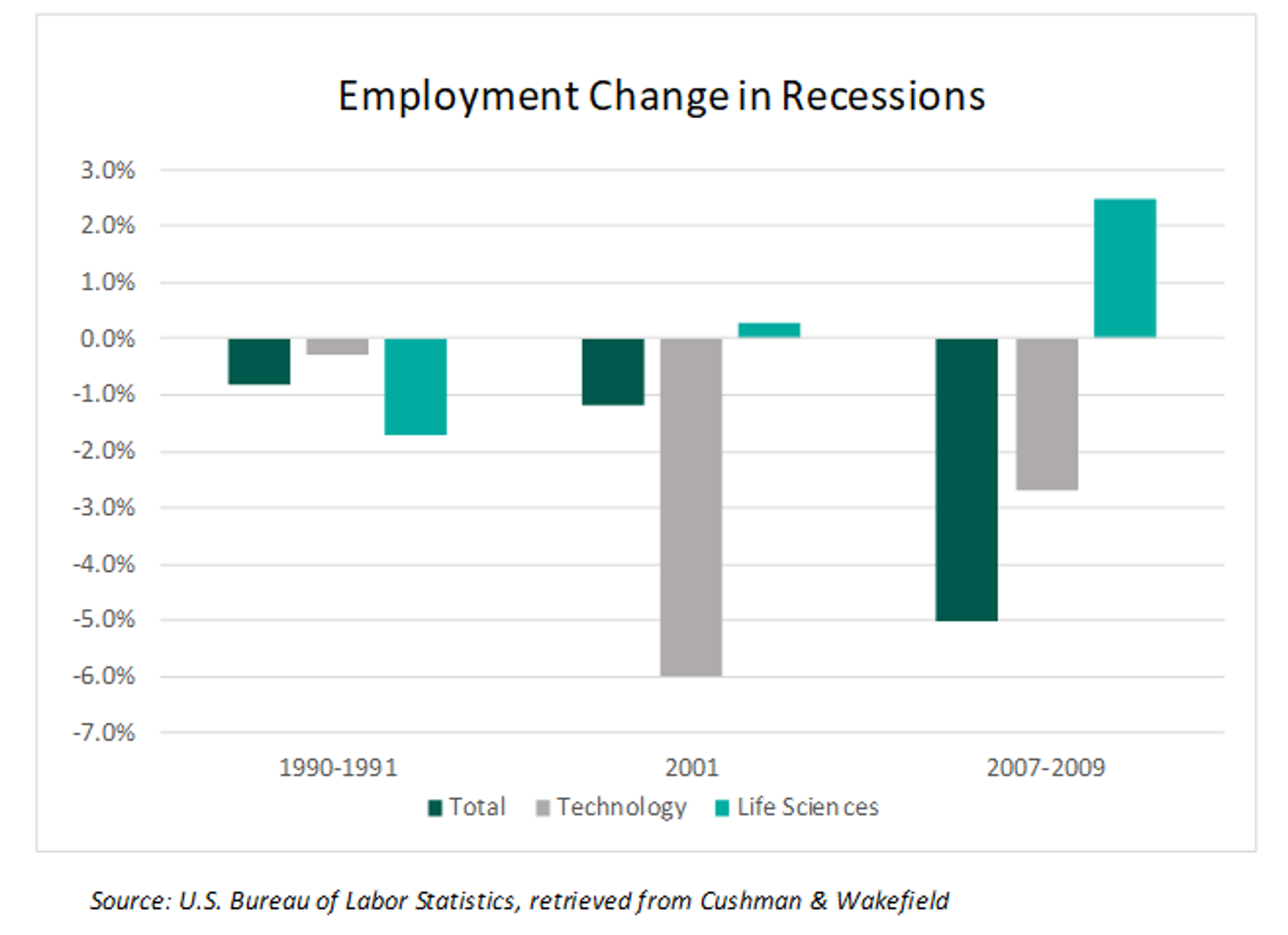

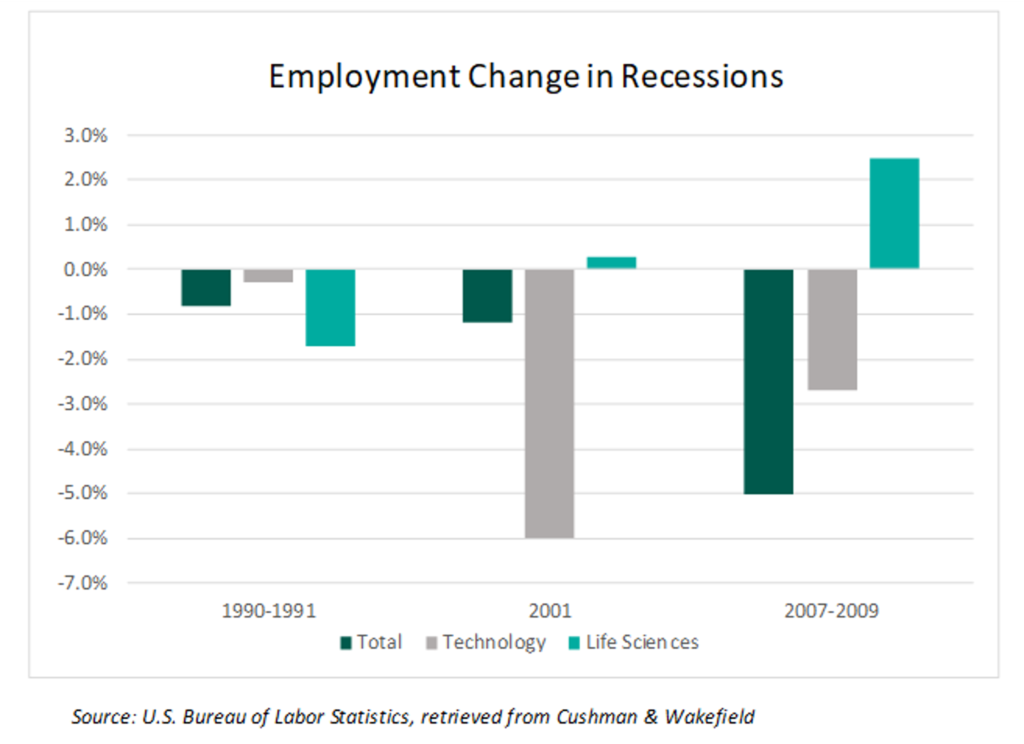

Life sciences tend to fare well in recessions. Since 2000, employment in life sciences has increased 87.9% compared to 14.4% as a whole for the U.S.[17] During the two economic downturns since 2000, life sciences outperformed the economy as well as the tech sector, which helped the industry earn a reputation as being somewhat recession resistant. The following chart illustrates unemployment fluctuations during previous recessions.[18]

While not entirely unscathed by the events of 2020, life sciences employment was less volatile when compared to total nonfarm jobs during the COVID-19 pandemic.[19]

Increased Funding

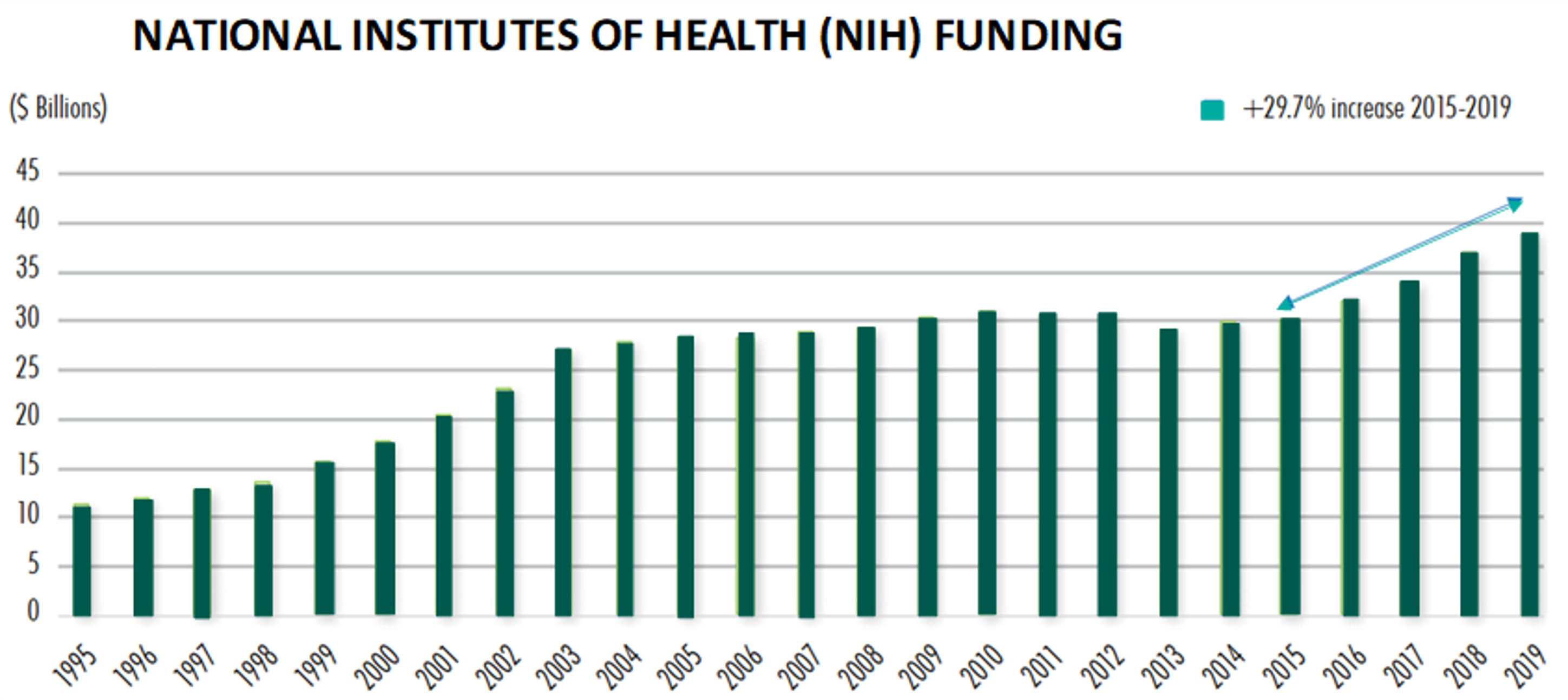

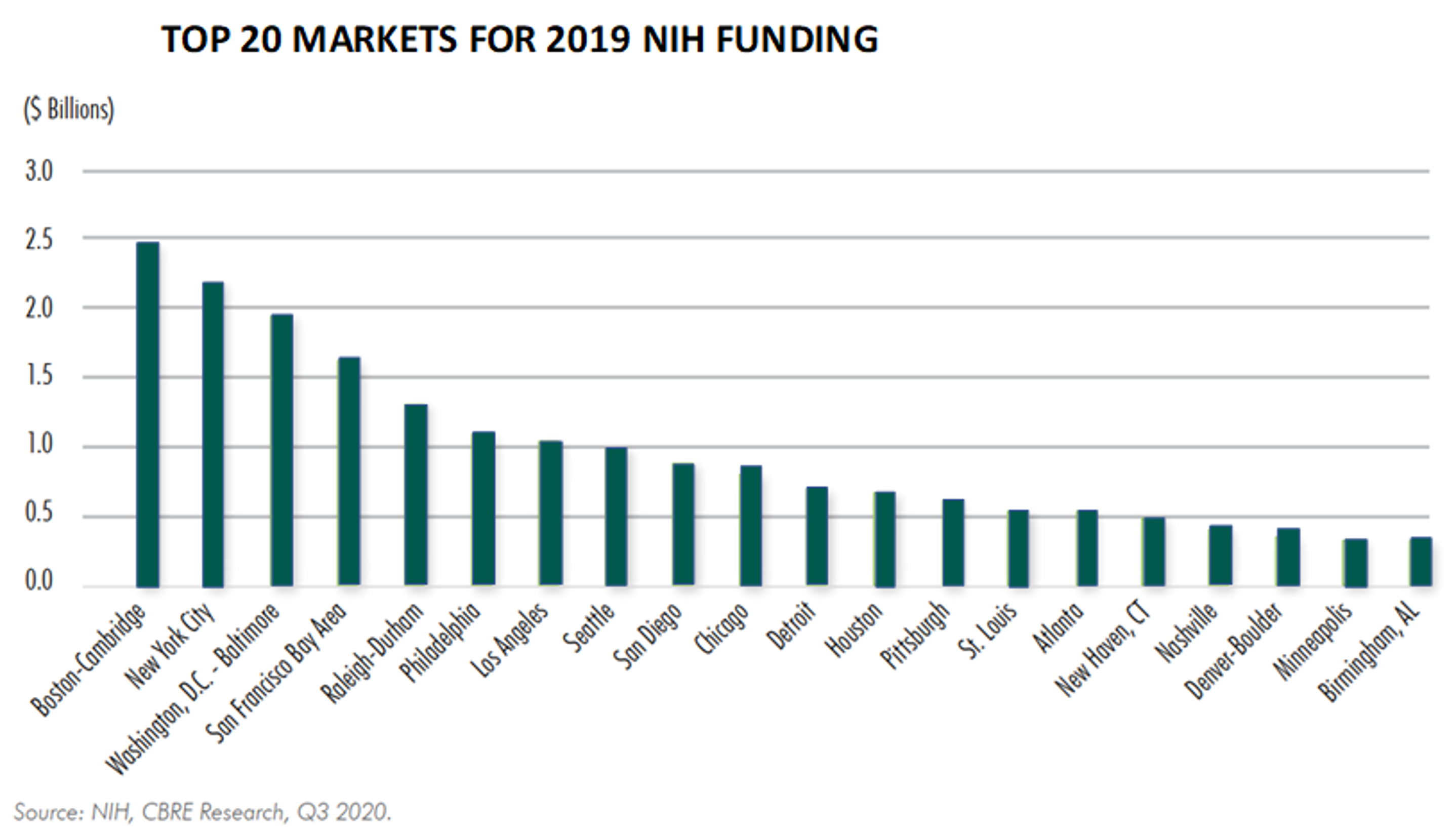

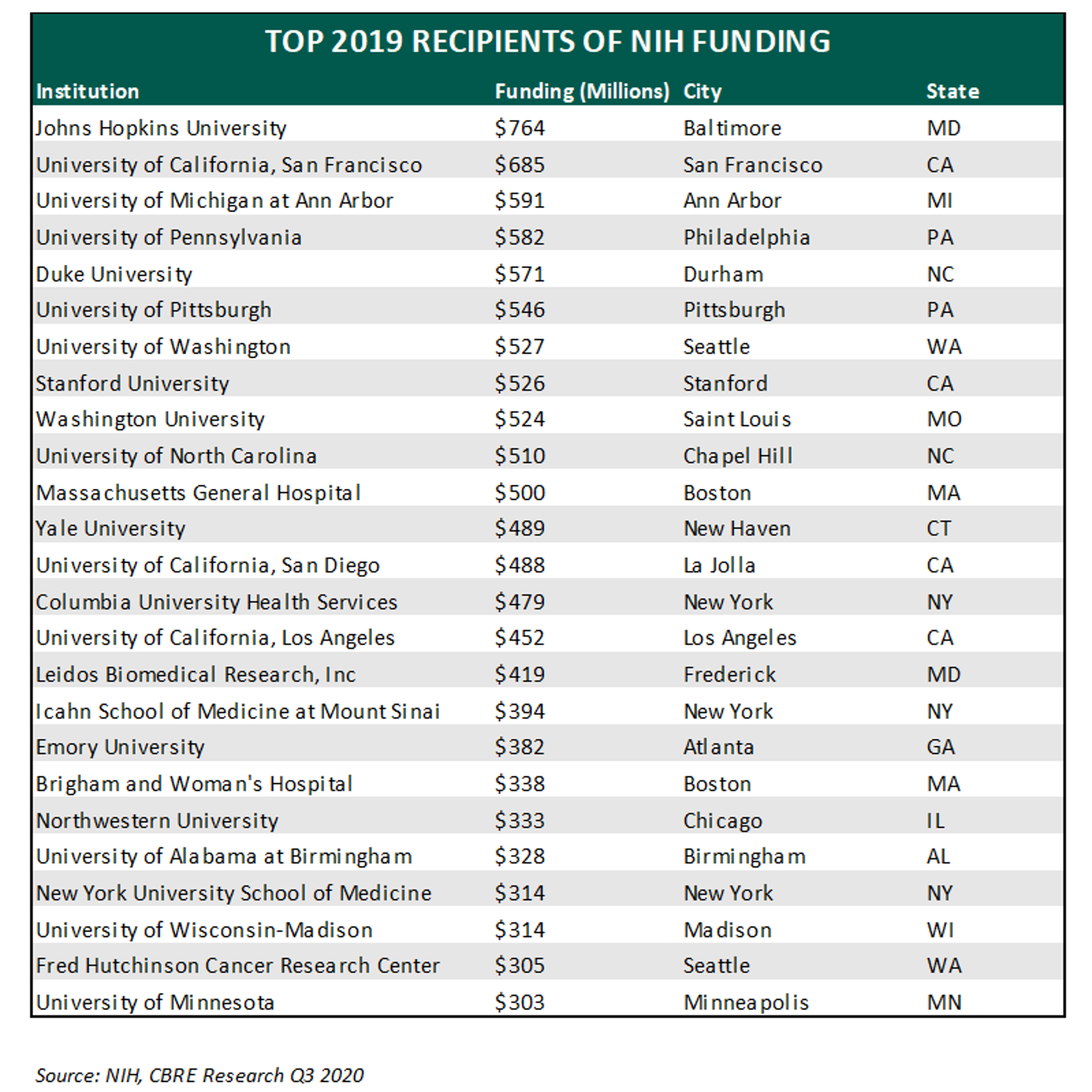

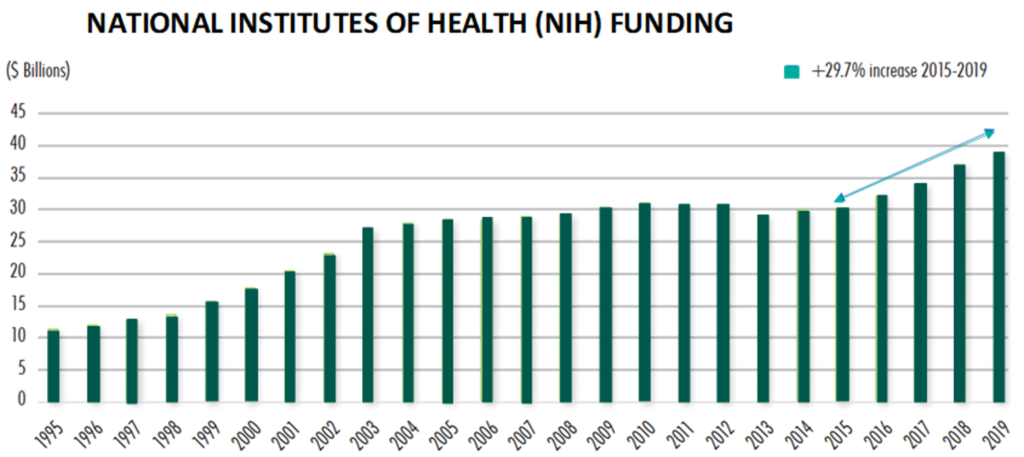

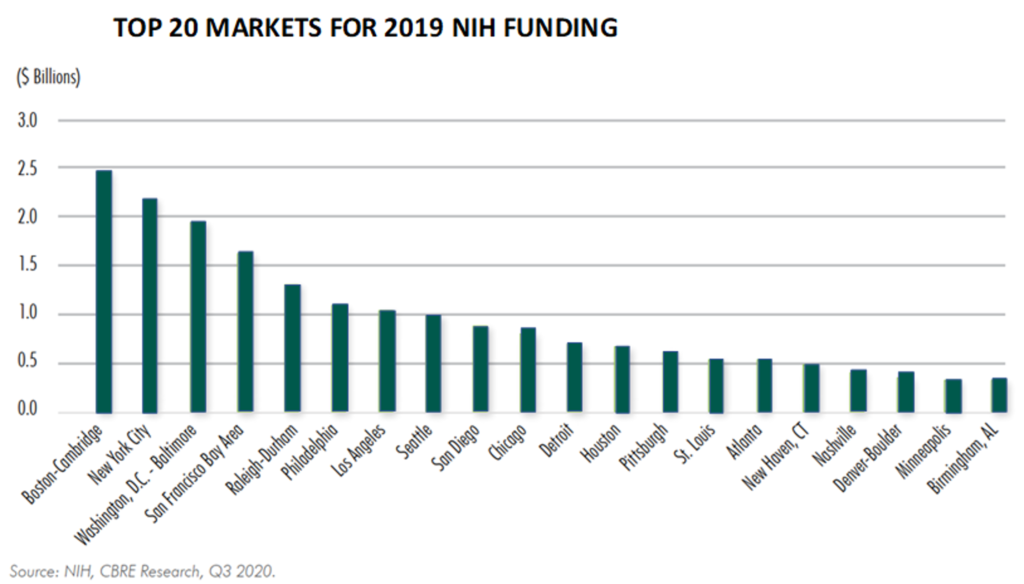

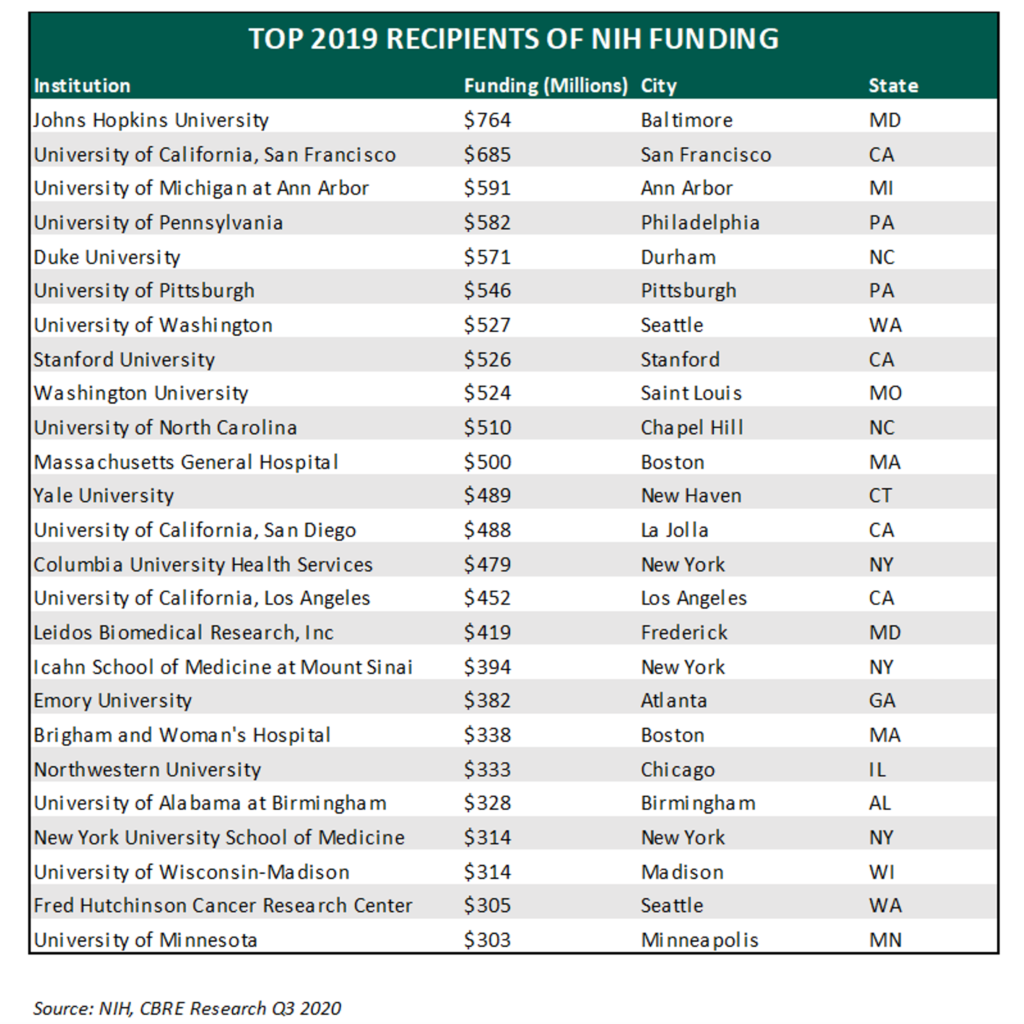

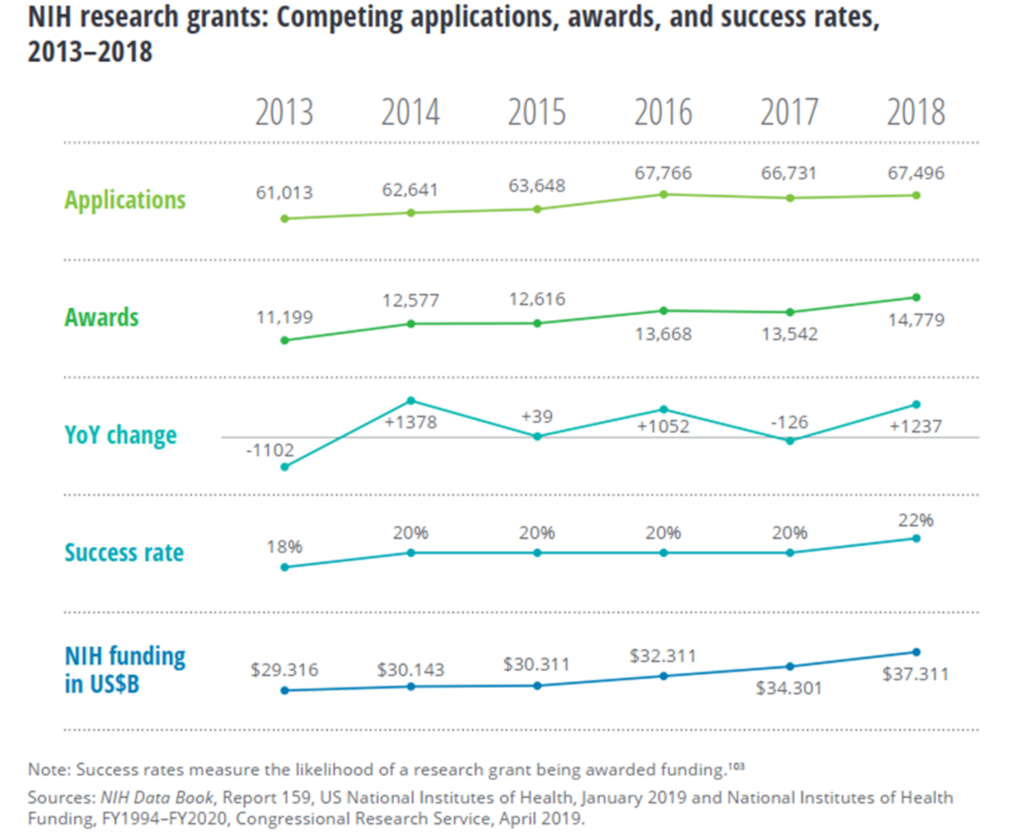

Outside funding for life science facilities comes from a combination of landlord provided capital (known as a “tenant improvement allowance” for traditional office real estate), National Institutes of Health (NIH) grants, venture capital, IPOs, and SPACS. It is worth nothing that the underwriting process for life sciences is complicated by the fact that some start-up life science tenants have no credit and no revenue in their early stages of development. Therefore, if a landlord is providing capital, it must evaluate the probability of a facility “going dark” along with the potential downside value if vacancy were to occur.[20] Despite these risks, funding is increasing across the board for life science facilities. Specifically, the funding from venture capital and NIH grants for life sciences is growing ~10% a year, according to John Cox of Alexandria Real Estate Equities, the largest owner of life sciences real estate in the nation.[21] The following charts illustrate year-over-year increases in NIH funding as well as the clusters and institutions to which this capital is being funneled.[22]

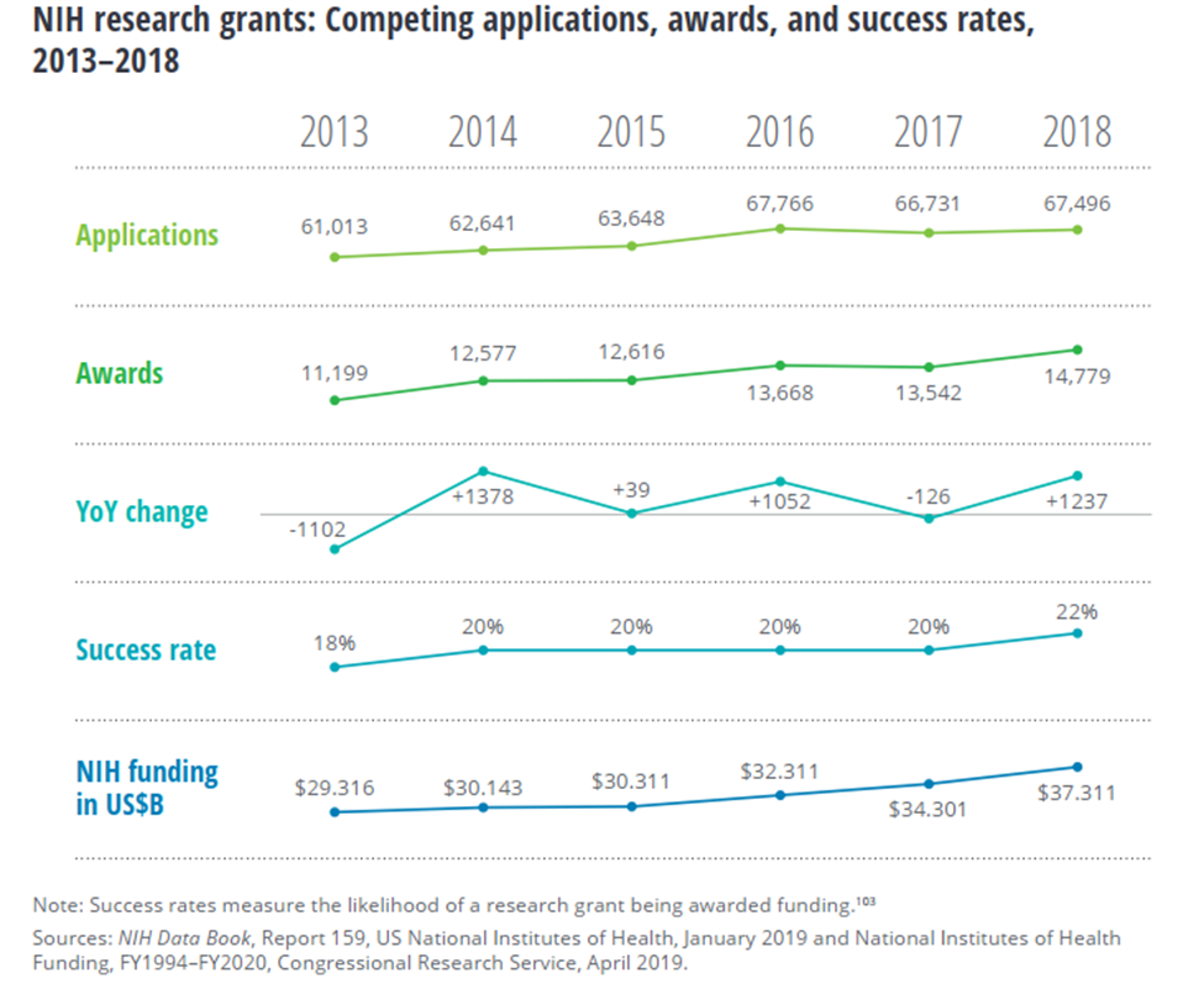

CBRE estimates the NIH funding to major universities and health-care research institutions will grow by 6% in 2020 to $42 billion.[23] One reason NIH funding is rising is that, on average, every NIH grant creates seven high-quality jobs.[24] These grants can stimulate the economy and potentially lead to significant medical breakthroughs. From 2013 to 2018, NIH received a growing number of applications and granted more money to research institutions on a year-by-year basis, according to the following graphic from Deloitte.[25]

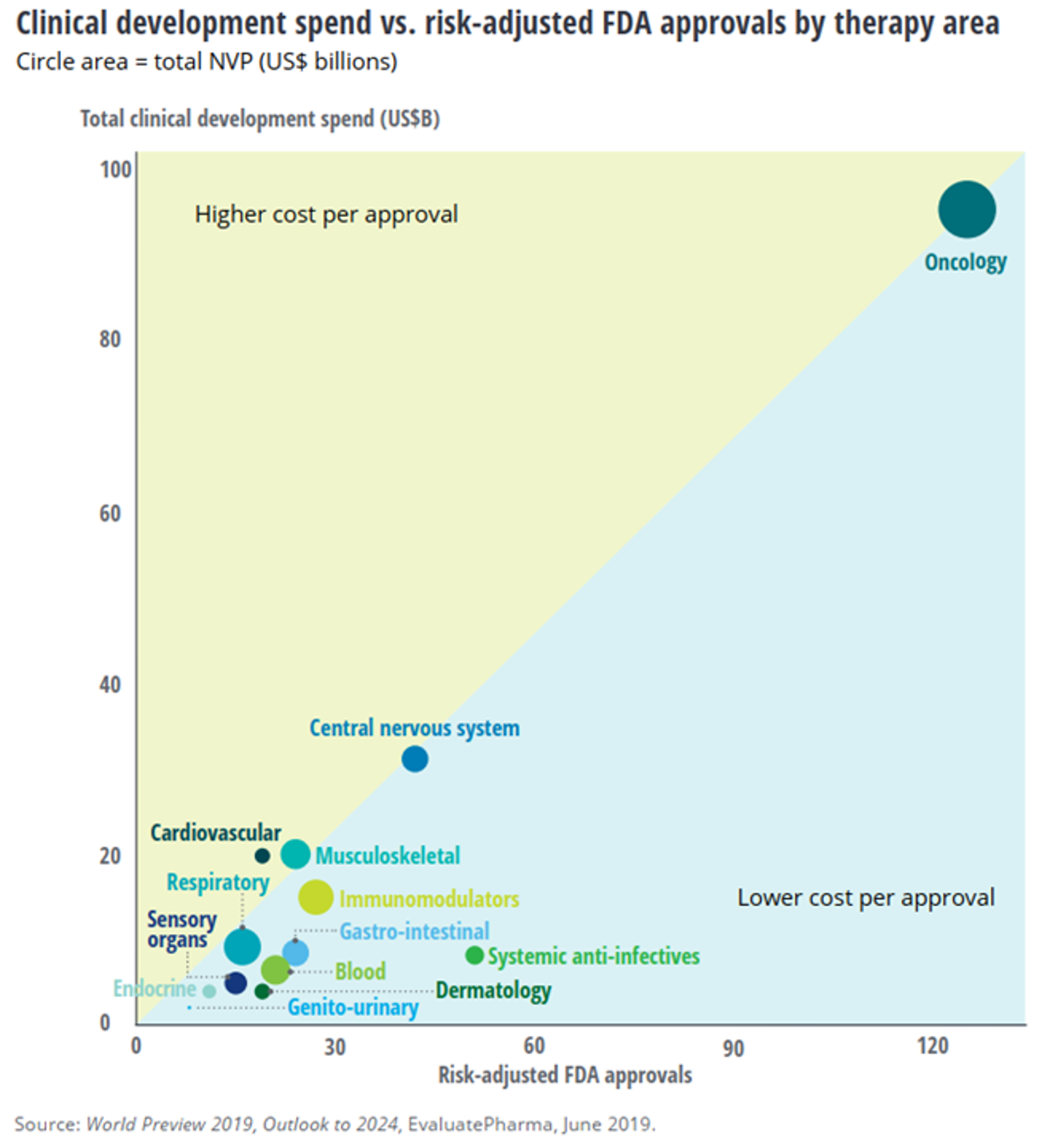

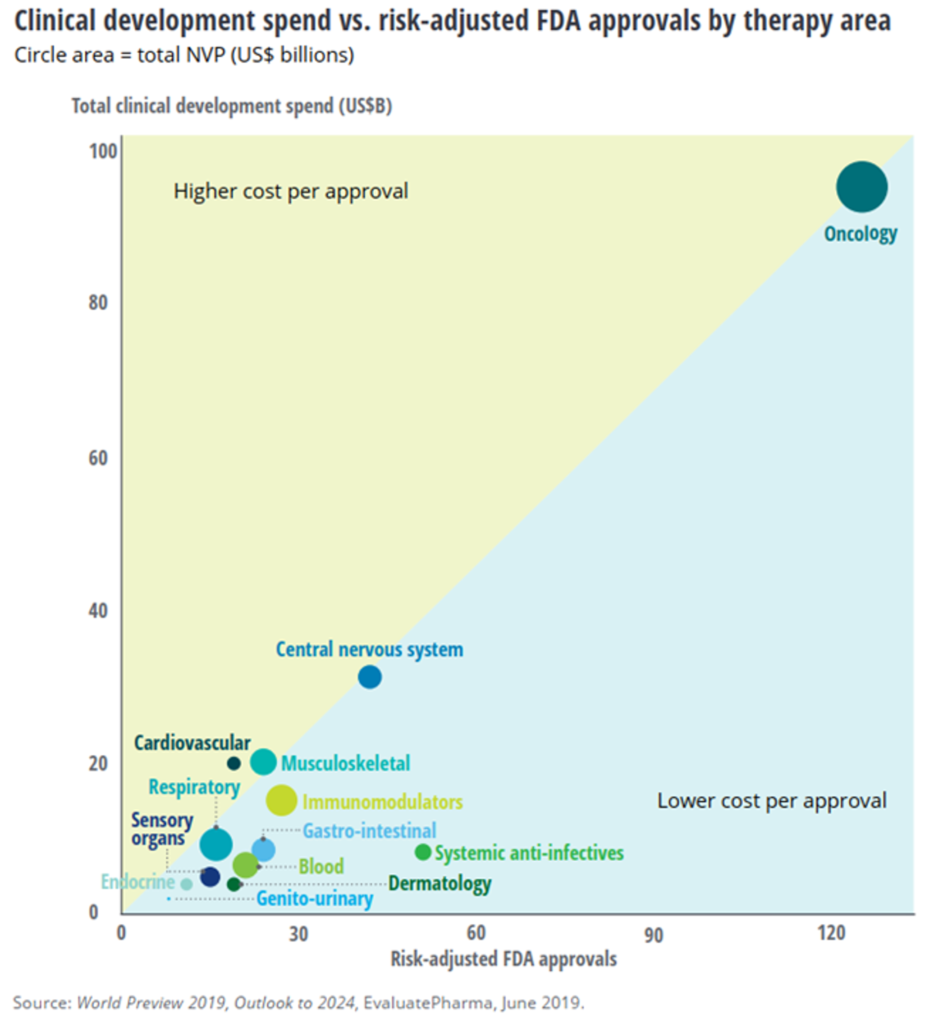

Increased funding and technological breakthroughs that lower costs make it easier for R&D to take on projects deemed too risky in the past. The following graph illustrates the level of risk and cost associated with different clinical development projects.[26]

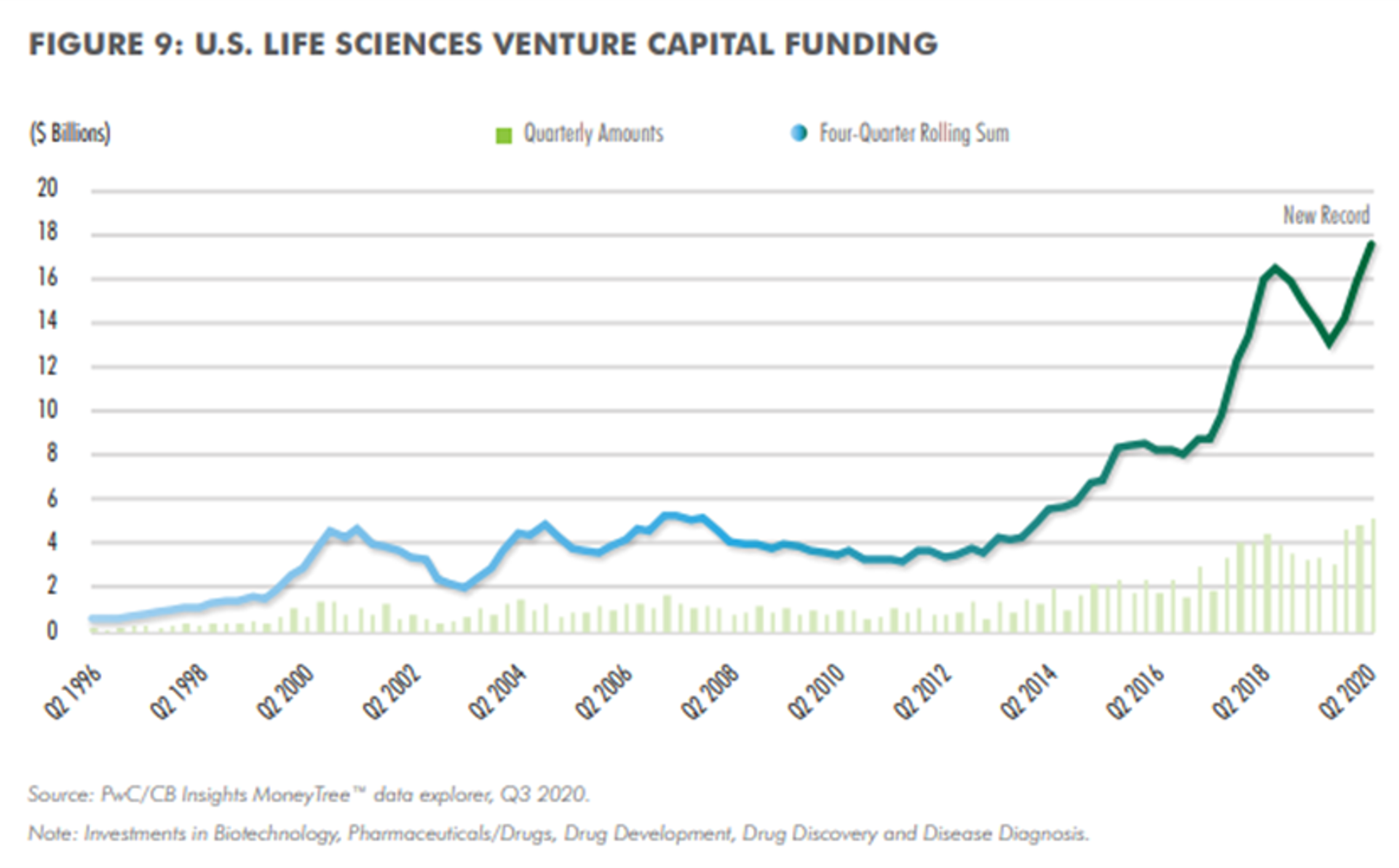

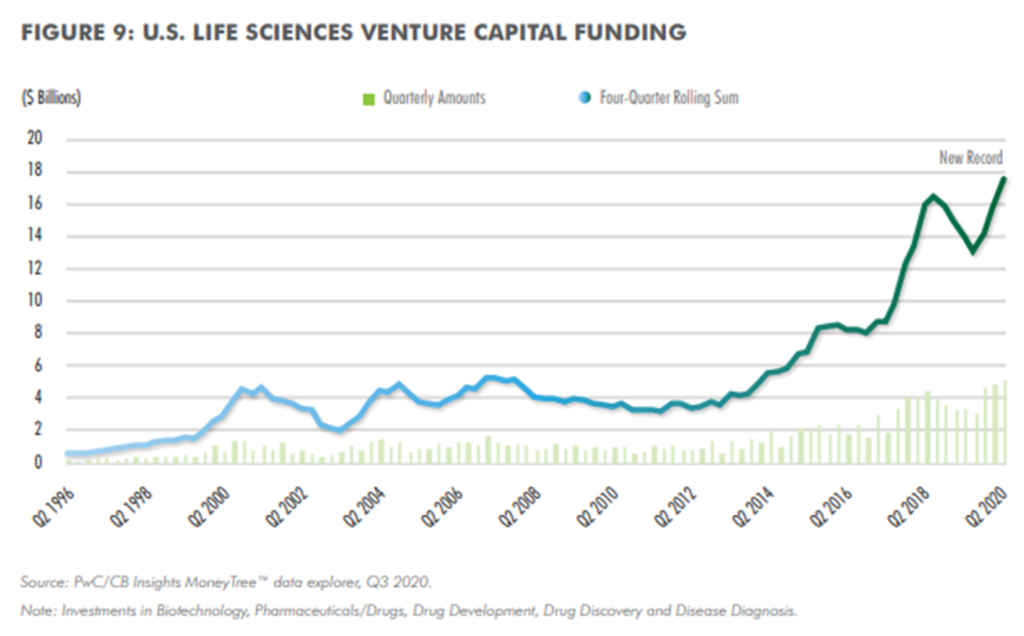

Venture capital funding for life sciences is also on the rise, signaling an increasingly bullish investor attitude towards the asset class. The following illustrates an upward trend in VC funding for the sector.[27]

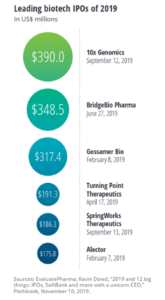

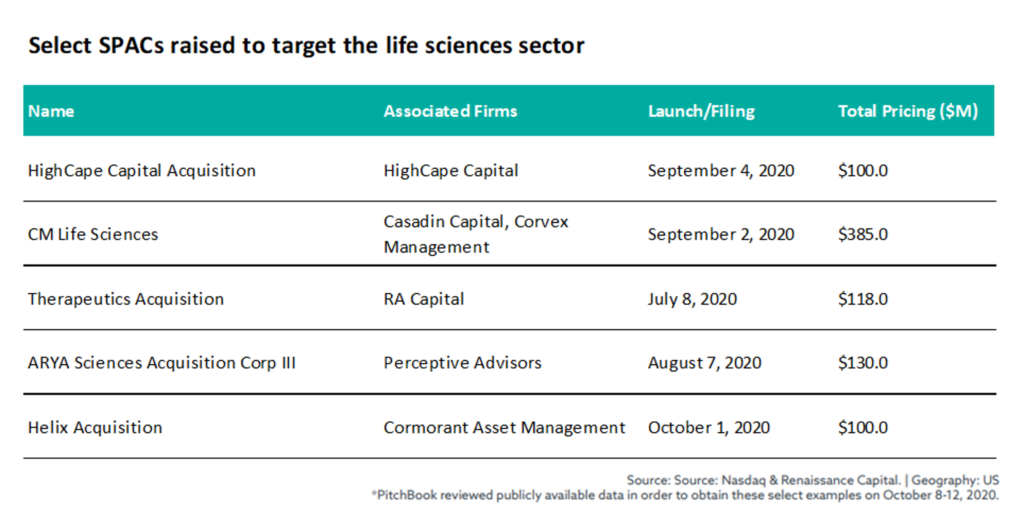

IPOs and SPACS are another source of funding when NIH and VC funding fail to acquire adequate capital for a project. The largest biotech IPOS of 2019 are outlined below.[28]

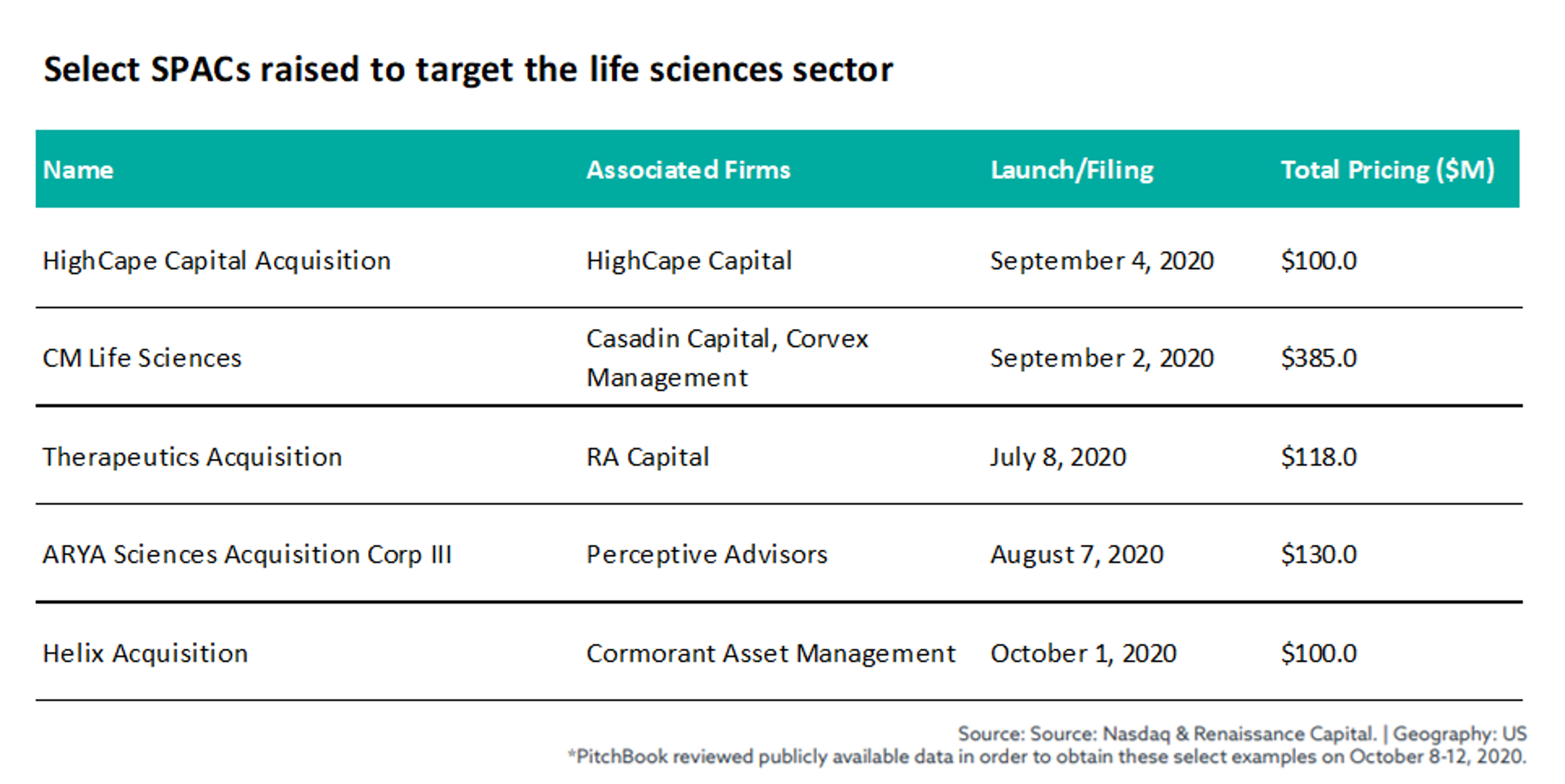

Special purpose acquisition companies (SPAC) are another vehicle for obtaining capital. There were several notable SPACs launched in 2020 to provide capital for life science deals.[29]

Key Players

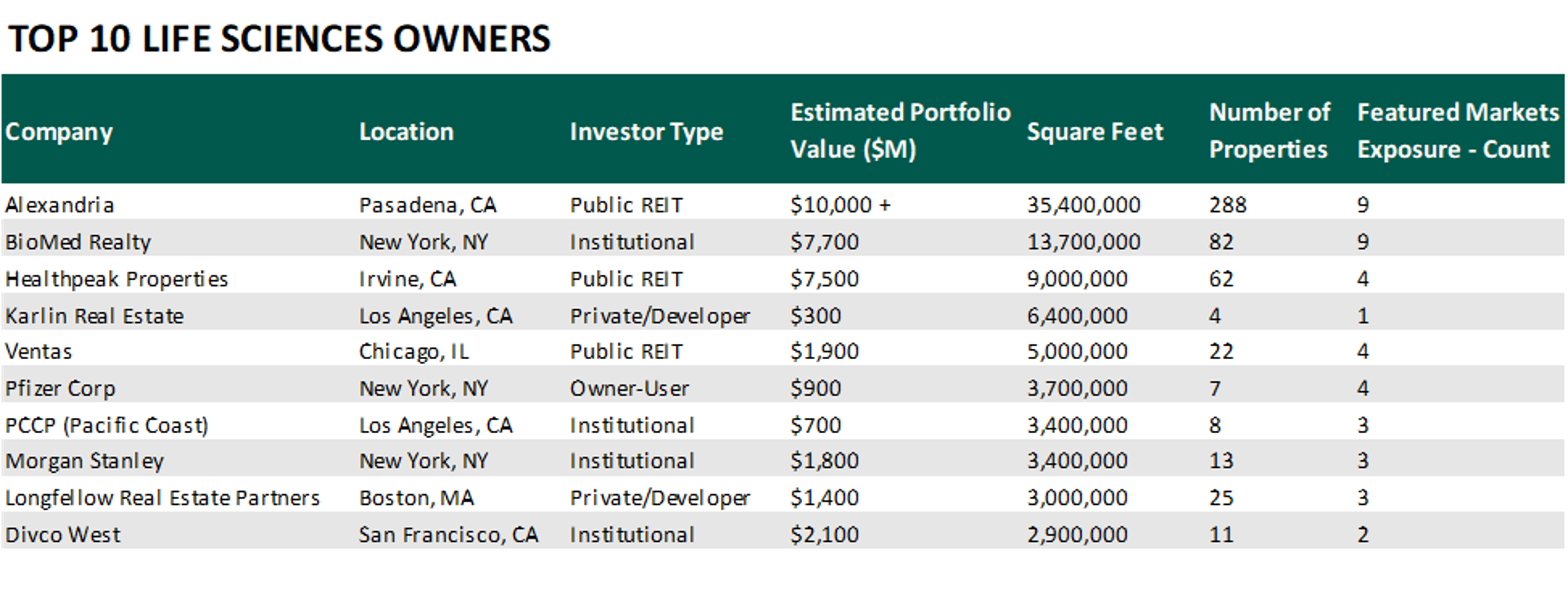

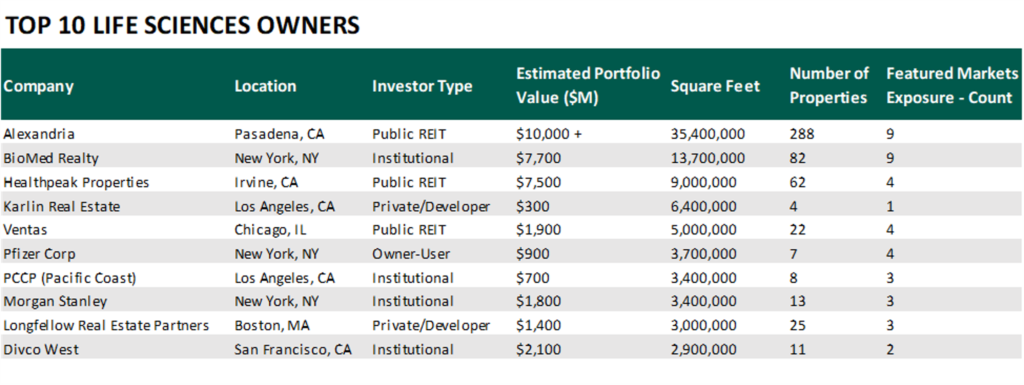

The life sciences real estate market is fairly consolidated due to the high cost of development. Newmark Knight Frank compiled a list of the industry’s top ten owners as shown below.[30]

Source: Newmark Knight Frank

Covid-19 Impacts on Market

While COVID-19 has upended most businesses and facets of daily life, it has had less of an impact on the life sciences industry. One reason is that life science tenants are able to operate as “essential” businesses and continue to occupy their spaces, although they must modify operations to maintain social distancing standards with staggered shifts and use personal protective equipment in all spaces.[31] Operations in labs (such as drug trials and development) are difficult to replicate at home, meaning office space for life sciences is not being subleased or renegotiated while tenants work remotely.[32] There has been little disruption to daily operations when compared to that of traditional offices. However, this industry is not immune to the economic headwinds resulting from COVID-19: the risk of VC funding drying up poses a significant threat to smaller, startup firms in the sector.[33]

Despite national economic volatility, the life sciences industry has fared relatively well in the face of the pandemic. Some speculate that the industry could “potentially emerge from this event in an even stronger position, while the shortfall in lab supply across the region will further encourage rapid ground-up development and office-to-lab conversions as rents reach cyclical highs.”[34] JLL expects capital markets interest to increase as life sciences proves to be a resilient investment in the current climate.[35]

Cushman & Wakefield reached a similar conclusion in a recent publication, noting that rapid technological advances and “surging demand from an aging population are creating a positive environment for life sciences growth.”[36] Cushman & Wakefield predicted increased demand for lab space and believed this upward trend in occupancy will “tend to give this sector a degree of recession resistance.”[37]

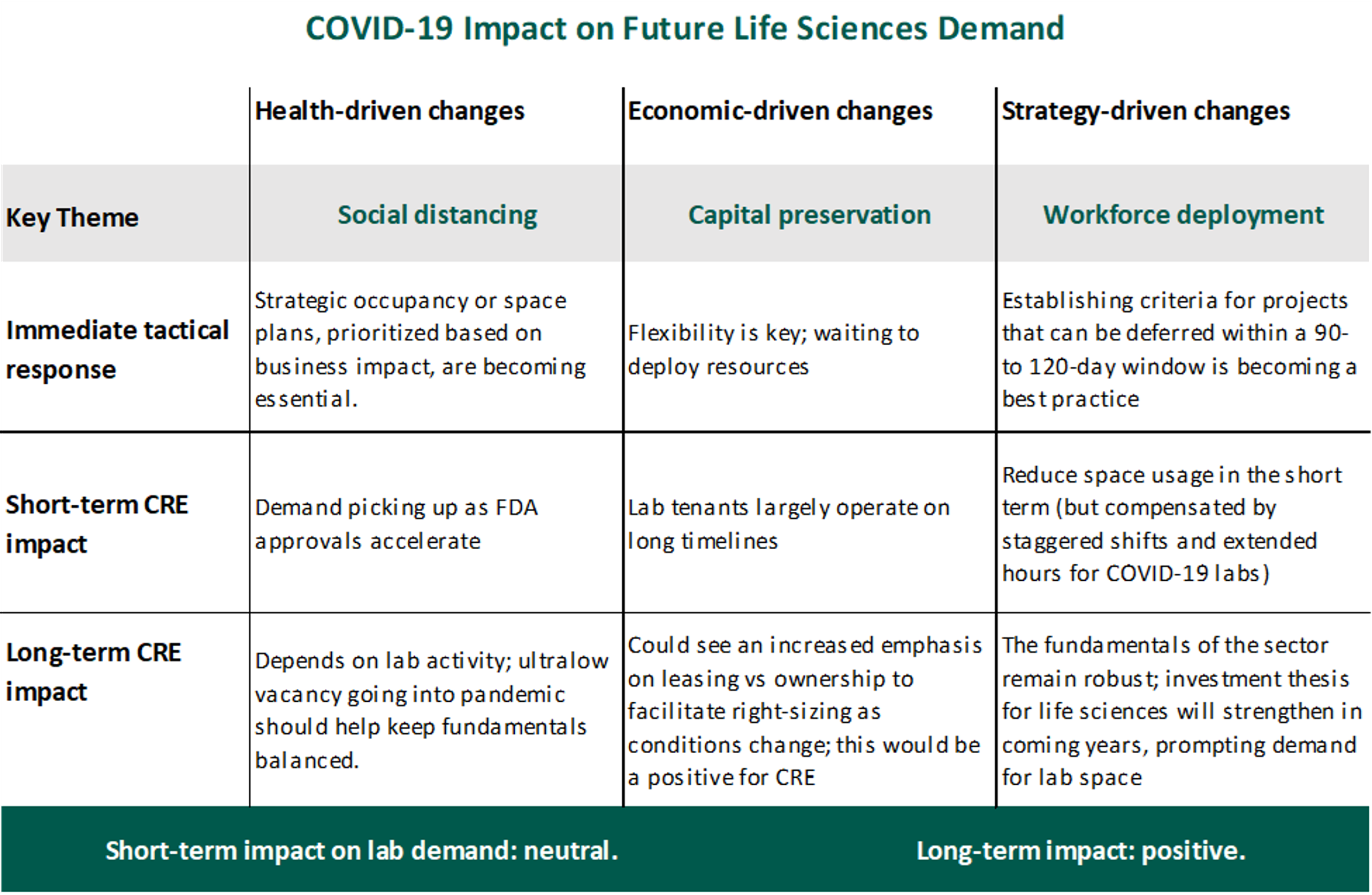

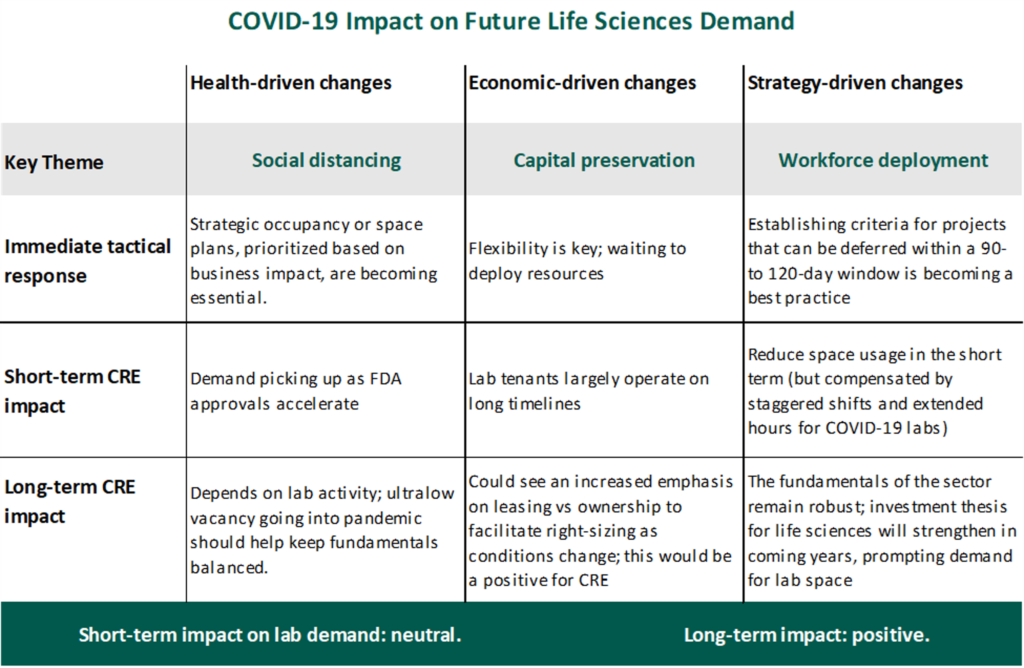

Regardless, the outbreak of COVID-19 has led to several health, economic, and social changes in the life science industry. The following graphic, sourced from JLL, illustrates short-term and long-term impacts of these changes on demand for the industry. [38]

Source: Jones Lang LaSalle

The comments of key players in the industry also suggest stability with growth potential. Alexandria and other biotech real estate holders, such as Biomed Realty and Healthpeak Properties, are not seeing the same challenges as their general-office counterparts when it comes to issues such as vacancy and rent collection during the pandemic. Collections are strong and vacancy remains low in this sector. For example, on July 28, 2020, during their Q2 earnings call transcript, Alexandria Real Estate Equities, the nation’s largest holder of biotech real estate, cited a 16.9% revenue gain. [39] Alexandria’s Co-CEO, Stephen Richardson, said the company collected 99.5% of accounts payable during Q2, and “the company leased more than 1 million square feet during the period, topping its first-quarter total.” [40] Alexandria’s overall portfolio is “94.8% leased up, and its rate of early lease renewals – a sign that companies are expecting to stay in place and not reduce space needs – was 78% during the quarter, well above the 69% it saw in earlier quarters before the pandemic.”[41]

Not only is lab space seeing demand, but government regulations are making manufacturing space more desirable for other tenants who could develop useful products during the pandemic. Manufacturers for masks and other PPE will benefit from the Defense Production Act, leading to an even greater demand for lab space during this time. Despite the pandemic-induced recession, the long-term outlook for the sector remains positive, as concluded by JLL and other industry analysts.

Underlying Market Fundamentals

The industry displays strong market fundamentals: pricing is competitive, demand is strong, the supply is growing, cap rates are compressing, rents are rising, and vacancy is low. Facilities for life sciences are unique in that they require a specialized buildout above and beyond the standard professional office space. Upgraded power and backup systems, added ventilation, lab pod designs, vivariums, the need to operate 24/7 and work in a secured environment, along with other tenant specific needs make these special use facilities. Tenant improvements can add $150 to $200 per square foot (or significantly more) on top of the base building work that the landlord provides. A vivarium alone could potentially cost over $1,000 per square foot due to the specialized systems requirements. Because of these added costs, rental rates are higher than those obtained for professional office or medical office space. Although rents vary with market, buildout, and other factors, they can range from $30 to $100 per square foot per year. Even at these rents, vacancy rates are lower than professional office indicators, with certain life science markets as low as 2%. Sale prices range widely, with lower quality, older facilities selling for under $300 per square foot, whereas highly specialized, new facilities in premium markets can command sales prices over $1,500 per square foot.

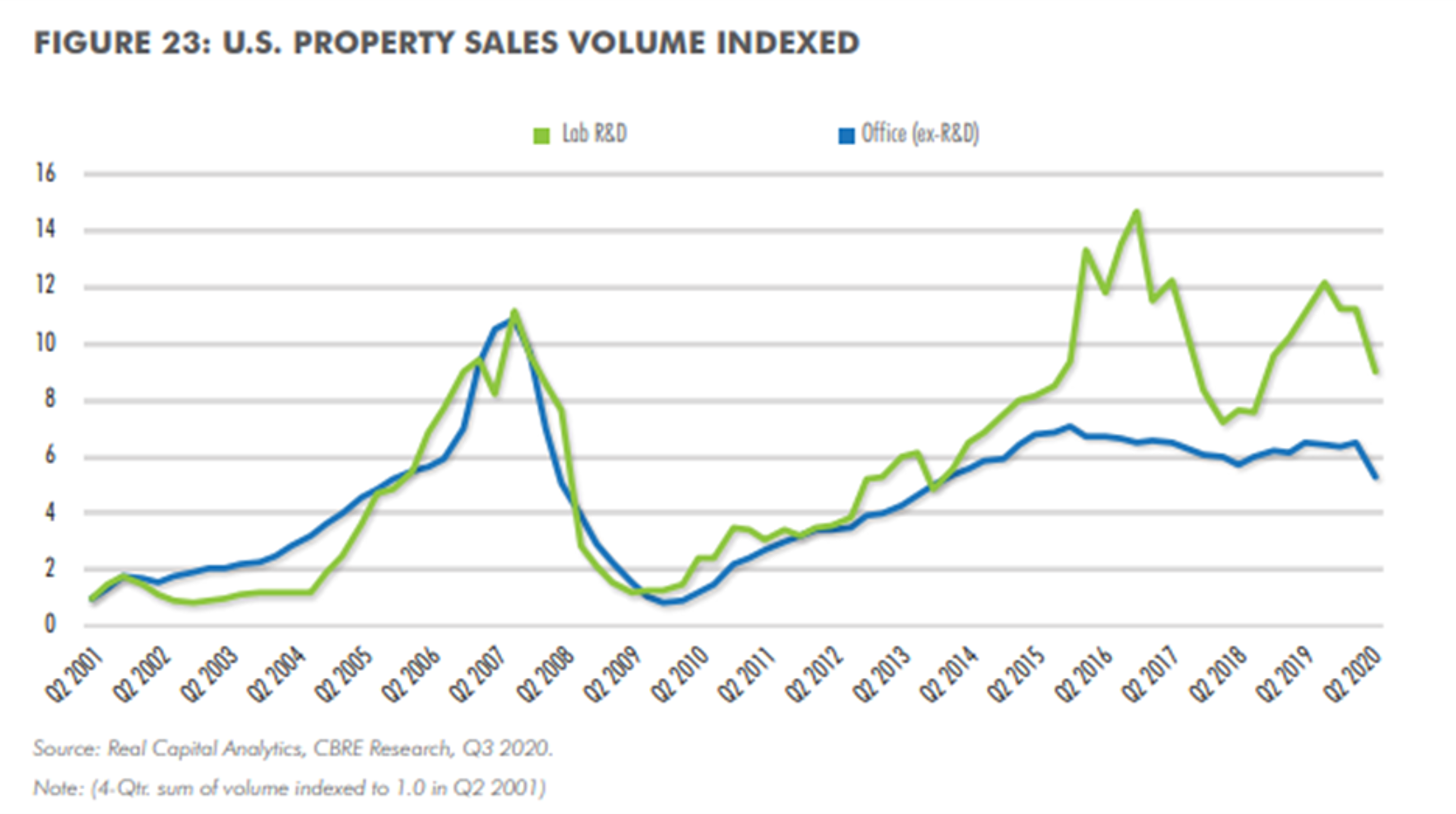

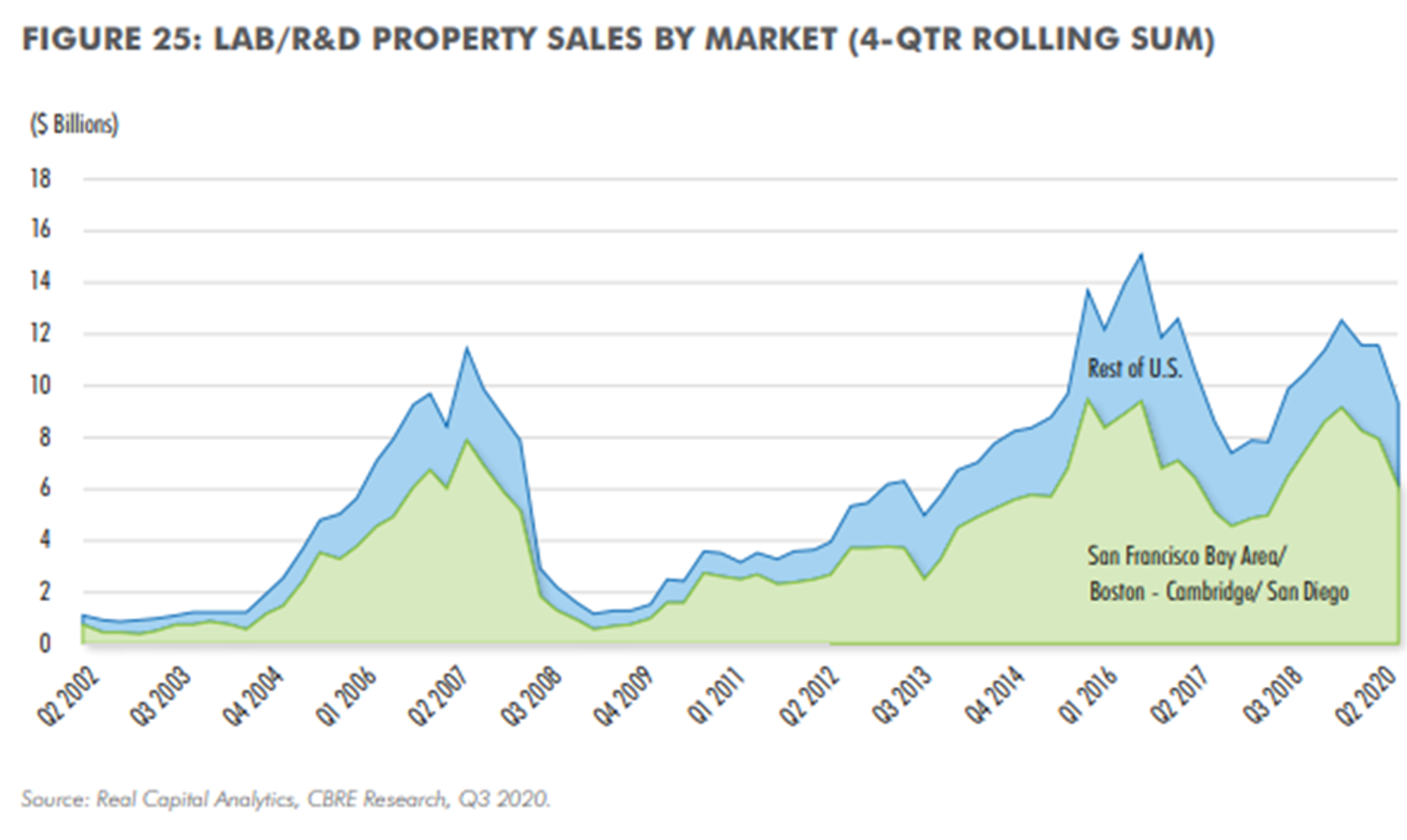

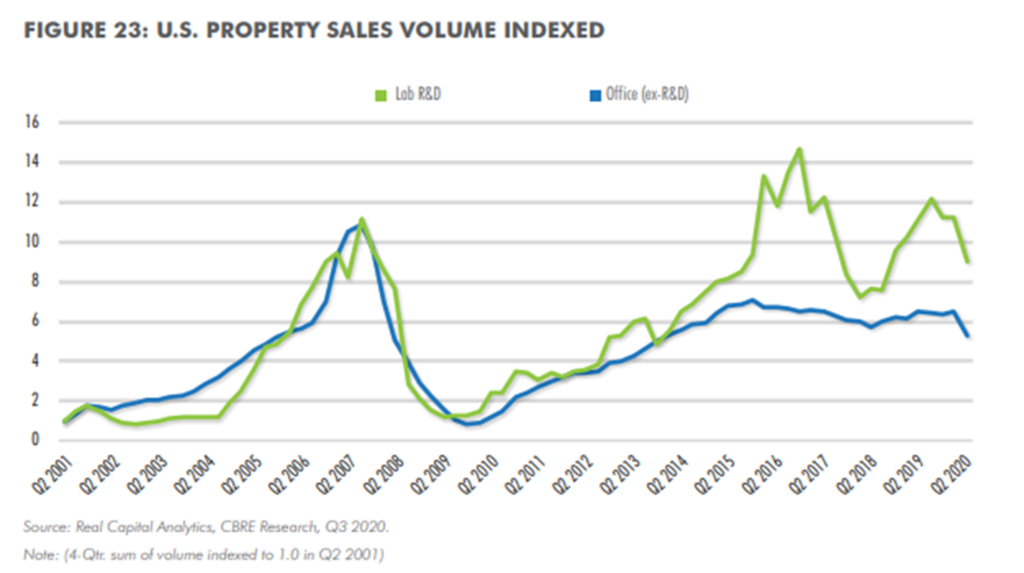

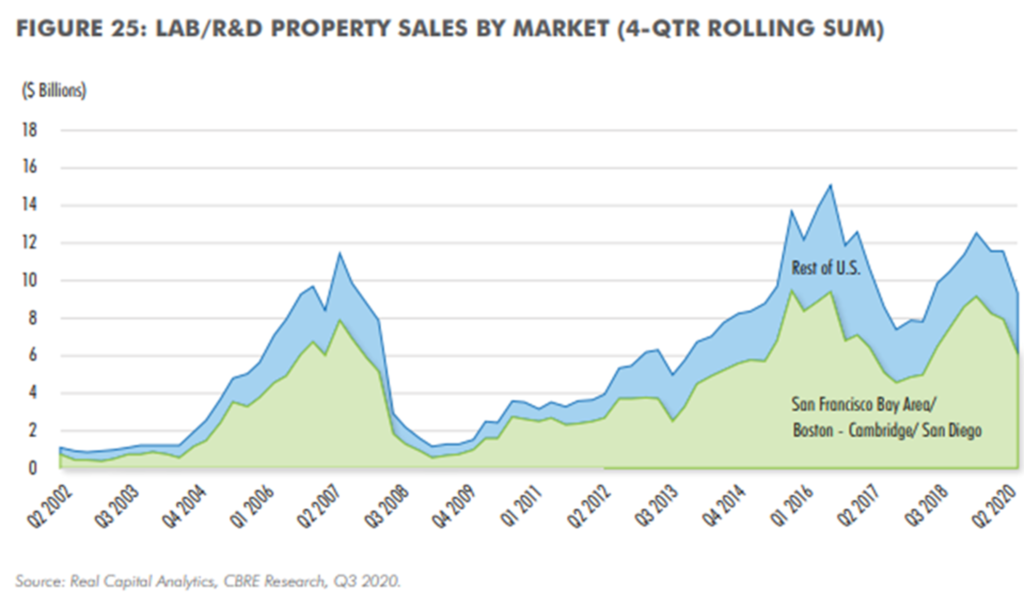

CBRE reported life science sales leading up to Q2 of 2020 to be around $9.6 billion, a 9-fold increase from 2001.[42] $9.6 billion is 18% lower than the year before, indicating that the industry may have been negatively impacted by COVID-19’s economic uncertainty, but CBRE notes pricing remains “intensely competitive” within this sector as tenant demands for space translates to a growing supply and rising rents.[43] The majority of sales took place in primary clusters (Boston-Cambridge, San Francisco, San Diego). High quality facilities in strong locations regularly command cap rates in the 4’s.

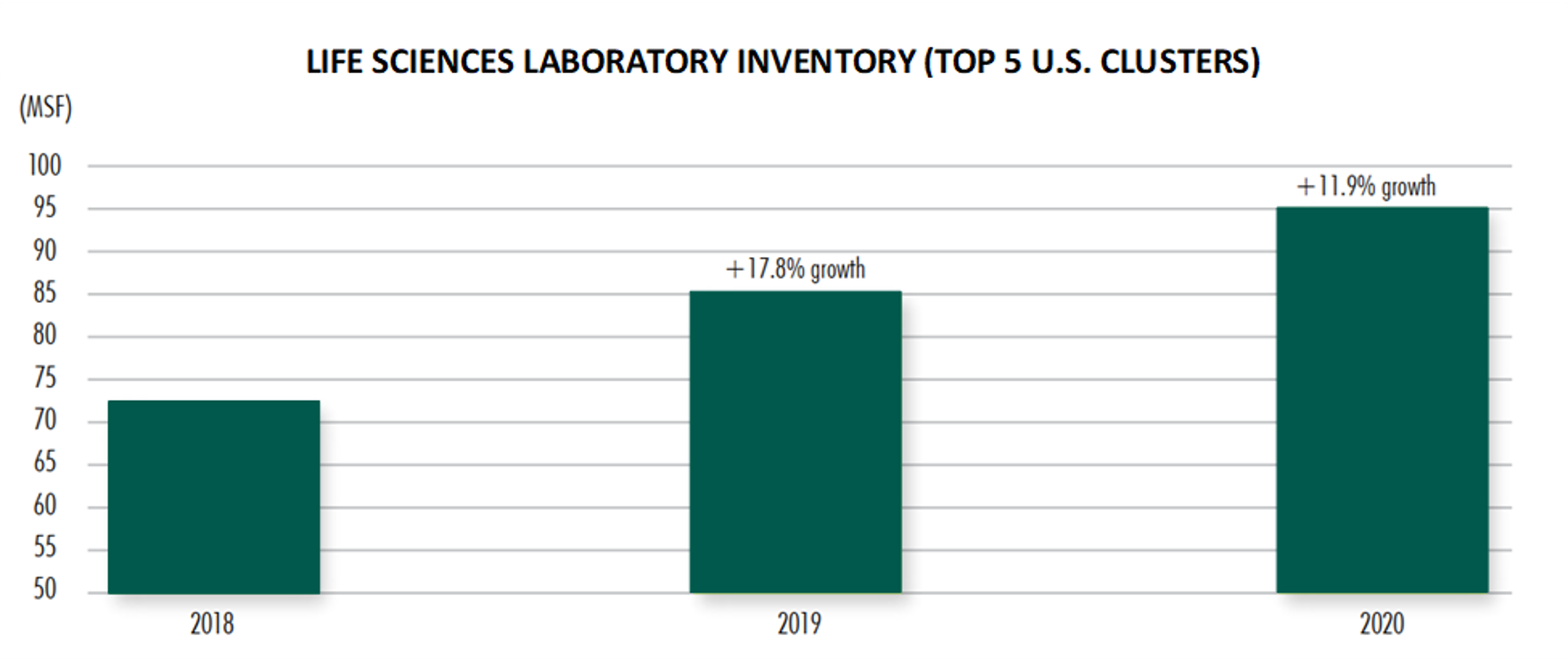

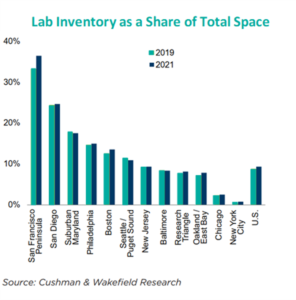

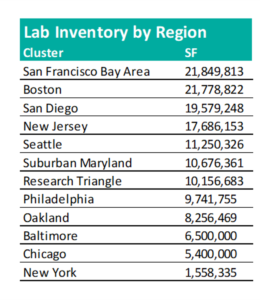

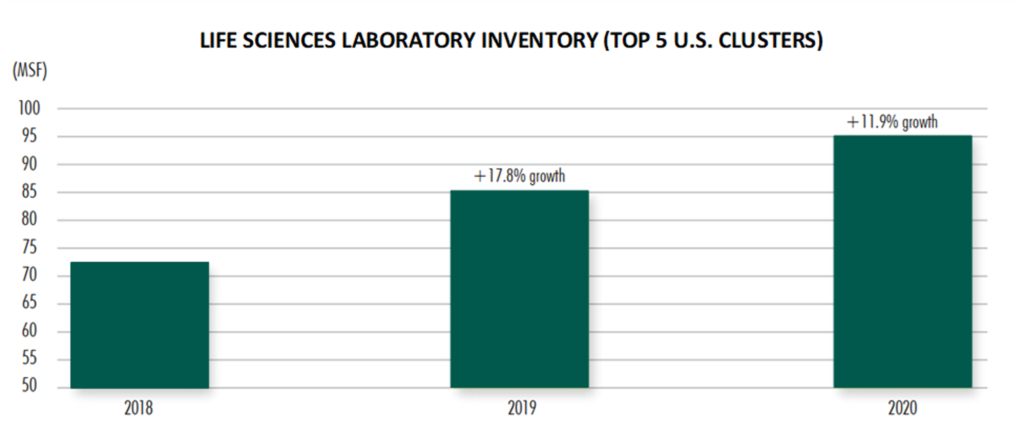

The total supply of commercial lab space in the U.S. grew by 12% in 2020, up to 95 million square feet, with an additional 11 million square feet under construction.[44] Because global supply chains have been negatively impacted by COVID-19, more life science manufacturers are moving onshore, leading to an even greater demand for domestic space.[45] The following graph illustrates the change in inventory for the industry.[46]

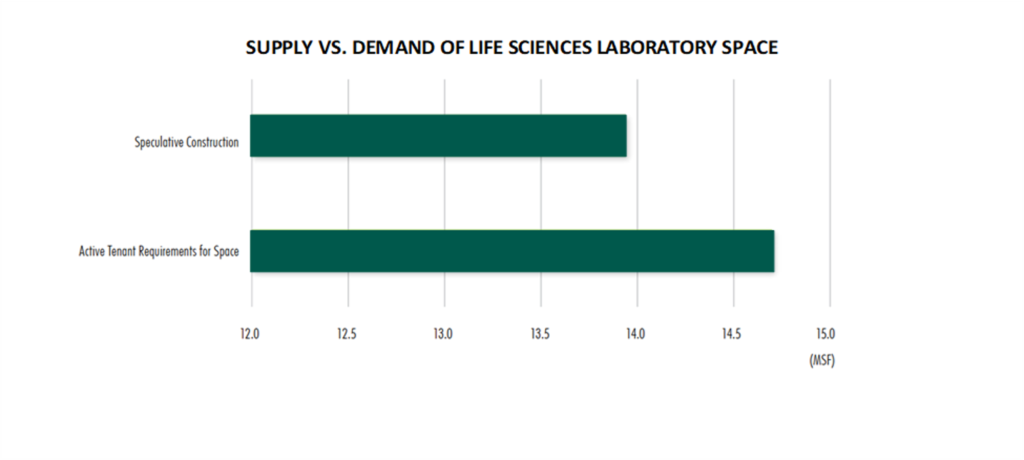

There are more tenants looking for lab space than there are lab spaces in the U.S., which is partly why the rents are high and vacancies are low in this sector.[47]

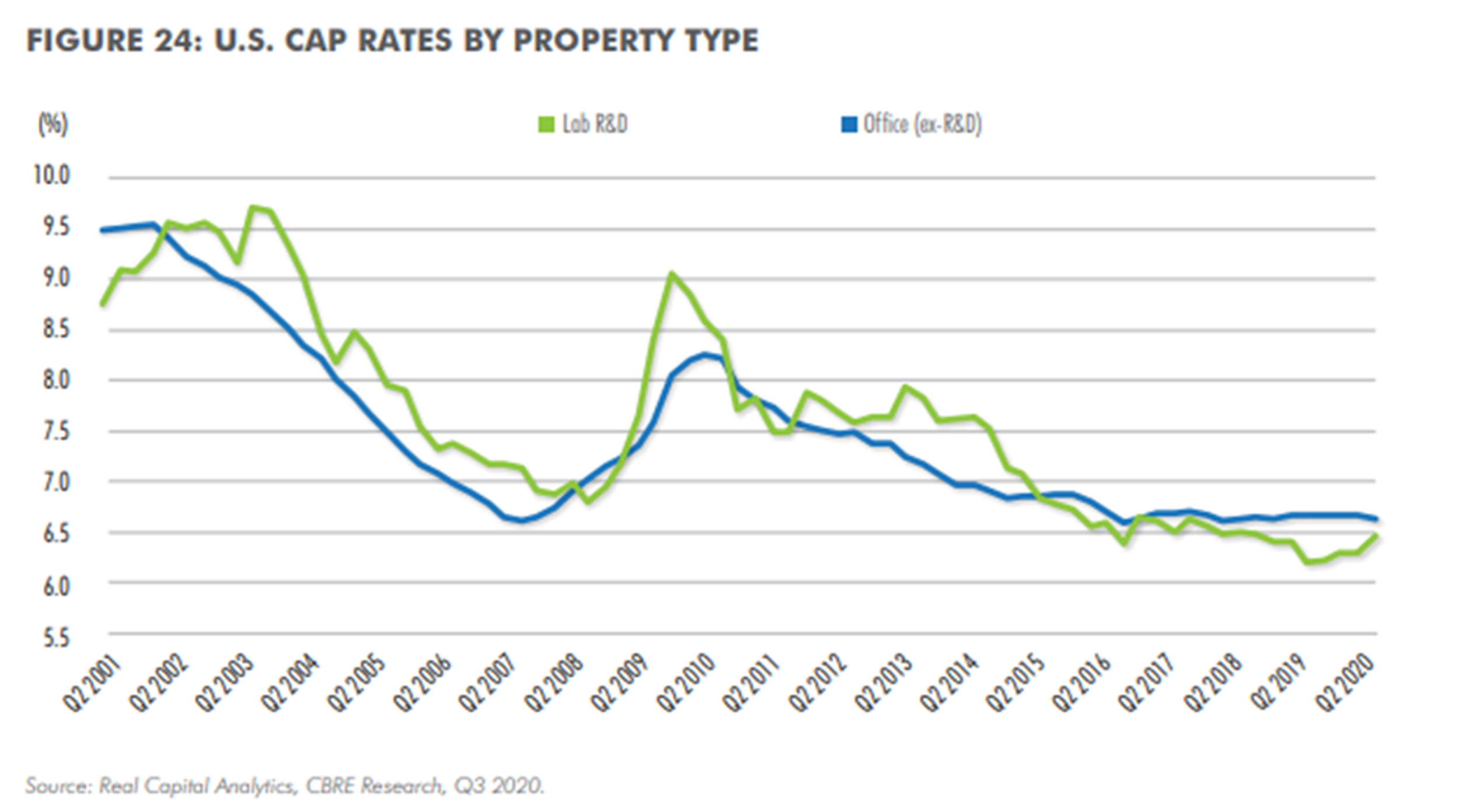

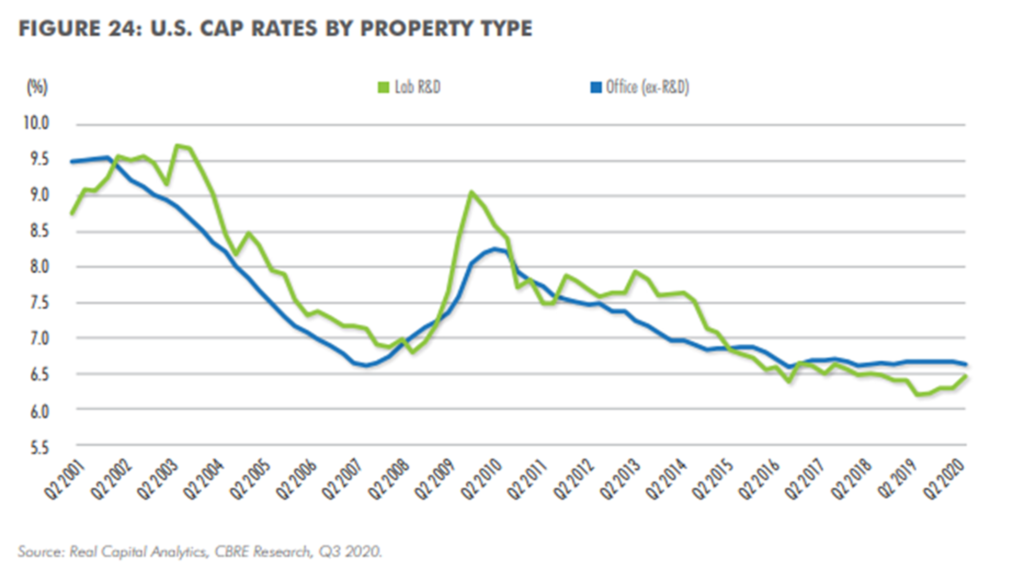

Cap rates for life sciences have been compressing over the last few years. Cap rates for life sciences have remained lower than cap rates for conventional offices since 2015.[48]

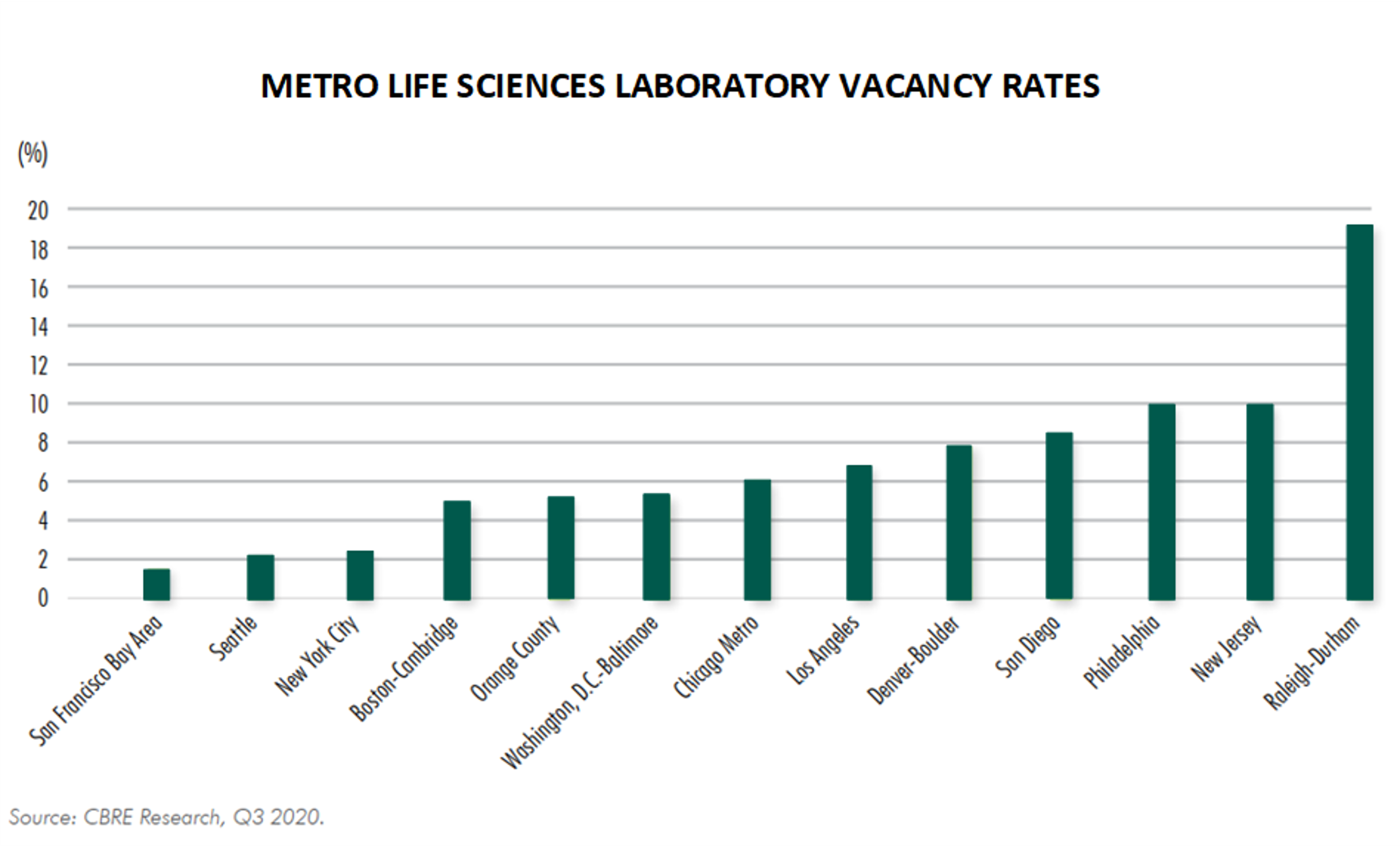

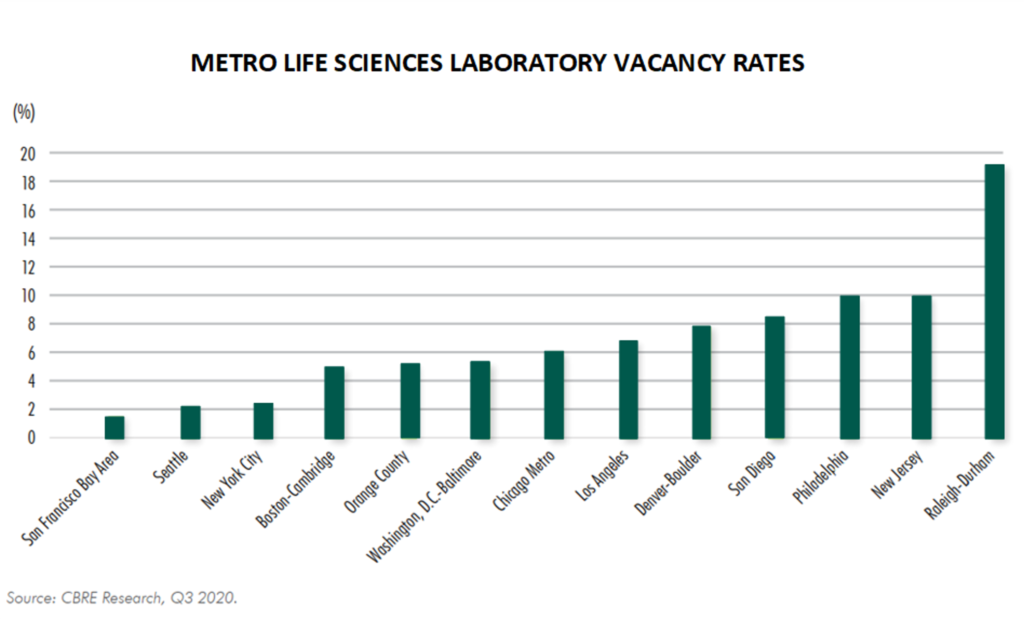

Life science labs tend to have low vacancy rates, especially within competitive, primary clusters.[49]

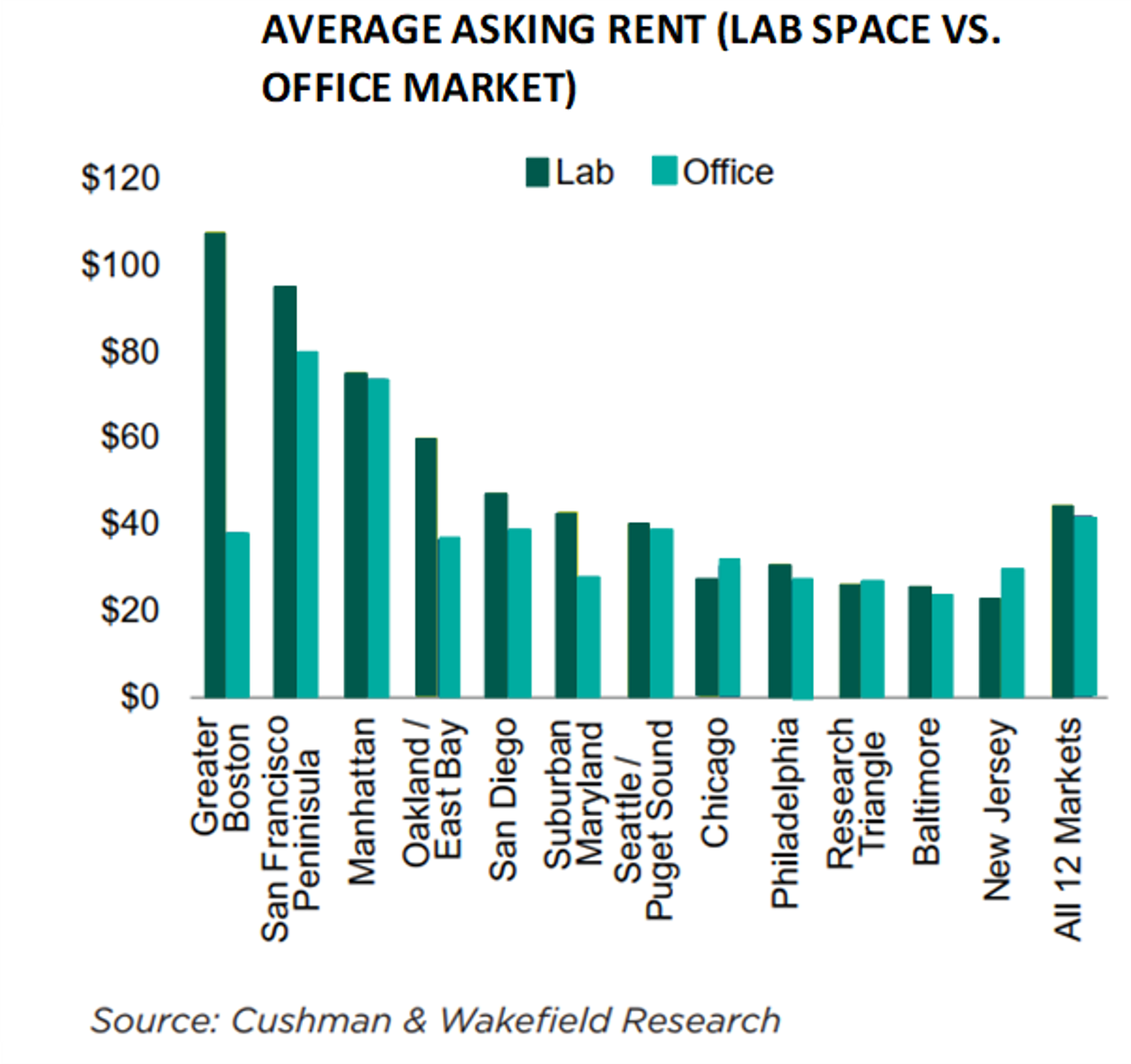

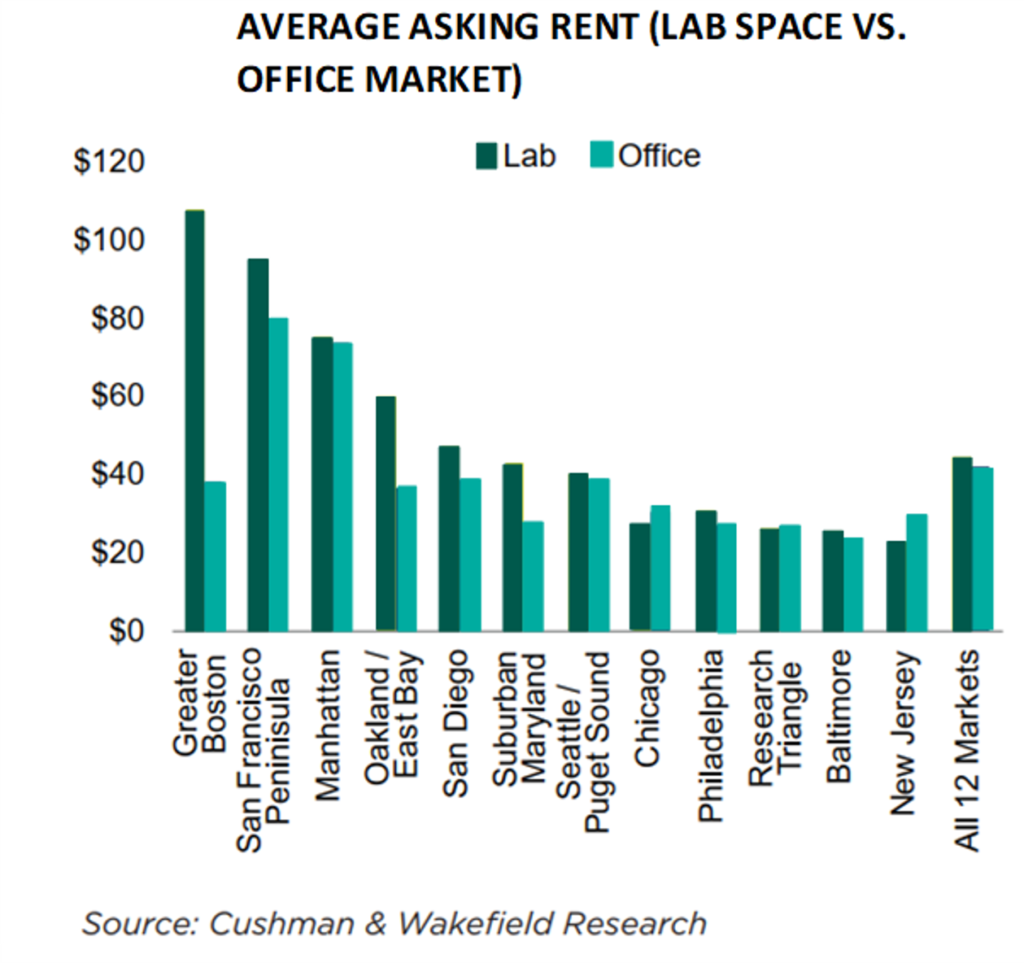

Life sciences labs also tend to have higher rents when compared to their traditional office counterparts.[50]

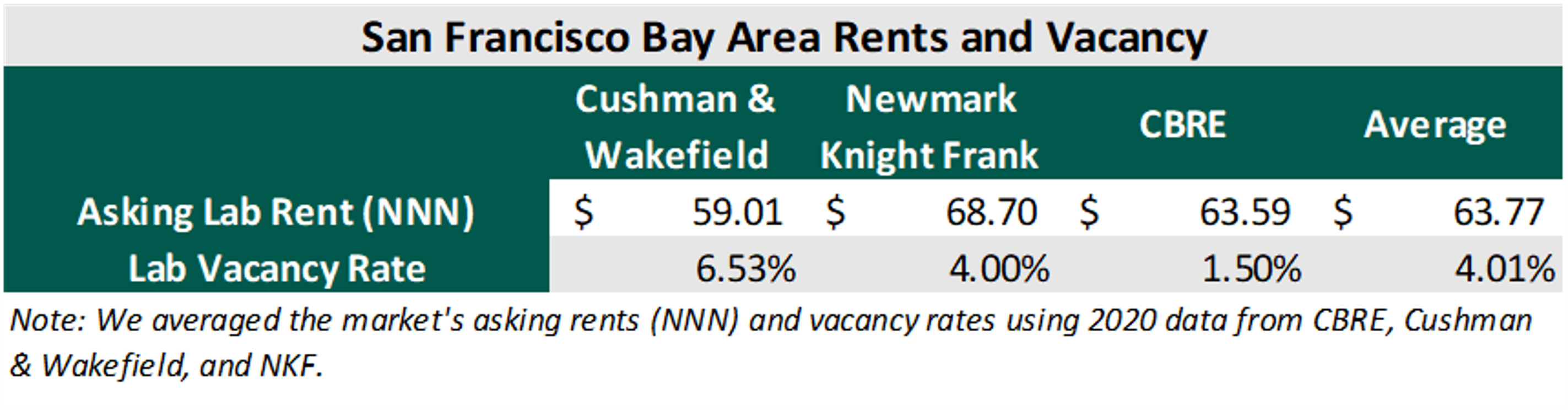

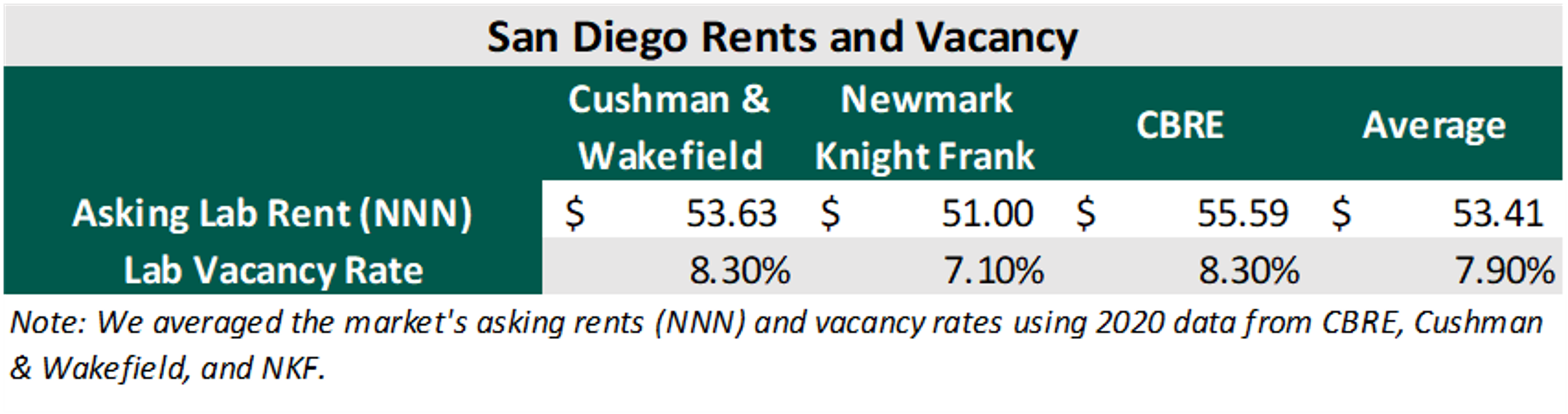

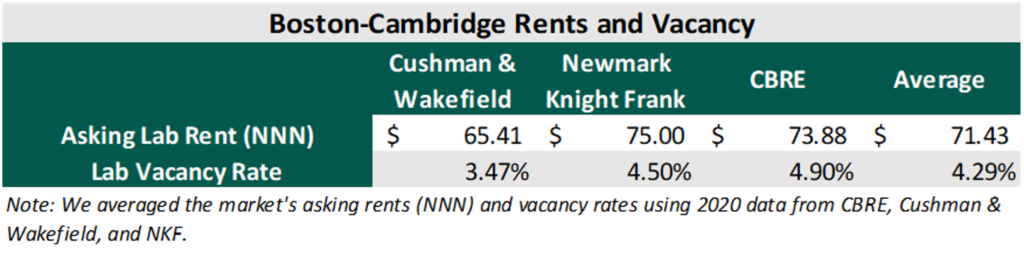

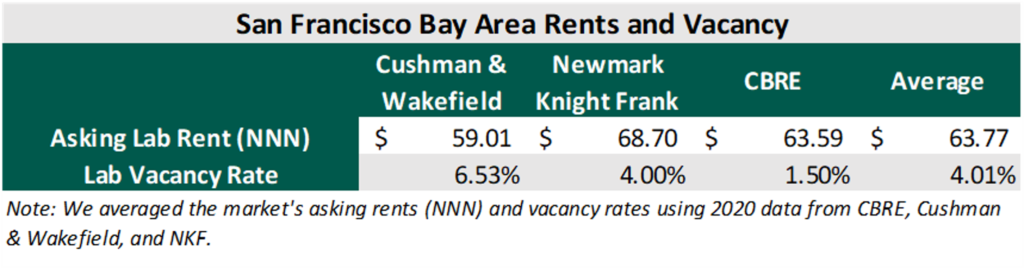

The following tables outline average asking rental rates (NNN) and vacancy rates for the top three life sciences markets: 1) Boston-Cambridge, 2) San Francisco Bay area, and 3) San Diego. Data was sourced from CBRE, Cushman & Wakefield, and NKF.

Boston-Cambridge lab market has been characterized with outsized demand, limited supply, and rising rental rates. The average TIs for this market, according to NKF, is $150-190/SF. The number of tenants seeking space in this market has increased 83% since last year. Notable new tenants include Thrive Sciences, Zymergen, Scorpion Therapeutics, and EQRX. The largest tenants in the market include Pfizer Inc, Novartis, TESARO, Sanofi, AbbVie, Thermo Fisher Scientific, and Amgen. Total employment in this market grew 7.7% from 2018 to 2019. This cluster secured $1.9B in VC funding for Q2 2020, the most since 1995. This cluster also secured $2.5B in NIH funding for 2019, the largest of any market. The majority of NIH funding in the market goes to Massachusetts General Hospital, Brigham and Women’s Hospital, and Harvard Medical School. As of Q2 2020, there is 4.3M sq. ft. of new lab space under construction. Core submarkets include Cambridge, Boston, Route 12B, and Route 495. Osborn Triangle sold in 2019 at for $1.1B ($1,625 per square foot) at a 4.3% cap rate – main tenants include Pfizer, Novartis, and Lab Central. 1030 Mass Avenue sold for $128M ($1,707 per square foot) at a 4.5% cap rate – main tenants include Astellas, Mitobridge, Obsidian TX, and Potenza TX. Top owners in the market are Alexandria, BioMed Realty, and Healthpeak Properties.

The San Francisco Bay area is a well-established life sciences cluster but has higher barriers to entry for investors because of the market’s uniqueness (significant competition for space and talent with tech companies). According to NKF, the average TIs are $150/SF over a lab ready shell. Submarkets within this cluster include Mission Bay, South San Francisco, Emeryville, San Carlos, Hayward, and Palo Alto. The top institutions in the area include Stanford, UCSF, and UC Berkeley. The largest tenants are AbbVie, Gilead Sciences, Pfizer, and Genentech/Roche. A lack of availability of lab space in San Francisco County has led to robust demand in surrounding markets. The area received $1.6B in NIH funding for 2019. For Q1 2020, the area received attracted $2.1B in VC funding, more than any other market. There is 4.2M sq. ft. of lab space under construction. Bayshore Tech Park (995,757sf) sold in 2019 as part of a portfolio sale for $323.4M at a 5.2% cap rate. 500 Forbes Blvd (155,685sf) sold in 2019 for $155M at a 4.0% cap rate. 7000 Marina Blvd (90,000sf) sold in 2019 for $77M at a 4.4% cap rate.

San Diego is a rapidly evolving cluster that is growing in popularity in part because of its access to talent and strong anchors such as Illumina and Scripps Research. Submarkets in San Diego include Torrey Pines, UTC, Sorrento Mesa, and Sorrento Valley. The highest rents are in Torrey Pines. According to NKF, the average TIs for this market are $200/SF on top of base building work delivered by landlord. The region has experienced five consecutive years of positive net absorption. New construction is estimated to be 736,000 sq. ft., which is modest compared to San Francisco and Boston-Cambridge. The area’s employment has increased 5.2% between 2018 and 2019. The market received $887M in NIH funding for 2019. The majority of NIH funding went to U.C. San Diego, Scripps, and Salk Institute for Biological Studies. San Diego attracted $796M in VC funding for Q2 2020 alone.

Conclusions and Takeaways

In conclusion, the life science industry is in a period of expansion and long-term growth prospects remain strong. Prior to the COVID-19 pandemic, life sciences real estate was a highly favorable asset in primary clusters like Boston-Cambridge, San Francisco Bay area and San Diego, achieving some of the lowest vacancy rates in the country, coupled with record high office rents. The growing demand in primary clusters has led to expansion into other areas in the country that exhibit a strong talent pool and mix of research and hospital institutions, such as the Research Triangle in Raleigh, University City in Philadelphia, New Jersey, and New York City. Similarly, Seattle and Los Angeles on the West Coast are emerging as clusters for life sciences due to the presence of tech companies, tech talent, and highly ranked STEM universities.[51] Life science employment, investment, growth, and investor awareness are at all-time highs. Tenant demand for high quality lab space remains robust in most markets nationally. Cap rates for these facilities remain low. Increased investor attention to the sector and the continued flow of capital should combine with the industry’s strong market fundamentals to fuel continued growth, both during and after COVID-19.

As investors, operators, and lenders evaluate acquisitions or new developments within the sector, proper underwriting and benchmarking is critical to evaluate risk and properly structure equity transactions or debt issuances. An FMV opinion that considers the value of the real estate in the context of a going concern, as well as in a potential “as vacant” scenario, is an important component of diligence and risk analysis. VMG’s valuation & advisory team is well-equipped to offer life sciences clients a variety of services, including quality of earnings, appraisals, operational benchmarking, and more. As the industry continues to grow and adapt to the post-pandemic economy, VMG will continue to closely monitor changes within this dynamic market sector.

Sources:

[1] Anderson, Ian et al., CBRE 2020 Life Science Report, CBRE U.S Life Sciences (October 2020).

[2] Assistant Secretary for Public Affairs., “Fact Sheet: Explaining Operation Warp Speed.” U.S. Department of Health & Human Services, November 20, 2020, https://www.hhs.gov/coronavirus/explaining-operation-warp-speed/index.html

[3] Bisconti, Greg et al., Cushman & Wakefield Life Sciences 2020: The Future is Here, Cushman & Wakefield U.S. Research Insights, Retrieved: November 30, 2020, https://www.cushmanwakefield.com/en/united-states/insights/life-science-report

[4] Id.

[5] Id.

[6] Id.

[7] World Bank, Population ages 65 and above for the United States [SPPOP65UPTOZSUSA], retrieved from FRED, Federal Reserve Bank of St. Louis; https://fred.stlouisfed.org/series/SPPOP65UPTOZSUSA, December 7, 2020.

[8] Id.

[9] Anderson, Ian et al., CBRE 2020 Life Science Report, CBRE U.S Life Sciences (October 2020).

[10] Bisconti, Greg et al., Cushman & Wakefield Life Sciences 2020: The Future is Here, Cushman & Wakefield U.S. Research Insights, Retrieved: November 30, 2020, https://www.cushmanwakefield.com/en/united-states/insights/life-science-report

[11] Id.

[12] Id.

[13] Anderson, Ian et al., CBRE 2020 Life Science Report, CBRE U.S Life Sciences (October 2020).

[14] Id.

[15] Richardson, Todd et al., CBRE 2019 Life Sciences Clusters Report, CBRE U.S. Life Sciences (February 2019)

[16] Bisconti, Greg et al., Cushman & Wakefield Life Sciences 2020: The Future is Here, Cushman & Wakefield U.S. Research Insights, Retrieved: November 30, 2020, https://www.cushmanwakefield.com/en/united-states/insights/life-science-report

[17] Id.

[18] Id.

[19] Anderson, Ian et al., CBRE 2020 Life Science Report, CBRE U.S Life Sciences (October 2020).

[20] “Life Sciences: Alan Gold, Executive Chairman of IQHQ.” Leading Voices in Real Estate with Matt Slepin, (November 2020), https://leadingvoicespodcast.com/alan-gold/

[21] Mugford, John., It’s boom time for life science real estate, Healthcare Real Estate Insights (November 2020), http://wolfmediausa.com/2020/11/24/feature-story-its-boom-time-for-life-science-real-estate/

[22] Anderson, Ian et al., CBRE 2020 Life Science Report, CBRE U.S Life Sciences (October 2020).

[23] Anderson, Ian et al., Key Insights: CBRE 2020 Life Science Report, CBRE U.S. Life Sciences (October 2020) https://www.cbre.us/research-and-reports/US-Life-Sciences-Report-2020

[24] Reh, Greg., 2020 Global Life Sciences Outlook, Deloitte Insights 2020, Retrieved: December 2, 2020, https://www2.deloitte.com/global/en/pages/life-sciences-and-healthcare/articles/global-life-sciences-sector-outlook.html

[25] Id.

[26] Id.

[27] Anderson, Ian et al., CBRE 2020 Life Science Report, CBRE U.S Life Sciences (October 2020).

[28] Reh, Greg., 2020 Global Life Sciences Outlook, Deloitte Insights 2020, Retrieved: December 2, 2020, https://www2.deloitte.com/global/en/pages/life-sciences-and-healthcare/articles/global-life-sciences-sector-outlook.html

[29] Griner, Greg et al., Orrick’s Life Sciences Snapshot: A Quarterly Report on Financing Trends in Q3 2020 – Venture Surges and the Rise of SPACS, Orrick Life Sciences Insights (October 2020). https://www.orrick.com/en/Insights/2020/10/Life-Sciences-Snapshot-A-Quarterly-Report-on-Financing-Trends-Q3-2020

[30] Kuhn, James et al., 2020 Life Sciences National Overview and Top Market Clusters, Newmark Knight Frank Research Insights (June 2020). https://www.ngkf.com/insights/thought-leadership/2020-life-sciences-national-overview-and-top-market-clusters

[31] Id.

[32] Id.

[33] Id.

[34] Symes, Audrey, and David Coffman. 2020 U.S. Life Sciences Real Estate Outlook, JLL Research (April 2020). https://www.us.jll.com/en/trends-and-insights/research/life-sciences-real-estate-outlook

[35] Id.

[36] Bisconti, Greg et al., Cushman & Wakefield Life Sciences 2020: The Future is Here, Cushman & Wakefield U.S. Research Insights, Retrieved: November 30, 2020, https://www.cushmanwakefield.com/en/united-states/insights/life-science-report

[37] Id.

[38] Symes, Audrey, and David Coffman. 2020 U.S. Life Sciences Real Estate Outlook, JLL Research (April 2020). https://www.us.jll.com/en/trends-and-insights/research/life-sciences-real-estate-outlook

[39] Alexandria Real Estate Equities Inc (ARE). Q2 2020 Earnings Call Transcript for the period ending June 30, 2020. https://www.fool.com/earnings/call-transcripts/2020/07/28/alexandria-real-estate-equities-inc-are-q2-2020-ea.aspx

[40] Id.

[41] Id.

[42] Anderson, Ian et al., Key Insights: CBRE 2020 Life Science Report, CBRE U.S. Life Sciences (October 2020) https://www.cbre.us/research-and-reports/US-Life-Sciences-Report-2020

[43] Id.

[44] Id.

[45] Anderson, Ian et al., CBRE 2020 Life Science Report, CBRE U.S Life Sciences (October 2020).

[46] Id.

[47] Id.

[48] Id.

[49] Id.

[50] Bisconti, Greg et al., Cushman & Wakefield Life Sciences 2020: The Future is Here, Cushman & Wakefield U.S. Research Insights, Retrieved: November 30, 2020, https://www.cushmanwakefield.com/en/united-states/insights/life-science-report

[51] Kuhn, James et al., 2020 Life Sciences National Overview and Top Market Clusters, Newmark Knight Frank Research Insights (June 2020). https://www.ngkf.com/insights/thought-leadership/2020-life-sciences-national-overview-and-top-market-clusters