GenesisCare Bankruptcy Emergence

Christa Shephard

June 11, 2024

Written by Quinn Murray and Ed McGrath, MHA

In the Fall of 2022, we wrote an article discussing not-for-profit health (NFP) system financial performance trends. At the time, NFP systems were experiencing major financial struggles given labor market and supply chain issues coupled with other inflation and industry pressures. While not the primary focus of our 2022 study, VMG Health also raised a concern relative to mid-size hospitals (larger than critical access, but not large enough to provide tertiary/quaternary care). Unfortunately, the concern has proven to be valid as hospital closures and bankruptcies continue. The outlook for these mid-size, independent hospital organizations is not promising given the lack of financial flexibility as larger systems continue the pursuit of acquiring any independent hospitals that have demonstrated any degree of financial success. In 2022, we also noted systems would experience increased competition by private equity–funded niche players and other organizations that could shift profitable services and commercial business from the systems. Their increased presence as disruptors in new markets has accelerated quicker than originally anticipated.

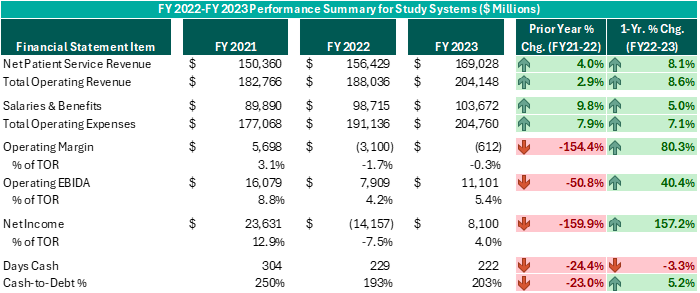

Our 2022 article summarized the financial performance of 21 systems across 32 states, with a combined fiscal year (FY) 2022 operating revenue of $188 billion. As noted in the prior article, the study was not intended to represent a statistically valid sample across all NFP systems, but did include a cross section of systems that provide care to patients in over 30 states with net revenues greater than $2 billion. Of these 21 systems, approximately 15 percent are clients of the VMG Health authors, but the vast majority are not.

Our updated article assesses how those same 21 systems performed in FY 2023 as compared to FY 2022 levels. As a result of this study, our team discovered the importance of understanding the broader implications resulting from the unfavorable financial performance of NFP health systems. This report also discusses the actions our clients and other NFP systems are taking to address the existing financial pressures and to proactively address potential future issues.

Executive leadership in these systems have made commendable decisions over the past 12–18 months despite ongoing challenges. While operating margins on a combined basis have improved by $2.5 billion from FY 2022 (and combined operating EBIDA improved over $3 billion), these organizations still experienced combined operating losses of ($612 million) in FY 2023. However, while positively trending toward break-even operating margins and 5% or higher operating EBIDA margins is no small feat following the adversity endured nationwide during FY 2022, these levels do not support long-term sustainability. Healthcare systems seeking sustainable financial operations should target operating margins of 3% or higher and operating EBIDA margins of 10% or higher. Those targets may not be achievable for all NFP Health Systems, but consecutive years of operating losses and minimal cash flows are not conducive for strategic growth and reduces an organization’s flexibility to certain strategic investments.

While the performance turnaround noted above is remarkable, the future of NFP healthcare systems continues to be very challenging. Organizations are seeking avenues to develop accretive opportunities to thrive—not just survive. Survival should not be the long-term objective. Systems are exploring and utilizing a variety of options and resources to improve performance, some of which have come to fruition in the past 12–18 months, as evidenced by the financial summary above.

Avenues some of our client system executives have pursued include the following. Note, each market and each situation is unique: One can apply similar approaches, but there is no cookie-cutter or templated solution. Rather, adjust the model to fit the situation as opposed to forcing the situation to fit the model.

To achieve long-term financial success, NFP systems should consider more innovative strategies that complement the evolving healthcare landscape. Patient preferences are not the same as they were 20 years ago, nor is the manner in which healthcare providers deliver care. Competitors and other organizations will capitalize on those who remain complacent and do not adapt. Therefore, sustainable success will require a willingness to adapt to the current industry environment in addition to proactive planning to meet the anticipated future needs of the patients and communities served.

Written by Sydney Richards, CVA; Erica Veri

The value a brand brings to a strategic partnership is overlooked in many healthcare joint ventures and affiliations. However, healthcare brands may have a significant impact on a partnership’s success. Healthcare brands can suggest top outcomes to communities in the face of intense competition, attract and retain leading providers, and evoke a sense of loyalty and trust among the patient base. In many joint ventures and partnerships, completing a brand valuation allows the licensor to receive a financial return for their contribution of this important asset. Below, we outlined important factors that may be considered in a brand valuation.

Healthcare brands are commonly contributed to a partnership through a license agreement. The structure and terms of the brand licensure can significantly influence the value. For example, a brand license agreement may stipulate payment terms, which can be structured as an upfront equity in a partnership, a fixed annual payment, or a variable (royalty rate) payment. These terms can have a significant impact on how financial risk is or is not shared between the parties, especially for partnerships such as de novo joint ventures. The license agreement can also specify the duration of the brand contribution and specify whether the rights to the brand are exclusive to the proposed licensee or whether the licensor may enter other brand contributions simultaneously.

From the licensor’s perspective, extending the use of their brand to a partner can offer an opportunity to access a larger patient population without sizable investment in capital and infrastructure. A licensor also gains the opportunity to monetize the positive reputation associated with its brand, which has often been built over significant time, investment in expertise and care quality, and marketing spend. While these historical costs may be difficult to quantify, the quality and strength of the brand, especially as compared to peers, can and should be considered in a brand valuation.

One of the ways the brand strength, recognition, and positioning can be considered in the appraisal is through a “with and without” analysis, which seeks to quantify how forecasted earnings would differ for an opportunity with vs. without using the brand. These earnings can be impacted by items such as speed to ramp up for partnered de novo ventures, increased occupancy or utilization due to the community’s association of the brand with high quality care, margin effects of greater economies of scale, or even a favorable payer mix shift.

Additionally, other benefits may be captured in the with and without analysis, including access to clinical integration, clinical trials and research, facilities and equipment planning, and recruiting. If the licensee is a smaller entity with less market share than the licensor, it may desire to leverage the branding entity’s experience and knowledge of best practices while conveying the expertise and reliability of the larger brand to the patient population.

The cost to replicate considers what it may cost to develop and maintain a comparable brand. While many retail brands communicate price and prestige, healthcare brands typically emphasize a company’s quality patient service, positive outcomes, and reliability. A healthcare brand can also attract physicians and help in retaining talent. These qualities may take years, even decades, to develop. While there are certain quantifiable measures that can be included in a brand appraisal, such as advertising and marketing spend to build and maintain a brand, it can be difficult to measure the true costs to replicate brand value for many healthcare brands. Additionally, unless the licensee can generate a return on these costs, it would not be reasonable to assume they would be willing to pay for all historical costs unrelated to a particular licensing arrangement. As a result, this approach is commonly considered but may not directly drive a value indication for the specific payment a licensee should make for the use of the brand.

A licensee’s financial performance may have a material impact on the amount it can expect to pay in a licensing arrangement. Factors such as business stage (start up, growth, or mature), subindustry, margin, and operational capacity or constraints can directly impact the ability of a brand to drive incremental earnings to the licensee through use of the brand. A brand valuation for a license payment between two entities commonly includes a thorough examination of the licensee’s position in the local and greater market, performance compared to peers, and outlook.

There are numerous market sources for brand valuation comparables. While commonly considered and thoroughly analyzed, due to the uniqueness of each licensing opportunity, many lack direct comparability to the royalty rates published in publicly available databases, such as MARKABLES, ktMINE, and Scope Research. To the extent that there are brand comparables, a brand valuation should consider reasonable market ranges for similar assets and transactions.

Compared to many healthcare business or other asset valuations, healthcare brand valuations can be difficult. There can be uncertainty (and differences of opinion) on the go-forward impact a brand may have on a business. Although there are established general market ranges within healthcare segments, there are less direct market comparables compared to other partnership contributions, such as business equity or real estate value, for brands. With VMG Health on your team, you can expect the quality, responsiveness, and expertise your brand deserves to overcome these hurdles and drive a successful brand contribution and lasting partnership.

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

My portion of the presentation was about the valuation of academic healthcare brands. I talked through different valuation methodologies, which are the income cost and market approach, by discussing the specifics related to brand valuation. Additionally, I spoke about the key things to consider in a brand valuation or in a transaction involving a brand, like how to structure the payment—whether it’s through a variable or fixed license rate—and some of the pros and cons to different affiliation structures.

In academic brand valuations, the owners of the academic brands tend to think their brand is extremely valuable. However, from an actual fair market value transaction perspective, the value of that brand is based on the licensee’s return, even if the brand is powerful and may drive allocations higher. If the licensee can’t make a monetary return on it, there won’t be a huge value that they have to pay. Otherwise, they’d be negative.

Leaders can look for opportunities with this knowledge. Brands are not a common part of a joint venture arrangement. Adding a health system’s brand to a joint venture may result in an additional return or credit for something that the system is contributing to the joint venture. Historically, leaders may not have valued brands, but they can.

The blog, Healthcare Brand Valuation: Purpose, Strategy, and FMV Implications, is a great supplemental resource for those looking to learn more about incorporating brand in healthcare transactions. Additionally, another article is coming to the VMG Health website soon, and it will focus on brand valuation. Watch our site for that upcoming content.

Brands can and should be considered, and possibly included, in healthcare transactions.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.