Five Key Analyses for Healthcare Financial Due Diligence

Christa Shephard

May 20, 2024

Written by Johnny Zizzi, CPA; Lukas Recio, CPA

When considering a new acquisition or transaction, accurate financial reporting is paramount for informed decision making. One significant aspect of financial reporting is the choice of accounting method: cash, accrual, or a hybrid of both. Many companies begin their journey with cash accounting, but as they grow and evolve or are otherwise acquired by a larger entity, they often transition to accrual accounting to meet regulatory requirements or achieve a more comprehensive financial picture.

This transition is not without its pitfalls and considerations, particularly when understanding its impact on enterprise valuation resulting from the quality of earnings process. Key considerations when converting from cash to accrual accounting include revenue recognition in accordance with ASC 606, expense accrual recognitions, managing changes in working capital, and earnings volatility.

Cash accounting, also called checkbook accounting, entails recording transactions when cash changes hands, which provides management with a straightforward method for tracking cash flow. Small businesses often prefer this method because the IRS allows it when certain size criteria are met and because it is easier to track money as it moves in and out of bank accounts. Further, there is no need to evaluate accounts receivable or payable to determine income when using cash accounting, simplifying the management of the financial statements as a whole.

However, for healthcare entities, this simplicity can be misleading, as it does not capture the true financial obligations and revenues tied to patient care and insurance reimbursements. Accrual accounting, on the other hand, records revenues when they are earned and expenses when they are incurred, regardless of when cash is exchanged. While cash accounting may be simpler for small businesses, accrual accounting offers a more accurate representation of a company’s financial health, especially as they grow and become more complex.

A crucial component of most healthcare services transactions is the quality of earnings analysis, which aims to assess the sustainability and accuracy of historical earnings and the achievability of future earnings, thereby providing potential buyers with a clear understanding of the company’s true earning potential.

Transitioning from cash-basis accounting to accrual accounting entails significant differences and challenges in revenue recognition. Under cash-basis accounting, revenue is recognized when cash is received, while accrual accounting dictates recognition when revenue is earned, irrespective of cash-flow timing. This shift necessitates adjustments to accurately reflect revenue generated within a given period, especially for long-term contracts or services rendered where cash receipts may occur at different points from when the revenue is earned. Challenges arise in estimating and timing revenue recognition, requiring careful assessment of performance obligations, delivery, and collectability.

Issues stemming from the diverse revenue streams and payment models prevalent in healthcare, such as fee-for-service, capitation, and bundled payments add an additional layer of complexity when converting from cash to accrual accounting, as each payment model has distinct timing and recognition criteria. Additionally, healthcare entities often engage in complex contractual arrangements with payors and providers, leading to variations in revenue and expense recognition practices. Moreover, healthcare organizations may have unique regulatory requirements and accounting treatments for certain transactions, further complicating conversion efforts.

Differences in case mix, payor mix, and procedure mix among healthcare entities can also impact revenue recognition as the collectability of outstanding accounts receivable is often different for specific payor and case mixes. Cash waterfalls, zero-balance analyses, and other revenue hindsight analyses are leveraged as part of VMG Health’s comprehensive quality of revenue analysis to ensure revenue recognition is converted from a cash basis to an accrual basis in accordance with ASC 606. Adherence to revenue recognition principles, while requiring meticulous analysis to mitigate misinterpretation and manipulation, is a critical component to a quality of earnings analysis, as it ensures financial statements provide a more comprehensive view of revenue performance, enhancing transparency and comparability. For further detail on quality of revenue analysis, see VMG Health’s previous article: Proceed with Caution: Five Key Considerations in Quality of Revenue Analysis.

Transitioning from cash to accrual accounting presents unique challenges beyond revenue recognition. One significant hurdle lies in accurately accounting for expenses, particularly in healthcare facilities where costs often span various departments and service lines. Accrual accounting requires recognizing expenses when incurred, irrespective of cash outflows, which can be intricate in healthcare settings due to the complex nature of patient care, procurement of medical supplies, and maintenance of facilities. Ensuring accountants properly match expenses to the periods in which they contribute to patient care or administrative functions may require complex allocation and estimation methodologies.

For instance, the timing and recognition of expenses related to medical supplies and pharmaceuticals can vary based on inventory management practices and rebate arrangements with suppliers. Historical cost of goods sold analysis and margin analysis are two of the most common strategies implemented to understand underlying changes in the business, providing a basis for accurately matching expenses to the relevant accounting periods. In large healthcare systems, these complexities are further amplified by the need to allocate costs accurately across multiple departments and service lines, such as inpatient, outpatient, surgical, and emergency services. Addressing expense accrual challenges necessitates a comprehensive understanding of healthcare operations and collaboration between finance and operational personnel to ensure the accuracy of accrual conversions.

In the context of a transaction, small businesses may prepay (malpractice insurance) or pay after the fact (common area maintenance charges) for certain expenses, which must be converted to an accrual basis to properly inform a buyer of the business’ financial condition.

Shifting from cash to accrual accounting also affects the management and assessment of working capital. Under cash accounting, working capital appears straightforward, often mirroring the cash flow directly. However, accrual accounting requires a more nuanced view, recognizing accounts receivable, accounts payable, and inventory changes that may not have immediate cash implications but significantly impact liquidity and operational efficiency. Accurate tracking and managing these elements is crucial, as they influence a healthcare organization’s true financial position and operational performance and may have purchase price implications.

Understanding and converting net working capital on an accrual basis also helps shareholders and potential buyers identify a business’ strengths and potential weaknesses. For healthcare entities, a rise in accounts receivable under accrual accounting indicates future cash inflows but also highlights the importance of effective revenue cycle management, including timely billing and collection processes. Similarly, accounts payable under accrual accounting provide insights into a company’s obligations and upcoming cash outflows, lending toward robust vendor management and procurement practices. Healthcare entities must develop comprehensive systems for monitoring these working capital components to ensure they reflect the actual financial health and to make informed decisions regarding cash management, investment opportunities, and strategic planning. However, there must first be benchmark net working capital to compare future trends.

Under cash accounting, earnings may appear more volatile, as revenues and expenses are recorded only when cash transactions occur. However, accrual accounting captures economic events more accurately and consistently. Fluctuations in reported earnings can be caused by timing differences in revenue and expense recognition and can be particularly pronounced in the healthcare sector, where seasonal variations and payor reimbursement lags are common, causing revenue to be recognized in one period and the corresponding expenses in another on a cash basis of accounting.

For stakeholders and potential investors, understanding the sources and implications of this volatility is crucial for assessing the company’s true financial health. Cash-to-accrual conversions within a quality of earnings analysis help identify and normalize these fluctuations, providing a clearer picture of sustainable earnings and operational performance. By aligning revenue and expense recognition to an accrual basis, stakeholders can benefit from more reliable insights into the company’s financial trajectory, aiding better investment and management decisions. For healthcare entities, this detailed analysis is particularly vital, given the sector’s unique financial dynamics and regulatory landscape. The application of advanced analytical techniques, such as trend analysis and scenario modeling, can further enhance the understanding of earnings volatility and its impact on long-term financial planning and stability.

Converting from cash accounting to accrual accounting in a quality of earnings analysis offers several positive benefits. Accrual accounting provides a more accurate reflection of a company’s financial performance by matching revenues and expenses to the periods in which they are earned or incurred, offering a clearer picture of the company’s profitability over time. This enables stakeholders to make better-informed decisions regarding operational changes, investment, lending, or acquisition opportunities. Additionally, accrual accounting enhances comparability with industry peers and facilitates benchmarking analysis, as financial statements prepared under an accrual basis are inherently more standardized and comparable. Moreover, accrual accounting can uncover trends and patterns in revenue and expense behaviors, providing deeper insights into the company’s underlying financial health and operational efficiency. Overall, the conversion to accrual accounting strengthens the transparency, reliability, and credibility of earnings analysis, fostering trust among investors, creditors, and other stakeholders.

Written by Timothy Kent; Jordan Tussy, CVA; Molly Smith

GenesisCare, a prominent provider of cancer services worldwide, filed for voluntary reorganization under Chapter 11 of the U.S. Bankruptcy Code on June 1, 2023, in the United States Bankruptcy Court for the Southern District of Texas (Case No. 23-90614). The Australian-based company, once valued at $5 billion and backed by private equity firm KKR, faced financial difficulties due to high debt levels and operational challenges.

Founded in 2004 by Dan Collins, GenesisCare (the “Company”) served Australian cancer patients until 2015, when the Company expanded to Europe via its purchase of eight cancer centers from Cancer Partners UK. During 2016, GenesisCare continued growing its European operations through the acquisitions of 17 centers in Spain from IMOncology and Oncosur Group.

In late 2019, GenesisCare made headlines with the acquisition of U.S.-based cancer provider 21st Century Oncology for $1.5 billion. Two years prior, 21st Century Oncology filed for bankruptcy because of declining reimbursement and “regulatory costs concerning electronic records and legal expenses.” At the time of acquisition by GenesisCare, 21st Century Oncology operated 294 locations, including 124 radiation oncology centers, with an estimated $230 million of earnings before interest, tax, and depreciation (EBITDA).

While rapidly expanding GenesisCare’s footprint, the 21st Century acquisition left the Company with significant levels of debt and a new operations base that was reemerging from bankruptcy. GenesisCare faced significant challenges in its effort to turnaround the U.S. operations, including an aging equipment base and IT system, operational inefficiencies, and increased competition. Prior to GenesisCare’s Chapter 11 filing, they reported approximately $2 billion of total debt on its balance sheet, largely associated with the 21st Century acquisition.

In March 2023, CEO and Founder Dan Collins stepped down, and three months later, the Company filed for bankruptcy on June 1, 2023.

Five months after its initial filing, GenesisCare announced the U.S. Bankruptcy Court for the Southern District of Texas confirmed the Company’s Chapter 11 Plan of Reorganization after receiving support from approximately 95% of voting creditors. The plan included significant deleveraging of GenesisCare’s balance sheet, with a reduction in total debt by approximately $1.7 billion.

On February 16, 2024, GenesisCare completed its reorganization process and emerged from Chapter 11. As part of its reorganization plan, GenesisCare will operate as four distinct businesses in the U.S., Australia, Spain, and the UK, with an independent governance structure and Board of Directors for each business. Furthermore, the businesses will be responsible for the strategies and performance of their market. The Company also received approximately $56 million of new capital infusion from investor groups to help support the growth of the remaining businesses. As a result of the restructuring plan, the Company is prepared to move forward well capitalized with a relatively low level of debt and a more focused operational strategy.

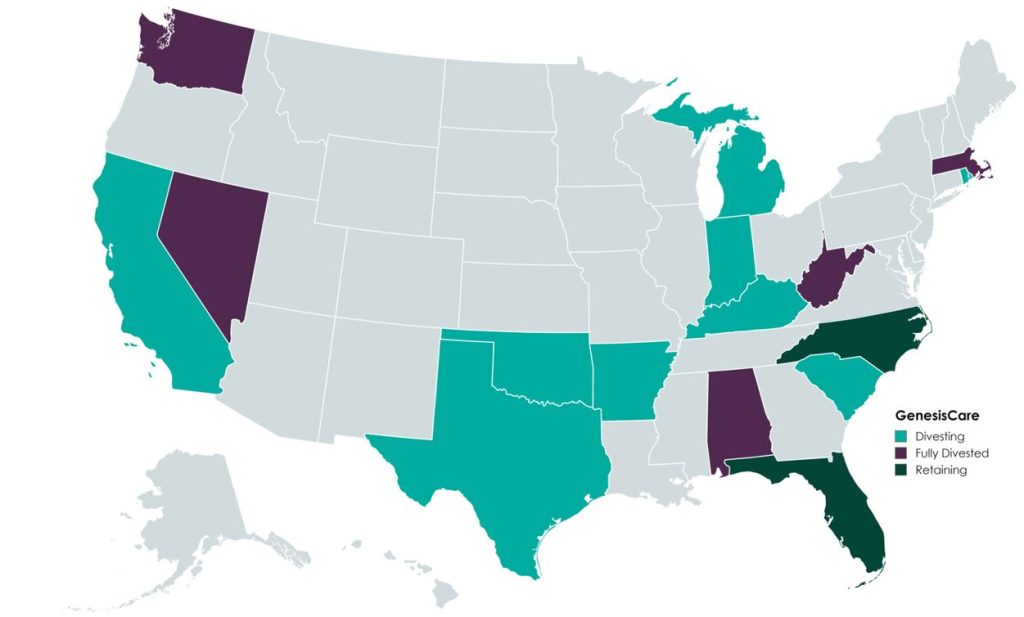

In the U.S., GenesisCare will retain practices in the “fast-growing markets” of Florida and North Carolina, which will continue to offer similar cancer care services (medical oncology, radiation oncology, surgery, and imaging). Currently, the Company operates 145 locations across the two states. GenesisCare has sold or is in the process of divesting its remaining assets across 14 states.

Newly appointed chief executive officer David Young said, “I am confident that our independently run businesses are strongly positioned to capture the exciting opportunities available to them in the markets they serve while never losing sight of our core goal: delivering better life outcomes to patients.”

A primary objective of GenesisCare’s restructuring plan was to divest all U.S.-based assets outside of North Carolina and Florida. This decision was part of its strategic plan to focus on core operations to ensure long-term sustainability.

According to bankruptcy filing documents, GenesisCare has divested 32 locations across 14 states. Assuming all of the transactions close at the defined purchase price in the transaction agreements, cash proceeds to GenesisCare would be approximately $113 million, with an implied equity value of approximately $131 million (see chart below). The assets have drawn interest from many different buyer types, including health systems, large oncology platforms, and practices. Dr. Shaden Marzouk, President of GenesisCare U.S., said, “The strong interest we received from a wide variety of buyers from across the U.S. is a reflection of what we have long known―that GenesisCare’s U.S. business benefits from an incredible team, a desirable footprint and a proven ability to care for patients.”

One notable transaction was OneOncology’s acquisition of two radiation oncology practices in South Carolina for $25.0 million (per the asset purchase agreement), expanding OneOncology’s service offerings in an existing market. CEO of OneOncology, Jeff Patton, MD, said, “For OneOncology, these are two great business assets that are really the only radiation facilities that are open in that market. It’s a market we were already in, so sometimes things match up well.” Specifically, OneOncology acquired a Myrtle Beach facility with three linear accelerators and a Conway Center with one.

California-based Sutter Health purchased five radiation oncology practices in Modesto, San Luis Obispo, Santa Cruz, Stockton, and Templeton, California. According to the purchase agreement, the total purchase price for these centers was $32 million. President and CEO of Sutter Health, Warner Thomas said, “We know how important it is for specialty services like cancer care to be offered close to home so patients can stay on track with their treatments. Keeping continued cancer care accessible in these communities was a driving force for Sutter to acquire these care centers.” Sutter also has certain capital investments in mind, including new radiation oncology equipment, technologies, and other support services.

Based on Kroll’s bankruptcy docket, there are medical and radiation oncology assets still available for sale, which could result in increased transaction activity with interest buyers, such as health systems, private equity–backed oncology platforms, and practice acquisitions. After successfully emerging from Chapter 11, GenesisCare is entering a new chapter, as emphasized by CEO David Young: “GenesisCare has achieved the goals it set out at the beginning of its restructuring process. We exit Chapter 11 with great businesses, each with a compelling future.” The Company’s focus on continuous growth is highlighted by the planned construction of three new radiation oncology centers in Australia, scheduled to open in 2024. With a more concentrated U.S. and global platform, GenesisCare has indicated that it is well positioned for future growth as a newly capitalized, low-debt entity committed to providing the highest level of care for its patients.

Patrick, A. (2024, February 18). GenesisCare emerges from bankruptcy, cuts deal with government. Australian Financial Review. Retrieved from https://www.afr.com/companies/healthcare-and-fitness/genesiscare-emerges-from-bankruptcy-cuts-deal-with-government-20240218-p5f5t5

Staff Writer. (2024). Amid major cancer care bankruptcy, oncology clinics sold. Oncology News Central. Retrieved from https://www.oncologynewscentral.com/article/amid-major-cancer-care-bankruptcy-oncology-clinics-sold

GenesisCare. (2024). GenesisCare’s reorganisation plan confirmed with overwhelming support from voting creditors. GenesisCare. Retrieved from https://www.genesiscare.com/au/news/genesiscare-reorganisation-plan-confirmed-with-overwhelming-support-from-voting-creditors

GenesisCare. (2024). GenesisCare completes reorganisation and emerges from Chapter 11. GenesisCare. Retrieved from https://www.genesiscare.com/au/news/genesiscare-completes-reorganisation-and-emerges-from-chapter-11

Patrick, A. (2019, December 13). Aussie cancer outfit makes first US move in $1.5b deal. Australian Financial Review. Retrieved from https://www.afr.com/companies/healthcare-and-fitness/aussie-cancer-outfit-makes-first-us-move-in-1-5b-deal-20191213-p53js7

Private Equity Stakeholder Project. (2024). Private equity healthcare bankruptcies are on the rise. Private Equity Stakeholder Project. Retrieved from https://pestakeholder.org/reports/private-equity-healthcare-bankruptcies-are-on-the-rise/

Authors