ASCs in 2023: A Year in Review

Rachel Linch

February 13, 2024

Written by Joel Gomez, ASA

Before you begin the process of selling your medical practice, it is always in your best interest to ensure your practice’s value is accurately represented. Most buyers of medical practices, including healthcare systems and hospitals, begin the transaction process with a fair market value analysis of the business revenues to determine the purchase price. Unfortunately, many practices in the position of selling are in a break-even or negative cash–flow scenario. In these instances, the value of the practice may be most accurately represented by the fair market value of personal property and real property.

Some buyers opt to have personal property valued on a “desktop” scope of work, relying on data in the form of a depreciation schedule or practice inventory as the basis of the fair market value analysis. While acceptable for fair market value purposes, this approach may not capture all owned personal property.

The first approach for identifying personal property through accounting documents is the use of a depreciation schedule or fixed asset listing (FAL). While real property is easily identifiable (the space is either owned or rented), personal property listings are often less maintained, reliant on an accountant’s tracking of capitalized assets, and may not fully reflect what is owned. When preparing a valuation, an appraiser is always subject to the quality of available data. FALs maintained by an accountant only display equipment that meets the predetermined capitalization cost threshold determined by that accountant. Additionally, some capitalized assets are removed from the FAL once it has fully depreciated according to accounting standards. Providing an equipment appraiser, a FAL as the basis of their appraisal could mean valuable practice assets are not captured.

An on-site inspection and asset inventory by an appraiser allows them to capture all assets on a room-by-room basis, regardless of original purchase cost or visibility on the FAL.

Another alternative to an appraiser performing an on-site inspection is to have a practice employee create the inventory. While this may sound like a good approach initially, information captured by someone other than an appraisal expert tends to be inconsistent. Items captured in one room are missed in the next, and inconsistent asset descriptions will lead to follow-up information requests, requiring the selling practice to invest more work hours.

Hiring an appraisal expert to complete an on-site inventory and inspection of the practice’s tangible personal property ensures personal property listings are maintained, fully reflect what is owned, and include consistent asset descriptions from room to room. VMG Health reviewed a sampling of projects over the past 18 months, across several practice specialties, and noted that when completing a site visit as part of our valuation process, the fair market value conclusion of exam rooms was roughly 60%–70% higher on a per-room basis compared to relying on practice data/inventories.

VMG Health’s qualified equipment appraisers have the knowledge and experience to complete a discrete and comprehensive inventory, gathering all necessary data during the visit and minimizing interruptions to the practice operations and patient flow.

VMG Health’s team of equipment appraisers has over 55 years of experience in the equipment appraisal field across all sectors of the healthcare industry and includes three accredited senior appraisers with the American Society of Appraisers. Since 1995, VMG Health has earned the trust of our clients with extensive expertise in navigating the dynamic factors that influence value. If you are in the process of valuing your practice, use VMG Health’s equipment appraisers to complete an on-site inspection, inventory, and valuation of your personal property.

Written by Isabella Rosman and Tim Spadaro, CFA, CPA/ABV

The following article was published by Becker’s Hospital Review.

Throughout VMG Health’s client base, we are privileged to work with many major players across the physician practices landscape—from solo practitioners and independent physician groups to large platform practices, private equity (PE)–backed physician practice rollups, and those affiliated with large health systems.

VMG Health has been engaged to assist clients in varying capacities associated with transactions, ranging from providing business valuations to financial due diligence (quality of earnings). This insight has provided important visibility into the buyer’s perspective. Further, our work has delved into the operations of practices, including coding and compliance, physician compensation, and strategy work. As a result, our experience offers us a unique glimpse into physician practices and the underlying transaction environment. From our experience, including anecdotal discussions with clients and operators in this space, we’ve outlined a few major headwinds and tailwinds facing physician practice transactions in 2024.

Reimbursement Pressure: Physician practices continue to face reimbursement pressure. In November 2023, the Centers for Medicare & Medicaid Services (CMS) issued its final rule announcing policy changes for Medicare payments under the Physician Fee Schedule (PFS) for 2024. Per CMS, overall payment rates under the PFS will be reduced by 1.25% in 2024, following a 2.0% decline in 2023. Although the overall impact on reimbursement varies across specialties, the rate cuts will continue to suppress margins and put pressure on physician practices. For more information on operational challenges and opportunities with physician practices, see VMG Health’s most recent Physician Alignment Tips & Trends Report.

Persistent Inflation: Wage inflation (largely driven by a tight labor market, an aging physician base, and recruiting challenges) and the rising costs of drug and medical supplies have been persistent. According to the government’s Medicare Economic Index (MEI), medical practice costs are expected to increase by 4.6% in FY 2024 on top of last year’s 3.8% increase. Without reimbursement keeping pace with increasing costs, many physician practices’ profit margins have contracted.

Many physician practices seek out a partner to help combat the daily pressures they face. Practices may benefit from operational synergies by consolidating with a larger organization, particularly if the larger organization has favorable reimbursement rates or anticipated cost savings from duplicate services (back-office employees, external accounting, etc.). In fact, many buy-side clients run a managed care or “black box” analysis to assess the potential rate lift and the resulting practice economics on a post-transaction basis to better inform themselves and their investment committees during diligence. Contact VMG Health’s Revenue Consulting & Analytics team to analyze the potential rate lift on your next deal.

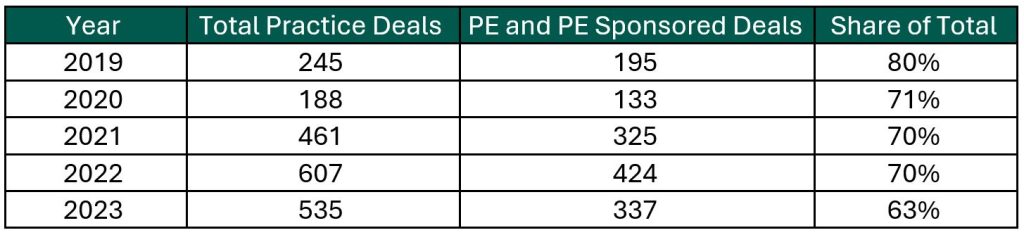

Record High Dry Powder: PE has been an active participant in the physician practice transaction space for many years, as evidenced by recent deal volume presented in the table below. Capital committed to PE funds but not yet deployed (dry powder) is presently at record highs for healthcare services. The current estimate of dry powder earmarked for healthcare services among U.S. headquartered PE managers is approximately $100 billion, according to Pitchbook’s Q4-2023 Healthcare Report. PE funds are regularly searching for a home to deploy this capital and physician practices are a common target.

Source: Irvin Levin, 2024 Health Care Services Acquisition Report

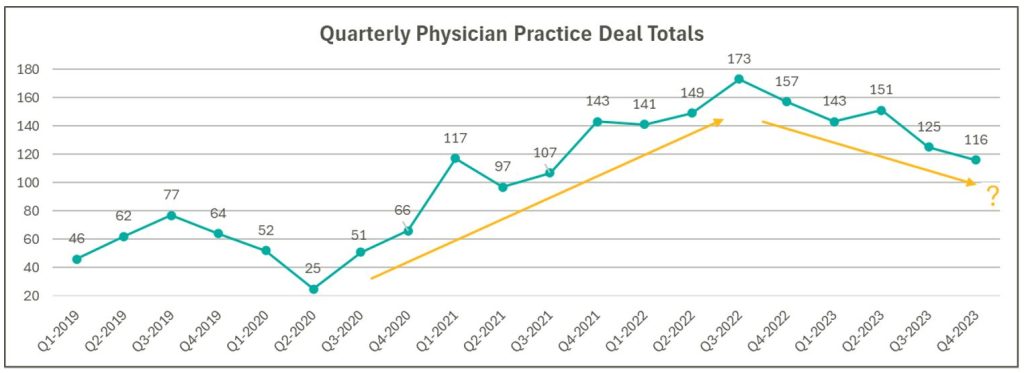

Source: Irvin Levin, Healthcare M&A Quarterly Reports

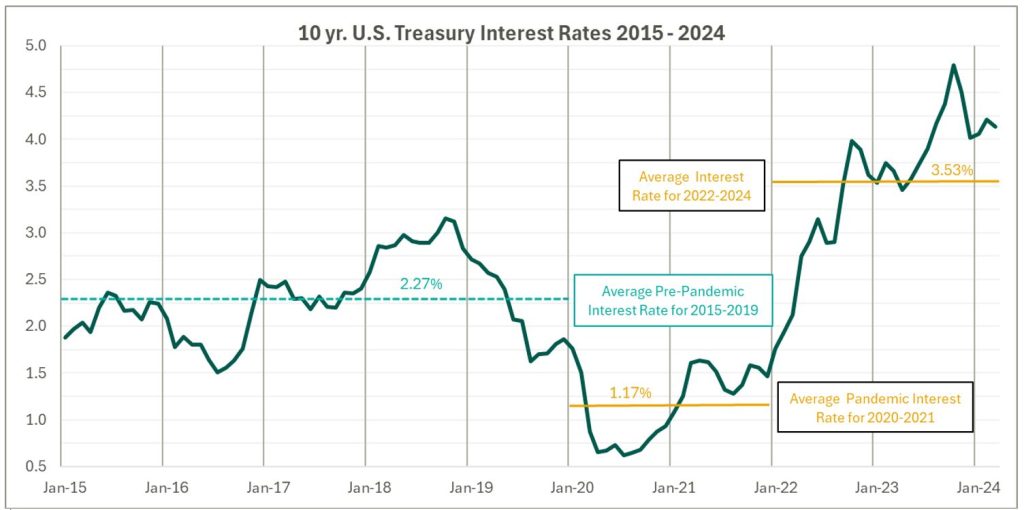

High Interest Rates: As the pandemic hit, fiscal stimulus and loosened monetary policy led to ultra-low interest rates relative to historical norms and spurred transaction activity. Interest rates began to materially rise throughout 2022, challenging overall transaction activity in the latter part of 2022 and during 2023 as access to capital tightened and the cost of capital increased. The below chart presents interest rates over the period as measured by the 10-year U.S. treasury.

Despite higher rates, transaction activity for physician practices has remained robust relative to pre-pandemic levels. However, there are signs that interest rates are having a lagged effect on deal volume considering the recent downward trend from Q3 2022 through Q4 2023 as observed in the above chart. While this does not necessarily mean that we should expect deal volume to revert to pre-pandemic levels, it does highlight that we have entered a new transaction environment. In this environment, the time to close deals lengthens as sellers digest lower valuation multiples and buyers increase scrutiny during due diligence given an uncertain future macroeconomic landscape. Contact VMG Health’s Financial Due Diligence team for details on how the changing tide is impacting the due diligence process.

At the start of 2024, interest rates remain elevated and volatile with an uncertain path to a normalized level, which continues to serve as a headwind for transaction activity. However, interest rates can change quickly, and the U.S. Federal Reserve has signaled that it will likely be appropriate to begin rate cuts at some point during 2024. Market participants have started anticipating rate cuts from this messaging, which could certainly serve as a tailwind throughout the remaining course of this year and into next.

Source: Federal Reserve 10 Year U.S. Treasury Market Data

Regulatory Transaction Oversight: Healthcare consumes a considerable amount of U.S. spending and is expected to continue increasing; CMS’ National Health Expenditure Accounts (NHEA) Healthcare projects healthcare spending to increase from approximately 18.3% of U.S. GDP in 2021 to 19.6% in 2031. Furthermore, it is an election year, with a current U.S. Presidential Administration keenly focused on the rising costs of healthcare. As a result, increased regulatory scrutiny has manifested itself over the ongoing consolidation across healthcare services, particularly within the physician practice space.

This heightened scrutiny is most recently evidenced by the Federal Trade Commission (FTC) suing U.S. Anesthesia Partners, Inc. (USAP), a prominent provider of anesthesia services in Texas, over an alleged “…anticompetitive acquisition spree to suppress competition and unfairly drive-up prices for anesthesiology services.” The FTC also hosted a workshop on March 5, 2024 to assess the public impact of private capital in healthcare. On that same day, the FTC, U.S. Department of Justice (DOJ) and U.S. Department of Health and Human Services (HHS) requested public comments on the effects of transactions involving PE, health systems, and payors on the healthcare providers and ancillary services space.

FTC Focus on Non-compete Agreements: It is not uncommon for physicians to a sign non-compete agreement upon joining a physician practice. The intent of a non-compete agreement, as well as the potential impact, are being hotly debated, with the FTC proposing a rule to ban non-compete clauses. A recent VMG article, Non-Compete Agreements: A Prevailing Quagmire provides details highlighting the arguments and broader implications of non-compete agreements and the proposed ban.

Overall interest in acquiring physician practices remains high, and we don’t expect that to change in the foreseeable future. The dynamics outlined above will likely dictate the path and volume of transactions throughout 2024 and beyond. To read more and stay informed as the year unfolds, please visit VMGHealth.com.

Centers for Medicare & Medicaid Services. Calendar Year (CY) 2024 Medicare Physician Fee Schedule Final Rule. Centers for Medicare & Medicaid Services website. Published November 2, 2023. https://www.cms.gov/newsroom/fact-sheets/calendar-year-cy-2024-medicare-physician-fee-schedule-final-rule

Centers for Medicare & Medicaid Services. CMS Finalizes Physician Payment Rule, Advances Health Equity. Centers for Medicare & Medicaid Services website. Published November 2, 2023. https://www.cms.gov/newsroom/press-releases/cms-finalizes-physician-payment-rule-advances-health-equity

Landi H. Physician groups decry finalized Medicare payment cuts as 2024 expenses rise. FierceHealthcare. Published November 3, 2023. https://www.fiercehealthcare.com/providers/physician-groups-decry-finalized-medicare-payment-cuts-2024-expenses-rise

American Medical Association. Only Cure for Medicare Payment Mess: Wholesale Reform. American Medical Association website. https://www.ama-assn.org/about/leadership/only-cure-medicare-payment-mess-wholesale-reform#:~:text=To%20put%20this%20into%20perspective,top%20of%20last%20year’s%203.8%25https://www.ama-assn.org/about/leadership/only-cure-medicare-payment-mess-wholesale-reform#:~:text=To%20put%20this%20into%20perspective,top%20of%20last%20year’s%203.8%25

VMG Health. 2023 Healthcare M&A Report. Published [publication date not provided]. https://vmghealth.com/2023-healthcare-ma-report/ https://vmghealth.com/2023-healthcare-ma-report/

PitchBook. Q4 2023 Healthcare Services Report. Published [publication date not provided]. https://pitchbook.com/news/reports/q4-2023-healthcare-services-report

Reuters. Fed’s Powell Set Election-Year Stage with Testimony on Rate Cuts, Inflation. Reuters website. Published March 6, 2024. https://www.reuters.com/markets/us/feds-powell-set-election-year-stage-with-testimony-rate-cuts-inflation-2024-03-06/

Centers for Medicare & Medicaid Services. National Health Expenditure Fact Sheet. Centers for Medicare & Medicaid Services website. Published [publication date not provided]. https://www.cms.gov/data-research/statistics-trends-and-reports/national-health-expenditure-data/nhe-fact-sheet

Federal Trade Commission. FTC Challenges Private Equity Firm’s Scheme to Suppress Competition in Anesthesiology Practices Across the United States. Federal Trade Commission website. Published September [publication date not provided], 2023. https://www.ftc.gov/news-events/news/press-releases/2023/09/ftc-challenges-private-equity-firms-scheme-suppress-competition-anesthesiology-practices-across

McDermott Will & Emery LLP. Top Takeaways: FTC Hosts Workshop, Solicits Public Comment on Private Equity in Healthcare. McDermott Will & Emery LLP website. Published [publication date not provided]. https://www.mwe.com/pdf/top-takeaways-ftc-hosts-workshop-solicits-public-comment-on-pe-in-healthcare/

Aguirre I. Non-Compete Agreements: A Prevailing Quagmire. VMG Health website. Published [publication date not provided]. https://vmghealth.com/thought-leadership/blog/non-compete-agreements-a-prevailing-quagmire/https://vmghealth.com/thought-leadership/blog/non-compete-agreements-a-prevailing-quagmire/https://vmghealth.com/thought-leadership/blog/non-compete-agreements-a-prevailing-quagmire/

Written by Grayson Terrell, CPA

The following article was published by Becker’s Hospital Review.

In today’s complex healthcare environment, mergers and acquisitions (M&A) are proving to be more challenging than ever, with heightened governmental regulations impacting both the operation of an entity and the purchase and sale of an entity.

To successfully navigate a transaction in the healthcare sector, it is paramount that buyers and sellers make informed decisions through all of the tools made available to them. For sellers, this can come in the form of understanding how their business operates, understanding inefficiencies and growth opportunities, and even understanding what their business is worth. For buyers, informed decision making relies heavily upon understanding the markets in which they are investing, including governmental regulations in some states that may impact their ability to invest and operate; understanding the key operating metrics of similar companies in similar industries; and ensuring that they are paying an appropriate amount for the business. This is especially important because, in healthcare transactions, the capital used to purchase is often provided by investors who are counting on timely positive returns.

Financial due diligence (FDD) is pivotal to the success of any healthcare transaction, as it requires detailed investigation and analysis of a company’s financial information and is used to validate a company’s true run-rate operating potential. With most healthcare M&A transactions, purchase price is based on a multiple of a company’s salable earnings before interest, taxes, depreciation, and amortization (EBITDA). As such, the buyer and seller must perform the appropriate financial due diligence procedures prior to executing a transaction. Below are five vital aspects of the financial due diligence process.

The Quality of Earnings (QofE) process consists of making adjustments to the entity’s reported financial statements to normalize EBITDA. The bulk of these adjustments involve adjusting or removing impacts of non-recurring and one-time items from earnings to arrive at an adjusted EBITDA figure that represents a more accurate view of the entity’s true cashflows. This process also gives the FDD team the opportunity to pose pointed questions related to the entity’s operations, finances, and accounting functions, highlighting key information that could negatively or positively impact adjusted earnings. Specific to healthcare transactions, some of the relevant areas of interest with respect to potential EBITDA adjustments are:

The Quality of Revenue (QofR) analysis may be the most important part of the FDD process when it comes to healthcare-related transactions, given the unique characteristics and nuances of healthcare revenue. During this process in many middle-market healthcare deals, the conversion of revenue from cash basis to accrual basis is a fundamental exercise with respect to the QofE analysis. The cash waterfall approach is the gold standard and therefore the most common method for accomplishing the cash-to-accrual conversion. With this method, detailed billing data is obtained from the entity’s revenue cycle management (RCM) system, which includes charges by date of service and payments by date of service and by date of payment. In this analysis, payments are adjusted back to their specific date of service (accrual basis), and outstanding collections on charges billed during the period under analysis are estimated based on historical collection patterns cut by payor, CPT code, or various other means.

Pro forma adjustments are forward-looking projections on certain aspects of the business, which are layered back in across the historical financial statements. These assumptions can help buyers understand potential areas of future direction and growth opportunities for the company; however, these adjustments should be thoroughly scrutinized during buy-side FDD procedures to ensure the adjusted EBITDA and purchase price are not over- or understated. These estimations tend to lean more in favor of the seller and are often a primary area of focus by the opposing buy-side FDD team. As such, a seller should understand all aspects of the business, especially as they relate to these forward-looking projections, and should be able to support the key inputs utilized to derive these pro forma adjustments. If properly supported, these adjustments often increase the sale price of the business enough to cover the cost of FDD procedures incurred by the seller, if not many times over. Some examples of commonly observed pro forma adjustments in healthcare related QofE reports include:

Another common analysis in FDD procedures is a Net Working Capital analysis, which is used to determine the working capital (current assets less current liabilities, excluding cash and debt) required to operate a business in the post-transaction environment. This subsection of FDD typically involves substantial negotiation between buyers and sellers when approaching the close of a deal, as both parties will view various inputs differently, often striving to set a working capital peg that is more favorable for themselves. As a miscalculation of this peg can cost a seller on a dollar-for-dollar basis if the agreed-upon level of net working capital is not met, it is imperative that management and their advisors are involved and knowledgeable on this calculation.

Most of the time, healthcare transactions occur on a cash-free, debt-free basis. Standard with any cash-basis business, many debt and debt-like items have the potential to be inaccurately reflected within a company’s balance sheet. As such, a Debt and Debt-Like Items analysis can assist buyers and sellers in understanding a company’s debts and liabilities as of the date of sale. These items can include potential tax-related exposures, outstanding litigation and legal settlements, deferred compensation, notes payable, and others.

In closing, FDD is a necessary step in ensuring that sellers have the keys to sell their businesses at the best possible price, and buyers can protect the money of their companies, firms, or investors by making a sound investment in the target company. This proactive approach creates trust between all parties and leads to more lucrative transactions for all.

Written by Grayson Terrell, CPA; Joe Scott, CPA; Lukas Recio, CPA; Wayne Prior, CPA; and the Baker Tilly team

The M&A healthcare industry presents a unique set of challenges, and it is important to have the proper M&A professionals involved to assist with identifying potential deal issues. In addition to financial due diligence experts, M&A tax professionals should assist with understanding and identifying the transactional tax consequences, as the identified tax issues may impact the overall deal structure or may be used to negotiate in the purchase agreement. During the M&A due diligence lifecycle, financial and tax due diligence teams must collaborate closely. This collaboration often uncovers synergies between their processes, enhancing completeness and efficiency. As their work is often completed first, the financial due diligence team may act as the first line of defense and can assist with identifying potential exposures earlier in the process. M&A tax advisors can assist with vetting and quantifying these exposures, which can assist with limiting the identified risks during the purchase negotiations. Tax considerations often influence the structure of a sale, determining whether it’s taxable or tax-free, whether assets or equity are bought, and whether taxable gains can be delayed through methods like earn-outs, installment sales, and debt.

The starting point for tax diligence is understanding the tax entity type of the target included in the transaction. Different tax issues may arise depending on how the entity is treated for tax purposes. The common tax entity types are:

S corporation:

Partnership:

C corporation:

Improper independent contractor classification (applicable to all tax entity types). While some employers misclassify their employees as independent contractors in error, others do it intentionally to avoid paying state and federal payroll taxes by passing that responsibility onto the employee. Employers found to have misclassified their employees are subject to payroll tax and penalties that could succeed to the buyer. During due diligence, it’s important to determine whether independent contractors should be considered full-time employees. A common healthcare tax due diligence issue is the misclassification of certified registered nurse anesthetists (CRNAs), doctors, and other healthcare professionals as independent contractors. It is important to request IRS Form 1099 and understand the services performed by the independent contractors. Depending on the time dedicated to the business, level of pay, direction from the employer, and several other factors, there may be contractors who could be misclassified, resulting in potential payroll tax exposures. The IRS provides a 20-factor test to help make that determination with considerations related to direction and control.

Unclaimed property (applicable to all entity types). Each state has an unclaimed property statute governing when and what types of property must be remitted to it. Examples of unclaimed property include uncashed or unclaimed refund checks, patient overpayments, insurance overpayments, payroll checks, or vendor checks. If unclaimed after a certain period (dormancy period), those checks must be turned over to the state. This is a common issue amongst healthcare providers, as there may be instances where a patient’s insurance covers more than what was originally estimated for an appointment or procedure, resulting in a patient overpayment. In a situation where a healthcare provider sees non-recurring patients, the patients are less likely to use a credit balance toward a future appointment. It is important to review the target’s accounts payable and accounts receivable aging schedules to determine whether there are any balances that give rise to an unclaimed property risk. Financial due diligence teams will likely have access to the target’s financials and can assist with pulling the documentation necessary to evaluate these potential risks. To avoid possible unclaimed property liability, buyers should determine whether the target is properly addressing its escheatable property.

Improper treatment of owner personal expenses (applicable to S and C corporations). Is the S corporation owner using a corporate account for any personal expenses? If so, these payments may be considered compensation and subject to payroll tax. If the employer’s share of payroll tax is unpaid, the buyer could be held liable for the amount owed after the acquisition, including interest and penalties. In parallel, if a C corporation shareholder is conducting similar activities, the IRS or state revenue service may classify these expenses as dividends, which are non-deductible for income tax purposes.

Unreasonable owner compensation (applicable to S and C corporations). Since an S corporation shareholder’s distributive share of income is not subject to self-employment or payroll tax, owners are often motivated to minimize their salary in favor of non-wage distributions. However, if the IRS determines an owner’s salary to be too low based on multiple factors—including profits, business activities, and the shareholder’s involvement in the business—non-wage distributions could be reclassified to wages subject to employment taxes. The buyer may be responsible for this tax if it isn’t resolved before the acquisition. Conversely, if a C corporation shareholder’s salary is too high relative to the available facts, the IRS or state revenue service may deem the compensation to be excessive and reclassify a portion to dividends.

Related-party transactions (applicable to all entity types). A related-party transaction takes place between two parties that hold a pre-existing connection prior to a transaction. There are many types of transactions that can be conducted between related parties, such as sales, asset transfers, leases, lending arrangements, guarantees, and allocations of common costs. These transactions can become problematic when an S corporation utilizes them as a vehicle to get extra cash out of the business. If a shareholder owns both Company A and Company B, and Company A pays the shareholder a below-market salary while also renting a building from Company B (an LLC taxed as flow-through) at inflated rates, it may be considered disguised compensation to avoid payroll taxes. It is important to request copies of the lease agreements and understand the fair market value of the square footage and rent of the property to determine a potential disguised compensation risk as it relates to related-party transactions. Problematic related-party transactions should be addressed during due diligence.

Cash vs. accrual accounting method (applicable to all entity types). The IRS prefers the accrual method, but if a company is on the cash basis of accounting for tax purposes, the buyer should determine whether they meet the requirements to continue using that method. The change in accounting method from cash to accrual may result in additional income that could be recognized in the post-closing period. By identifying the issue and quantifying the potential exposure, the buyer and seller can negotiate who will bear the tax on the additional income.

Pass-through entity tax (PTET) (applicable to S corporations and partnerships). In certain states, eligible S corporations can make PTET elections, whereby the entity is responsible for paying the shareholder’s share of tax at the entity level. States began enacting responses to state and local tax deduction limitation because of the 2017 Tax Cuts and Jobs Act (TCJA), which limited the allowable deduction for state and local taxes on an individual’s tax return to $10,000. The primary benefit is reduction of federal income taxes; however, use caution when evaluating whether benefit exists on state returns. PTET elections may shift the successor liability for state income taxes from the shareholder to the entity. Most of the elections are irrevocable. During due diligence, determine whether the company has made these elections for the states that have enacted these rules. Given the ever-changing PTET rules, companies should maintain a process to review company’s PTET elections.

20 Percent Deduction Under Section 199A (applicable to S corporations and partnerships). Section 199A was enacted as part of the TCJA and provides a deduction for qualified business income (QBI) from a qualified trade or business operated directly or through a pass-through entity. For healthcare providers, the application of Section 199A can be complex due to the nature of healthcare services being classified as a non-qualifying Specified Service Trade or Business (SSTB). However, certain healthcare-related businesses may qualify, such as a dermatology practice’s sales of skincare products or certain laboratories whose tests benefit the healthcare industry but aren’t independently viewed as health services. Additionally, while a doctor, nurse, or dentist is in the field of health, someone who merely endeavors to improve overall well-being, such as a personal trainer or the owner of a health club, is not in the field of health.

Built-in gains tax (applicable to S corporations). When a corporation has converted its status from C corporation to S corporation, or has acquired assets from a C corporation in a tax-free transaction and has a recognition event within five years, it may be subject to a corporate-level, “built-in gains” tax in addition to the tax imposed on its shareholders from the transaction. The buyer can leverage its knowledge of a potential, built-in-gains tax liability, as identified in the due diligence process, to negotiate with the seller such that the buyer would not inherit said liability.

Non-resident withholding (applicable to S corporations and partnerships). State and local governments are permitted to tax the income of their residents and the income of nonresidents if that income is derived from sources within their state or locality. It’s important to ensure that the S corporation or partnership complies with state and local income tax withholding regulations.

When it comes to healthcare acquisitions, it is important to consider the above items from a tax perspective. Financial and tax due diligence teams should work together to help buyers and sellers avoid tax liabilities, identify unrealized tax savings, and structure the transaction in a tax-efficient manner. Baker Tilly’s M&A tax team can assist in identifying the related risks and opportunities associated with healthcare acquisitions, all in an effort to maximize value. If you have any questions or would like additional information, please contact:

Michael O’Connor, Partner Emeritus: Michael.OConnor@bakertilly.com

Michael DeRose, Senior Manager: Michael.DeRose@bakertilly.com

Peter Dewan, Manager: Pete.Dewan@bakertilly.com

Kendra Nowak, Senior Associate: Kendra.Nowak@bakertilly.com

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

I spoke with King and Spalding attorney Kim Roeder on different, hot-button issues that arise when structuring and valuing different value-based arrangements. It started off as a presentation of different case studies and focused on what Roeder has encountered from a legal perspective and what I have encountered from a valuation perspective. We often receive questions when it comes to structure or even value drivers, and we wanted to present solutions to what we saw or clients struggling with so that they could develop a better understanding of them.

The focus on the metrics themselves and how carefully they need to be considered seemed to be the most surprising. Recent regulations have been really focused on metrics, and that’s what we get the most questions about. I think our audience was also surprised to learn that Kim had experienced those questions as well, and metrics aren’t just a consideration on the valuation perspective. Both legal and valuation perspectives must carefully consider metrics.

Our presentation was a very pragmatic way of illustrating six key issues that often come up during valuation. It’s a great resource for healthcare leaders to reference as they go through and check the boxes to ensure they have thought through all of the considerations that we often see as eleventh-hour issues.

I co-wrote a section of the 2023 Physician Alignment: Tips and Trends Report that discusses quality incentives for providers. It captures key factors to consider, from a valuation perspective, when looking to enter value-based arrangements and where to start.

Value-based arrangements require a very orchestrated balance between legal and compliance, operational champions, and valuation teams. Operational teams should be able to focus on what changes and improvements they want to implement, valuation teams must have an understanding of those goals, and legal and compliance must be involved to ensure the approach is appropriate and compliant. Without cohesion between these three groups, we see those eleventh-hour issues pop up.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.

Authors