The Perils of the “Trend and Bend” (Part 1 of 3)

September 6, 2012

Part One: Trend and Bend

When I think of the trend and bend (or just bend), I’m always reminded of the classic line by Irwin M. Fletcher as aircraft mechanic G. Gordon Liddy “c’mon guys, it’s so simple, do you need a refresher course, it’s all ball bearings these days”. Neither the quote nor the process is as simple as it seems.

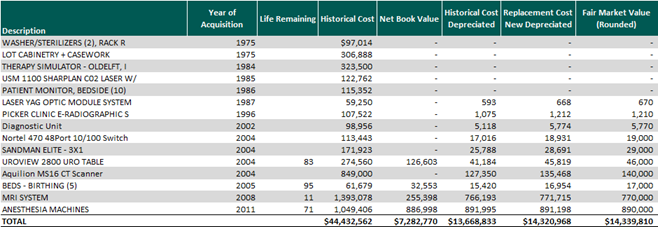

So as a brief “refresher course”, the trend part of the process comes from applying equipment specific cost indices to the historical cost (note not original cost) to estimate an indirect replacement cost new. The distinction between historical cost and original cost is notable because historical cost is intended to reflect an asset when new, whereas original cost can mean new cost, new to the current owner, or used. Used costs should NEVER be trended, so historical cost is the only cost that should be trended.

The asset class derives from a lookup table that has 80+ trends. The trends are based on information available from the Bureau of Labor Statistics – Producer Price Index. Note that the trend for certain assets is identical, despite a difference in age. Identical trends mean that data was unavailable beyond a certain time frame and is notable for two specific reasons: the asset is very old and/or the trend beyond that time frame would result in an unreasonable estimate of replacement cost new. Trending historical costs beyond ten years is, at best, a dicey proposition.

After applying a trend to a historical cost, we arrive at replacement cost new. Many also refer to this result as a reproduction cost new, since the historical cost basis typically includes reproducing an asset of identical utility, which is obviously different from “like or similar utility.”

This goes without saying that welearned a long time ago that certain things in life should not ever be reproduced: the IBM PC Jr, the Ford Pinto, the AMC Pacer, and Michael Moore all leap to mind, so we try to avoid the reproduction term. We work around the concept of reproduction cost new by referring to the “trend” as helping estimate an indirect replacement cost new. In an ideal world we could find current replacement cost new information to either confirm our indirect estimate or allow us to override the indirect estimate.

Without this confirmation, by definition, we have implied we have not researched the new equipment cost market for the actual cost to replace an asset, but have merely gone through a mathematical exercise. Make no mistake, the results of a purely mathematical exercise are imprecise and therefore unreliable.

Categories: