Written by Mallorie Holguin and Patrick McGinn

Over the last several years, healthcare executives and practice administrators have faced challenges in securing anesthesiology services, particularly in the inpatient setting. These challenges have been exacerbated over the past couple of years due to staffing shortages caused by the COVID-19 pandemic and an ever-increasing demand for anesthesia services.

At the outset of 2023, the United States population consisted of approximately 65.6 million adults eligible for Medicare with a projected growth to 76 million Medicare-eligible adults in 2030 [1]. The projected growth in the Medicare-eligible population will result in a corresponding increase in demand for inpatient procedures and diagnostic testing which may require anesthesia and the expertise of anesthesiologists, certified registered nurse anesthetists (CRNAs), and other anesthesia providers [2]. Meanwhile, current data reported by the Association of American Medical Colleges (AAMC) suggests only 43.1% of active anesthesiologists are under the age of 55, and there is a projected shortage of 12,500 anesthesiologists in 2033 [3,4]. Furthermore, anesthesiologists are largely practicing as independent providers to hospitals/health systems and are faced with decreasing reimbursement and increased expenses related to staffing, supply chain, and provider compensation.

Reimbursement Trends

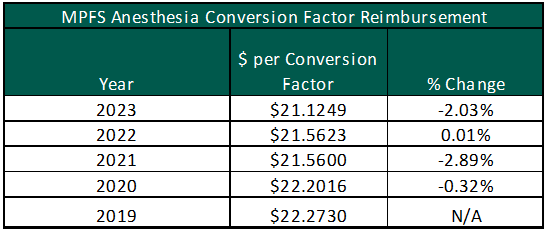

While the demand for anesthesia services increases, reimbursement for Medicare patients has decreased from $22.2730 per unit in 2019 to $21.1249 in 2023 under the Medicare Physician Fee Schedule (MPFS). The chart to the right illustrates the year-over-year percentage change in the anesthesia conversion factor under the MPFS. Anesthesia providers were further impacted by the implementation of the No Surprises Act (NSA) and the independent dispute resolution (IDR) process. The NSA has led to unintended consequences for anesthesia providers. Based on discussions with anesthesia practice leaders, payor insurers have utilized the IDR to reduce their required reimbursement by refusing to go in-network with the anesthesia providers [5,6]. As a result, VMG Health has been receiving an increasingly high number of requested subsidy arrangements for ambulatory surgery centers (ASCs). Hospitals and other free-standing surgery centers should partner with their anesthesia group and advocate for in-network contracts with all major payors in their market.

Staffing Shortages & Market Compensation Pressure

The reduction in federal and commercial reimbursement for anesthesia services compounds the increased cost pressures faced by anesthesia providers, particularly as it relates to provider staffing costs. Per Medscape’s 2023 Physician Compensation Report, anesthesiology reported a 10% increase in compensation which is consistent with market-observed trends and conversations with health system operators. The charts below show the most current compensation data for anesthesiologists and CRNAs from the AMGA, MGMA, SullivanCotter, Inc., and Gallagher compensation and productivity survey reports:

MGMA recently released its 2023 Provider Compensation and Production Survey Report, which shows further increases in median compensation levels: anesthesiology compensation falling close to $500,000 and CRNA compensation reported at approximately $215,000. At the same time, Merritt Hawkins reports record-level sign-on bonuses, relocation expenses, and medical education loan repayments.

New Reality for Anesthesiology Groups & Health Systems

The confluence of decreased federal and commercial reimbursement amid increased compensation associated with staffing anesthesia providers is challenging independent anesthesiology groups and health system/ASC partners. Going forward, health systems, ASCs, and anesthesia partners may need to consider alternative partnerships including acquiring the practice, negotiating a new professional services agreement or amending an existing one, and/or considering recruitment assistance. Regardless of the avenue, the anesthesia practice will likely require some sort of direct support (e.g., through revenue guarantees or subsidy arrangements) to ensure they are able to recruit and retain providers.

In each of the cases outlined above, documentation that illustrates the relationship between the parties has been established at fair market value (FMV) and represents best practices for compliance and regulatory purposes. Regarding the direct employment of anesthesiologists and CRNAs, the employment terms should be based on the personally performed services of the respective provider and the unique demands of the local market. For anesthesiology revenue guarantee and subsidy arrangements, key factors to consider are the number of anesthetizing locations, the proposed care team model (i.e., physician medical direction versus supervision), and the projected payor mix of the facility. As previously mentioned, the NSA has led to decreased commercial reimbursement which has led to the need for subsidy/revenue guarantee agreements for ASCs that historically have not been required.

As health systems, ASC systems, and anesthesia providers navigate the increasing demand for anesthesia services in the face of declining federal and commercial reimbursement, VMG Health can provide both FMV and strategic services for the various stakeholders.

Sources

- Center for Medicare and Medicaid Services. (2023). National Healthcare Expenditures, Health Insurance Enrollment and Enrollment Growth Rates, Table 17.

- Merritt Hawkins. (2021). Anesthesiology: Supply, Demand and Recruiting Trends

- Association of American Medical Colleges. (2019). Active Physicians by Age and Specialty, 2019. Physician Specialty Data Report.

- Lee, L. (January 12, 2023). Opportunities for Operational Efficiency in Anesthesia Services. FTI Consulting.

- Newitt, P. (September 16, 2022). The downsides to the No Surprises Act’s dispute resolution process. Becker’s ASC Review.

- Newitt, P. (December 22, 2022). No Surprises Act is hurting anesthesia reimbursements, CEO says. Becker’s ASC Review.

- Kane, L. (April 14, 2023). Medscape Physician Compensation Report 2023: Your Income vs Your Peers’. Medscape.

- Merritt Hawkins. (June 30, 2022). 2022 Review of Physician and Advanced Practitioner Recruiting Incentives.