Sitting Down with Our Industry Experts: Debra Stinchcomb

May 7, 2024

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

1. Can you provide a high-level overview of what you spoke about at the Ambulatory Surgery Center Association Conference and Expo?

The title of my presentation was Anatomy of a Deposition. My co-speaker, Will Miller, from Higgs Fletcher & Mack in San Diego, and I discussed what a deposition is and how it fits into the steps of a lawsuit from patient injury to subpoena, the discovery phase and the trial itself. We discussed how to prepare for a deposition, the possible ramifications of not utilizing an attorney in the process, and how to answer questions during a trial honestly while learning from your lawyer’s cues. For example, if you’re asked a question and your lawyer objects and says the question is vague and ambiguous, you might take that as a hint that you need to ask for the question to be rephrased before you respond.

2. What do you think the audience was the most surprised to learn from your presentation?

I received feedback from someone who was there, and they said that the presentation was a great reminder to pay attention to their documentation practices. It’s important not to get complacent with the documentation and to ensure nursing staff document what they need to while watching the scope of practice and licensure of themselves and other employees at the facility. You must always be cognizant of whether they’re functioning within their licensure or certification, and this course was a great reminder of that.

3. How do you think your presentation helped healthcare leaders better prepare for challenges?

I’ve already heard from a few people who are taking this information back to their surgery centers, and they’re educating their staff on proper nursing documentation as well as risk management, and giving them a little taste of what a deposition might be like. The two cases we highlighted in our presentation included documentation issues, such as not documenting on the correct form, not adding post-op score accurately, and lack of physician orders. These issues highlight why staff must pay attention to what they document and be sure their medical record tells the story of the patient experience. Leaders can use this information to show their staff what improper documentation looks like to a jury, how it ruins credibility, and the importance of proper documentation.

4. What resources would you suggest for those interested in learning more?

ESupport is an annual subscription for ambulatory surgery centers (ASCs), and it includes a host of resources: updated policies and procedures, a forum where they can write to and learn from a consultant, tools they can use in just about every aspect of their ASCs, and continuing education modules. Specific to this issue, we have a one-page training document on nursing documentation and an hour-long webinar that dives deeper into the topic.

Within ESupport, there’s also a risk management page that talks about more than just depositions; it provides a nice overview of what risk management is and some of the tools that people can use in their risk management program.

5. If someone takes only one message from your presentation, what would you want it to be?

Go back to Nursing Documentation 101. The rules have not changed, so go back to the basics. Make sure you document everything going on with your patients. Your documentation should reflect a patient’s story; if I read your medical record, it should tell me everything that happened with that patient during their episode with you.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.

Navigating Value-Based Care: Insights from Nicole Montanaro at the ABA Emerging Issues in Healthcare Law Conference

May 2, 2024

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

1. Can you provide a high-level overview of what you spoke about at the American Bar Association Emerging Issues in Healthcare Law Conference?

I spoke with King and Spalding attorney Kim Roeder on different, hot-button issues that arise when structuring and valuing different value-based arrangements. It started off as a presentation of different case studies and focused on what Roeder has encountered from a legal perspective and what I have encountered from a valuation perspective. We often receive questions when it comes to structure or even value drivers, and we wanted to present solutions to what we saw or clients struggling with so that they could develop a better understanding of them.

2. What do you think the audience was the most surprised to learn from your presentation?

The focus on the metrics themselves and how carefully they need to be considered seemed to be the most surprising. Recent regulations have been really focused on metrics, and that’s what we get the most questions about. I think our audience was also surprised to learn that Kim had experienced those questions as well, and metrics aren’t just a consideration on the valuation perspective. Both legal and valuation perspectives must carefully consider metrics.

3. How do you think your presentation helped healthcare leaders better prepare for challenges?

Our presentation was a very pragmatic way of illustrating six key issues that often come up during valuation. It’s a great resource for healthcare leaders to reference as they go through and check the boxes to ensure they have thought through all of the considerations that we often see as eleventh-hour issues.

4. What resources would you suggest for those interested in learning more?

I co-wrote a section of the 2023 Physician Alignment: Tips and Trends Report that discusses quality incentives for providers. It captures key factors to consider, from a valuation perspective, when looking to enter value-based arrangements and where to start.

5. If someone takes only one message from your presentation, what would you want it to be?

Value-based arrangements require a very orchestrated balance between legal and compliance, operational champions, and valuation teams. Operational teams should be able to focus on what changes and improvements they want to implement, valuation teams must have an understanding of those goals, and legal and compliance must be involved to ensure the approach is appropriate and compliant. Without cohesion between these three groups, we see those eleventh-hour issues pop up.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.

Hospitals and health systems have been developing strategies for vertical integration with physician groups for decades. Through the premise of integrated care delivery, “defined as a coherent set of methods and models on the funding, administrative, organizational, service delivery and clinical levels,” U.S. policymakers, healthcare operators and payors expect to improve the quality, service and efficiency of healthcare services. Results of value generated through integrated delivery models are mixed, and the operating model is often confounded with varying market dynamics (payor concentration, culture, physician supply/demand, leadership, etc.) by community.

Regardless of integrated care delivery success, health system employment continues to increase and today accounts for greater than 50% of all practicing physicians. Interestingly and unknown to many, other strategics (private equity, Optum, CVS, etc.) account for approximately another 25%, leaving approximately a quarter of physicians organized in a private practice.

Figure 1: 2023 Physician Employment by Type

Source: Physicians Advocacy Institute: Physician Practice Trends Specialty Report

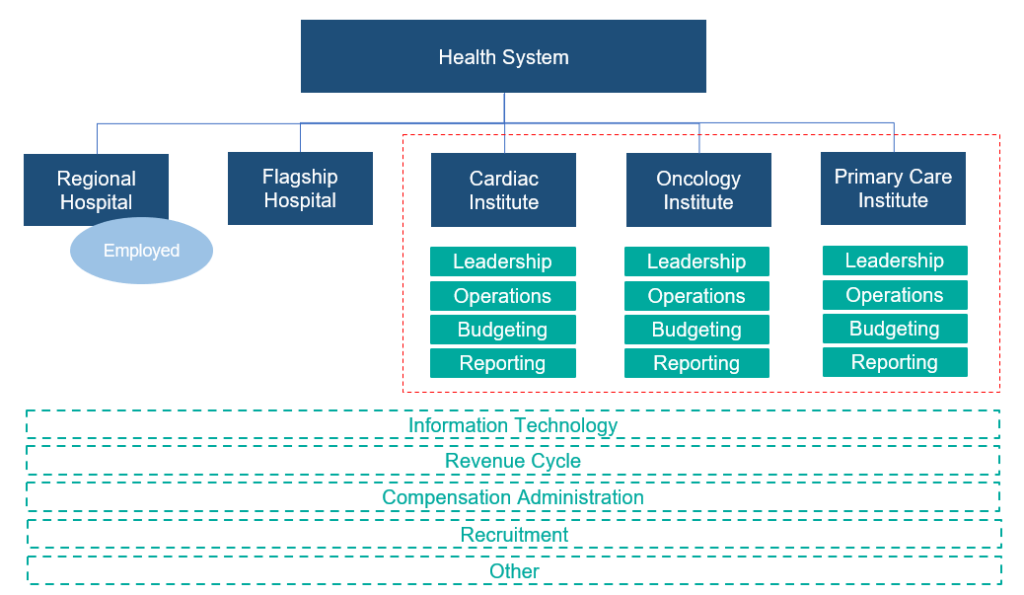

Across many integrated delivery systems, physicians are organized under a formal medical group structure, often with supporting leadership, governance, and practice management systems. This structure essentially groups the collective interests of primary care, surgical subspecialists, medical subspecialists, and hospital-based physicians together. Unlike independent, multispecialty practices who have an underpinning of sharing economics, most multispecialty groups in integrated delivery systems lack material financial alignment across subspecialties.

To this end, there are several challenges with a multispecialty group structure in health systems, including an aggregation of physician losses whereby various revenue streams (e.g., in-office ancillaries) have been integrated with hospital operations, sensitivity to practice losses based on confounding facts as to the true operating performance, silo board and/or decision making, and frustration by large clinical service lines due to widely held convention that everything needs to be the same for all physicians across the physician enterprise. Figure 2 outlines the most prevalent medical group structure and its multispecialty orientation.

Figure 2: Prevalent Medical Group Structure for Employed Physicians

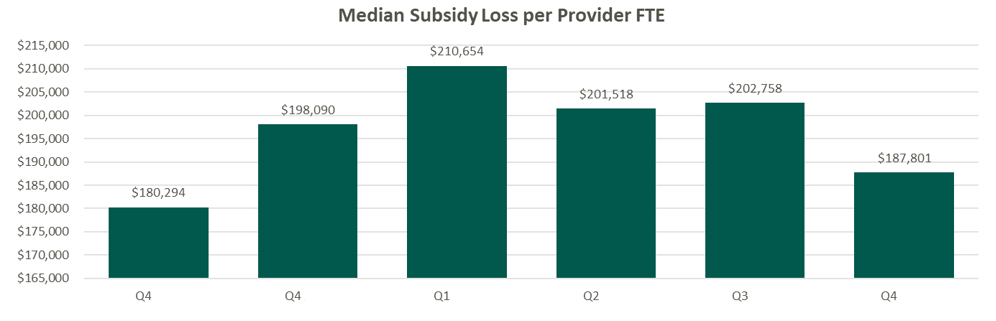

Financial system reporting remains inconsistent across organizations; however, there are data repositories that suggest continued median subsidies for employed providers. As figure 3 outlines, regardless of timing and/or subspecialty orientation, there remains a significant net investment per provider.

Figure 3: Median Subsidy (Combined Subspecialty Mix)

Source: Kaufman Hall Flash Reports

Based on VMG Health’s experience, significant financial reporting subsidies lead to suboptimized decision making, as significant pressure is placed on medical group leadership to reduce practice losses and improve overall practice performance. This has led to a variety of strategic missteps for organizations operating in competitive markets.

As an alternative, VMG Health has been working with clients to reorganize physician enterprise offerings inside of integrated delivery systems, including the development of financial reporting, management, and governance systems that better align care delivery across service lines. These more contemporary structures, while variable system to system, are all designed to:

Boost physician loyalty to their primary clinical practice location (e.g., office based, value-based orientation, hospital, ASC, etc.).

Improve leadership, financial reporting, and budgeting so that business units are accountable for both facility- and professional-level operations and key performance indicators.

Afford focus on best-in-class infrastructure to support all professional practice applications.

Remove silo barriers and outdated concepts of medical group subsidies and associated strategic implications from an antiquated structure.

Figure 4: Contemporary Medical Group Structure

Conclusion

The landscape of physician organizational structures within hospitals and health systems remains in transition. While traditional, multispecialty group practice models remain prevalent, challenges such as physician losses and inconsistent financial reporting have spurred the need for more contemporary structures. Through strategic reorganization and improved governance, health systems can enhance physician loyalty, accountability, growth, and operational efficiency, ultimately optimizing care delivery and aligned (or improved) financial performance.

Sources

Heeringa, J., et. al. (2020). Horizontal and Vertical Integration of Health Care Providers: A Framework for Understanding Various Provider Organizational Structures. National Library of Medicine. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC6978994/

Sitting Down with Our Industry Experts: Andrew Maller

April 17, 2024

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

1. Can you provide a high-level overview of what you spoke about at the American Society of Ophthalmic Administrators/American Society of Cataract and Refractive Surgery Annual Meeting?

The course itself, Physician Compensation Trends for Employed and Owner Providers, had two main focal points. We discussed current compensation and benefits trends for employed providers in group practices, as well as tips for assessing the feasibility of adding new providers in today’s challenging recruitment environment. We also discussed common income and expense sharing models for owner providers in group practices.

2. What do you think the audience was the most surprised to learn from your presentation?

The biggest surprise for attendees was just how competitive the current recruitment environment is for practices looking to hire new providers. There truly is a supply and demand imbalance, meaning that there are more practices looking to hire providers than there are available ophthalmologists looking for positions. The combination of this challenge with influences from private equity–backed companies has resulted in higher, guaranteed starting salaries for providers on the job market.

All of this is happening while practices are facing declining reimbursement and ever-increasing operating expenses, making the challenging decision to hire a new provider even more complicated.

Many practices I work with feel that this is a challenge to them specifically, based on geography or practice situation. However, the reality is that ophthalmic practices across the country are all struggling to recruit.

3. How do you think your presentation helped healthcare leaders better prepare for challenges?

One of the key topics of discussion focused on developing a thorough feasibility analysis when determining whether the timing is right to hire a new provider. Practices can exponentially increase their likelihood of making the right decision by taking a disciplined approach in assessing the revenue opportunity for the new provider, their estimated compensation, and other incremental overhead costs. The hiring decision should not be made based on a gut feeling, but instead through a review of objective data points given the potential positive (or negative) impact to the practice.

4. What resources would you suggest for those interested in learning more?

BSM Connection for Ophthalmology has a several fantastic resources for practices in the recruitment process, including the New Provider Feasibility Analyzer and the Key Contract Considerations Guide for ophthalmologists and optometrists, which provide guidance on compensation and benefit trends. The Provider Recruitment section of the website also includes a Contract Review Worksheet and a sample Letter of Understanding, although we always recommend practices work with legal counsel to ensure appropriate documentation is completed.

For information regarding income and compensation models, our experts have written articles related to income-sharing models for group practices. VMG Health also offers a Provider Needs Assessment.

5. If someone takes only one message from your presentation, what would you want it to be?

With all areas of practice management, leaders must make business decisions using a disciplined approach. That starts with being educated and realizing the challenges that exist right now when it comes to provider recruitment.

As it relates to owner income and expense-sharing models, the takeaway is the need for transparency. Practice administrators and executives are often the ones charged with administering the compensation model, so the key is to remain neutral and transparent throughout the entire process.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.

Fair Market Value and Commercial Reasonableness Considerations Amid CMS Radiopharmaceutical Reimbursement Challenges

April 4, 2024

Written byCarla Zarazua, Preston Edison, and James Tekippe, CFA

Radiopharmaceutical drugs (RPs) are “radioactive substances used for diagnostic or therapeutic purposes.” To effectively diagnose and treat diseases, physicians need to have access to radiopharmaceutical agents that will assist with detecting and treating medical conditions. The current pricing methodology for RPs under the Centers for Medicare and Medicaid Services (CMS) has created a financial burden on hospitals and health systems. In addition, it has created a barrier to patient access when considering the utilization of diagnostic RPs in hospital outpatient departments. This article will outline the challenges created by the current CMS payment structure and outline steps hospitals and health systems can take to remain compliant with fair market value (FMV) and commercial reasonableness (CR) while CMS reconsiders its position.

In the 2008 Hospital Outpatient Prospective Payment System (HOPPS) final rule, CMS opted to categorize all diagnostic RPs as supplies rather than drugs. Under this current pricing structure, the reimbursement for diagnostic RPs is bundled into the technical procedure rate, known as a “policy-packaged drug.” CMS categorizes procedures with similar costs and clinical work effort into an ambulatory payment classification (APC) group. All procedures in an APC group are reimbursed at the same rate based on the average cost of all the procedures within that APC, inclusive of the primary service, ancillary service, and drug. As such, there is a set price for procedures in an APC group regardless of the policy-packaged drug in use. Unfortunately, this pricing methodology can create a misalignment in the expense incurred to acquire an RP and the reimbursement received from CMS, especially for high-cost drugs.

A report issued by the U.S. Government Accountability Office indicated that CMS will encourage hospitals to use the most effective resource that minimizes costs while still being able to meet the patient care needs. In addition, the structure does not incentivize medically unnecessary services and encourages hospitals to negotiate drug purchase pricing with manufacturers.

There is a temporary exception to the pricing for RPs for new and high-costs drugs, which can qualify for a pass-through period of two to three years. Under the pass-through methodology, the RP will be paid separately from the technical procedure rate at the average sales price + 6% incurred by a provider for the RP. Although this provides some relief to the misalignment of costs and reimbursement for RPs, the pass-through period is finite for an RP, and once outside of the pass-through period, an RP will be bundled or “packaged” within the APC procedure rate. Although CMS’ intent is understandable, under the current pricing model, hospitals may face a challenging financial burden, and providers may be confronted with difficult decisions that may impact patient care.

In the post-COVID era, hospitals have increased focus on increasing margins and reducing costs, and the current payment structure for RPs is putting increased pressure on the hospitals’ and health systems’ bottom line. Various stakeholders have voiced concerns about the economic burden resulting from CMS’ payment structure for RPs. For example, the American Medical Association indicated that, for financial reasons, hospitals may need to limit or end the use of radiopharmaceuticals, especially the high-cost or newer ones, given the misalignment in reimbursement. In addition, the American Hospital Association has put out a statement that the 2024 HOPPS final rule is an “inadequate update to hospital payments.” Hospitals and health systems unfortunately face heavy financial risk if a provider chooses to select a policy-packaged, high-cost drug that is more than the APC payment rate for a procedure. For this reason, hospitals may want to limit the use of the high-cost drugs by its providers, which may cause patients to receive sub-optimal care.

Given this dynamic, providers may choose not to utilize more expensive or advanced RPs, although it may be better off for a patient in the long term. As indicated by the Medical Imaging & Technology Alliance (MITAS), utilizing an advanced RP would be more beneficial in the patient’s overall treatment management, as these RPs have earlier, more accurate detection and can actually reduce the use of other unnecessary treatments because physicians will be in a better position to understand and treat the disease. Even more challenging, some advanced RPs truly have no alternative or substitute, so concerns about costs may result in the use of a less effective RP, which could result in misdiagnoses and ill-tailored treatment plans.Lastly, the lack of reimbursement inhibits innovation and development of new drugs because drug manufacturers would not be incentivized to continue the research and development if the drugs have a low clinical use.

As demonstrated above, there are several issues with the current pricing structure for RPs, but CMS has asked for comments on potential remedies. In the 2024 CMS proposed rule, CMS outlined the following five alternative payment models for RPs:

Paying separately for diagnostic radiopharmaceuticals with per-day costs above the OPPS drug packaging threshold of $140

Establishing a specific per-day cost threshold that may be greater or less than the OPPS drug packaging threshold

Restructuring the ambulatory payment classification (APC), including by adding nuclear medicine APCs for services that utilize high-cost diagnostic radiopharmaceuticals

Creating specific payment policies for diagnostic radiopharmaceuticals used in clinical trials

Adopting codes that incorporate the disease state being diagnosed or a diagnostic indication of a particular class of diagnostic radiopharmaceuticals.

While various stakeholders appreciate CMS requesting and seeking recommendations on changes to the structure, many stakeholders such as MITAS and the American College of Radiology (ACR) recommend that “CMS establish separate payment for diagnostic radiopharmaceuticals, including a per day cost threshold based on average sales price (ASP) + 6% methodology.” Stakeholders believe this method will allow for adequate reimbursement and treatment access options for patients.

Unfortunately, CMS did not make a decision on how to move forward with the reimbursement structure for radiopharmaceuticals in the 2024 HOPPS final rule. Given the potential, pending changes in reimbursement, and the fact that CMS reimburses some RPs at a lower amount than it costs to acquire them, it is important for hospital outpatient departments to document and outline a plan with their care teams on how best to use RPs within their organization to remain compliant when it comes to FMV and CR. As such, VMG Health has outlined some important factors to consider for each compliance component in the interim.

Fair Market Value:

Review any existing or new agreements with vendors and negotiate pricing when able.

Engage a third-party valuator to review any existing or new agreements and determine market comparable pricing of the services.

Although, the price paid for the drug may be within market range upon determining FMV, CMS may not reimburse at this rate for certain RPs. As such, given that CMS is the most widely cited market comparable and a market maker in terms of how these drugs are reimbursed, hospitals may find that they are losing on these types of arrangements. For this reason, it is important to document the legitimate business purpose of the use of the RP:

Commercial Reasonableness:

Document reasons for medical necessity of higher-priced drugs.

Have a documented process “decision tree” for deciding which radiopharmaceuticals to use on patients.

Consider the frequency and volumes of how often these drugs are used and document it.

While CMS hasn’t reached a solution on the changes to reimbursement for RPs, it is important for hospitals and health systems to consider the financial and patient care implications of what RPs providers use. Developing compliance protocols around how best to determine the utilization of these RPs can minimize the risk placed on patients and hospitals.

Sources

GAO. (2021). Medicare Part B Payments and Use for Selected New, High-Cost Drugs. United States Government Accountability Office. https://www.gao.gov/assets/720/712727.pdf

Klitzke, A. (2023). Passage of the Facilitating Innovative Nuclear Diagnostics (FIND) Act. American Medical Association Organized Medical Staff Section. https://www.ama-assn.org/system/files/i23-omss-resolution-7.pdf

Trouble in Paradise? Disputes, Divorce, and Damages

April 3, 2024

Written byIngrid Aguirre, CFA

The formation of any business partnership typically begins with an eager commitment by each party to pursue a particular goal, business, or venture. Often, the endeavor begins with an eagerness and readiness to overcome growing pains and challenges at the onset. However, some challenges cannot be overcome, and instead, they may exacerbate what turns into a tenuous relationship. Healthcare partnerships are not exempt from these challenges. Over its almost 30-year history of serving healthcare clients, VMG Health has been engaged to perform a variety of damage analyses and provide its expert witness services, including, but not limited to, disputes, divorces, and commercial damages. These damages are often in the form of diminution of business value or lost profits. VMG Health has served as a trusted advisor to its clients amid these challenging situations.

Disputes

Ambulatory surgery centers (ASCs) are one such example where disputes may arise. With at least 11,000 surgery centers nationwide and with multiple partners at each of these surgery centers, there are many instances where disputes arise among partners (often consisting of physicians, health systems, and management companies). Typical to any business where partners come and go, physicians will buy in and buy out of surgery centers. This opens the door to disputes in situations where one partner is offered a purchase price that may not be appropriate. Alternatively, a physician may be forcibly redeemed of her shares. Inevitably, the greater the number of partners, combined with human nature, the greater the likelihood of an eventual dispute. Of course, disputes are certainly not specific to surgery centers but remain an ever-present adversity insofar as human fallibility exists.

In these disputes, it is typical to engage attorneys who subsequently may engage healthcare expert appraisers to determine the value of the interest in question. A few examples, specific to surgery centers, whereby VMG Health has provided its expert opinion, and in some cases, expert witness testimony on, are as follows:

Surgery center dispute whereby the relationship between physicians and the operator soured, resulting in the physicians abandoning the surgery center and damaging the operator owner’s interest.

Surgery center dispute where the buy-out price for a non-controlling interest was in question.

Surgery center where a physician owner was inappropriately terminated without cause.

Surgery center where distributions were inappropriately withheld by one of the owners.

Divorce

Marital dissolution has its challenges and unique considerations. One key component is determining the allocation of community assets among both spouses. The challenges lie in determining the value of private interests that either spouse may own. This may take the form of the entirety of a privately held business (e.g., physician practice or lab company) or an interest in a smaller, yet still private, business (e.g., interest in an ASC). Regardless of the interest owned, it is imperative to determine the value of a private business for the purpose of a marital dissolution.

Unlike other disputes among business partners, a marital dissolution has its nuanced challenges that an appraiser must understand. First, an appraiser must understand state specific requirements, through discussions with legal counsel, regarding any statutory regulations on equitable distribution. Some states follow the policy of equitable distribution, which requires a fair allocation of the assets between spouses at the time of a divorce. It is necessary to understand the jurisdiction, particularly if the state does not require equitable distribution. Second, an appraiser must understand personal goodwill. Personal goodwill may be defined as the value created and attributed to an individual’s efforts. As an example, personal goodwill may be applied to a physician owner. However, understanding that the business itself may have goodwill, it is important that the appraiser separate enterprise goodwill from personal goodwill, as applicable. Quantifying personal goodwill is necessary to understand when providing an opinion for purposes of a marital dissolution. Third, the valuation date must be defined following discussions with legal counsel. In a marital dissolution, the valuation date may be based on the date of separation, the date of filing or the date of trial.

VMG Health has provided expert opinions, and in some cases, expert witness testimony, on a variety of marital dissolutions, including, but not limited to, the following:

Marital dissolution of a provider owning interest in a pain management business, a surgery center, and pharmacies.

Marital dissolution of a physician owning a primary care business.

Marital dissolution of a physician owning interest in a surgery center.

Marital dissolution of a physician with a healthcare product in development.

Marital dissolution of an owner of a home care business.

Damages

Last, not too dissimilar from a marital dissolution, a partnership between business owners or other parties that are contractually aligned may also fracture. The quantification of damages may take the form of a valuation, a calculation of value, or a lost profits analysis. Due to the unique nature of each damage engagement, it is imperative to define and quantify the damage appropriately. This also requires the valuation expert to work closely with the client’s legal counsel.

Lost profits and damages calculations have been performed by VMG Health along with expert witness services in a variety of scenarios, including, but not limited to the following:

Lost profits calculation for a franchisor violating its agreement with a franchisee.

Lost profits calculation regarding an agreement between a payor and health system.

Calculation of patient revenue lost attributable to an unauthorized letter distributed to former patients.

Calculation of damage whereby all physician owners left the practice and its original owner to form a competing practice; a non-compete was not in place.

Calculation of damages to a practice whereby the sale price of the practice was inflated due to upcoding of evaluation and management codes prior to the sale.

Conclusion

In the intricate landscape of disputes, divorces, and damages, navigating the complexities can be a daunting challenge. VMG Health understands the toll these situations may take both emotionally and financially. When faced with these difficult situations, it is crucial to entrust your needs to valuation experts aligned with your needs. VMG Health provides valuation and damages guidance through these litigated and dispute resolution matters.

Sitting Down with Our Industry Experts: Regina Boore

March 28, 2024

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

1. Can you provide a high-level overview of what you spoke about at Caribbean Eye?

I was part of a panel discussion called, “Regulatory Compliance and Insurance Trends for ASCs.” Representing Progressive Surgical Solutions (PSS): A Division of VMG Health, I focused on two new regulatory issues in the ambulatory surgery center (ASC) space: the new water quality standard and putting together a whole program for water quality inspection, testing, and maintenance requirements throughout the year; and then I gave an update on Medicare’s mandatory quality reporting requirements for surgery centers.

The big thing that I focused on is the Outpatient Ambulatory Surgery Consumer Assessment of Healthcare Providers and Systems (OAS CAHPS) requirement, which is now 34 questions. This assessment will be mandatory as of January 1, 2025, and ASCs must work with a vendor approved by the Centers for Medicare & Medicaid Services (CMS). There are only so many CMS-approved vendors, and there are thousands of surgery centers, so it’s important to get on it and decide which vendor you’re going to work with, and then start the implementation process.

2. What do you think the audience was the most surprised to learn from your presentation?

I think many people were just unaware of this new water quality standard, and I don’t think they had a good grasp on what is involved in administering this survey. ASCs must work through one of the CMS-approved vendors, and there is a process to getting set up to be able to implement it.

3. How do you think your presentation helped healthcare leaders better prepare for challenges?

Knowledge is key. Many attendees took pictures of my slides, and I provided resources for them to find the most updated information of the OAS CAHPS program. It was imperative to give them that knowledge and empower them to stay a step ahead as the new requirements are implemented.

4. What resources would you suggest for those interested in learning more?

Our eSupport membership program contains a wide array of resources. The PSS team has intimate knowledge of ASC operations from years of hands-on experience. We constantly update eSupport so ASCs can remain compliant, successful, and confident—even when regulations change.

To dive into the continued evolution of ASCs, check out VMG Health’s ASCs in 2023: A Year in Review article, which includes everything from market dynamics to provider reimbursement.

5. If someone takes only one message from your presentation, what would you want it to be?

Be prepared. The downside of being unprepared with this water management program is that you could get a deficiency citation on a survey, announced or unannounced. As for the OAS CAHPS survey, if an ASC fails to submit the required number of surveys in 2025, it will be hit with a 2% penalty on its Medicare reimbursement in 2027. Both situations should be avoided at all costs, and staying prepared is key.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.

What You Need to Know About Medical Transport and Fair Market Value

March 27, 2024

Written by Alex Wiederin, CVA and Nicole Montanaro, CVA

Over the past few years, the medical transport industry has experienced constant growth, which is projected to continue into the foreseeable future. This growth can be attributed mainly to the increasing number of vehicle accidents, the growing elderly population, and medical tourism. As part of this trend, medical transport arrangements with hospitals have come under increased scrutiny from regulators as it relates to fair market value and compliance.

When entering into a medical transport arrangement with a third-party provider, it is important for hospitals to understand what services are being provided, the reimbursement environment for medical transports, and the impact of any compliance issues. Services are often provided not just by the medical transport vendor, but also by the hospital, which may offer services to the medical transport vendor as well. From a compliance perspective, fees for both sets of services should be at fair market value (FMV). Based on VMG Health’s extensive experience in valuing medical transport arrangements, we have outlined some fundamental questions to help hospitals/facilities understand the elements of their arrangement and determine which services need to be valued.

Which transports are covered by Medicare? The Medicare Ambulance Fee Schedule (AFS) lists the levels of ambulance service that are covered under Medicare Part B. The Medicare AFS payment structure is a base rate plus a mileage rate. Reimbursement is tied to the particular level of service transport provided and includes compensation for staff, vehicle, equipment, and supplies. The rates are updated annually and adjusted by locality. Please see the chart below for the list of HCPCS codes included in the Medicare AFS and the corresponding level of service.

HCPCS Code

Level of Service Description

A0425

Ground Mileage – Loaded per mile

A0426

Advanced Life Support I – Non-emergency

A0427

Advanced Life Support I – Emergency

A0428

Basic Life Support – Non-emergency

A0429

Basic Life Support – Emergency

A0430

Fixed Wing Transport

A0431

Rotor Wing Transport

A0432

Paramedic Intercept

A0433

Advanced Life Support II

A0434

Specialty Care Transport

A0435

Fixed Wing Mileage

A0436

Rotor Wing Mileage

What transports are not covered by Medicare? The Medicare AFS does not have an analogous Medicare HCPCS code for all transport types; therefore, contracted rates for these transports cannot be tied to the Medicare AFS. Some examples of transports not covered by the Medicare AFS are non-emergency transports (ambulatory, wheelchair, and stretcher), bariatric transports, and ride-share services. These types of transports are most commonly used to assist patients by getting to and from their medical appointments, discharges from the hospital, and transports between facilities. The ride-share services are fairly new to the medical transport market but are expected to make a significant impact by offering lower-cost rides, allowing the patient to schedule their own rides, and by reducing the number of missed medical appointments. Transports not covered by the Medicare AFS should be valued to ensure compensation aligns with FMV.

What additional services are provided in the arrangement? Medical transport agreements can be tailored to the specific needs of each hospital or facility, usually associated with the provision of specialty care transports (neonatal, pediatric, and/or high-risk obstetrics). In some cases, the transport vendor can be contracted for exclusive transport services and/or the hospital or facility can provide support services to assist the transport vendor in providing the transports. These support services can include the provision of staff, medical supplies, medical equipment, program management, business outreach, medical direction, helipad, crew quarters, and branding. Generally, compensation for these additional services cannot be tied to the Medicare AFS and would need to be valued separately to ensure the fees are consistent with FMV.

Which party is financially responsible for the transports provided in the arrangement? One of the most frequently asked questions related to medical transports is, Who is paying for the transport? The answer to this question ultimately depends on what the transport is for and where is the patient going. Medically necessary transports to a hospital, critical access hospital (CAH), or a skilled nursing facility (SNF) are typically covered by Medicare Part B. For Medicare Part B transports, the transport vendor should seek payment from the patient or the patient’s insurance. However, a patient admitted to a hospital, CAH, or SNF may require transportation to another level or site of care as an inpatient. Reimbursement for these transports is generally included in Medicare Part A payments to the hospital/facility. For Medicare Part A transports, the transport vendor can seek payment from the hospital, CAH, SNF, or the entity that received the Medicare Part A payment.

What are the FMV/compliance risks associated with medical transport? With medical transport arrangements being under close watch by regulators, it is important to understand the risks around these types of arrangements. Some factors that can lead to noncompliant arrangements include oral arrangements, old contracts, transports not medically necessary, fees not covering the costs of the service, and “swapping.” One of the biggest compliance risks associated with medical transport arrangements is the risk of swapping. Swapping occurs when a transport vendor agrees to provide below-market (or sometimes below-cost) transports to the hospital or facility in exchange for sending the more lucrative transports covered by Medicare, other governmental payors, or commercial payors. To mitigate these factors, review the services provided by both parties, identify the transport direction (i.e., transports to or from the hospital or facility), tie fees to the Medicare AFS when possible, and watch out for services being provided for free or at a discount.

Medical transportation plays a critical and necessary role in the healthcare industry. Arrangements for medical transportation services can be extremely complex. VMG Health has extensive experience valuing payments for all kinds of medical transport arrangements and understands the numerous risks associated with these types of valuations, which helps clients enter arrangements compliant with FMV.

Proceed with Caution: Five Key Considerations in Quality of Revenue Analysis

March 20, 2024

Written by Melissa Hoelting, CPA and Lukas Recio, CPA

In healthcare-related mergers and acquisitions (M&A), quality of revenue analysis represents both the most vital piece of due diligence and its most unique aspect given the nature of healthcare revenue. For many transactions, buyers rely on due diligence advisors to provide independent net revenue hindsight analyses to facilitate valuation efforts, such as growth potential, risk analysis, and financial stability. Quality of revenue analysis becomes even more crucial in healthcare transactions due to the added complexity of payor contracting and unique reimbursement mechanisms by vertical. Due to this complexity, investors and advisors need to know the key indicators that arise in quality of revenue analysis to address the issues and properly assess the merits of the transaction. In this article, our financial due diligence team previews five key considerations:

1. Payor Concentration

When revenues are concentrated with a select few payors, there is potential for future revenue loss from either unfavorable reimbursement rate changes or the loss of in-network status. Even minor changes in reimbursement rates may have a material impact on top-line revenue when applied to key groups. A key consideration when evaluating payor concentration comes from a large reliance on government payors, as the rates can change year to year without the company’s input or control. Payor concentration in and of itself will not impact the revenue hindsight analysis, as collections for previous dates of service will follow the current contracts, but investors and their advisors should make it a priority to understand the payor mix to properly identify and assess the inherent risks. Additionally, any upcoming contract negotiations should be discussed to evaluate the potential near-term impact of negative price adjustments to make necessary pro forma/forecasting assumptions.

2. Increasing Days Sales Outstanding (DSO)

Aging accounts receivable balances indicate difficulties in the billing and/or collection process, which directly impact the company’s cash flows and the reliability of reported revenues for companies on an accrual basis. Increasing DSO could be the result of certain non-recurring events, such as the loss of key personnel in the billing department or converting revenue cycle management systems, or may be indicative of deeper issues at play within the company. In the case of third-party payors, increased DSO could point to two potential issues:

Disputes with payors, or

Insufficient collections of copays, coinsurance, or deductibles. If it is discovered that increased DSO for certain third-party payors stems from remaining patient responsibility, the company could be under-collecting copays, coinsurance, and deductibles at the time of service. This misstep in the collection process can leave a company exposed to an accounts receivable balance overly weighted toward patient balances, which can be more difficult to collect.

Regardless of the payor type exhibiting increased DSO, decrease in collection speed should always alert the investment team that more analysis and discussion is required to properly determine the collectability of accounts receivable, and thus, the revenue accruals themselves.

3. Reconciliation Irregularities

Revenue analysis fundamentally begins with a reconciliation of the payment data to the bank statements to anchor the data to verifiable cash inflows. Variances between collections from the billing system and bank statement deposits could indicate that the company does not deposit all collections, certain revenue streams do not run through the billing system, or there are significant delays in posting cash receipts to the billing system. By comparing the reported revenue to the bank statements, teams can identify overstatements of revenue that are not supported by bank deposits. Regardless of the variance’s cause, any discrepancies should be investigated and discussed with management to ensure data completeness and integrity before using the billing system reports for any revenue analysis.

4. Variability in Gross-to-Net Ratios

An entity’s gross-to-net ratios (net collections as a percentage of total gross charges) often highlight changes in underlying processes or outcomes for a given period of service; therefore, they are a key consideration during the due diligence process. Effective gross-to-net ratio analysis starts at the lowest level, such as by CPT code by payor. Significant variations at this level from month to month or quarter to quarter may indicate rate changes, an altered chargemaster, or increased/decreased denial activity. At a less detailed level, changes in this ratio may also illustrate changes in payor mix or procedure mix. In any case, the underlying drivers must be identified and their impact to future cash flows assessed to determine the true quality of the underlying revenue streams.

5. Billing and Coding Irregularities

A foundational component in the revenue recognition process, the billing and coding process can be the area most susceptible to downside surprise. Investors and their advisors should focus on CPT code-level trending to determine key metrics, such as payment per code and code distribution. By comparing these metrics to contracted rates and industry or specialty norms, irregularities in coding practice can be identified and investigated. For example, if an organization has higher concentration in level one or level five evaluation and management codes, it could indicate consistent undercoding to avoid payor scrutiny or overcoding for work performed, respectively. On a similar note, if an organization receives similar reimbursement on office visit codes for a doctor and a mid-level provider, it could indicate that the billing team is not coding and charging the proper rates. Identified irregularities in the coding metrics should be discussed in detail, as inappropriate coding can result in downward adjustments to both historical collections and any outstanding collections, as well as takebacks owed to insurance companies for prior periods.

Conclusion

For any healthcare transaction, revenue analysis remains the most essential and most complicated part of the diligence process. Because of the payor contracts that underpin most healthcare revenues, investment teams must identify any variances in reimbursement, charges, and coding that could indicate errors or changes in the billing process. When considering adjustments or estimating future collections, teams must consider the changes and errors they have identified through these variances. These five considerations represent just a portion of the potential intricacies and issues that arise during quality of revenue analysis. Thus, an organization looking to enter into a transaction, whether on the buy-side or the sell-side, would benefit from the services of a financial due diligence and/or coding and compliance firm to bring an additional layer of confidence to the target’s revenues.

Supply-Side Constraints and Operational Headwinds in Skilled Nursing Valuation

March 19, 2024

Written by Grace McWatters, Danny Cuellar, Carlos Flores-Rodriguez, Blake Pierro, and Cameron Tolbert

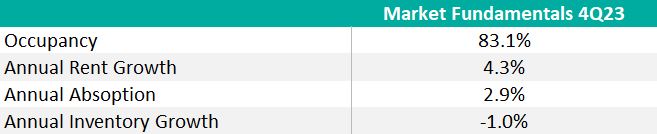

Inflation, a shaky supply chain, and rate hikes have extended production schedules and increased the cost and risk associated with developing new skilled nursing facilities. While new supply is constrained, existing nursing facilities grapple with staffing shortages and weak reimbursements. Despite positive chatter about recovering occupancy, rent growth, and a looming “silver tsunami” of retirees, the industry sits in a precarious position.

The inflated cost to build, buy, and operate skilled nursing facilities has led to a downward pressure on valuations. This affects the risk profile of the sector, both from a regulatory risk perspective (in the context of joint ventures or lease renewals, for instance) and from an underwriting or acquisition/disposition perspective (due to the elevated cost of debt combined with rising operating costs).

Strong Demand, Weak Performance

Strong demand for skilled nursing facilities is primarily driven by an aging populace in the United States; over the next 10 years, the 75+ population is projected to grow by 44%. According to research funded by the National Investment Center for Seniors Housing & Care, 60% of this population will have mobility limitations, with 20% requiring high healthcare or functional needs.

Cushman and Wakefield predict consumer demand for senior housing and care facilities, including independent living, assisted living, memory care, and skilled nursing, will overwhelm the market within the next five years. It would take approximately 3,100 new skilled nursing facilities by 2030, or about 500 net openings annually, to meet the forecasted need. Despite robust demand, skilled nursing inventory fell 1% in 2023.

Over the last year, closures continually outpaced openings as financial pressures from inflation, poor reimbursement rates, and staffing shortages led to industry-wide “right sizing” to control cost and mitigate labor shortages. For example, in 2022 and 2023 when labor shortages became a flashpoint, operators, bound by minimum staffing requirements, had to consider contract labor. The contract nursing labor utilization increased 56% in 2022, which “equates to approximately $400,000 in additional costs for the average facility in the country.” Average overall nursing wages increased 10.6% in 2022, a much faster clip than revenue growth.

These cost surges came at a price, and without a mechanism to raise prices, taking beds offline was often inevitable. The American Health Care Association surveyed thousands of skilled nursing facilities in an August 2023 report and found that 21% of homes are downsizing beds or units, and 24% have closed a wing, unit, or floor because of the labor shortages.

Since 2020, an estimated 579 facilities have closed (approximately 162 per year, over the 43-month period), and 38% of these closures were 4- or 5-star rated facilities. Only three skilled nursing facilities opened in 2023, down significantly from an average of 64 openings in both 2020 and 2022.

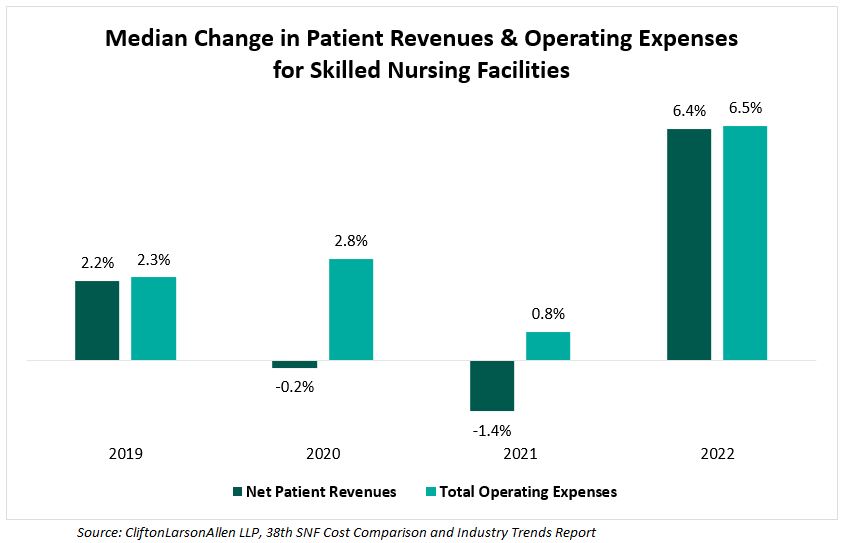

The tight supply has supported rent growth and occupancy recovery across the industry, but these gains have been outpaced by increased costs for staffing and supplies, exacerbating structural forces specific to the industry. From 2019 to 2022, Clifton Allen Larson analyzed cost reports for 10,500 facilities (nearly two-thirds of all Medicare-certified SNFs in the country) and found that expenses have consistently grown faster than revenues.

Operating expense growth in other industries can be mitigated by “shrinkflation” or higher prices, but in healthcare, providers cannot ethically reduce the amount of care administered, nor can they regularly renegotiate their contracts and expect immediate increases in Medicare reimbursements.

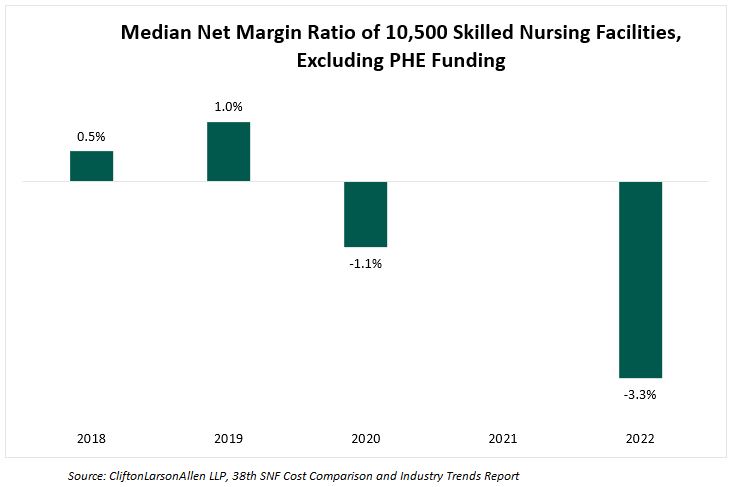

In 2023, Clifton Larson Allen analyzed cost reports of 10,500 nursing facilities and found a significant downward trend in the median net margin ratio since 2020. This ratio measures a facility’s efficiency in controlling costs in relation to its total revenue by comparing net income or loss to total revenue.

Heightened Risk, Lower Reward

Construction for new facilities has dwindled since 2020, as high interest rates and inflation have developers wary. Costs are rising, but market valuations have not necessarily followed, which means developers would take on more risk for potentially less reward. These factors have decreased the overall incentive for developers to initiate new projects. When analyzing the all-in construction costs of 142 senior housing developments in 2022, CBRE reported the average cost had increased 17.8% per unit since 2020, clarifying that this increase “is largely attributable to higher labor and materials costs, as well as operating expenses and outlays for entitlements.”

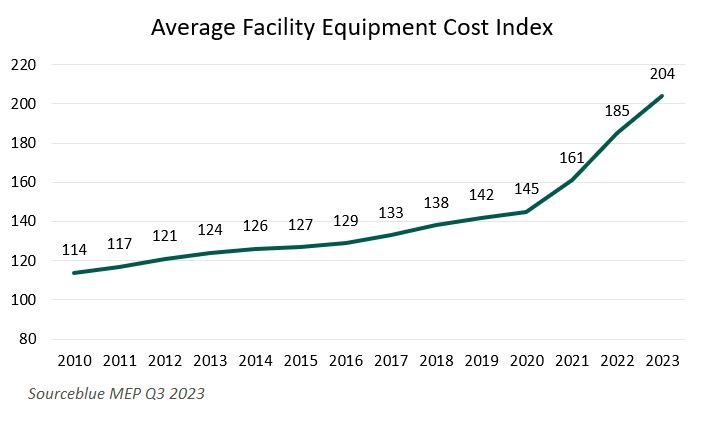

This is mostly attributable to hard cost increases, but there were significant increases in soft costs and FF&E costs as well. Hard costs, which include site work, foundation, shell, and finishes, increased 24% per revenue unit (i.e., per bed) since 2020. Soft costs, which can cover architect and design fees, permitting and inspection fees, rose 14% per unit, and FF&E bumped up 10% per unit . Similarly, an index based primarily on mechanical and electrical equipment in new construction showed a significant uptick in their average cost in 2022 (increased by 15.1%) and 2023 (increased by 10.4%).

While FF&E represents a small part of the overall senior care development budget (CBRE estimates 3% overall) , any transactions and leases involving FF&E at senior living and care facilities are subject to regulatory scrutiny, just like real property.

Those willing to take the risk of building a new facility find it difficult to acquire capital in the wake of rate hikes and bank failures in the broader economy. A significant amount of funding for the purchase of senior living and care assets originates from commercial bank loans, but lending grew scarce following the failings of Silicon Valley Bank and Signature Bank in March 2023.

As other banks teetered on the edge of bankruptcy and commercial bank stocks dropped up to 50%, banks began to stop the flow of lending, and instead focused on cleaning up their balance sheets. Preserving limited capital, banks began to raise interest rates and stiffen security terms for available loans. This folded into rising rates on a larger macroeconomic scale, as the Federal Reserve hiked their rates to curb inflation, increasing interest rates by 525 basis points in 2022 and 2023.

Higher interest rates lend themselves to higher projected operating costs of acquired facilities. This increase in operating costs has been offset by a substantial decrease in purchasing prices. Cain Brothers reported a 20–30% decrease in skilled nursing facility valuations since the beginning of 2023, citing several deals in their report, including a New York facility that declined in value 47% in less than two years, and a Kentucky facility that dropped 28% in less than one year. Haven Senior Investments notes valuation declines between 15% and 30% but emphasizes the influence of factors like rising property taxes and insurance premiums, as well as the portfolio penalty.

Regulatory Implications

The inflationary environment combined with longer-term industry headwinds continue to place pressure on the senior living and skilled nursing industry. Over the last two years, the cost of capital has increased, and commercial loans have become less available, making it more expensive and time consuming to acquire the funds necessary for new developments or strategic acquisitions. Operating costs continue to outpace revenue growth, and the median net margin ratio for two-thirds of the country’s facilities was negative 3.3% in 2022. This environment has contributed to rising capitalization rates and downward pressure on valuations.

The decline in skilled nursing facility valuations has increased the industry’s risk profile, both from a regulatory risk perspective and from an underwriting or acquisition/disposition perspective. The turbulent market conditions over the last 18 months have created a need for increased diligence when developing, buying, or selling senior living assets. However, long-term demographic trends will continue to drive transaction activity in the sector, as market participants seek solutions to address demand in the face of rising costs and increased cost of capital.

Sources

Beets, K., Ferroni, L. (2024). Seniors Housing & Care Investor Survey and Trends. JLL. https://www.us.jll.com/en/trends-and-insights/research/seniors-housing-care-investor-survey-and-trend-outlook

Pearson, C., et. al. (2019). The Forgotten Middle: Many Middle-Income Seniors Will Have Insufficient Resources For Housing And Health Care. HealthAffairs. https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2018.05233

Boywer, Z. (2023). Investor Survey and Trends Report: U.S. Senior Living & Care. Cushman & Wakefield. https://www.cushmanwakefield.com/en/united-states/insights/senior-living-and-care-investor-survey-and-trends-report

Shuman, T. (2023). How Will America’s “Silver Tsunami” Impact Demand for Nursing Homes? Seniorliving.org. https://www.seniorliving.org/nursing-homes/nursing-home-demand-projections/

Vison, N. (2024). 4Q23 Market Fundamentals. NIC MAP Vision. https://info.nicmapvision.com/rs/016-QJL-848/images/4Q23-NIC-MAP-Market-Fundamentals-PDF.pdf

Connect, C. (2024). 38th SNF Cost Comparison and Industry Trends Report: One Industry, Thousands of Stories. CLA. https://www.claconnect.com/en/resources/white-papers/snf-cost-comparison-industry-trends-report

Vance, M., et. al. (2022). 2022 Seniors Housing Development Costs. Intelligent Investment. https://www.cbre.com/insights/reports/2022-seniors-housing-development-costs

SourceBlue. (2023). 2023 MEP Cost Index Q4. https://media.licdn.com/dms/document/media/D4E1FAQFQj5FKBkLXVg/feedshare-document-pdf-analyzed/0/1705173887049?e=1711584000&v=beta&t=FlP19mqHb4j8iSVBePK8gHaWLHauSTUgdorcMH2TTlg

Goldreich, M. (2023). 2023 Debt Capital Markets Impact on Senior Living Asset Valuation. Cain Brothers Industry Insights. https://www.key.com/content/dam/kco/documents/businesses___institutions/Industry_Insights_11.15.23.pdf

Investments, H. (2023). The Present and Future of Senior Living Sector Acquisitions. Haven Senior Investments. https://havenseniorinvestments.com/downloadable/the-present-and-future-of-senior-living-sector-acquisitions/