Navigating Value-Based Care: Insights from Nicole Montanaro at the ABA Emerging Issues in Healthcare Law Conference

May 2, 2024

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

1. Can you provide a high-level overview of what you spoke about at the American Bar Association Emerging Issues in Healthcare Law Conference?

I spoke with King and Spalding attorney Kim Roeder on different, hot-button issues that arise when structuring and valuing different value-based arrangements. It started off as a presentation of different case studies and focused on what Roeder has encountered from a legal perspective and what I have encountered from a valuation perspective. We often receive questions when it comes to structure or even value drivers, and we wanted to present solutions to what we saw or clients struggling with so that they could develop a better understanding of them.

2. What do you think the audience was the most surprised to learn from your presentation?

The focus on the metrics themselves and how carefully they need to be considered seemed to be the most surprising. Recent regulations have been really focused on metrics, and that’s what we get the most questions about. I think our audience was also surprised to learn that Kim had experienced those questions as well, and metrics aren’t just a consideration on the valuation perspective. Both legal and valuation perspectives must carefully consider metrics.

3. How do you think your presentation helped healthcare leaders better prepare for challenges?

Our presentation was a very pragmatic way of illustrating six key issues that often come up during valuation. It’s a great resource for healthcare leaders to reference as they go through and check the boxes to ensure they have thought through all of the considerations that we often see as eleventh-hour issues.

4. What resources would you suggest for those interested in learning more?

I co-wrote a section of the 2023 Physician Alignment: Tips and Trends Report that discusses quality incentives for providers. It captures key factors to consider, from a valuation perspective, when looking to enter value-based arrangements and where to start.

5. If someone takes only one message from your presentation, what would you want it to be?

Value-based arrangements require a very orchestrated balance between legal and compliance, operational champions, and valuation teams. Operational teams should be able to focus on what changes and improvements they want to implement, valuation teams must have an understanding of those goals, and legal and compliance must be involved to ensure the approach is appropriate and compliant. Without cohesion between these three groups, we see those eleventh-hour issues pop up.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.

Hospitals and health systems have been developing strategies for vertical integration with physician groups for decades. Through the premise of integrated care delivery, “defined as a coherent set of methods and models on the funding, administrative, organizational, service delivery and clinical levels,” U.S. policymakers, healthcare operators and payors expect to improve the quality, service and efficiency of healthcare services. Results of value generated through integrated delivery models are mixed, and the operating model is often confounded with varying market dynamics (payor concentration, culture, physician supply/demand, leadership, etc.) by community.

Regardless of integrated care delivery success, health system employment continues to increase and today accounts for greater than 50% of all practicing physicians. Interestingly and unknown to many, other strategics (private equity, Optum, CVS, etc.) account for approximately another 25%, leaving approximately a quarter of physicians organized in a private practice.

Figure 1: 2023 Physician Employment by Type

Source: Physicians Advocacy Institute: Physician Practice Trends Specialty Report

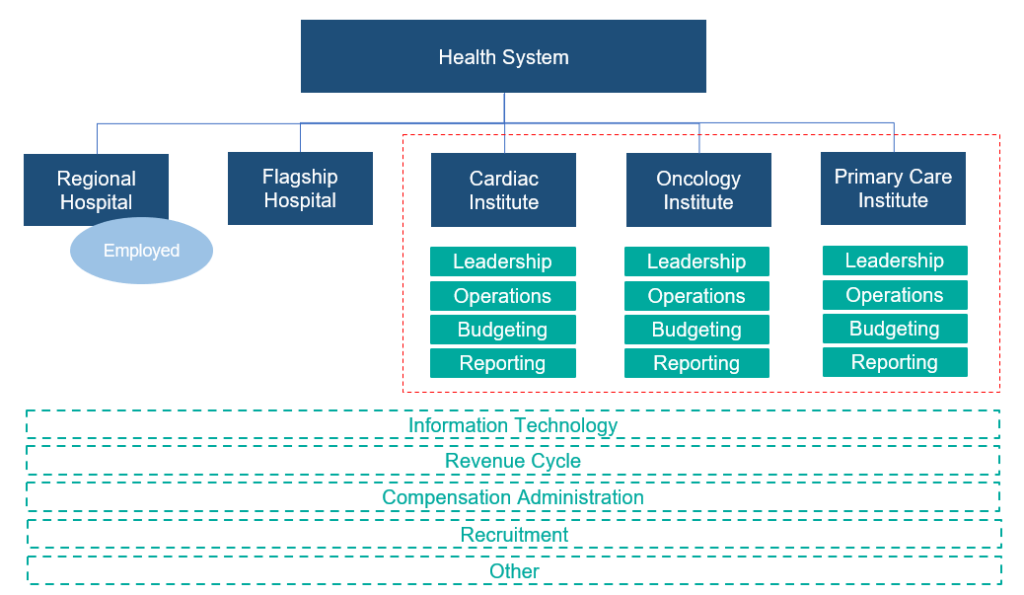

Across many integrated delivery systems, physicians are organized under a formal medical group structure, often with supporting leadership, governance, and practice management systems. This structure essentially groups the collective interests of primary care, surgical subspecialists, medical subspecialists, and hospital-based physicians together. Unlike independent, multispecialty practices who have an underpinning of sharing economics, most multispecialty groups in integrated delivery systems lack material financial alignment across subspecialties.

To this end, there are several challenges with a multispecialty group structure in health systems, including an aggregation of physician losses whereby various revenue streams (e.g., in-office ancillaries) have been integrated with hospital operations, sensitivity to practice losses based on confounding facts as to the true operating performance, silo board and/or decision making, and frustration by large clinical service lines due to widely held convention that everything needs to be the same for all physicians across the physician enterprise. Figure 2 outlines the most prevalent medical group structure and its multispecialty orientation.

Figure 2: Prevalent Medical Group Structure for Employed Physicians

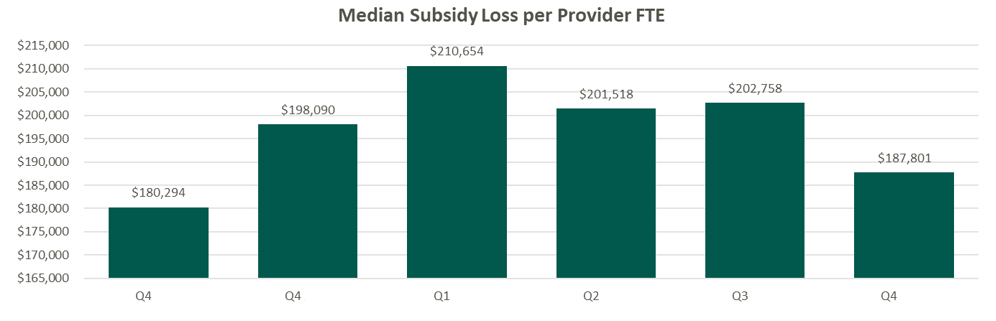

Financial system reporting remains inconsistent across organizations; however, there are data repositories that suggest continued median subsidies for employed providers. As figure 3 outlines, regardless of timing and/or subspecialty orientation, there remains a significant net investment per provider.

Figure 3: Median Subsidy (Combined Subspecialty Mix)

Source: Kaufman Hall Flash Reports

Based on VMG Health’s experience, significant financial reporting subsidies lead to suboptimized decision making, as significant pressure is placed on medical group leadership to reduce practice losses and improve overall practice performance. This has led to a variety of strategic missteps for organizations operating in competitive markets.

As an alternative, VMG Health has been working with clients to reorganize physician enterprise offerings inside of integrated delivery systems, including the development of financial reporting, management, and governance systems that better align care delivery across service lines. These more contemporary structures, while variable system to system, are all designed to:

Boost physician loyalty to their primary clinical practice location (e.g., office based, value-based orientation, hospital, ASC, etc.).

Improve leadership, financial reporting, and budgeting so that business units are accountable for both facility- and professional-level operations and key performance indicators.

Afford focus on best-in-class infrastructure to support all professional practice applications.

Remove silo barriers and outdated concepts of medical group subsidies and associated strategic implications from an antiquated structure.

Figure 4: Contemporary Medical Group Structure

Conclusion

The landscape of physician organizational structures within hospitals and health systems remains in transition. While traditional, multispecialty group practice models remain prevalent, challenges such as physician losses and inconsistent financial reporting have spurred the need for more contemporary structures. Through strategic reorganization and improved governance, health systems can enhance physician loyalty, accountability, growth, and operational efficiency, ultimately optimizing care delivery and aligned (or improved) financial performance.

Sources

Heeringa, J., et. al. (2020). Horizontal and Vertical Integration of Health Care Providers: A Framework for Understanding Various Provider Organizational Structures. National Library of Medicine. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC6978994/

Sitting Down with Our Industry Experts: Andrew Maller

April 17, 2024

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

1. Can you provide a high-level overview of what you spoke about at the American Society of Ophthalmic Administrators/American Society of Cataract and Refractive Surgery Annual Meeting?

The course itself, Physician Compensation Trends for Employed and Owner Providers, had two main focal points. We discussed current compensation and benefits trends for employed providers in group practices, as well as tips for assessing the feasibility of adding new providers in today’s challenging recruitment environment. We also discussed common income and expense sharing models for owner providers in group practices.

2. What do you think the audience was the most surprised to learn from your presentation?

The biggest surprise for attendees was just how competitive the current recruitment environment is for practices looking to hire new providers. There truly is a supply and demand imbalance, meaning that there are more practices looking to hire providers than there are available ophthalmologists looking for positions. The combination of this challenge with influences from private equity–backed companies has resulted in higher, guaranteed starting salaries for providers on the job market.

All of this is happening while practices are facing declining reimbursement and ever-increasing operating expenses, making the challenging decision to hire a new provider even more complicated.

Many practices I work with feel that this is a challenge to them specifically, based on geography or practice situation. However, the reality is that ophthalmic practices across the country are all struggling to recruit.

3. How do you think your presentation helped healthcare leaders better prepare for challenges?

One of the key topics of discussion focused on developing a thorough feasibility analysis when determining whether the timing is right to hire a new provider. Practices can exponentially increase their likelihood of making the right decision by taking a disciplined approach in assessing the revenue opportunity for the new provider, their estimated compensation, and other incremental overhead costs. The hiring decision should not be made based on a gut feeling, but instead through a review of objective data points given the potential positive (or negative) impact to the practice.

4. What resources would you suggest for those interested in learning more?

BSM Connection for Ophthalmology has a several fantastic resources for practices in the recruitment process, including the New Provider Feasibility Analyzer and the Key Contract Considerations Guide for ophthalmologists and optometrists, which provide guidance on compensation and benefit trends. The Provider Recruitment section of the website also includes a Contract Review Worksheet and a sample Letter of Understanding, although we always recommend practices work with legal counsel to ensure appropriate documentation is completed.

For information regarding income and compensation models, our experts have written articles related to income-sharing models for group practices. VMG Health also offers a Provider Needs Assessment.

5. If someone takes only one message from your presentation, what would you want it to be?

With all areas of practice management, leaders must make business decisions using a disciplined approach. That starts with being educated and realizing the challenges that exist right now when it comes to provider recruitment.

As it relates to owner income and expense-sharing models, the takeaway is the need for transparency. Practice administrators and executives are often the ones charged with administering the compensation model, so the key is to remain neutral and transparent throughout the entire process.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.

Sitting Down with Our Industry Experts: Regina Boore

March 28, 2024

At VMG Health, we’re dedicated to sharing our knowledge. Our experts present at in-person conferences and virtual webinars to bring you the latest compliance, strategy, and transaction insight. Sit down with our in-house experts in this blog series, where we unpack the five key takeaways from our latest speaking engagements.

1. Can you provide a high-level overview of what you spoke about at Caribbean Eye?

I was part of a panel discussion called, “Regulatory Compliance and Insurance Trends for ASCs.” Representing Progressive Surgical Solutions (PSS): A Division of VMG Health, I focused on two new regulatory issues in the ambulatory surgery center (ASC) space: the new water quality standard and putting together a whole program for water quality inspection, testing, and maintenance requirements throughout the year; and then I gave an update on Medicare’s mandatory quality reporting requirements for surgery centers.

The big thing that I focused on is the Outpatient Ambulatory Surgery Consumer Assessment of Healthcare Providers and Systems (OAS CAHPS) requirement, which is now 34 questions. This assessment will be mandatory as of January 1, 2025, and ASCs must work with a vendor approved by the Centers for Medicare & Medicaid Services (CMS). There are only so many CMS-approved vendors, and there are thousands of surgery centers, so it’s important to get on it and decide which vendor you’re going to work with, and then start the implementation process.

2. What do you think the audience was the most surprised to learn from your presentation?

I think many people were just unaware of this new water quality standard, and I don’t think they had a good grasp on what is involved in administering this survey. ASCs must work through one of the CMS-approved vendors, and there is a process to getting set up to be able to implement it.

3. How do you think your presentation helped healthcare leaders better prepare for challenges?

Knowledge is key. Many attendees took pictures of my slides, and I provided resources for them to find the most updated information of the OAS CAHPS program. It was imperative to give them that knowledge and empower them to stay a step ahead as the new requirements are implemented.

4. What resources would you suggest for those interested in learning more?

Our eSupport membership program contains a wide array of resources. The PSS team has intimate knowledge of ASC operations from years of hands-on experience. We constantly update eSupport so ASCs can remain compliant, successful, and confident—even when regulations change.

To dive into the continued evolution of ASCs, check out VMG Health’s ASCs in 2023: A Year in Review article, which includes everything from market dynamics to provider reimbursement.

5. If someone takes only one message from your presentation, what would you want it to be?

Be prepared. The downside of being unprepared with this water management program is that you could get a deficiency citation on a survey, announced or unannounced. As for the OAS CAHPS survey, if an ASC fails to submit the required number of surveys in 2025, it will be hit with a 2% penalty on its Medicare reimbursement in 2027. Both situations should be avoided at all costs, and staying prepared is key.

Our team serves as the single source for your valuation, strategic, and compliance needs. If you would like to learn more about VMG Health, get in touch with our experts, subscribe to our newsletter, and follow us on LinkedIn.

What You Need to Know About Medical Transport and Fair Market Value

March 27, 2024

Written by Alex Wiederin, CVA and Nicole Montanaro, CVA

Over the past few years, the medical transport industry has experienced constant growth, which is projected to continue into the foreseeable future. This growth can be attributed mainly to the increasing number of vehicle accidents, the growing elderly population, and medical tourism. As part of this trend, medical transport arrangements with hospitals have come under increased scrutiny from regulators as it relates to fair market value and compliance.

When entering into a medical transport arrangement with a third-party provider, it is important for hospitals to understand what services are being provided, the reimbursement environment for medical transports, and the impact of any compliance issues. Services are often provided not just by the medical transport vendor, but also by the hospital, which may offer services to the medical transport vendor as well. From a compliance perspective, fees for both sets of services should be at fair market value (FMV). Based on VMG Health’s extensive experience in valuing medical transport arrangements, we have outlined some fundamental questions to help hospitals/facilities understand the elements of their arrangement and determine which services need to be valued.

Which transports are covered by Medicare? The Medicare Ambulance Fee Schedule (AFS) lists the levels of ambulance service that are covered under Medicare Part B. The Medicare AFS payment structure is a base rate plus a mileage rate. Reimbursement is tied to the particular level of service transport provided and includes compensation for staff, vehicle, equipment, and supplies. The rates are updated annually and adjusted by locality. Please see the chart below for the list of HCPCS codes included in the Medicare AFS and the corresponding level of service.

HCPCS Code

Level of Service Description

A0425

Ground Mileage – Loaded per mile

A0426

Advanced Life Support I – Non-emergency

A0427

Advanced Life Support I – Emergency

A0428

Basic Life Support – Non-emergency

A0429

Basic Life Support – Emergency

A0430

Fixed Wing Transport

A0431

Rotor Wing Transport

A0432

Paramedic Intercept

A0433

Advanced Life Support II

A0434

Specialty Care Transport

A0435

Fixed Wing Mileage

A0436

Rotor Wing Mileage

What transports are not covered by Medicare? The Medicare AFS does not have an analogous Medicare HCPCS code for all transport types; therefore, contracted rates for these transports cannot be tied to the Medicare AFS. Some examples of transports not covered by the Medicare AFS are non-emergency transports (ambulatory, wheelchair, and stretcher), bariatric transports, and ride-share services. These types of transports are most commonly used to assist patients by getting to and from their medical appointments, discharges from the hospital, and transports between facilities. The ride-share services are fairly new to the medical transport market but are expected to make a significant impact by offering lower-cost rides, allowing the patient to schedule their own rides, and by reducing the number of missed medical appointments. Transports not covered by the Medicare AFS should be valued to ensure compensation aligns with FMV.

What additional services are provided in the arrangement? Medical transport agreements can be tailored to the specific needs of each hospital or facility, usually associated with the provision of specialty care transports (neonatal, pediatric, and/or high-risk obstetrics). In some cases, the transport vendor can be contracted for exclusive transport services and/or the hospital or facility can provide support services to assist the transport vendor in providing the transports. These support services can include the provision of staff, medical supplies, medical equipment, program management, business outreach, medical direction, helipad, crew quarters, and branding. Generally, compensation for these additional services cannot be tied to the Medicare AFS and would need to be valued separately to ensure the fees are consistent with FMV.

Which party is financially responsible for the transports provided in the arrangement? One of the most frequently asked questions related to medical transports is, Who is paying for the transport? The answer to this question ultimately depends on what the transport is for and where is the patient going. Medically necessary transports to a hospital, critical access hospital (CAH), or a skilled nursing facility (SNF) are typically covered by Medicare Part B. For Medicare Part B transports, the transport vendor should seek payment from the patient or the patient’s insurance. However, a patient admitted to a hospital, CAH, or SNF may require transportation to another level or site of care as an inpatient. Reimbursement for these transports is generally included in Medicare Part A payments to the hospital/facility. For Medicare Part A transports, the transport vendor can seek payment from the hospital, CAH, SNF, or the entity that received the Medicare Part A payment.

What are the FMV/compliance risks associated with medical transport? With medical transport arrangements being under close watch by regulators, it is important to understand the risks around these types of arrangements. Some factors that can lead to noncompliant arrangements include oral arrangements, old contracts, transports not medically necessary, fees not covering the costs of the service, and “swapping.” One of the biggest compliance risks associated with medical transport arrangements is the risk of swapping. Swapping occurs when a transport vendor agrees to provide below-market (or sometimes below-cost) transports to the hospital or facility in exchange for sending the more lucrative transports covered by Medicare, other governmental payors, or commercial payors. To mitigate these factors, review the services provided by both parties, identify the transport direction (i.e., transports to or from the hospital or facility), tie fees to the Medicare AFS when possible, and watch out for services being provided for free or at a discount.

Medical transportation plays a critical and necessary role in the healthcare industry. Arrangements for medical transportation services can be extremely complex. VMG Health has extensive experience valuing payments for all kinds of medical transport arrangements and understands the numerous risks associated with these types of valuations, which helps clients enter arrangements compliant with FMV.

Proceed with Caution: Five Key Considerations in Quality of Revenue Analysis

March 20, 2024

Written by Melissa Hoelting, CPA and Lukas Recio, CPA

In healthcare-related mergers and acquisitions (M&A), quality of revenue analysis represents both the most vital piece of due diligence and its most unique aspect given the nature of healthcare revenue. For many transactions, buyers rely on due diligence advisors to provide independent net revenue hindsight analyses to facilitate valuation efforts, such as growth potential, risk analysis, and financial stability. Quality of revenue analysis becomes even more crucial in healthcare transactions due to the added complexity of payor contracting and unique reimbursement mechanisms by vertical. Due to this complexity, investors and advisors need to know the key indicators that arise in quality of revenue analysis to address the issues and properly assess the merits of the transaction. In this article, our financial due diligence team previews five key considerations:

1. Payor Concentration

When revenues are concentrated with a select few payors, there is potential for future revenue loss from either unfavorable reimbursement rate changes or the loss of in-network status. Even minor changes in reimbursement rates may have a material impact on top-line revenue when applied to key groups. A key consideration when evaluating payor concentration comes from a large reliance on government payors, as the rates can change year to year without the company’s input or control. Payor concentration in and of itself will not impact the revenue hindsight analysis, as collections for previous dates of service will follow the current contracts, but investors and their advisors should make it a priority to understand the payor mix to properly identify and assess the inherent risks. Additionally, any upcoming contract negotiations should be discussed to evaluate the potential near-term impact of negative price adjustments to make necessary pro forma/forecasting assumptions.

2. Increasing Days Sales Outstanding (DSO)

Aging accounts receivable balances indicate difficulties in the billing and/or collection process, which directly impact the company’s cash flows and the reliability of reported revenues for companies on an accrual basis. Increasing DSO could be the result of certain non-recurring events, such as the loss of key personnel in the billing department or converting revenue cycle management systems, or may be indicative of deeper issues at play within the company. In the case of third-party payors, increased DSO could point to two potential issues:

Disputes with payors, or

Insufficient collections of copays, coinsurance, or deductibles. If it is discovered that increased DSO for certain third-party payors stems from remaining patient responsibility, the company could be under-collecting copays, coinsurance, and deductibles at the time of service. This misstep in the collection process can leave a company exposed to an accounts receivable balance overly weighted toward patient balances, which can be more difficult to collect.

Regardless of the payor type exhibiting increased DSO, decrease in collection speed should always alert the investment team that more analysis and discussion is required to properly determine the collectability of accounts receivable, and thus, the revenue accruals themselves.

3. Reconciliation Irregularities

Revenue analysis fundamentally begins with a reconciliation of the payment data to the bank statements to anchor the data to verifiable cash inflows. Variances between collections from the billing system and bank statement deposits could indicate that the company does not deposit all collections, certain revenue streams do not run through the billing system, or there are significant delays in posting cash receipts to the billing system. By comparing the reported revenue to the bank statements, teams can identify overstatements of revenue that are not supported by bank deposits. Regardless of the variance’s cause, any discrepancies should be investigated and discussed with management to ensure data completeness and integrity before using the billing system reports for any revenue analysis.

4. Variability in Gross-to-Net Ratios

An entity’s gross-to-net ratios (net collections as a percentage of total gross charges) often highlight changes in underlying processes or outcomes for a given period of service; therefore, they are a key consideration during the due diligence process. Effective gross-to-net ratio analysis starts at the lowest level, such as by CPT code by payor. Significant variations at this level from month to month or quarter to quarter may indicate rate changes, an altered chargemaster, or increased/decreased denial activity. At a less detailed level, changes in this ratio may also illustrate changes in payor mix or procedure mix. In any case, the underlying drivers must be identified and their impact to future cash flows assessed to determine the true quality of the underlying revenue streams.

5. Billing and Coding Irregularities

A foundational component in the revenue recognition process, the billing and coding process can be the area most susceptible to downside surprise. Investors and their advisors should focus on CPT code-level trending to determine key metrics, such as payment per code and code distribution. By comparing these metrics to contracted rates and industry or specialty norms, irregularities in coding practice can be identified and investigated. For example, if an organization has higher concentration in level one or level five evaluation and management codes, it could indicate consistent undercoding to avoid payor scrutiny or overcoding for work performed, respectively. On a similar note, if an organization receives similar reimbursement on office visit codes for a doctor and a mid-level provider, it could indicate that the billing team is not coding and charging the proper rates. Identified irregularities in the coding metrics should be discussed in detail, as inappropriate coding can result in downward adjustments to both historical collections and any outstanding collections, as well as takebacks owed to insurance companies for prior periods.

Conclusion

For any healthcare transaction, revenue analysis remains the most essential and most complicated part of the diligence process. Because of the payor contracts that underpin most healthcare revenues, investment teams must identify any variances in reimbursement, charges, and coding that could indicate errors or changes in the billing process. When considering adjustments or estimating future collections, teams must consider the changes and errors they have identified through these variances. These five considerations represent just a portion of the potential intricacies and issues that arise during quality of revenue analysis. Thus, an organization looking to enter into a transaction, whether on the buy-side or the sell-side, would benefit from the services of a financial due diligence and/or coding and compliance firm to bring an additional layer of confidence to the target’s revenues.

Supply-Side Constraints and Operational Headwinds in Skilled Nursing Valuation

March 19, 2024

Written by Grace McWatters, Danny Cuellar, Carlos Flores-Rodriguez, Blake Pierro, and Cameron Tolbert

Inflation, a shaky supply chain, and rate hikes have extended production schedules and increased the cost and risk associated with developing new skilled nursing facilities. While new supply is constrained, existing nursing facilities grapple with staffing shortages and weak reimbursements. Despite positive chatter about recovering occupancy, rent growth, and a looming “silver tsunami” of retirees, the industry sits in a precarious position.

The inflated cost to build, buy, and operate skilled nursing facilities has led to a downward pressure on valuations. This affects the risk profile of the sector, both from a regulatory risk perspective (in the context of joint ventures or lease renewals, for instance) and from an underwriting or acquisition/disposition perspective (due to the elevated cost of debt combined with rising operating costs).

Strong Demand, Weak Performance

Strong demand for skilled nursing facilities is primarily driven by an aging populace in the United States; over the next 10 years, the 75+ population is projected to grow by 44%. According to research funded by the National Investment Center for Seniors Housing & Care, 60% of this population will have mobility limitations, with 20% requiring high healthcare or functional needs.

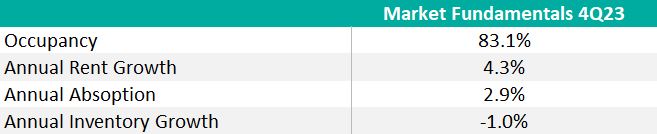

Cushman and Wakefield predict consumer demand for senior housing and care facilities, including independent living, assisted living, memory care, and skilled nursing, will overwhelm the market within the next five years. It would take approximately 3,100 new skilled nursing facilities by 2030, or about 500 net openings annually, to meet the forecasted need. Despite robust demand, skilled nursing inventory fell 1% in 2023.

Over the last year, closures continually outpaced openings as financial pressures from inflation, poor reimbursement rates, and staffing shortages led to industry-wide “right sizing” to control cost and mitigate labor shortages. For example, in 2022 and 2023 when labor shortages became a flashpoint, operators, bound by minimum staffing requirements, had to consider contract labor. The contract nursing labor utilization increased 56% in 2022, which “equates to approximately $400,000 in additional costs for the average facility in the country.” Average overall nursing wages increased 10.6% in 2022, a much faster clip than revenue growth.

These cost surges came at a price, and without a mechanism to raise prices, taking beds offline was often inevitable. The American Health Care Association surveyed thousands of skilled nursing facilities in an August 2023 report and found that 21% of homes are downsizing beds or units, and 24% have closed a wing, unit, or floor because of the labor shortages.

Since 2020, an estimated 579 facilities have closed (approximately 162 per year, over the 43-month period), and 38% of these closures were 4- or 5-star rated facilities. Only three skilled nursing facilities opened in 2023, down significantly from an average of 64 openings in both 2020 and 2022.

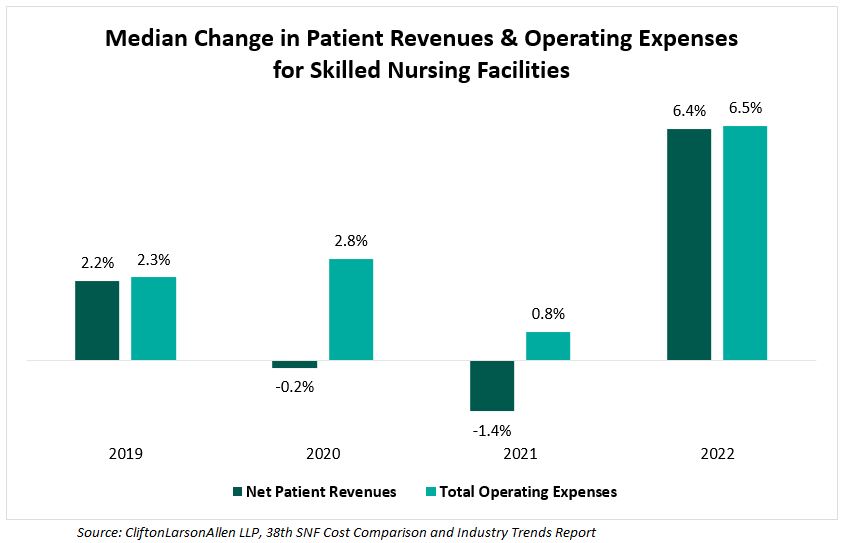

The tight supply has supported rent growth and occupancy recovery across the industry, but these gains have been outpaced by increased costs for staffing and supplies, exacerbating structural forces specific to the industry. From 2019 to 2022, Clifton Allen Larson analyzed cost reports for 10,500 facilities (nearly two-thirds of all Medicare-certified SNFs in the country) and found that expenses have consistently grown faster than revenues.

Operating expense growth in other industries can be mitigated by “shrinkflation” or higher prices, but in healthcare, providers cannot ethically reduce the amount of care administered, nor can they regularly renegotiate their contracts and expect immediate increases in Medicare reimbursements.

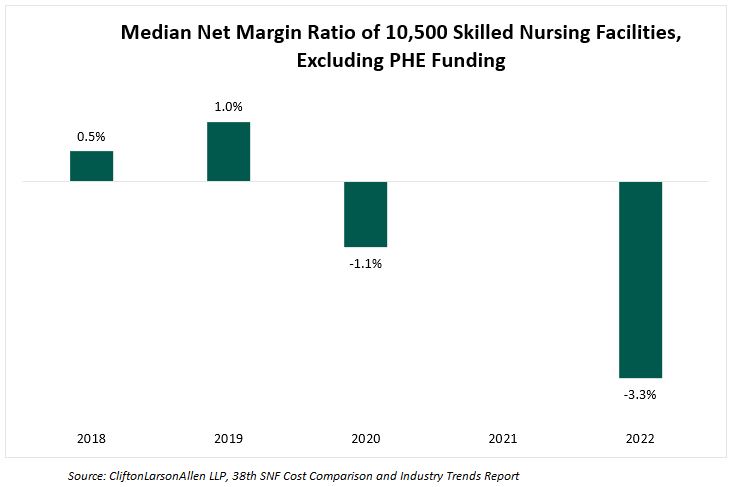

In 2023, Clifton Larson Allen analyzed cost reports of 10,500 nursing facilities and found a significant downward trend in the median net margin ratio since 2020. This ratio measures a facility’s efficiency in controlling costs in relation to its total revenue by comparing net income or loss to total revenue.

Heightened Risk, Lower Reward

Construction for new facilities has dwindled since 2020, as high interest rates and inflation have developers wary. Costs are rising, but market valuations have not necessarily followed, which means developers would take on more risk for potentially less reward. These factors have decreased the overall incentive for developers to initiate new projects. When analyzing the all-in construction costs of 142 senior housing developments in 2022, CBRE reported the average cost had increased 17.8% per unit since 2020, clarifying that this increase “is largely attributable to higher labor and materials costs, as well as operating expenses and outlays for entitlements.”

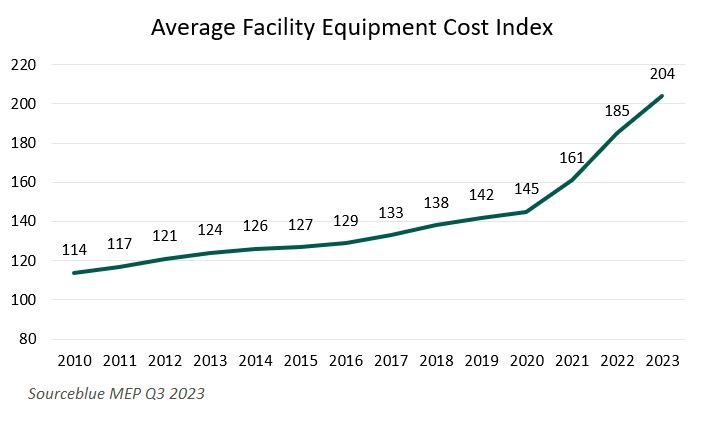

This is mostly attributable to hard cost increases, but there were significant increases in soft costs and FF&E costs as well. Hard costs, which include site work, foundation, shell, and finishes, increased 24% per revenue unit (i.e., per bed) since 2020. Soft costs, which can cover architect and design fees, permitting and inspection fees, rose 14% per unit, and FF&E bumped up 10% per unit . Similarly, an index based primarily on mechanical and electrical equipment in new construction showed a significant uptick in their average cost in 2022 (increased by 15.1%) and 2023 (increased by 10.4%).

While FF&E represents a small part of the overall senior care development budget (CBRE estimates 3% overall) , any transactions and leases involving FF&E at senior living and care facilities are subject to regulatory scrutiny, just like real property.

Those willing to take the risk of building a new facility find it difficult to acquire capital in the wake of rate hikes and bank failures in the broader economy. A significant amount of funding for the purchase of senior living and care assets originates from commercial bank loans, but lending grew scarce following the failings of Silicon Valley Bank and Signature Bank in March 2023.

As other banks teetered on the edge of bankruptcy and commercial bank stocks dropped up to 50%, banks began to stop the flow of lending, and instead focused on cleaning up their balance sheets. Preserving limited capital, banks began to raise interest rates and stiffen security terms for available loans. This folded into rising rates on a larger macroeconomic scale, as the Federal Reserve hiked their rates to curb inflation, increasing interest rates by 525 basis points in 2022 and 2023.

Higher interest rates lend themselves to higher projected operating costs of acquired facilities. This increase in operating costs has been offset by a substantial decrease in purchasing prices. Cain Brothers reported a 20–30% decrease in skilled nursing facility valuations since the beginning of 2023, citing several deals in their report, including a New York facility that declined in value 47% in less than two years, and a Kentucky facility that dropped 28% in less than one year. Haven Senior Investments notes valuation declines between 15% and 30% but emphasizes the influence of factors like rising property taxes and insurance premiums, as well as the portfolio penalty.

Regulatory Implications

The inflationary environment combined with longer-term industry headwinds continue to place pressure on the senior living and skilled nursing industry. Over the last two years, the cost of capital has increased, and commercial loans have become less available, making it more expensive and time consuming to acquire the funds necessary for new developments or strategic acquisitions. Operating costs continue to outpace revenue growth, and the median net margin ratio for two-thirds of the country’s facilities was negative 3.3% in 2022. This environment has contributed to rising capitalization rates and downward pressure on valuations.

The decline in skilled nursing facility valuations has increased the industry’s risk profile, both from a regulatory risk perspective and from an underwriting or acquisition/disposition perspective. The turbulent market conditions over the last 18 months have created a need for increased diligence when developing, buying, or selling senior living assets. However, long-term demographic trends will continue to drive transaction activity in the sector, as market participants seek solutions to address demand in the face of rising costs and increased cost of capital.

Sources

Beets, K., Ferroni, L. (2024). Seniors Housing & Care Investor Survey and Trends. JLL. https://www.us.jll.com/en/trends-and-insights/research/seniors-housing-care-investor-survey-and-trend-outlook

Pearson, C., et. al. (2019). The Forgotten Middle: Many Middle-Income Seniors Will Have Insufficient Resources For Housing And Health Care. HealthAffairs. https://www.healthaffairs.org/doi/full/10.1377/hlthaff.2018.05233

Boywer, Z. (2023). Investor Survey and Trends Report: U.S. Senior Living & Care. Cushman & Wakefield. https://www.cushmanwakefield.com/en/united-states/insights/senior-living-and-care-investor-survey-and-trends-report

Shuman, T. (2023). How Will America’s “Silver Tsunami” Impact Demand for Nursing Homes? Seniorliving.org. https://www.seniorliving.org/nursing-homes/nursing-home-demand-projections/

Vison, N. (2024). 4Q23 Market Fundamentals. NIC MAP Vision. https://info.nicmapvision.com/rs/016-QJL-848/images/4Q23-NIC-MAP-Market-Fundamentals-PDF.pdf

Connect, C. (2024). 38th SNF Cost Comparison and Industry Trends Report: One Industry, Thousands of Stories. CLA. https://www.claconnect.com/en/resources/white-papers/snf-cost-comparison-industry-trends-report

Vance, M., et. al. (2022). 2022 Seniors Housing Development Costs. Intelligent Investment. https://www.cbre.com/insights/reports/2022-seniors-housing-development-costs

SourceBlue. (2023). 2023 MEP Cost Index Q4. https://media.licdn.com/dms/document/media/D4E1FAQFQj5FKBkLXVg/feedshare-document-pdf-analyzed/0/1705173887049?e=1711584000&v=beta&t=FlP19mqHb4j8iSVBePK8gHaWLHauSTUgdorcMH2TTlg

Goldreich, M. (2023). 2023 Debt Capital Markets Impact on Senior Living Asset Valuation. Cain Brothers Industry Insights. https://www.key.com/content/dam/kco/documents/businesses___institutions/Industry_Insights_11.15.23.pdf

Investments, H. (2023). The Present and Future of Senior Living Sector Acquisitions. Haven Senior Investments. https://havenseniorinvestments.com/downloadable/the-present-and-future-of-senior-living-sector-acquisitions/

MAT Clinics: At the Nexus of Healthcare Expansion and Investment

March 14, 2024

Written by William Teague, CFA; Justin Vachon; and Ash Midyett, CFA

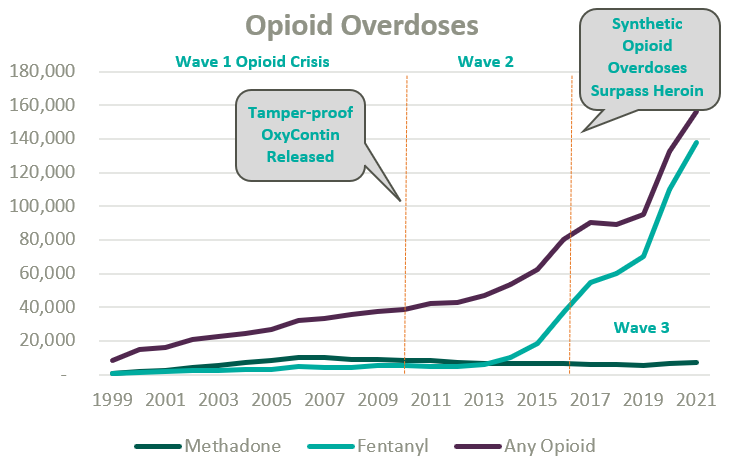

Since the start of the opioid epidemic in the late 1990s, over one million overdoses have been recorded. This figure continues to climb at an accelerated rate following the COVID-19 pandemic and the proliferation of fentanyl. Since 2020, opioid overdoses increased 64%, prompting lawmakers and regulators alike to initiate widespread deregulation and funding of Medication Assisted Treatment (MAT) for Opioid Use Disorder (OUD) to increase access to care amidst what is widely considered a national crisis.1

Medication-assisted treatment (MAT) is a primary method for treating opioid use disorder (OUD) and integrates prescription opioid agonists, which can help manage cravings and withdrawal symptoms, with comprehensive care. Typically, this care combines prescription medications with behavioral health and occupational therapy, drug screenings and occupation advocacy, and other counseling services. MAT can widely be categorized as formal opioid treatment programs (OTPs) and less formalized office-based opioid treatment programs.

OTPs were first established in the mid-1960s from the established medical community’s reluctance to treat the stigmatized patient group and unwillingness to prescribe opioid drugs to those suffering from OUD. Traditionally, OTPs have relied on Methadone, a synthetic analgesic drug similar to morphine, to ease opioid withdrawal symptoms while patients simultaneously attended mental health and occupational counseling.

Office-based opioid treatment (OBOT) refers to outpatient treatment services provided outside of licensed OTPs by clinicians. OBOT treatment allows patients to obtain care at the convenience of their typical primary care provider or local healthcare facilities and does not require comprehensive behavioral health services to be integrated into the delivery model.

Methadone treatment remains the preferred drug type for high-acuity addiction and can be prescribed by a physician, physician’s assistant, nurse practitioner, or clinical nurse specialists, and is typically administered daily through a liquid shot and occasionally as a pill. After a detoxification process at progressive dosing, the patient’s response is typically monitored through a series of physicals. Afterward, maintenance dosages are prescribed on a daily frequency for a recommended one-year period. Methadone may only be distributed through a SAMHSA-certified and DEA-registered OTP clinics.

Since its initial approval by the FDA in 2002, Buprenorphine, a partial opioid agonist, is increasingly relied upon within the OTP and OBOT settings for OUD detoxification and maintenance for less acute addiction. As a partial opioid agonist, Buprenorphine has a lower risk profile than methadone and is thus more widely accessible. For instance, while Methadone may only be distributed in an OTP setting, Buprenorphine can be distributed in an OBOT setting. By market share, Buprenorphine currently dwarfs similar medications for opioid use disorder.2

New OUD Treatment Regulations to Expand Access

Because opioid agonists are inherently prone to abuse, regulation of MAT has been historically stringent to prevent further misuse or illicit trade. All OTPs are required to receive full certification by the Substance Abuse and Mental Health Services Administration (SAMHSA), and many states require a Certificate of Need. SAMHSA also regulates prescription protocols and procedures.

On January 31, 2024, SAMHSA made the most impactful change to MAT regulation in decades by finalizing recommendations initiated during the COVID-19 pandemic.3 Most notably, SAMHSA eliminated the one-year OUD qualification and further expanded eligibility for Methadone take-home doses. Additionally, guideline updates granted permanent approval for Buprenorphine telehealth induction without an in-person exam, expanded the definition of “practitioner,” and eliminated the X-waiver requirement, which formerly authorized the outpatient use of Buprenorphine and stipulated patient caps per prescriber.

Market Growth and Transaction Activity

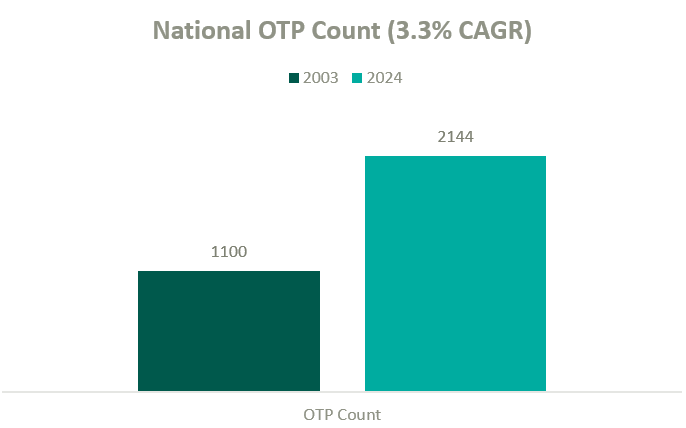

According to the Opioid Treatment Program Directory, patient demand in conjunction with deregulation and clinical advocacy has resulted in a near doubling of OTP clinics nationally over the past two decades. As federal funding and popular outcry grows, OTP growth continues to gain momentum.

The growth in OTPs over the past two decades has resulted in a highly fragmented industry where several notable players hold significant leverage in what will likely become a consolidating market. There are many examples of private equity (PE)–backed companies beginning to participate in merger and acquisition activity in the MAT space.

BayMark Health Services, backed by Webster Equity Partners, claims to be the largest provider of MAT services in North America. BayMark, with over 280 facilities in North America, has acquired over a dozen facilities since the pandemic throughout the U.S.

Acadia Healthcare is the largest publicly traded behavioral health provider in the United States and maintains a significant focus on opioid use disorder. Recent comments from Acadia’s CEO, Chris Hunter, chart an ambitious acquisition strategy to acquire 14 OTPs in fiscal year 2024 after kicking off the year with two MAT acquisitions in North Carolina.4

Key players in the behavioral health industry that are building a presence in the MAT space include, but are not limited to, the following:

Other notable behavioral healthcare providers growing their presence in the industry’s substance use disorder (SUD) and MAT sub-sector include Acadia Health and Universal Health Systems. However, it’s difficult to determine how many stand-alone MAT clinics they have in operation from publicly available information.

Based on data from Irving Levin Associates, Inc., SUD transaction activity has grown significantly over the past decade while having receded marginally from pandemic highs.

MAT Reimbursement Landscape

MAT clinics operate with a unique reimbursement model compared to other healthcare sectors, and OTPs specifically bill under a set of HCPCS G-Codes. Upon admittance, new patients are billed under an intake code while maintenance visits are reimbursed by the Centers for Medicare & Medicaid Services with bundled payments based on weekly episodes of care.

The table below outlines frequently utilized HCPCS G-Codes for OTP services:

HCPCS Code

Description of Services

G2076

Intake activities, including medical exam, physical evaluation, initial assessment, and preparation of comprehensive treatment plan.

G2067

Weekly bundle for medication assisted treatment (Methadone). Includes the drug itself, administration, substance use counseling, therapy, and toxicology testing.

G2068

Weekly bundle for medication assisted treatment (Buprenorphine, oral). Includes the drug itself, administration, substance use counseling, therapy, and toxicology testing.

G2078

7-day, take-home supply of Methadone

G2079

7-day, take-home supply of Buprenorphine

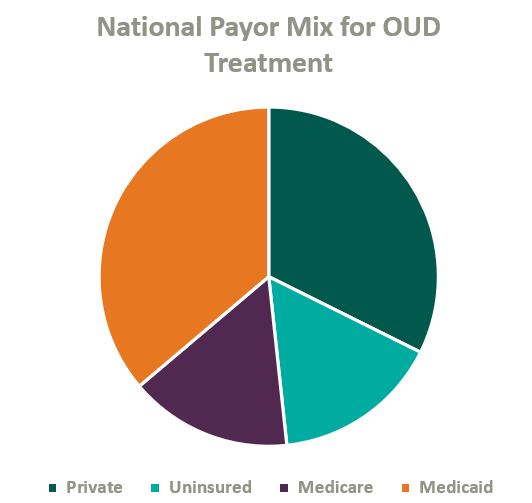

Over the past two decades, Congress has made strides to expand public and private insurance coverage for MAT care. According to the National Survey on Drug Use and Health, roughly 84% of those who suffer from OUD in the United States are covered by some form of insurance (see chart below for total payor mix). Nonetheless, out-of-pocket expense for OUD treatment remains prohibitively expensive for many patients, and sporadic and disparate coverage discourages many operators from accepting insurance. This may change as Congress continues to pass legislation improving affordability of OUD treatment.

On January 1, 2020, Congress passed the SUPPORT Act,5 which established a new Medicare Part B benefit for OUD treatment services provided by OTPs and mandated that all states cover OTP services in their Medicaid programs effective October 1, 2020.6

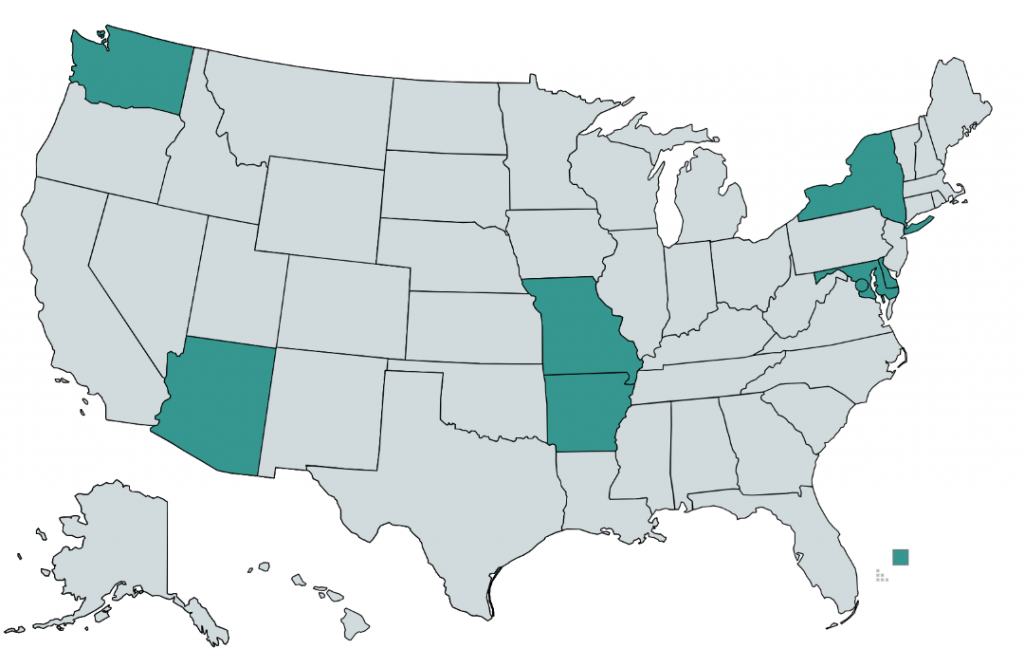

As of 2020, only eight states and the District of Columbia require commercial insurers to provide coverage of medications for opioid use disorder (see map below).7 Although many plans provide coverage regardless of state requirements, coverage is often restricted to a provider network or limited to a cap on services and many MAT clinics choose to pursue an out-of-network or self-pay strategy.8

States That Require Commercial Insurers to Cover OUD Medication

Grant revenue is critical in lowering out-of-pocket costs for OUD patients and can play a significant role in the operational sustainability of MAT clinics. In 2017, the U.S. Department of Health and Human Serviced committed $485 million in grants to be distributed through SAMSHA, which is intended to increase access for patients, bolster existing MAT operations, and catalyze continued facility expansion.

Conclusion

As access and reimbursement for OUD treatment expands, we expect the supply of care to continue to lag demand for the foreseeable future. In addition, we expect PE-backed platforms to continue consolidating the fragmented industry, driving transaction activity. We also anticipate federal funding, patient inelasticity, and a lack of competition within many markets to fortify pricing while demand continues to attract practitioners into the market—ultimately incentivizing further industry growth and higher valuations.

Update (April 23, 2024): On April 23, 3034 the Federal Trade Commission issued a final rule to generally ban non-compete clauses for most workers. According to the FTC, the final rule will become effective 120 days after publication in the Federal Register.

On January 5, 2023, the Federal Trade Commission (FTC) indicated that it would be proposing a rule to ban non-compete clauses.

Non-compete clauses are industry agnostic and cover a wide gamut of professions. The purpose of a non-compete is to protect the employer’s interest when hiring new employees. The non-compete inhibits an employee from opening a competing business or joining a competing firm within a certain geographical distance and for a certain period. The FTC argues that, in addition to inhibiting competition, non-compete clauses also lower wages for workers who are subject to them as well as workers who are not. The FTC has provisioned an exception to this ban, which would be applicable in the sale of a business where the person subject to a non-compete has an ownership interest of at least 25%.

Within the healthcare industry, physician non-competes are common and often accompany an employment agreement. Whether large health systems or smaller physician groups, many providers are subject to non-competes when employed by these entities. For example, if a physician owner hires two other providers to operate out of her practice, those two physicians may be subject to non-compete agreements. In hiring and training the two new providers, the physician owner may use her eminence in the marketplace, time, patient contacts, and resources to establish the two new providers in the market. Without a non-compete, those two new physicians would be able to join any competing practice nearby to the detriment of their first employer. This problem may become cyclical. The practice that hired those physicians would also be subject to the same risk and, without non-compete agreements, may see those same physicians leave to another competing practice around the corner. VMG Health has been engaged in various situations to determine the value of buying out a non-compete for either litigated matters or transactional matters.

It is important to note, however, that as health systems expand and more physicians are employed by those health systems, it becomes more difficult for physicians to practice out of the geographic limitations set forth by the non-compete if they do choose to leave their employer.

Following this announcement by the FTC, some states have begun moving legislature regarding non-competes. Recently, in January 2024, New York Governor Kathy Hochul vetoed a similar proposal to ban non-competes. Delaware Supreme Court recently ruled in favor of holding non-competes in place in a ruling regarding a financial services company. For example, in California, Oklahoma and North Dakota, non-competes are either not enforceable or outright banned.

The American Medical Association (AMA) echoed the limitations of non-competes noted by the FTC. The AMA supports any policy that would “prohibit covenants not-to-compete for all physicians in clinical practice.”1 The case could also be made for the removal of non-compete agreements due to the current provider shortage around the country.

In drafting non-compete agreements, employers may consider a liquidated damages provision in anticipation of damages. This provision could speak to a reasonable buy-out requirement for a physician seeking to leave and compete nearby. Given the complexities of valuing the buy-out of a non-compete, it is important to engage an expert who understands certain key components: the term of the non-compete, enforceability of the non-compete, the market and competitive landscape, and the financial impact of potential competition.

Across its client base, VMG Health has been engaged to quantify any damages resulting from a client’s workforce leaving for a competitor or to form their own business entity to then compete with their prior employer in the same geographical area. In situations like these, VMG Health has been engaged to determine the value of a non-compete for a litigated matter or for transactional purposes.

It is important to note that the enforceability of physician non-compete agreements can vary depending on the specific language of the agreement, the jurisdiction in which the case is heard, and the facts and circumstances of the case. If you are facing a legal issue related to a physician non-compete agreement, it is imperative to seek legal advice from a qualified attorney and valuation expert who can provide you with personalized guidance based on your situation.

Public Sector Predictions for Healthcare Utilization in 2024

March 5, 2024

Written by Jordan Tussy, Colin McDermott, and Madi Whyde

Contributing researchers: Bill Jordan, Ryan Mendez, Molly Smith, Rashika Tomar, and Michael Welcer

The public sector often provides valuable insights on broader industry trends, which may be particularly helpful for the private sector in planning for the 2024 calendar year and beyond. VMG Health has identified a select number of companies that operate within the healthcare sector and reviewed the latest earnings calls to develop an understanding of how recent financial and operational trends may provide an indication of future utilization. Identified companies include distributors, equipment suppliers, facility operators, and managed care organizations, all of which are integral in the deployment of healthcare services in the United States and deeply invested in the underlying drivers of future utilization.

We have included some of the most interesting statements made by the leaders of these organizations below.

For medical equipment suppliers and distributors, 2024 predictions were primarily driven by 2023’s utilization, with many companies reporting continued growth over 2023 due to persisting patient backlogs.

“…Average system utilization [procedures per installed clinical system] continues to be above long-term trends, increasing by 9.0% for the full year of 2023. Higher system utilization reflects both a higher mix of shorter-duration, benign procedures and the need to address patient backlogs.” – Jamie E. Samath, Senior Vice President and Chief Financial Officer, Intuitive Surgical, Inc. FQ4 Earnings Call, January 23, 2024.

“During the quarter, we saw strong procedural demand… Additionally, demand for our capital products remained very robust in the quarter, with double-digit organic growth in Medical, Instruments and Endoscopy.” – Jason Beach, Vice President of Investor Relations, Stryker Corporation. FQ4 2023 Earnings Call, January 30, 2024.

“Second quarter revenue increased 3.0% to $3.9 billion, which, as Jason alluded to, reflects quarterly revenue growth for the Medical segment for the first time in over two years. This increase was driven by growth in both at-home solutions and global medical products and distribution…” – Aaron E. Alt, Chief Financial Officer, Cardinal Health, Inc. FQ2 2024 Earnings Call, February 1, 2024.

“There is a bolus of patients coming out into the market after COVID-19, which has made 2023 market growth faster than historical averages.” – Joaquin Duato, Chief Executive Officer and Chairman, Johnson & Johnson. FQ4 2023 Earnings Call, January 23, 2024.

As key customers of medical equipment suppliers and distributors, healthcare operators mirrored their observations of continued growth in utilization, particularly in the fourth quarter of 2023.

“But at a structural level, there is nothing to suggest that our surgical volume trends are going to change for the year, we had really solid volume growth in surgery. And we continue to invest heavily in our programs, both on the outpatient side and supporting our inpatient activity with more acute in complex program offerings.” – Samuel N. Hazen, Chief Executive Officer and Director, HCA Healthcare, Inc. FQ4 2023 Earnings Call, January 30, 2024.

“We finished the year strong and delivered results in the fourth quarter that were well above the expectations we set. This was driven by continued volume strength as well as cost and utilization management.” – Saum Sutaria, Chairman and Chief Executive Officer, Tenet Healthcare Corporation. FQ4 2023 Earnings Call, February 8, 2024.

These companies were also consistent in crediting the elevated utilization trends to volume growth in a few key specialties.

“As we have noted, we believe that in 2023, we saw recovery in demand that included some impact from deferred volume, particularly in GI and ENT services. – Saum Sutaria, Chief Executive Officer, Tenet Healthcare Corporation. FQ4 2023 Earnings Call, February 8, 2024.

“Throughout the year, we saw ongoing strength and recovery in GI, urology and ENT procedures. This organic growth was driven by continued expansion of service lines and growth in our population of partnered and affiliated physicians as well as the fundamental tailwinds of patient demand for safe and convenient surgical care options.” – Saum Sutaria, Chief Executive Officer, Tenet Healthcare Corporation. FQ4 2023 Earnings Call, February 8, 2024.

“Starting first with procedures, growth for the full year was 22.0%. Areas of strength included general surgery in the United States… In the U.S., general surgery procedure growth was led by cholecystectomy, with foregut procedures rising as well. Colon and hernia procedure growth was also healthy for the year. Bariatric procedures grew year-over-year.” – GaryS. Guthart, Chief Executive Officer and Director, Intuitive Surgical, Inc. FQ4 2023 Earnings Call, January 23, 2024.

While volume recovery resulted in top line revenue growth for operators and their vendors, payors expressed higher-than-expected medical costs driven by the strong utilization.

“…In the non-inpatient space, despite the recent decline in observation events, we saw a sequential uptick in overall medical cost per member per month (PMPM) in the fourth quarter, driven largely by increases in physician, outpatient surgical and supplemental benefits cost categories.” – Humana Inc. Fourth Quarter 2023 Prepared Management Remarks, January 25, 2024.

“Care patterns remain consistent with those we shared with you in the first half of ‘23. Activity levels continue to be led by outpatient care for seniors—with orthopedic and cardiac procedure categories among the more prominent. As we’ve noted, our benefit design approachassumed these activity levels persist throughout ’24, and the care patterns we observed exiting ’23 reconfirm that decision.” – John Rex, Chief Financial Officer, UnitedHealth Group. FQ4 2023 Earnings Call, January 12, 2024.

2024 Expectations

The companies were nearly unanimous in their expectations that 2023 growth trends will persist throughout 2024, driven by the elevated backlogs, stabilizing macroeconomic trends, and an aging population.

Healthcare Manufacturers and Distributers

“We project MedTech operational sales growth to be relatively consistent throughout the year, expecting procedures in 2024 to remain above pre-COVID levels.” – Joseph J. Wolk, Executive Vice President and Chief Financial Officer, Johnson & Johnson. FQ4 2023 Earnings Call, January 23, 2024.

“And we see that trend [faster market growth post-COVID] continuing into a good part of 2024. And therefore, being a tailwind into 2024. There’s a lot of factors playing into that. But overall, we see the amended procedures continuing into, at least, the first half of 2024.” – Joaquin Duato, Chief Executive Officer and Chairman, Johnson & Johnson. FQ4 2023 Earnings Call, January 23, 2024.

“…We continue to see an increased volume of procedures in orthopedics based on coming out of COVID. And we don’t see any change in that, neither in the hips or in the knee area, or in any of the segments that we compete. So, we are optimistic about our orthopedics trajectory.” – Joaquin Duato, Chief Executive Officer and Chairman, Johnson & Johnson. FQ4 2023 Earnings Call, January 23, 2024.

“So, embedded in the guidance for 2024, which we’re very confident on the 5.0% to 6.0%, is macro and micro reasons. So, from a macro perspective… the markets are going to continue to be healthy. You got better patient demographics, younger patients, you got the dynamic of cases moving into an ASC… You’ve seen shorter, better rehabilitation processes.” – Ivan Tornos, Chief Operating Officer, President, Chief Executive Officer, and Director, Zimmer Biomet Holdings, Inc. FQ4 2023 Earnings Call, February 8, 2024.

“The size of our pipeline is twice what it used to be in 2018… This is not the same market growth profile that we used to have. Patient demand is strong. Procedure volume is very strong given a variety of reasons.” – Ivan Tornos, Chief Operating Officer, President, Chief Executive Officer, and Director, Zimmer Biomet Holdings, Inc. FQ4 2023 Earnings Call, February 8, 2024.

“Procedure volumes are strong. The capital markets are very strong. Hospitals are spending. We have exited the year with more backlog than we began the year, which means, obviously, our orders are continuing to be strong for capital equipment.” – Kevin A. Lobo, Chairman, Chief Executive Officer, and President, Stryker Corporation. FQ4 2023 Earnings Call, January 30, 2024.

“We continue to expect the ortho markets will remain strong in 2024, driven by continued adoption in robotic-assisted surgery, demographics, a more favorable pricing environment, and healthy patient activity levels with surgeons… Hospital CAPEX budgets remain healthy, and our capital order book remains elevated as we enter 2024.” – Jason Beach, Vice President of Investor Relations, Stryker Corporation. FQ4 2023 Earnings Call, January 30, 2024.

“Based on our momentum from 2023, strong procedural volumes, healthy demand for capital products, and a stabilizing macro-economic environment, we expect 2024 organic net sales growth to be in the range of 7.5% to 9.0%.” – Glenn S. Boehnlein, Vice President and Chief Financial Officer, Stryker Corporation. FQ4 2023 Earnings Call, January 30, 2024.

“…Our overall procedure guidance range assumes that growth moderates from last year, given the elevated backlog benefit we experienced in 2023.” – Brian King, Head of Investor Relations, Intuitive Surgical, Inc. FQ4 2023 Earnings Call, January 23, 2024.

“…Utilization continues to be quite good and predictable. So, we’re in a nice environment for ongoing growth…” – Jason M. Hollar, Chief Executive Officer and Director, Cardinal Health, Inc. FQ2 2024 Earnings Call, February 1, 2024.

Healthcare Operators

“The volume strength was also very good during the year. And so, I think that we believe that we’ll continue to see acute care recovery in 2024 like we saw in 2023. And if we’re able to open up capacity effectively to service the demand that we want, which again is consistent with our high acuity strategy, I think that’s what gets us to the upper end of our guidance, right? It’s really the volume potential there.” – Saum Sutaria, Chief Executive Officer, Tenet Healthcare Corporation. FQ4 2023 Earnings Call, February 8, 2024.

“…I think we’re reading continued strong demand. We saw really strong enrollment in the health insurance exchanges across our states… We believe we continue to see strong economic indicators and employments and our access to contracted lives remaining well.” – William B. Rutherford Executive VP and Chief Financial Officer, HCA Healthcare. FQ4 2023 Earnings Call, January 30, 2023.

“…We are really judging our business and thinking about 2024 optimistically around where the demand for healthcare is at least in our markets.” – Samuel N. Hazen, CEO and Director, HCA Healthcare. FQ4 2023 Earnings Call, January 30, 2023.

“Our initial assumption for volume growth assumes that volume will build as the year progresses, reflecting the historically high same-store case growth that we saw in the first quarter of 2023. We are very confident in the long-term growth rates of this business.” – Saum Sutaria, Chief Executive Officer, Tenet Healthcare Corporation. FQ4 2023 Earnings Call, February 8, 2024.

Managed Care

“Given the recency and magnitude of the uptick in the utilization trend, we have prudently assumed that the higher costs seen in the fourth quarter persist throughout 2024. Based on our review of our initial claims data, we believe that the seasonal factors are not driving the increase.” – Bruce Dale Broussard, Chief Executive Officer and Director, Humana Inc. FQ4 2023 Earnings Call, January 25, 2024.

“Looking at January data, which is very early—so we only have really some look into the first two weeks—we would say [utilization] is continuing to stay at the elevated levels that we saw in the fourth quarter.” – Susan Marie Diamond, Chief Financial Officer, Humana Inc.FQ4 2023 Earnings Call, January 25, 2024.

Conclusion

The prevailing theme noted in the earnings calls VMG Health reviewed pertained to the elevated utilization in 2023 and its persistence into 2024. Particularly notable were the trends around volumes recovering post-COVID (especially for otolaryngology, orthopedics, and urology services). This was coupled with a recovering macroeconomic environment and favorable patient dynamics. While an encouraging trend for operators, device companies and distributors, higher utilization translated to increased medical claims on the payor side.

Based on this commentary and insight from the public sector, the VMG Health team is optimistic that 2024 will be a strong utilization year for our healthcare service provider clients.